1. Research on the ADC Drug Market

Antibody drug conjugates (ADCs) are a new type of targeted anti-tumor drug that use monoclonal antibodies to deliver connected cytotoxic drugs directly to tumor cells, thereby enhancing the therapeutic activity of antibodies, increasing the targeting of cytotoxic drugs for killing tumor cells, and reducing their toxic side effects on normal tissues. Although ADCs have complex structures, they possess advantages such as high specificity, strong selectivity, and low cytotoxicity.

The US FDA has recently approved the market launch of five ADC drugs. In addition, dozens of ADC candidate molecules have entered clinical research worldwide. ADC drugs have become a research hotspot and development direction in tumor targeted therapy. The following are the five ADC drugs that have been approved for marketing by the FDA:

| product name | generic name | target | company | approval time | Main indications |

| Adcetris | Brentuximab Vedotin | CD30 | Takeda | August 19, 2011 | Hodgkin lymphoma |

| Kadcyla | Ado-trastuzumab Emtansine Injection | HER2 | Roche | February 22, 2013 | breast cancer |

| Besponsa | Inotuzumab ozogamicin | CD22 | Pfizer | August 17, 2017 | Acute lymphoblastic leukemia |

| Mylotarg | Gemtuzumab ozogamicin | CD33 | Pfizer | September 1, 2017* | Acute myeloid leukemia |

| Polivy | Polatuzumab vedotin-piiq | CD79b | Roche | June 10, 2019 | Relapsed or refractory diffuse large B-cell lymphoma |

*Note: September 1, 2017 is the re-approval date after the market was suspended.

Data source: FDA, Frost & Sullivan

Among the marketed ADC drugs, Roche Pharma's HER2-targeted breast cancer drug Kadcyla (ado-trastuzumab emtansine), which has performed best in the market, saw global sales reaching 979 million Swiss francs (about $1 billion) in 2018 according to the company's annual report. The success of Kadcyla has further fueled the enthusiasm for ADC research and development.

The indication for Kadcyla® is advanced HER2-positive breast cancer. Breast cancer (BC) is the most common malignant tumor among women worldwide. Among new breast cancer cases each year, approximately 3%-10% of women have distant metastases at the time of diagnosis. In early-stage patients, 30%-40% may develop into advanced breast cancer, with a 5-year survival rate of only 20%, and the overall median survival time is 2-3 years.[1]HER2 is a member of the human epidermal growth factor receptor (EGFR) family proteins, and as a tyrosine kinase receptor, it plays an important role in regulating numerous behaviors such as cell proliferation, differentiation, and survival. HER2-positive breast cancer accounts for about 20% to 25% of all breast cancers. This type of breast cancer has a higher degree of invasiveness and a poorer prognosis.[2]With the continuous emergence and widespread application of anti-HER2 drugs, the prognosis of HER2-positive breast cancer patients has improved significantly.

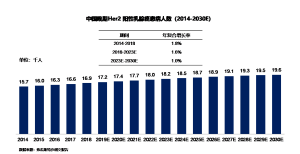

Between 2014 and 2018, the number of patients with advanced HER2-positive breast cancer in China increased from 15,700 to 16,900, with an annual compound growth rate of 1.8%. It is estimated that by 2023, the number of patients with advanced HER2-positive breast cancer in China will reach 18,200, followed by a continuous annual compound growth rate of 1.0%, reaching 19,600 by 2030.

As of the end of June 2019, three antibody-drug conjugate clinical trials in China have progressed to phase II and beyond. Among them, Roche's Ado-Trastuzumab emtansine has submitted an NDA application, BeiGene's BAT8001 has entered phase III clinical trials, and Rongchang Biopharmaceutical (Yantai) Co., Ltd. (hereinafter referred to as 'Rongchang Biopharmaceutical')'s RC48 has entered phase II clinical trials. The following table lists the anti-HER2 monoclonal antibody conjugate drugs that have entered phase II or above clinical trials in China:

| product name | Company Name | Indications | status |

Drug Evaluation Center Scheduling Date/ First Public Announcement Date of Clinical Trial |

| Ado-trastuzumab emtansine injection | Roche | HER2-positive breast cancer | Non-Disclosure Agreement | March 27, 2019 |

| HER2-positive gastric cancer | II/III | September 9, 2014 | ||

| BAT8001 | Biaotai | HER2-positive breast cancer | III | February 22, 2018 |

| RC48 | Rongchang Biology | HER2-positive breast cancer | II | May 3, 2018 |

| HER2-positive urothelial carcinoma | II | April 13, 2018 | ||

| HER2-positive gastric cancer | II | July 2, 2018 |

Data source: CDE, Frost & Sullivan report

In the future, ADC technology is expected to enter a phase of large-scale application due to the benefits of site-specific and quantitative conjugation technology, improved development and application of small molecule toxins, as well as the refinement of antibody modification techniques. Coupled with the widespread use of cancer combination therapies, ADC technology has the potential to achieve significant progress.

