Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') released the 'Rehabilitation Medical Devices Market Study' on June 25th. The following content is an excerpt from this report.

1. Overview of the Medical Device Market

1.1 Definition of Medical Devices

Medical devices refer to instruments, equipment, appliances, in vitro diagnostic reagents and calibrators, materials, and other similar or related items that are used directly or indirectly on the human body, including the required computer software. Medical devices are primarily implemented through physical means rather than pharmacological, immunological, or metabolic methods, or although these methods are involved, they only play an auxiliary role. The clinical applications of medical devices include disease diagnosis, prevention, monitoring, treatment, or alleviation; injury diagnosis, monitoring, treatment, alleviation, or functional compensation; inspection, replacement, regulation, or support of physiological structures or processes; life support or maintenance; pregnancy control, etc.

1.2 China's Medical Device Market Size

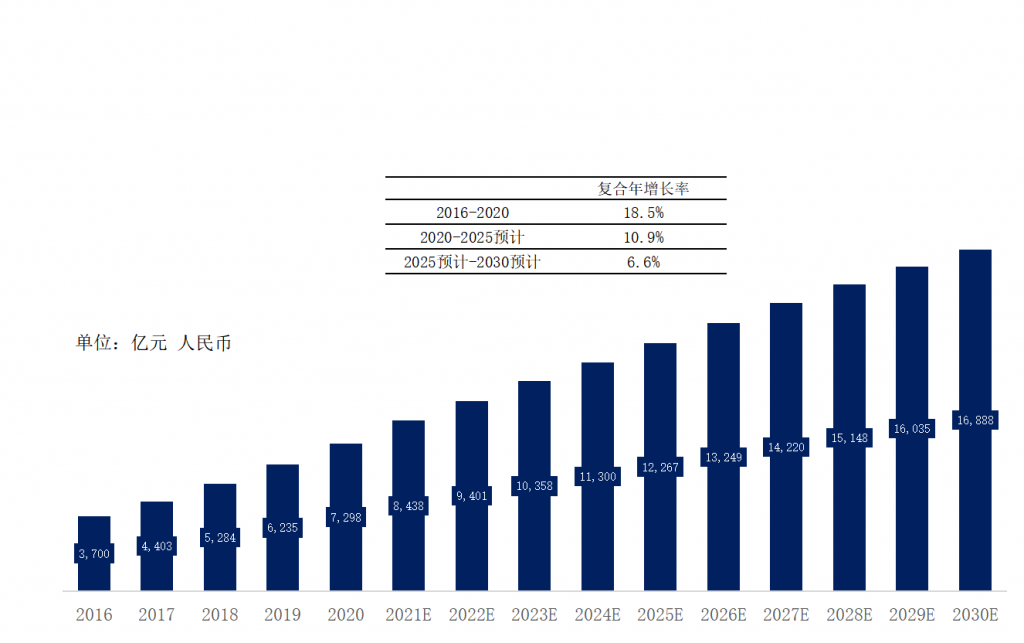

In China, with the improvement of residents' living standards and enhanced awareness of healthcare, the demand for medical device products continues to grow. Affected by national support policies for the medical device industry, the domestic medical device industry as a whole has entered a stage of rapid growth. From 2016 to 2020, the scale of China's medical device market increased from 370 billion yuan to 729.77 billion yuan, with an annual compound growth rate of 18.5% during this period. In 2020, China's medical device market accounted for 23.2% of the global medical device market. The Chinese medical device market will continue to grow and is expected to reach 1,688.78 billion yuan by 2030. With the process of population aging, the growth of per capita disposable income, and strong policy support, there is still broad room for growth in the medical device industry in the future.

Chart 1: China's Medical Device Market Size, 2016-2030E

Data source: Analysis by Frost & Sullivan

2. Market Analysis of Rehabilitation Medical Devices

2.1 Overview of Rehabilitation Medical Devices in China and Analysis of the Industrial Chain

In a general sense, rehabilitation equipment refers to devices, apparatuses, instruments, technologies, and software that are adapted or specially designed for use alone or in combination to improve the functional status of individuals with disabilities. More specifically, rehabilitation equipment specifically refers to medical instruments used in rehabilitation medicine for rehabilitation training and treatment, assisting in improving or compensating human functions.

In China's rehabilitation medical device industry chain, the upstream consists of hardware providers and software providers. They provide materials and accessories required for the research, development, and production of rehabilitation medical devices, as well as information technology services; the midstream includes manufacturers of rehabilitation medical devices and rehabilitation device distribution enterprises; the downstream includes application sites such as rehabilitation institutions and patient service organizations. Rehabilitation medical devices are most widely used in medical institutions, elderly care facilities, and disability rehabilitation centers. Among them, manufacturers of rehabilitation medical devices located in the midstream mainly provide products for rehabilitation, elderly care, medical, and other institutions.

