Report research scope

market scope

- China's industrial market

- China's Industrial Internet Market

- China Industrial Internet Platform Market

Time range

- Base year: 2021

- Historical Years: 2015 to 2021

- Forecast Years: 2022 to 2026

Regional scope

- Mainland China

1. Overview of China's Industrial Market Industries

1.1 Current Development Status of China's Industrial Market

In recent years, China's industry has continued to develop rapidly by relying on advantages such as the demographic dividend and seizing opportunities such as industrial transfer, becoming the 'world factory'. In 2010, China surpassed the United States to become the country with the highest added value in global manufacturing. By 2019, China's manufacturing added value reached 26.9 trillion yuan, accounting for 28.1% of the global total, maintaining its position as the world's largest manufacturing country for eleven consecutive years. From 2016 to 2019, China's industrial added value grew by an average of 5.9% annually, far higher than the world's industrial average annual growth rate of 2.9% during the same period. It is expected that China will continue to play an important role in the world's industrial field in the future.

1.2 Added Value of China's Industrial Market

From 2016 to 2019, China's industrial added value increased from 24.54 trillion yuan to 31.71 trillion yuan, with an average annual growth rate of 5.9%, far exceeding the world's average annual industrial growth rate of 2.9% during the same period; in that year, the main business income of industrial enterprises above designated size in China reached 105.78 trillion yuan. Advanced manufacturing and large-scale manufacturing were once the development supports for powerful countries such as the UK, the US, Germany, and Japan. In 2019, the added value of manufacturing in the US accounted for 11.1% of GDP, Germany's was 19.4%, Japan's was 19.5%, and the UK's was 8.6%. Compared with developed countries, China's added value of manufacturing as a proportion of GDP was still as high as 27.2% in 2019 after more than a decade of continuous decline.

In 2020, affected by the COVID-19 pandemic, industrial added value slightly declined to 31.31 trillion yuan. However, the main business income of industrial enterprises above designated size in China still achieved growth, reaching 106.14 trillion yuan. The '14th Five-Year Plan' particularly emphasizes 'maintaining the basic stability of the manufacturing sector's proportion', which also conveys the signal that manufacturing, as the leading sector of the national economy, is the backbone of the society's basic material production and industrial innovation.

Source: National Bureau of Statistics, Frost & Sullivan

Note: Since 2017, there have been incomparable factors between the main economic indicator data of industrial enterprises above designated size nationwide and the previous year's data. The main reasons are as follows: (1) According to the statistical system, the survey scope for industrial enterprises above designated size is adjusted regularly each year. Each year, some enterprises reach the scale standard and are included in the survey scope, while others exit due to reduced scale, as well as changes such as newly established enterprises, bankruptcies, and suspension (closure) of businesses. (2) Strengthening statistical law enforcement has led to the clearance of enterprises found not to meet the statistical requirements for industrial enterprises above designated size during inspections, and relevant bases have been corrected according to regulations. (3) Enhancing data quality management has eliminated duplicate statistical data across regions and industries.

1.3 Analysis of the Driving Forces for the Development of China's Industrial Market

1.3.1. Policy-driven

In recent years...

1.3.2. Technology-driven

With the continuous innovation of basic sciences...

1.4 Analysis of Restricting Factors for Industrial Development in China

1.4.1. The demographic dividend is weakening

1.4.2. Key technologies are restricted by foreign countries

1.4.3. Uncertainty in international relations in the post-pandemic era

1.5 Future Development Trends of China's Industrial Market

Currently, China's industry is embracing trends of digitization and intelligence. With industrial Internet platforms as an important carrier, the transformation of industrial paradigms is accelerating.

1.5.1. Accelerate the integration and development of new-generation information technology and industry

1.5.2. Chinese industrial enterprises shift from company-level competition to industry-level competition

1.5.2. Chinese industrial enterprises are accelerating the transformation from single applications to overall digitization

2. Overview of China's Industrial Internet Industry

2.1 Definition and Classification of the Industrial Internet Market in China

Industrial Internet provides network infrastructure for industrial intelligence upgrades by constructing both internal and external factory networks. Based on manufacturing, the Industrial Internet gradually penetrates into various emerging business forms, promoting the optimization and upgrading of related industries.