2. Market Research on Ib/IIIa Receptor Antagonists

Coronary heart disease, also known as 'atherosclerotic heart disease', refers to a condition where insufficient blood supply and myocardial hypoxia occur due to varying degrees of obstruction in the coronary arteries. It remains one of the 'number one killers' threatening human health worldwide. Antiplatelet aggregation can significantly reduce the risk of thrombotic events in patients with coronary heart disease, and guidelines both domestically and internationally recommend antiplatelet aggregation drugs as a Class I recommendation for the treatment of coronary heart disease.

There are many types of antiplatelet aggregation drugs, among which IIb/IIIa receptor antagonists have the characteristics of strong efficacy and stable effects, and are widely used in intravenous and coronary anticoagulation.

According to Frost & Sullivan data, in 2018, there were 850,000 PCI surgeries in China. Domestic IIb/IIIa receptor antagonists such as tirofiban hydrochloride have been launched on the market. The market size of tirofiban in China was about 200 million yuan in 2018.

3. Market analysis of anti-PD-1 monoclonal antibodies

PD-1 is mainly expressed on activated T lymphocytes, B cells, monocytes, NK cells, and antigen-presenting cells. As a key sentinel regulating immune cell function, once it binds to PD-L1 expressed on antigen-presenting cells, it blocks the conduction of the PD-1 signaling pathway, reduces T cell proliferation and cytokine release, and inhibits anti-tumor immunity.

Anti-PD-1 monoclonal antibodies are monoclonal antibodies targeting the PD-1 receptor, capable of inhibiting the binding of programmed death receptor-1 (PD-1) and its ligands (PD-L1 and PD-L2), and are used for the treatment of various solid tumors and hematological malignancies.

As of the end of June 2019, China has five marketed PD-1 inhibitors, including Bristol-Myers Squibb's Opdivo® (nivolumab), Merck Sharp & Dohme's Keytruda® (pembrolizumab), Shanghai Junshi Biopharmaceutical Technology Co., Ltd. (hereinafter referred to as 'Junshi Biosciences')'s Toripalimab® (tislelizumab), Innovent Biologics' Dabrucevimab® (daboclizumab), and Hengrui Medicine's Atezolizumab® (camrelizumab). In addition, BeiGene (Beijing) Biotechnology Co., Ltd. (hereinafter referred to as 'BeiGene') submitted an NDA application for Tislelizumab in 2018, and several other PD-1 inhibitors such as Biotec are in clinical trials. The following is a list of anti-PD-1 monoclonal antibody drugs that have been marketed or submitted for NDA in China:

| product name | Company Name | Indications | status | Listing time/Drug Evaluation Center Scheduling Date |

| Nivolumab | Pfizer | Locally advanced or metastatic non-small cell lung cancer with EGFR-negative and ALK-negative status | Listed | June 2018 |

| Pembrolizumab | Merck Sharp & Dohme | Inoperable or metastatic melanoma | Listed | July 2018 |

| Trimercept | Junshi Biology | Localized progression or metastatic melanoma | Listed | December 2018 |

| Sintilimab | Innovent Biologics | Recurrent or refractory classical Hodgkin lymphoma | Listed | December 2018 |

| Camrelizumab | Hengrui Medicine | Recurrent or refractory classical Hodgkin lymphoma | Listed | May 2019 |

| Tislelizumab | Baiji Shenzhou | Recurrent or refractory classical Hodgkin lymphoma | Non-Disclosure Agreement | August 2018 |

Gastric cancer cells with Epstein-Barr virus (EBV) are known as Epstein-Barr virus-associated gastric carcinoma (EBVaGC). EBVaGC is a subtype of gastric cancer with unique clinical and pathological characteristics, and it is strongly associated with age. After EBV infection, the expression of PD-L1 and PD-L2 is upregulated, making EBVaGC more sensitive to PD-1/PD-L1 immunotherapy.

EBVaGC is strongly correlated with age. Between 2014 and 2018, the number of newly diagnosed EBV-positive gastric cancer patients in China increased from 32,000 to 36,300, with an annual compound growth rate of 3.2%. It is estimated that by 2023, the number of newly diagnosed EBV-positive gastric cancer patients in China will reach 41,900, followed by a continuous annual compound growth rate of 2.6%, reaching 50,300 by 2030.