Chart 2. Rehabilitation Medical Device Industry Chain

Data source: Analysis by Frost & Sullivan

The sales model of rehabilitation medical devices can be divided into direct sales and distribution. Under the direct sales model, the company's sales network is generally extensive, with its own sales staff directly connecting with downstream end customers for product sales and providing supporting solutions. In the distribution model, companies usually cooperate with agents or general indirect customers on a long-term basis. After the agent develops business with terminal institutions, goods are directly shipped to the terminal institutions for acceptance.

2.2 Policy Analysis of Rehabilitation Medical Devices in China over the Past 5 Years

According to the 'Classification Catalogue of Medical Devices', due to the complexity of rehabilitation devices, only some products are included within the scope of medical device industry supervision. Rehabilitation aids that do not fall under the category of medical devices only need to comply with relevant national standards and quality system regulations and will not be subject to additional supervision.

To promote the development of China's rehabilitation assistive device industry, in 2016, the State Council issued the 'Several Opinions on Accelerating the Development of Rehabilitation Assistive Devices', integrating rehabilitation assistive devices into the development process of 'Made in China 2025'. In September 2017, the Ministry of Civil Affairs, together with five other departments and units, issued the 'Notice on Carrying Out Comprehensive Innovation Pilot Projects for the National Rehabilitation Assistive Device Industry', indicating that China will conduct comprehensive innovation pilot projects for the national rehabilitation assistive device industry in 12 regions to explore the deep integration of rehabilitation assistive devices in fields such as elderly care, disability assistance, medical care, and health.

Chart 3: Encouraging Policies for the Rehabilitation Medical Device Industry

| Promulgation date | Enacting Authority | Policy name | Main content and impact | |

| 2021/10 | National Health Commission | Notice on Carrying out Pilot Work on Rehabilitation Medical Services | Throughout 2022, 15 provinces were designated as pilot areas for rehabilitation medical services. This includes increasing the number of medical institutions and beds providing rehabilitation services, strengthening the capacity building of rehabilitation medicine disciplines, enhancing the training of rehabilitation professionals, innovatively developing multidisciplinary cooperation models in rehabilitation medicine, and accelerating the development of home-based rehabilitation medical services. | |

| June 2021 | National Health Commission, etc. | Notice on Printing and Distributing Opinions on Accelerating the Development of Rehabilitation Medicine | Strive to gradually establish a rehabilitation medical professional team with a reasonable number and excellent quality by 2022, reaching 6 rehabilitation physicians and 10 rehabilitation therapists per 100,000 population. By 2025, the goal is to reach 8 rehabilitation physicians and 12 rehabilitation therapists per 100,000 population. | |

| 2021/3 | Adopted at the Fourth Session of the 13th National People's Congress | Outline of the 14th Five-Year Plan for National Economic and Social Development of the People's Republic of China and Long-Range Objectives Through the Year 2035 | Strengthen prevention, treatment, nursing, and rehabilitation in an organic manner. Improve the traditional Chinese medicine service system and give full play to the unique advantages of traditional Chinese medicine in disease prevention, treatment, and rehabilitation. Establish a rehabilitation university to promote the market-oriented development of rehabilitation services, improve the fitting rate of rehabilitation aids, and enhance the quality of rehabilitation services. | |

| 2021/1 | Ministry of Civil Affairs | Notice on Printing and Distributing the List of National Comprehensive Innovation Pilot Work Policies and Measures to Support the Rehabilitation Assistive Devices Industry | Encourage and guide banking financial institutions to innovate financial products and service methods, and increase support for the rehabilitation assistive device industry in pilot areas. Support rehabilitation assistive device enterprises in pilot areas to raise funds by issuing non-financial corporate debt financing instruments such as short-term financing bills and medium-term notes. | |

| 2019/11 | National Health Commission | Notice of the General Office of the National Health Commission on Carrying out Pilot Work on Accelerated Rehabilitation Surgery | In 31 provinces, autonomous regions, and municipalities directly under the Central Government across the country, 195 pilot hospitals were selected. Joint surgery, spinal surgery, trauma orthopedics, bone tumor surgery, and foot and ankle surgery were identified as pilot disease types. Efforts were made to strengthen education for medical staff and patients, integrating rehabilitation concepts into the diagnosis and treatment of related diseases. | |

| 2019/10 | National Health Commission, etc. | Several Opinions on Further Promoting the Integrated Development of Medical Care and Elderly Care | Encourage elderly care institutions to closely connect with surrounding rehabilitation medical (rehabilitation centers), nursing homes (nursing centers) and other continuing healthcare providers, establish collaborative mechanisms, and encourage localities to gradually increase the scope of medical rehabilitation projects included in basic medical insurance expenditures as stipulated. | |

| 2018-11 | National Medical Products Administration | Notice of the General Office of the National Medical Products Administration on Printing and Distributing Key Points and Judgment Principles for Medical Device Clinical Trial Inspections | Compress the registration approval time limit for medical devices, introduce optimized measures to encourage the market launch of innovative medical device products, etc. Deepen the reform of 'delegating power, improving regulation, and optimizing services' to optimize access services. Comprehensively deepen the reform of the medical device review and approval system, promote medical device technological innovation, drive high-quality development of medical devices, and meet public clinical needs. | |

| May 2018 | National Medical Products Administration | "Special Approval Procedure for Innovative Medical Devices |

