Based on research and analysis of the Chinese IT infrastructure market, Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') has released the latest 'White Paper on China's IT Infrastructure Industry'. The white paper points out that driven by factors such as increased demand for enterprise digital transformation and national policy support, by the end of 2018, the scale of the Chinese IT infrastructure market had reached 225.94 billion yuan, of which the traditional IT infrastructure market size was 133.53 billion yuan (accounting for 59.1%) and the cloud infrastructure market size was 92.41 billion yuan (accounting for 40.9%). In the next five years, driven by the rapidly growing demand for large-scale computing power in the mobile internet era and the need for rapid release and deployment, cloud infrastructure will be further popularized among downstream users (especially enterprise users). Frost & Sullivan expects that the scale of the Chinese IT infrastructure industry market is expected to reach 704.09 billion yuan by 2023.

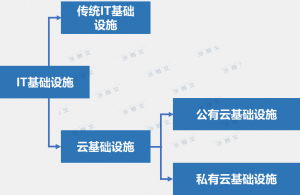

IT infrastructure definition and classification

IT infrastructure refers to the collection of IT hardware resources and basic software resources required to support IT environments for governments, enterprises, and individuals with special needs. It mainly includes computing resources, storage resources, network resources, and underlying software that enables virtualization and manages servers. Depending on the deployment environment, IT infrastructure can be divided into traditional IT infrastructure and cloud infrastructure. Infrastructure deployed in non-cloud environments is considered traditional IT infrastructure, while infrastructure deployed in cloud computing environments is considered cloud infrastructure, which can be further divided into public cloud infrastructure and private cloud infrastructure.

IT infrastructure classification

Source: Drawn by Frost & Sullivan Research

Cloudification, customization, and intelligence are the three major development directions of the IT infrastructure industry in the future.

1. Cloudification: As the world enters a period of digital transformation, it has become increasingly common for traditional enterprises to move towards digitalization. Cloud computing services meet the 'lightweight' and 'on-demand' information technology needs of enterprises in the internet era. At the same time, the continuously decreasing prices make cloud computing services an attractive choice for enterprises during their digital transformation process. The 'cloudification' of the IT infrastructure industry will become an irreversible trend.

2. Customization: The diversification of market demand has provided a broader development space for the IT infrastructure industry, but it also places higher demands on the technical level, product variety, and service offerings of IT infrastructure providers. More and more suppliers are making corresponding adaptations in their products and services, providing customized and proprietary infrastructure for customers. This not only improves performance but also saves costs for customers, enhancing the company's competitiveness within the industry.

3. Intelligence: The application of AI in various industries is showing a trend of explosive growth, and the industrialization of AI technology will become inevitable. For cloud computing service providers, the large amount of data accumulated on cloud computing platforms and their massive computing power provide fundamental resource support for AI technology. The application of AI technology will also enrich the functions and use cases of cloud computing services. The accelerated integration of AI and cloud computing is inevitable. The launch of AI services and products based on cloud computing will open up a new growth area for cloud infrastructure enterprises, while also promoting business innovation and transformation among enterprise customers.

The industry competition landscape is relatively concentrated, and Chinese manufacturers are on the rise.

The IT infrastructure industry in China includes all enterprises that deliver IT infrastructure resources in various forms. In the past few years, traditional IT infrastructure providers have dominated the market share across the entire industry scale. With the development of cloud computing technology, more and more enterprises are choosing to 'cloudify' their own IT architectures, and the focus of the IT infrastructure industry's development has gradually shifted towards the cloud. Taking Huawei as an example, Huawei has gained a leading position in the Chinese IT infrastructure market with a 23.1% market share, thanks to its years of technical accumulation and user reputation in the hardware device market, as well as its comprehensive deployment across both traditional IT infrastructure and cloud infrastructure markets. Inspur ranks second in the industry with its outstanding performance in the market over the past two years.

Market share of China's IT infrastructure industry, 2018

Source: Software compilation by fsTEAM, compiled by Frost & Sullivan Data Center

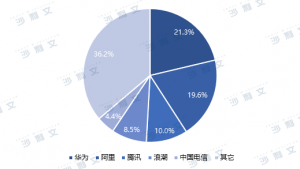

The China cloud infrastructure market encompasses all providers that deliver IT infrastructure resources through hardware, software, and services. The industry is relatively concentrated, with five companies—Huawei, Alibaba, Tencent, Inspur, and China Telecom—accounting for 63.8% of the market share.

Market share of Chinese cloud infrastructure providers, 2018

Source: Software compilation by fsTEAM, data compiled by Frost & Sullivan