On August 27, 2025, the 19th Frost & Sullivan Global Growth, Innovation and Leadership Summit & 4th New Investment Conference (referred to as '2025 Frost & Sullivan New Investment Conference' or 'Conference') hosted by Frost & Sullivan was grandly inaugurated at the Shangri-La Shanghai Jing'an Hotel.

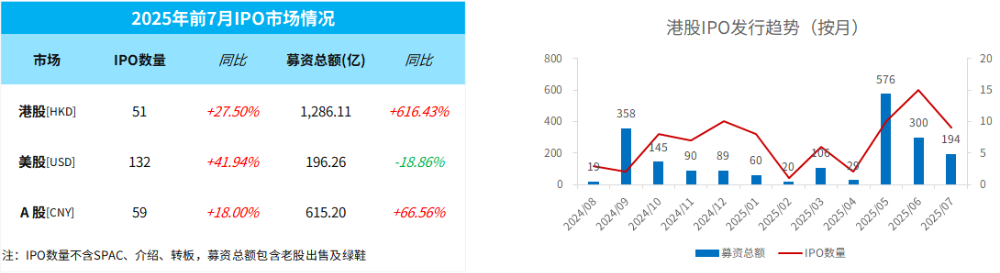

Hong Kong stock market IPO activities have significantly warmed up. In the first seven months of this year, 51 new shares were listed on the Hong Kong stock market (a year-on-year increase of 27.5%), raising a total of HK$1286 billion (a year-on-year increase of 616%). The CEO of the Hong Kong Stock Exchange said that currently, more than 200 listing applications are under processing, and mainland companies' listing in Hong Kong continues to accelerate.

In the first seven months of 2025, a total of 16 companies in the daily consumption/specialty consumer sector went public on the Hong Kong stock market (including 3 A+H shares), raising approximately HK$281 billion, accounting for 31% and 22% of Hong Kong's IPOs during the same period respectively.

In the first seven months of 2025, consumer stocks included in IPOsHaitian Flavor Industry(106 HK$ billion, A+H),Anjing Food(24 HK$ billion, A+H), etc. In contrast, in 2024, it wasMao GPing(2.7 billion Hong Kong dollars),Tea Hundred Ways(2.6 billion Hong Kong dollars).

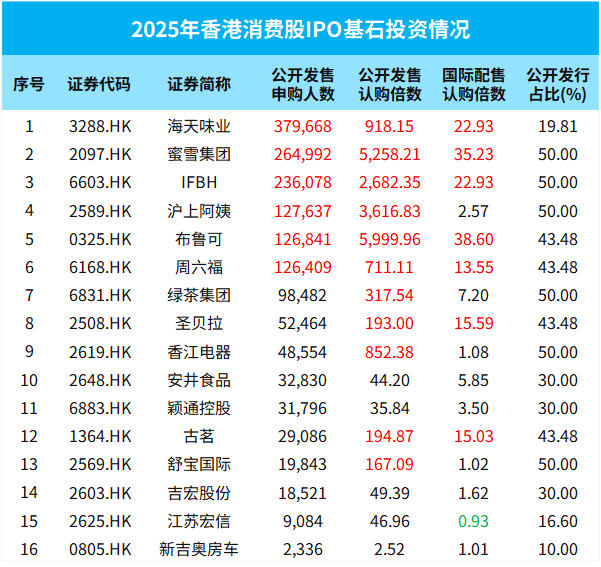

Haitian Flavor IndustryEight cornerstone investors subscribed for HK$4.667 billion, accounting for 46%. The investors include leading private equity firms such as Hillhouse/Horizons/Summit Ridge/Bright Edge [headquarters private equity], GIC/Hong Kong Bank of Commerce/Ruiseven [foreign institutional investors], and Foshan Development [local industrial investment];

Haitian Flavor IndustryNearly 380,000 people participated in new share subscriptions (the highest in the past four years), with an open subscription ratio of 918 times and a state-owned allocation subscription ratio of 23 times;

Brucoli: 127,000 people subscribed, with a public offering subscription ratio of 6,000 times (the highest within the year and third-highest in history), and state-owned allocation subscriptions at 38.6 times.

The Hong Kong IPO performance of 16 consumer stocks was outstanding, with an intraday increase probability of 62.50% and an average increase of 18.16%; the probability of a first-day increase was 56.25%, with an average increase of 13.78%. Among them, star companies such as BRKU saw an average increase of over 40% on their first day of listing, and their performance in the market has been strong, with stock prices doubling compared to the IPO issue price, attracting widespread market demand!

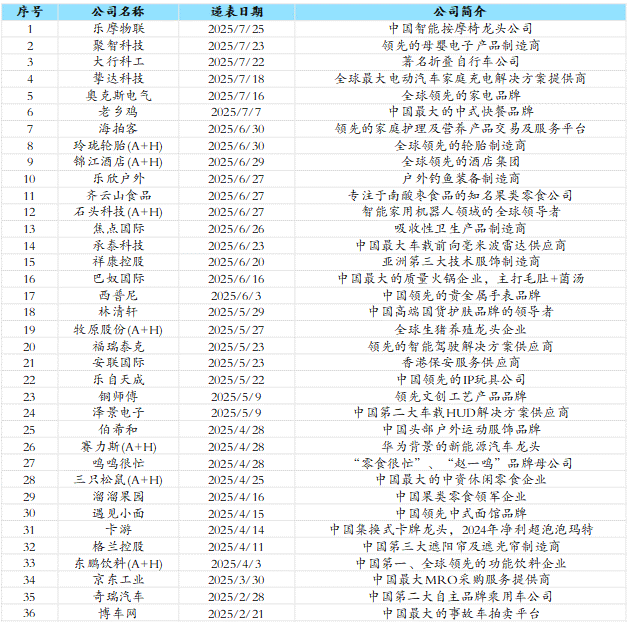

As of the end of July, more than 30 consumer companies have submitted their listing applications to the Hong Kong Stock Exchange. Among them, seven A-share companies are heading to Hong Kong for a dual listing of A+H shares, including Muyuan Co., Ltd., Sailisi Co., Ltd., Dongpeng Beverage Co., Ltd., Stone Technology Co., Ltd., Jinjiang Hotel Group Co., Ltd., and Linglong Tire Co., Ltd. The first three are all enterprises with a market value of over one hundred billion. In addition, there are many other star consumer companies.

Outstanding business model: Typical cases such asOld Shop Gold—— More than 20 times increase in value in one year since listing! A representative company of new consumption, with an extremely high brand premium;

Globalized Enterprises That Succeed in Going Global: Typical Casespopomart—— A cumulative increase of 28 times over three years! IP value release + remarkable results in going global, a model of globalization;

Stable profit distribution: Typical cases are as follows:Midea GroupSince 2013, the cumulative dividend has reached 1342 billion RMB, with an average dividend rate of nearly 50%;

Industry leading companies: including the aforementioned companies, as well asMao GPing,zero-carLeading consumer companies, which are also present in the Hong Kong stock market, enjoy a high valuation premium.

popomartIt achieved nirvana through going global, and with the 'recreating a Bubble Mart overseas', its overseas expansion brought about a double boost in valuation and performance. Since the low point in 2022, its stock price has risen by more than 30 times.