Revised the 'Special Approval Procedures for Medical Devices' issued in 2014 to form a special approval procedure for innovative medical devices, aiming to ensure the safety and effectiveness of medical devices. Encourage research and innovation in medical devices. Promote the popularization and use of new medical device technologies, and support the review and approval of rehabilitation medical devices. | |

| October 2017 | National Medical Products Administration | "Opinions on Deepening the Reform of the Evaluation and Approval System to Encourage Innovation in Drugs and Medical Devices" | Encourage the research and development of new drugs and innovative medical devices, strengthen intellectual property protection, promote medical device innovation, enhance the full life cycle management of medical devices, and meet society's demand for the use of medical devices. | |

| September 2017 | Ministry of Civil Affairs, etc. | Notice on Carrying out Comprehensive Innovation Pilot Projects for the National Rehabilitation Assistive Devices Industry | Twelve prefecture-level administrative regions across the country will be selected to carry out comprehensive innovation pilots for the rehabilitation assistive device industry, aiming to create a favorable environment for the development of this sector. | |

| August 2017 | State Council | "Opinions on Further Promoting Cost Reduction and Efficiency Improvement in Logistics to Boost the Development of the Real Economy" | Deepen the reform of 'delegating power, improving regulation, and optimizing services' to stimulate the vitality of logistics operators; increase efforts to reduce taxes and fees to effectively alleviate the burden on enterprises; accelerate the informatization, standardization, and intelligence of logistics and warehousing; deepen linkage and integration to promote coordinated industrial development. | |

Data source: Analysis by Frost & Sullivan

2.3 Market Scale and Competitive Landscape of Rehabilitation Medical Devices in China

Currently, rehabilitation equipment can be divided into physical therapy devices, rehabilitation assessment devices, rehabilitation training devices, and other rehabilitation equipment according to different application fields. Physical therapy devices refer to rehabilitation medical devices that use physical factors such as sound, light, electromagnetic energy, etc., to treat the human body in order to improve or restore function. Depending on the treatment method, they can be further subdivided into electrotherapy, thermal (cold) therapy, phototherapy, pressure therapy, magnetotherapy, ultrasonic therapy, and high-frequency therapy; rehabilitation assessment devices refer to instruments that effectively and accurately evaluate the type, nature, scope, location, severity, and prognosis of disabilities using objective quantitative methods, mainly including neurological function assessment devices, balance testing devices, gait analysis systems, and physiological parameter-induced diagnostic devices; rehabilitation training devices generally refer to instruments used by therapists when conducting rehabilitation training with patients, which can target various causes of dysfunction (such as hemiplegia, paraplegia, cerebral palsy, amputation, etc.). Using movement therapy and occupational therapy, these devices can maximize the recovery of residual functions for patients, including two main parts: biofeedback training systems and motor rehabilitation training devices; other rehabilitation equipment includes rehabilitation education devices and assistive devices. Rehabilitation education devices refer to rehabilitation medical devices that restore basic functions of disabled individuals through training interventions; assistive devices are products used to improve, compensate for, replace human functions, implement auxiliary treatment, and prevent disabilities.

Chart 4. Classification of Rehabilitation Devices

Data source: Analysis by Frost & Sullivan

From the perspective of downstream demand, China has a huge population that requires rehabilitation services and medical devices due to neurological diseases, bone and joint muscle disorders, the elderly, and postpartum women. With the acceleration of population aging, the increasing number of chronic disease patients year by year, the increase in the number of postpartum women after the relaxation of the two-child policy, and other factors, the demand for rehabilitation medical services and medical devices in China will continue to grow. The market share of rehabilitation medical devices in China increased from 225.0 billion yuan in 2017 to 450.3 billion yuan in 2021, with a compound annual growth rate of 19.0%. It is estimated that by 2030, the market share can reach 941.5 billion yuan.