Data sources: public documents, expert interviews, Frost & Sullivan

From the perspective of product types and unified production organization methods, industrial enterprises can be categorized into discrete manufacturing industries and process manufacturing industries.

2.1.1 Discrete Manufacturing Industry

2.2.2. Process Manufacturing Industry

2.2 Analysis of the Industrial Chain in China's Industrial Internet Industry

The industrial Internet industry chain is complex, and there is a strong correlation and synergy among its various links. The upstream of the industry chain mainly consists of hardware devices, including sensors, controllers, industrial-grade chips, etc., which provide intelligent hardware devices for collecting data on the industrial Internet platform. The midstream of the industry chain includes internet platforms that analyze and process data, offering industry application solutions. The downstream of the industry chain represents typical application scenarios of the industrial Internet, such as equipment manufacturing, automotive industry, etc.

2.2.1 Enterprises in the Industrial Internet Industry Chain

2.2.2. Edge Layer Hardware Devices

- sensor

- controller

- Industrial chip

- Device IoT gateway

2.2.3. Industrial Internet Platform

2.3 Analysis of the market scale of China's industrial Internet industry, classified by industrial Internet levels

2.3.1. Industrial Internet market scale

2.3.2. IoT Connected Device Market Size

2.3.3. Industrial Internet Platform Market Size

2.3.4. Data Innovation Business Market Size

2.3.5. Industrial APP market scale

2.4 Analysis of the market scale of China's industrial Internet industry, categorized by different solutions

2.4.1 Market Size of Intelligent Manufacturing IIOT Solutions

2.4.2. Product Intelligence IIOT Solution Market Size

2.4.3. Industrial Chain IIoT Solution Market Size

2.5 Analysis of Industrial Policies in China's Industrial Internet Industry

2.6 Analysis of the Driving Forces for the Development of China's Industrial Internet Industry

2.6.1. Market Size of Intelligent Manufacturing IIOT Solutions

2.6.2. Product Intelligence IIOT Solution Market Size

2.7 Analysis of the Development Trend of China's Industrial Internet Industry

Currently, the industrial Internet industry is still in its early stages of development. The competitive landscape has not yet taken shape, and the development model is changing rapidly. Enterprises with strong technical accumulation and implementation experience are expected to gradually form a leading advantage in future competition.

