Frost & Sullivan (Frost & Sullivan, abbreviated as 'Frost & Sullivan') focuses on the digital store and electronic price tag markets and has officially released the 'Global and Chinese Electronic Price Tag Market and Digital Store Market Research Report'. The report includes information on the following aspects: analysis of the global electronic price tag market and competitive landscape, analysis of the Chinese electronic price tag market and competitive landscape, an overview of the global digital store market, as well as relevant economic data.

I. Analysis of the Global and Chinese Electronic Price Label Market and Competitive Landscape

-

Definition and Classification of Electronic Price Labels Market

Electronic price tags, also known as electronic shelf labels (ESL), are electronic display devices with information sending and receiving capabilities. They can display text, numbers, pictures, color blocks, barcodes, and QR codes. They are mainly used in supermarkets, convenience stores, and other electronic displays where price information is displayed. An electronic price tag system typically includes communication base stations, software system cloud platforms, handheld PDAs, electronic price tag devices, and accessories.

According to the different screen materials, mainstream electronic price tags on the market can be divided into EPD (Electronic Paper Display) and LCD (Liquid Crystal Display) electronic price tags; based on different data transmission protocols, electronic price tags can also be categorized into WiFi transmission, Bluetooth communication, 433MHz, and other specifications.

-

Global electronic price tag market industry chain

The upstream of electronic price tags mainly focuses on raw material production, including display screens, electronic circuit boards, motherboard chips, batteries, device casings, etc. Display screens are the most important raw material for electronic price tags, with electronic paper displays being the majority. The display medium for electronic paper displays is electronic ink, while other raw materials include liquid crystal displays, etc.

The midstream of electronic value-added tax (e-VAT) solutions mainly includes providers of e-VAT system solutions, responsible for the technical solutions, product design, production delivery, and after-sales service of e-VAT systems. This encompasses a comprehensive solution including hardware, software, and services.

The downstream of electronic price tags mainly consists of retail enterprises, primarily used in supermarkets/giant stores, department stores, convenience stores, and specialty stores. Some electronic price tags are also applied in industrial scenarios, such as factory warehousing and production management.

Source: Frost & Sullivan report

-

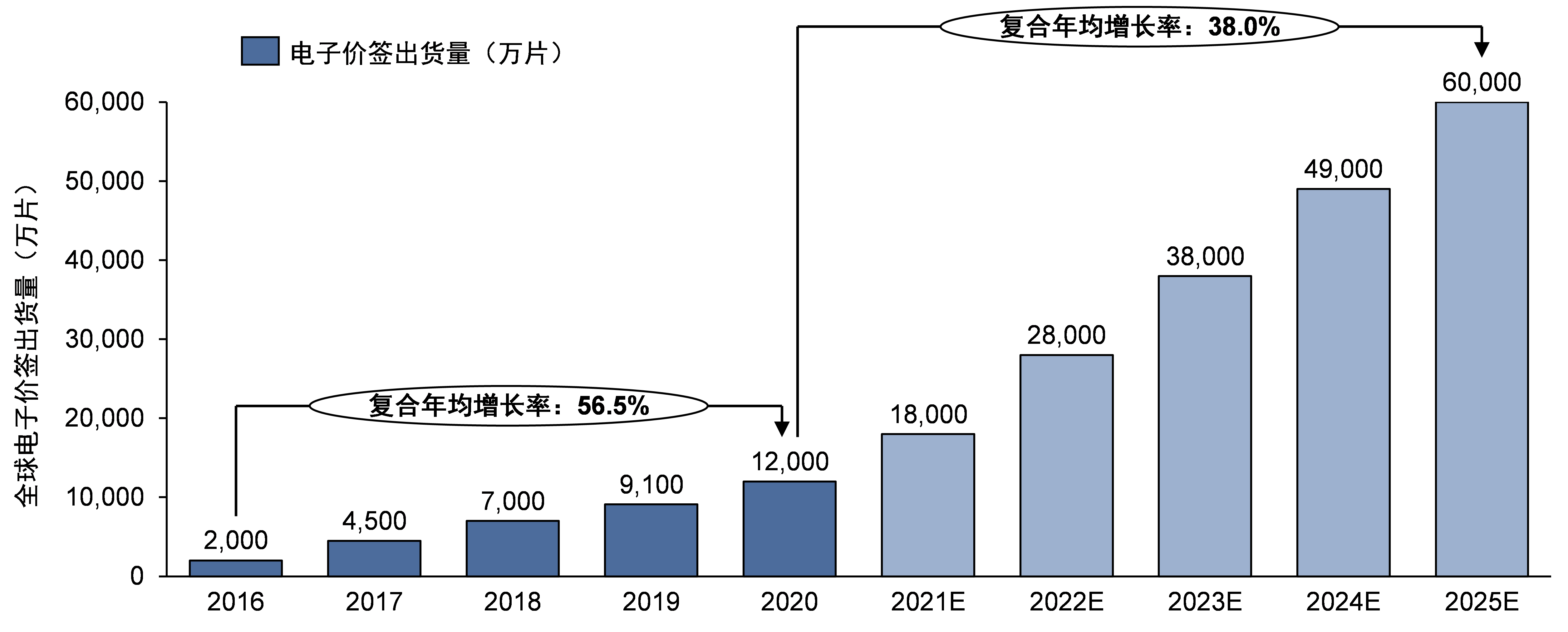

Global electronic price tag market size

In terms of electronic tag shipments, the global electronic tag market has been growing rapidly, increasing from about 20 million tags in 2016 to 120 million tags in 2020, with a compound annual growth rate of up to 56.5%. With the continuous rise in global labor costs, the popularization of technologies such as mobile payment, and fierce competition in online channels, electronic tags are expected to become an important solution for reducing offline store operating costs and be widely applied to more offline stores and scenarios. The penetration rate of electronic tags is expected to further increase. It is estimated that by 2025, global electronic tag shipments will reach 600 million tags, with a compound annual growth rate of 38.0% between 2020 and 2025.