Chart 5. Market Size and Forecast of Rehabilitation Medical Devices in China

Data source: Analysis by Frost & Sullivan

In 2021, the market for rehabilitation medical devices in China reached 45 billion yuan. Among them, the market scale of physical therapy equipment was 6.73 billion yuan; the market scale of rehabilitation assessment equipment was 510 million yuan; the market scale of rehabilitation training equipment was 1.88 billion yuan; and the market scale of other rehabilitation equipment was 35.91 billion yuan. At present, the rehabilitation medical device market is still mainly composed of wheelchairs, prosthetics, hearing aids, barrier-free facilities, and other rehabilitation equipment. There are a wide variety of products, showing a low concentration, low unit prices, and large physical scale.

Currently, in addition to suppliers producing rehabilitation aids, there are nearly a thousand rehabilitation medical device companies in China. With the continuous development of domestic technology and policy encouragement for independent innovation, as the country promotes domestic substitution, it will continuously drive product substitution and technological innovation in high-value rehabilitation devices, leading the overall rehabilitation device market from being dominated by low-value rehabilitation education and auxiliary devices to that of high-end devices. For example, under the favorable policy of including some traditional Chinese medicine services in the general medical service catalog, the market prospects for traditional Chinese medicine rehabilitation medical devices such as traditional Chinese medicine fumigation machines, damp heat compresses, and electro-moxibustion therapy devices are broad. Additionally, affected by the relaxation of the two-child policy and the increasing awareness of postpartum recovery among patients, there is a strong demand in the field of pelvic floor and postpartum rehabilitation. The market scale for postpartum rehabilitation devices such as postpartum rehabilitation therapy machines and pelvic floor muscle trainers will continue to grow.

In 2021, among the overall market competition landscape of rehabilitation medical devices in China, the top five companies were Henan Xiangyu Medical, Nanjing Weisi Medical, Nanjing Maitan Medical, Suzhou Haobo Medical, and Guangzhou Longzhijie.

Currently, the rehabilitation medical device industry in China is characterized by a large market scale, a wide variety of products, small revenue volumes for participating enterprises, and a focus on a single category. The main reasons for these characteristics include: first, the patient population facing rehabilitation medical devices is vast, with complex diseases spanning multiple departments and a wide range of product categories. Most products are small, medium, and household-use equipment consumables with low unit values. Second, due to product characteristics, most R&D enterprises in the Chinese rehabilitation medical device industry tend to focus their R&D and commercialization capabilities on different niche areas, reducing cost expenditures on one hand and gaining differentiated advantages in the field of rehabilitation medical devices on the other. Finally, since the rehabilitation specialty departments in domestic hospitals are still in the early stages of development, the procurement of rehabilitation medical device products relies heavily on other specialties, resulting in insufficient one-stop procurement needs. This has maintained the current situation where there are small revenue volumes for individual enterprises and a large number of companies. Therefore, despite having nearly a thousand production enterprises, the annual revenue of leading companies is only 520 million RMB. Most enterprises in the industry have an annual income of less than one billion RMB in the rehabilitation medical device sector.

In the sub-section of physical therapy equipment, the main companies include Henan Xiangyu Medical, Nanjing Weisi Medical, Suzhou Haobo Medical, Guangzhou Longzhijie, Pumen Technology, Changzhou Qianjing Rehabilitation, and Guangzhou Yikang Medical. In 2021, in the field of physical therapy equipment, Henan Xiangyu Medical had a market share of 4.4%, while Nanjing Weisi Medical's market share was 6.2%.

In the rehabilitation evaluation device sub-section, major companies include Henan Xiangyu Medical, Guangzhou Longzhijie, Changzhou Qianjing Rehabilitation, Suzhou Haobo Medical, and Guangzhou Yikang Medical. According to information collected through official public channels, in 2021, Henan Xiangyu Medical's market share in the rehabilitation evaluation device sub-section was 4.1%.

In the subsector of rehabilitation training equipment, major companies include Henan Xiangyu Medical, Nanjing Weisi Medical, Suzhou Haobo Medical, Guangzhou Longzhijie, Changzhou Qianjing Rehabilitation, and Guangzhou Yikang Medical. Among them, in 2021, Henan Xiangyu Medical's market share was 8.3%.

In the field of rehabilitation medical devices, in addition to being classified by device function type, they can also be categorized by the departments they treat, such as Traditional Chinese Medicine (TCM), Neurology, Cardiology and Pulmonary Medicine (Internal and Surgical), Orthopedics, Pain Management, Pediatrics, Obstetrics and Gynecology, etc. The product coverage often represents a manufacturer's level of technological research and development. Currently, there are few comprehensive rehabilitation medical device companies in China that provide multi-departmental coverage and a comprehensive product layout. Companies with coverage across five or more departments include Henan Xiangyu Medical, Pumen Technology, and Suzhou Haobo Medical. According to publicly available information collection and annual report data from listed companies, in 2021, the top three local Chinese companies providing multi-departmental coverage for rehabilitation medical device products were Henan Xiangyu Medical, Suzhou Haobo Medical, and Pumen Technology.