2.7.1. The industry's development has shifted from policy-driven to enterprise-led

2.7.2. SMEs accelerate cloud and platform adoption

3. Analysis of the Technology and Development Status of China's Industrial Internet Platforms

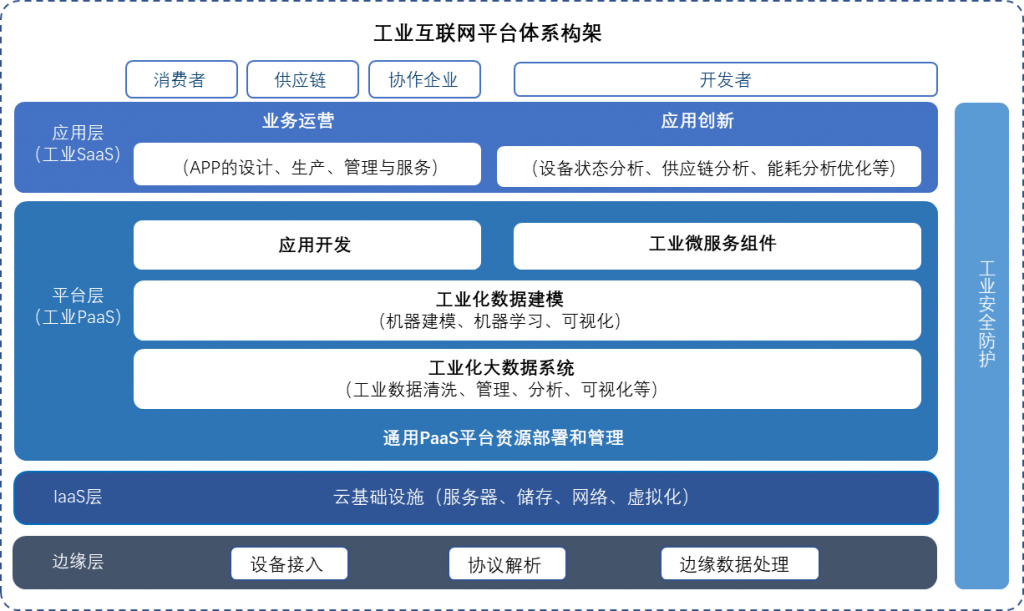

3.1 Analysis of the Architecture of China's Industrial Internet Platform

Industrial Internet is an industrial and application ecosystem formed by the comprehensive integration of the Internet, new-generation information technology, and industrial systems. It is a key comprehensive information infrastructure for the intelligent development of industry. Industrial Internet platforms are an extended development of enterprise industrial cloud platforms. They build more precise, real-time, and efficient data collection systems by overlaying new technologies such as the Internet of Things, big data, artificial intelligence, and blockchain on traditional enterprise cloud platforms. They construct industrial enabling platforms that include collection, storage, integration, analysis, and management functions, realizing cross-application of industrial equipment, experience knowledge, and big data, and ultimately increasing the output value of industrial enterprises.

The architecture of China's industrial Internet platform system is mainly aimed at the digitalization, networking, and intelligence needs of the industrial field. It constructs a service system based on device information collection, storage, and analysis to support the ubiquitous connection, elastic supply, and efficient allocation of industrial resources through an industrial cloud platform.

Source: Public information, AII, Frost & Sullivan

3.2 Analysis of the Current Development Status at Each Level of the Industrial Internet

3.2.1 Analysis of the current development status of the edge layer

3.2.2 Analysis of the Current Development Status of the IaaS Layer

3.2.3. Analysis of the current development status of the PaaS layer

3.2.4 Analysis of the Current Development Status of the SaaS Layer

3.3 Analysis of the Current Development Status and Trends of Industrial Internet Platforms

4. Case analysis of application fields of China's industrial Internet platforms

4.1 Overview of the Development of Industrial Internet in the Construction Machinery Field

3.1.1 Development Status of Construction Machinery in the Field

3.1.2. Current Application Status and Trends of Internet Platforms in the Construction Machinery Field

4.2 Overview of the Development of Industrial Internet in the Automotive Industry

4.2.1. Current Development Status of the Automotive Industry

4.2.2. Current Application Status of Industrial Internet Platforms in the Automotive Industry

5. Analysis of market competition pattern

5.1 Analysis of Market Competitors in China's Industrial Internet

Taking the 15 'double-cross' platform enterprises announced by the Ministry of Industry and Information Technology as an example, these include those that build data infrastructure and cloud services, such as Alibaba Cloud's SupET Industrial Internet Platform, Inspur Cloud Delta industrial platform, Huawei FusionPlant Industrial Internet Platform, Tencent WeMake Industrial Internet Platform, and Unigroup's UNIPower Industrial Internet Platform. In terms of the application entities for 'double-cross' platforms, industrial internet enterprises relying on large enterprise groups include COSMOPlat Industrial Internet Platform, Foxconn Fii Cloud Industrial Internet Platform, and Baisin xIn3Plat Industrial Internet Platform. From the perspective of the independence of industrial internet business operations, several platforms, including Aerospace Cloud Network INDICS Platform, Dongfang Guoxin CLOUDIIP Platform, Han Yun Industrial Internet Platform, Root Cloud ROOTCLOUD Industrial Internet Platform, Himi H-IIP Industrial Internet Platform, and Lan Zhuo supOS industrial operating system, are third-party innovative enterprises or relatively independent of large enterprise groups, gradually providing more cross-industry and cross-domain applications.

5.2 Competitive Landscape of Industrial Internet in the Construction Machinery Field in China![]()