4. Market Analysis of Anti-CD20 Monoclonal Antibodies

Since the approval of rituximab (trade name Rituxan) as the first anti-CD20 therapeutic monoclonal antibody in 1997, this class of drugs has developed rapidly. Rituxan combined with chemotherapy has become the standard first-line treatment recommendation for most B-cell NHL patients, but there are still 10% to 15% of patients who respond poorly or not at all to rituxan combined with chemotherapy, or even relapse after effective treatment.

Lymphoma is a malignant tumor of lymphocytes that originates in lymph nodes and/or extranodal lymphoid tissues, growing as solid tumors in tissues and organs rich in lymphoid tissue. Lymphomas can be divided into Hodgkin lymphoma (HL) and non-Hodgkin lymphoma (NHL). NHL is a common hematopoietic system malignancy in clinical practice. Most NHLs originate from B lymphocytes, and about 95% of NHL patients in China are CD20 positive. Common types of NHL include diffuse large B-cell lymphoma (DLBCL), mucosa-associated lymphoid marginal zone lymphoma (MZL), follicular lymphoma (FL), chronic lymphocytic leukemia/small lymphocytic lymphoma (CLL/SLL), mantle cell lymphoma (MCL), and others.

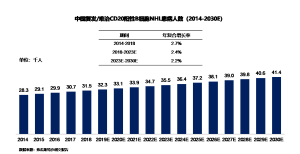

Between 2014 and 2018, the number of relapsed/refractory CD20-positive B-cell NHL patients in China increased from 28,000 to 32,000, with an annual compound growth rate of 2.7%. It is estimated that by 2023, the number of NHL patients will reach 36,000, with an annual compound growth rate of 2.4%. Subsequently, the number of patients will continue to grow at a compound annual growth rate of 2.2%, reaching 41,000 by 2030.

As of the end of June 2019, there were only two marketed anti-CD20 monoclonal antibody injections in China: Roche's Rituximab (Mylotrexate) and Fosun Pharma's Hanlimab (Rituximab biosimilar). Innovent Biologics has submitted an NDA application, while the anti-CD20 monoclonal antibody injections of Shenzhen Celltech, Hisun Pharma, Jiahe Biotech, Zhengda Tianqing, and Hualan Biotech have progressed to phase III clinical trials. The following table lists the anti-CD20 monoclonal antibodies that have entered phase III clinical trials or are on the market in China.

| product name | Company Name | Indications | status |

Listing time/ Acceptance date of the Center for Drug Evaluation First Public Notice Date |

| Merck Sharp & Dohme | Roche Pharmaceuticals | NHL | Listed | March 15, 2000 |

| HANLIKANG® | Fosun Pharma | NHL | Listed | February 22, 2019 |

| RA | III | August 15, 2018 | ||

| IBI301 | Innovent Biologics | DLBCL | Non-Disclosure Agreement | June 27, 2019 |

| SCT400 | Shenzhou Cell | DLBCL | III | June 6, 2016 |

| NA | Hisun Pharmaceutical | DLBCL | III | July 3, 2018 |

| GB241 | Jiahé Biology | DLBCL | III | November 28, 2018 |

| TQB2303 | Sunny and clear | DLBCL | III | December 11, 2018 |

| HL03 | Hualan Biology | DLBCL | III | April 17, 2019 |

5. Market Research on Anti-VEGF Humanized Monoclonal Antibodies

The recombinant anti-VEGF humanized monoclonal antibody is an IgG1 monoclonal antibody specifically designed for the treatment of fundus diseases. It can inhibit the binding of VEGF to its receptor VEGFR by neutralizing VEGF, thereby suppressing angiogenesis. It is intended for the treatment of wet age-related macular degeneration (wAMD), diabetic macular edema (DME), and diabetic retinopathy (DR) among other fundus diseases.

Age-related macular degeneration (AMD) is an age-related structural change in the retina's macular area, mainly caused by irreversible vision loss or impairment due to retinal pigment epithelial cells and retinal degenerative changes. Clinically, AMD is divided into dry AMD and wet AMD (wAMD), with wAMD being more likely to lead to severe vision loss. Its main pathological feature is the formation of new blood vessels in the choroid of the macular area. There are many physical treatment methods for wAMD, but none can improve the patient's vision. Since the advent of anti-VEGF drugs over a decade ago, they have been widely used as first-line treatments for wAMD in clinical practice. In 2006, the FDA approved Lucentis® (ranibizumab) for marketing in the United States, and it has now been approved for six indications including wet AMD and diabetic macular edema (DME). In 2012, the NMPA approved ranibizumab for the treatment of wAMD, making it the first anti-VEGF biologic drug for ophthalmology in China.