2.4 Analysis of Market Development Drivers and Trends in China's Rehabilitation Medical Devices Industry

(1) The demand for rehabilitation treatment is enormous

The end-users of rehabilitation medical devices mainly include the elderly, patients with chronic diseases, disabled individuals, those with postoperative functional impairments, postpartum functional impairments, and people with serious illnesses, among others, indicating a huge potential for rehabilitation needs. According to global disease burden studies (GBD) on rehabilitation, it is estimated that about 2.41 billion people worldwide may benefit from rehabilitation treatment during illness or injury in 2021. Among them, China has the largest rehabilitation demand, with as many as 460 million people needing rehabilitation services in 2021. The vast patient base indicates that there is great potential for further development of rehabilitation medical devices.

(2) Technological advancements in the field of rehabilitation equipment

The upgrade of rehabilitation medical technology has directly driven the improvement in the treatment level of rehabilitation medical devices. Currently, China has developed and produced several intelligent devices, such as intelligent daily life occupational training systems, digital OT assessment and training systems, digital upper limb assessment and training instruments, intelligent massage and spinal manipulators, etc. These include devices that can be used for multi-person rehabilitation training and scenario interactive ones, which not only enhance the sensory experience of users but also improve treatment outcomes. In addition, the integration of artificial intelligence technology with traditional rehabilitation medical devices, assessment equipment, and rehabilitation robot technology enables intelligent human-computer interaction to better assist patients with functional impairments in rehabilitation training, improve their exercise enthusiasm, facilitate medical staff to follow up on the patient's rehabilitation progress, improve treatment outcomes, and achieve medical modernization. In the future, with further innovation in disease diagnosis and treatment technology, patients' acceptance will be further enhanced, which will drive the demand for rehabilitation medical devices.

(3) Improvement in the accessibility of rehabilitation care

The number of rehabilitation hospitals in our country continues to increase, with private institutions being the main driving force. We are actively exploring the establishment of a three-level rehabilitation medical service system, stipulating that comprehensive hospitals at or above the second level should set up rehabilitation medicine departments, encouraging private capital to enter rehabilitation hospitals, supporting the transformation of secondary comprehensive hospitals into specialized rehabilitation hospitals, and encouraging early intervention in rehabilitation surgery. According to the 'China Health Statistics Yearbook', from 2015 to 2020, the number of beds in rehabilitation medicine departments in health care institutions in China increased from 161,800 to 300,000, with a CAGR of 13.2%. Therefore, under the guidance of national policies and the participation of social capital, rehabilitation medical resources have rapidly increased, improving accessibility to rehabilitation services, ensuring the release of rehabilitation medical needs, and is expected to drive a continuous rise in the demand for rehabilitation medical device allocation, promoting rapid growth in the overall market scale.

In the future, China's rehabilitation medical devices will develop in the direction of scale-up, quality improvement, intelligence, refinement, and home-based care:

(1) Scale-up

The rehabilitation medical device industry has a strong channel-sharing characteristic. On one hand, once a product is recognized by customers, companies can continuously promote other products through the established channel platforms; on the other hand, the channels in the rehabilitation medical device industry have certain exclusivity features. Due to the long service life of products, it is easier for those who enter first to form channel barriers, leading to a trend where the stronger ones become even stronger and market concentration continues to increase. Therefore, having a complete range of products and achieving scale are inevitable trends for the long-term development of the industry.

(2) Quality-oriented

Rehabilitation medical devices are closely related to human life safety, and the brand effect of these devices is highly enduring. Rehabilitation medical device enterprises that have formed a branded scale are subject to strict industry supervision, making their product quality, safety, and controllability more assured. Therefore, brands with quality assurance will become the preferred choice for customers as they feel more secure and prioritized. To compete with international rehabilitation medical device enterprises, the market requires domestic rehabilitation medical device enterprises to develop in the direction of quality and branding, creating competitive domestic independent brands.

(3) Intelligence

Rehabilitation medical devices are mainly used for patients with functional impairments, so it is of great significance to achieve intelligent and digital functions for human-computer interaction between rehabilitation medical devices and patients. In the future, rehabilitation medical devices will integrate with technologies such as smart sensors, the Internet of Things, and big data, developing in the direction of intelligence. At the same time, the concept of intelligent human-computer interaction for rehabilitation has emerged. Networked rehabilitation medical devices will achieve communication between output control devices and remote intelligent devices, enabling remote communication and medical care, which is conducive to increasing patients' enthusiasm for rehabilitation exercises, facilitating medical staff to follow up on the patient's recovery process, improving the effectiveness of rehabilitation treatment, and realizing modernization of healthcare.

(4) refinement

Currently, another development trend in rehabilitation medical devices is refinement, which involves developing smaller, portable devices with more refined functional classifications to address the limited space for health care in hospitals and homes. This enables medical staff to quickly and simply transfer medical equipment and accurately locate its functions. In addition, the refinement of rehabilitation medical devices also provides feasibility for saving on rehabilitation treatment sites and reducing the labor costs of medical staff. From a research and development perspective, with the advancement of technologies such as sensors and microfluidics, it has become possible to produce devices with various functional configurations and nursing settings while reducing product size.

(5) Home-based

Home medical care device products are essentially a type of popularized small-scale healthcare equipment, which have certain functions such as prevention, diagnosis, health care, treatment, adjuvant therapy, and rehabilitation. They are suitable for use at home by families and the elderly. With the gradual improvement of China's tertiary rehabilitation medical system construction, rehabilitation medical resources will be decentralized to primary medical institutions and even communities. Rehabilitation medical equipment will eventually gradually enter households and develop in the direction of facilitating home-based care.

3. Market Analysis of Balloon-Assisted External Counterpulsation Systems

3.1 Overview of Chinese Balloon-expandable Extracorporeal Counterpulsation Systems

Counterpulsation refers to a method of auxiliary circulation that reduces systolic blood pressure and increases diastolic blood pressure within the aorta through mechanical means, thereby assisting the heart in performing its work, improving blood circulation, and increasing blood flow to organs such as the heart, brain, and kidneys. Counterpulsation increases coronary artery blood supply by raising diastolic arterial pressure, rescuing ischemic myocardium, and enhancing the heart's pumping function. Common counterpulsation methods include intra-aortic balloon counterpulsation and extracorporeal counterpulsation.

The balloon extracorporeal counterpulsation device controls the balloon to apply appropriate pressure to the body during diastole by synchronizing with physiological signals (including but not limited to electrocardiogram) outside the human body. It is an auxiliary circulatory device that increases arterial pressure during diastole and cancels the pressure before systole, thereby reducing systolic blood pressure.

Extracorporeal counterpulsation devices can be classified into two types based on the treatment method: non-enhanced extracorporeal counterpulsation and enhanced extracorporeal counterpulsation. Compared to non-enhanced extracorporeal counterpulsation devices, enhanced extracorporeal counterpulsation devices add a hip airbag in addition to limb airbags. Since the hemodynamic effect of enhanced extracorporeal counterpulsation is currently the best available form of extracorporeal counterpulsation, all extracorporeal counterpulsation devices on the market currently adopt the design model of enhanced extracorporeal counterpulsation, commonly referred to as 'extracorporeal counterpulsation' devices.

3.2 Market Size and Competitive Landscape of Airbag-type Extracorporeal Counterpulsation Systems in China

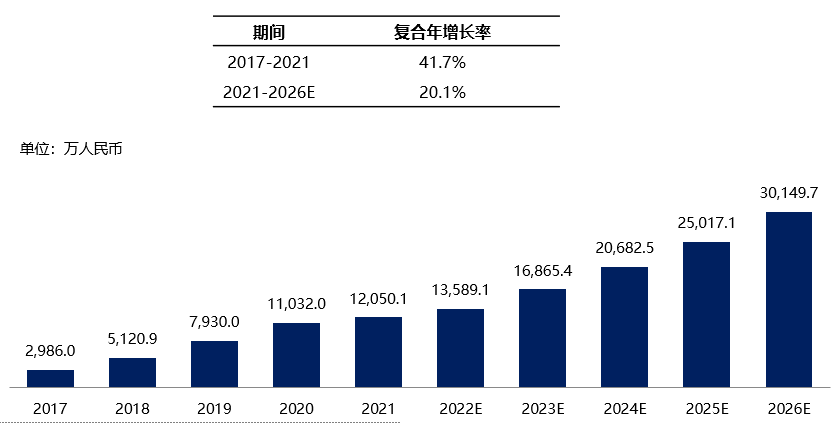

In China, the manufacturing technology of airbag extracorporeal counterpulsation systems has become relatively mature, and currently, most products on the market are domestically produced. There are not many approved products, and there is no competition from similar imported products, leaving significant development space. The market share of airbag extracorporeal counterpulsation systems in China increased from 29.86 million yuan in 2017 to 120 million yuan in 2021, with a compound annual growth rate of 41.7%. It is expected that by 2026, the market share can reach 310 million yuan.

Chart 7. Market Size and Forecast of Airbag-type Extracorporeal Counterpulsation Systems in China, 2017 - 2026E

Data source: Analysis by Frost & Sullivan

In China, the main enterprises producing and developing airbag-type extracorporeal counterpulsation device systems include Pusikang Medical, Guangzhou Aomai Medical, Yidian Medical, and Jiepai Medical.