WAMD mostly occurs in individuals over the age of 45, with the incidence increasing with age. With the acceleration of aging in China and the popularization of electronic products, the number of people suffering from blindness caused by WAMD is on the rise year by year. Between 2014 and 2018, the number of WAMD patients in China increased from 46.21 million to 52.57 million, with an annual compound growth rate of 3.3%. It is estimated that by 2023, the number of WAMD patients in China will reach 55.65 million, followed by a continuous annual compound growth rate of 0.8%, reaching 58.83 million by 2030.

As of the end of June 2019, in the field of treatment for fundus diseases, three anti-VEGF drugs have been approved for marketing in China: ranibizumab, aflibercept, and conbercept. The following is a list of anti-VEGF drugs that have been marketed in China for the treatment of fundus diseases:

| product name | Company Name | Indications | status | Listing time |

| Lezru monoclonal antibody | Novartis Pharmaceuticals | wet age-related macular degeneration | listing | December 2011 |

| Abemaciclib | Bayer Pharma | Wet age-related macular degeneration diabetic macular edema | listing | February 2018 |

| Conbercept | Chengdu Kanghong Biotechnology Co., Ltd. | wet age-related macular degeneration | listing | November 2013 |

6. Market Analysis of Anti-Trop2 Monoclonal Antibody Conjugates

Triple negative breast cancer (TNBC) is a subtype of breast cancer based on the expression status of estrogen receptor (ER), progesterone receptor (PR), and human epidermal growth factor receptor 2 (HER2). TNBC refers to breast cancer that is ER(-), PR(-), and HER2(-). TNBC has become a research hotspot among breast cancer subtypes because of its unique biological behavior, which makes it more aggressive than other subtypes, has a shorter disease-free survival period, a higher rate of soft tissue and visceral metastases, and a higher mortality rate within 5 years compared to non-TNBC patients.

Approximately 10-15% of breast cancers are triple-negative breast cancers, and Trop2 (trophoblastic cell surface glycoprotein antigen 2) is overexpressed in 80% of TNBC patients, while it is lowly expressed or not expressed at all in normal tissues. Therefore, Trop2 has become an ideal anti-TNBC target.

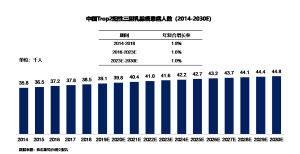

The number of newly diagnosed Trop2-positive triple-negative breast cancer patients in China increased from 36,000 to 39,000, with an annual compound growth rate of 1.8% during this period. With the younger age of onset of breast cancer, it is estimated that by 2023, the number of newly diagnosed Trop2-positive triple-negative breast cancer patients in China will reach 42,000. Subsequently, the number of new patients will continue to grow at an annual compound rate of 1.0%, reaching 45,000 by 2030.

BAT8003 is an innovative drug independently developed by Bai'ao Tai. It is the first product in China to submit an IND for this target, and there are no similar products on the market globally.

7. Market Analysis of Neuromyelitis Optica Spectrum Disorders Market

Neuromyelitis optica spectrum disorder (NMOSD) is a highly recurrent and disabling disease, with over 90% of patients experiencing a multi-phase course. Approximately 60% of patients relapse within one year, and 90% within three years. Most patients are left with severe visual impairment and/or limb dysfunction, as well as urinary and fecal disorders. In 2018, the National Health Commission and five other departments jointly formulated the 'First Batch of Rare Diseases Catalogue', in which neuromyelitis optica was included.

Between 2014 and 2018, the number of patients with neuromyelitis optica spectrum disorder (NMOSD) in China increased from 56,000 to 57,000, with an annual compound growth rate of 0.5%. It is estimated that by 2023, the number of NMOSD patients in China will reach 59,000, followed by a continuous annual compound growth rate of 0.3%, reaching 60,000 patients by 2030.

[1]Anonymous. Expert Consensus on the Clinical Diagnosis and Treatment of Advanced Breast Cancer in China (2018 Edition) [J]. Chinese Journal of Oncology, 2018, 40(9):703.

[2]Ross J S, Slodkowska E A, Symmans W F, et al. The HER-2 receptor and breast cancer: ten years of targeted anti-HER-2 therapy and personalized medicine [J]. Oncologist, 2009, 14(4): 320-368.