3.3 Market Development Trends of Airbag-type Extracorporeal Counterpulsation Systems in China

(1) In response to the continuous expansion of the patient population

With the intensification of the aging population trend in China, the number of people suffering from cardiovascular and cerebrovascular diseases has correspondingly increased; at the same time, due to poor dietary and lifestyle habits among contemporary people, cardiovascular and cerebrovascular diseases are also showing an 'youthful' trend, leading to a continuous upward trend in morbidity rates in our country. Cardiovascular and cerebrovascular diseases such as heart failure, coronary heart disease, angina pectoris, and stroke have become the leading cause of death among Chinese residents, with extremely high mortality rates, imposing a heavy burden on society and families.

The main treatment methods for such diseases include drug therapy and interventional trauma surgery. Although these two mainstream approaches are effective and have relatively significant therapeutic effects, drug therapy has issues such as side effects and drug resistance; or due to the high trauma, sequelae, and cost of interventional trauma surgery, many patients do not choose this treatment method. In contrast, extracorporeal counterpulsation (ECAP) is a physical therapy that does not involve drugs or surgery, and can avoid the side effects and sequelae associated with traumatic and invasive treatments. Studies have shown that the use of ECP can significantly increase coronary perfusion pressure, enhance myocardial function, promote the formation of collateral circulation, and effectively treat various cardiovascular and cerebrovascular diseases, including heart failure, angina pectoris, acute myocardial infarction, stroke, etc.

(2) Usage scenarios are continuously expanding.

In addition to treatment, extracorporeal counterpulsation devices can also play a role in postoperative rehabilitation or daily health care. Patients with cardiovascular and cerebrovascular diseases need to go through a long cardiac rehabilitation process after surgical treatment. However, considering that some patients are unable to undergo exercise rehabilitation due to mobility limitations, low exercise tolerance, and discomfort during exercise, extracorporeal counterpulsation devices can be used as a transition or alternative to exercise training to prevent patients from experiencing another acute myocardial infarction and requiring reimplantation of stents. In addition, extracorporeal counterpulsation devices can improve the user's exercise tolerance and cardiopulmonary function, help delay arteriosclerosis, maintain good vascular condition, and play a role in daily health care.

(3) The market continues to expand overseas

Unlike most medical devices dominated by imports, the basic theory of extracorporeal counterpulsation (ECOP), instrument development, and clinical application in China began in 1976. The enhanced ECOP technology developed locally in China is at the forefront internationally and recognized by experts and enterprises from developed countries. The manufacturing technology of ECOP devices has become relatively mature in China, with current market products mainly domestic, and there are not many approved products. At the same time, there is no competition from imported similar products, leaving significant room for the development of domestic ECOP devices.

(4) Device optimization

The demand for extracorporeal counterpulsation devices is high, manufacturing technology is mature, and it is a Class A reimbursable treatment item that can be fully included in the reimbursement scope. However, currently, extracorporeal counterpulsation devices are not widely used in the treatment of cardiovascular and cerebrovascular diseases. The main reasons are their large size, which requires more corresponding supporting space, and patients need to undergo treatment in a dedicated treatment room under the supervision of professional medical staff, with high equipment requirements; on the other hand, due to the low single treatment fee for extracorporeal counterpulsation, but its purchase price and subsequent maintenance costs are high, making it difficult for many hospitals to accept, resulting in the lack of widespread popularization of extracorporeal counterpulsation devices. Therefore, miniaturization, intelligence, and rational structure are the main research directions for future extracorporeal counterpulsation devices.

4. Microwave Therapy Machine Market Analysis

4.1Overview of Microwave Therapies in China

Microwave refers to electromagnetic waves with a frequency of 300 MHz-300 GHz, which is an abbreviation for a limited frequency band within radio waves. Clinically, the interaction between microwaves and living organisms can be divided into two main categories: microwave thermal effects and non-microwave thermal effects. The microwave therapy used by microwave treatment devices is a non-contact heating method that serves to stop bleeding, coagulate, cauterize or reduce inflammation, reduce swelling, relieve pain, improve local tissue blood circulation, etc., in diseased tissues. It does not cause thermal burns or electric burns due to electrical contact and is a new technology that can replace electrocautery, cryotherapy, and laser surgery.

Microwave has high thermal efficiency and strong penetration into human tissues, with the advantage of generating heat both internally and externally. Microwaves generate heat within human tissues, reaching depths of 5-8 centimeters. They can penetrate surface coverings such as clothing and plaster to reach the affected area, promoting blood circulation, water absorption, and new granulation tissue growth. At the same time, the ratio of heat generated by microwaves in fat to muscle is close (for short-wave and ultrashort-wave, the temperature rise in fat is about 9 times that of muscle under the action of electrodes), meaning that the microwave thermal effect is more uniform, and there is still a significant thermal effect in deeper muscle layers. Therefore, even for conditions in deeper areas, good therapeutic effects can be achieved.

Microwave therapy machines were born with the research and application of microwave therapy. They are new intelligent treatment instruments made using the biological effects of microwaves on the human body and their strong penetration ability. By utilizing the thermal and non-thermal effects of microwave on biological tissues, patients experience no pain or discomfort during treatment. It can accurately and effectively stop bleeding, coagulate, cauterize, reduce inflammation, reduce swelling, relieve acute conditions, alleviate pain, or improve local tissue blood circulation in diseased tissues.

At the same time, microwave therapy devices have a very wide range of applications and can treat various diseases such as gynecology, urology, anorectal surgery, otolaryngology, surgery, dermatology, etc. For example: bladder tumors, prostatitis, polyp removal, ulcer coagulation, lumbar muscle strain, cervical spondylosis, sprains, scapulohumeral periarthritis, arthritis, etc. Microwave therapy machines are usually the preferred choice for comprehensive surgical treatment equipment in outpatient wards. There are complete and non-adhesive special internal radiation devices and surgical instruments. Using a microwave therapy machine is simple to operate, without tissue carbonization, rapid hemostasis, no splashing, and good wound repair. In addition, the treatment process has the characteristics of being painless, non-invasive, having no side effects, rapid hemostasis, no splashing, and good wound repair. On this basis, the machine itself is reasonably priced with a high return rate, suitable for use in hospitals at all levels and outpatient clinics.

4.2Market scale and competitive landscape of microwave therapy machines in China

In China, microwave therapy has been widely applied in multiple departments, and the market for microwave therapy machines has rapidly expanded and developed accordingly. The market share of microwave therapy machines in China increased from 140 million yuan in 2017 to 200 million yuan in 2021, with a compound annual growth rate of 20.1%. It is estimated that by 2026, the market share can reach 430 million yuan. According to information collected through official public channels, there are currently more than forty microwave therapy machine research and development manufacturers.

Chart 8. Market Size and Forecast of Microwave Therapies in China, 2017 - 2026E

Data source: Analysis by Frost & Sullivan

In China, the main enterprises producing and developing microwave therapy machines include Puning Nanjing Yigao Medical, Wuhan Kangyou Medical, Tianjin Shunbo Medical, Tianjin Schneider Medical, Suzhou Haobo Medical, and Xuzhou Novan Medical.

4.3Development Trend of China's Microwave Therapy Machine Market

(1) The product has a wide range of applications

Currently, microwave therapy has been widely applied in multiple departments. Microwave therapy has a wide range of applications, high safety, and is simple to operate, making it suitable for use in hospitals and outpatient clinics at all levels. Coupled with the affordable price and high return rate of equipment, microwave therapy devices have been widely used in primary hospitals across China, playing an important role in departments such as gynecology, oncology, neurology, gastroenterology, urology, proctology, otolaryngology, rehabilitation physiotherapy, etc., with a very broad market prospect.

(2) The number of use cases is constantly increasing

Due to the new directions in microwave therapy research in recent years, it will drive the development of traditional physiotherapy in the field of minimally invasive treatment. Currently, various methods of tumor treatment using ultrasound-guided microwaves are widely practiced clinically, utilizing the thermal penetration of microwaves to achieve non-surgical treatment of tumors. This field has become a research hotspot worldwide over the past decade. Minimally invasive treatment is one of the rapidly developing new technologies for tumor treatment in recent years. Compared with traditional surgery, minimally invasive surgery has advantages such as less trauma, finer scars, less bleeding during surgery, less pain for patients after surgery, and faster recovery. Against this backdrop, a class of minimally invasive ablation technologies and products represented by 'microwave ablation' have also emerged and are already being used in the treatment of brain tumors and bladder tumors. Currently, there is a wide variety of imported and domestic microwave therapy devices on the Chinese market, and companies will form good synergies through competition, influencing and promoting each other, thereby further developing the microwave therapy device market.

(3) Clinical application promotes technological breakthroughs

The application of microwaves in medicine has rapidly expanded and developed, but its breadth and depth are far from fully exploited. There are indeed many challenges to overcome and improvements to be made in medical treatment. For instance, most microwave therapy devices on the market are relatively large in size and pose certain risks when used. Prolonged use or excessive power may lead to local burns, requiring them to be used under the supervision of a physician. Additionally, those with severe circulatory disorders or who have lost their sensitivity to temperature cannot use them. To further enhance the applicability of microwave therapy devices, portability and intelligence are key points for future microwave therapy devices that can be used at home. Moreover, with the emergence of new microwave emitters and improvements in microwave radiators, especially as research on the interaction mechanisms between microwaves and living organisms continues to deepen, as well as with further strengthening of control over microwave radiation depth, intensity, and safety, microwave therapy instruments will surely enter broader fields.