Source: Frost & Sullivan report

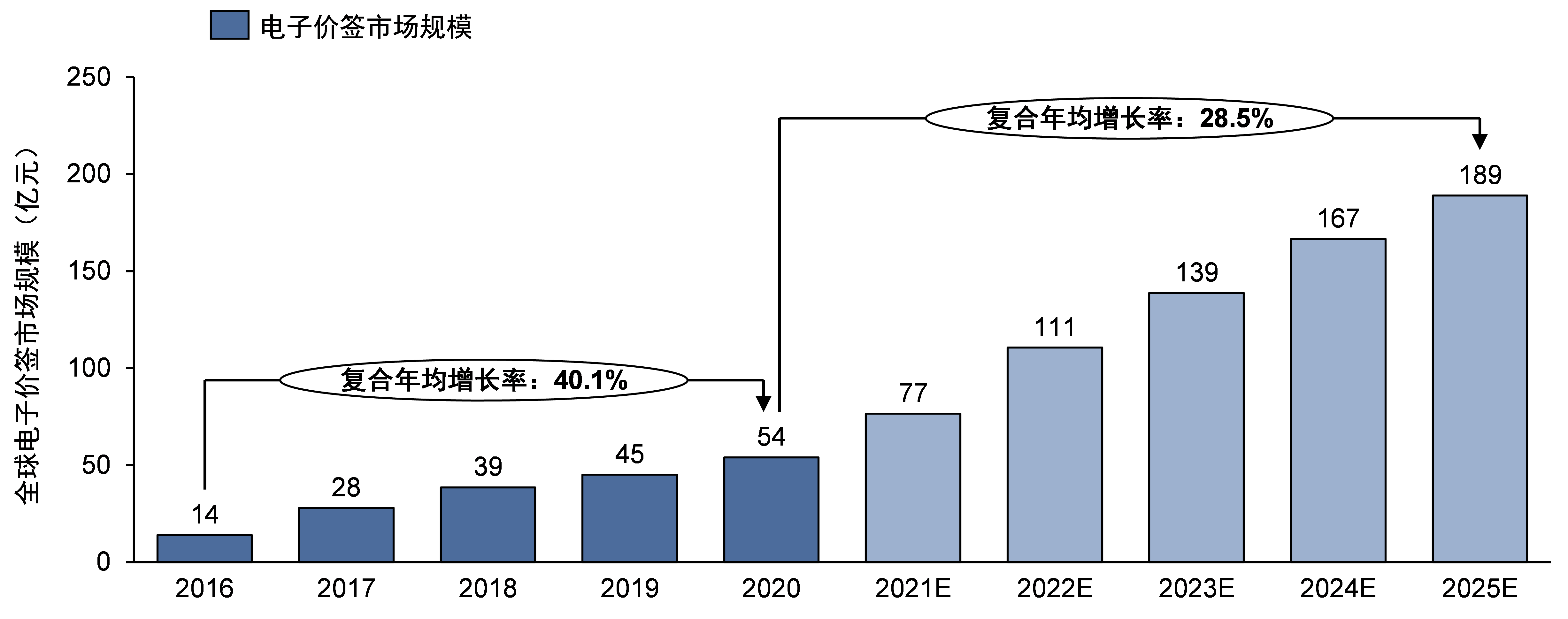

In terms of retail sales, the global electronic price tag market size increased from 1.4 billion yuan in 2016 to 5.4 billion yuan in 2020, with a compound annual growth rate of 40.1%. As labor costs continue to rise, electronic price tags, as an important tool for reducing retail store operating costs, are expected to be increasingly used in major retail stores in the future. It is estimated that global electronic price tag retail sales will continue to grow rapidly during the forecast period, reaching 18.9 billion yuan by 2025, with a compound annual growth rate of 28.5% from 2020 to 2025.

Source: Frost & Sullivan report

-

Market scale of electronic price tags in China

Electronic price tag shipments refer to the quantity produced by manufacturers that is shipped to agents (or intermediaries), commonly used for statistical analysis of the scale and level of the electronic price tag industry and its participants.

The shipment volume of electronic price tags in China increased from about 2 million units in 2016 to about 8 million units in 2020, with a compound annual growth rate as high as 41.4%. In the future, the shipment volume of electronic price tags in China is expected to maintain high-speed growth and is projected to grow to 20 million units by 2025, with a compound annual growth rate of about 20.1% during the period from 2020 to 2025; the market size of electronic price tags in China (measured by retail sales based on shipments) increased from about 150 million yuan in 2016 to about 400 million yuan in 2020, with a compound annual growth rate of about 27.8%. In the next few years, with the normalization of epidemic prevention and control, the improvement of the supply chain, continued growth in market demand, and the collaborative advancement of technological progress and smart scenarios, electronic price tags will gradually be applied in more and more fields. The market size of electronic price tags is expected to recover and continue to grow rapidly. It is projected that by 2025, the market size of electronic price tags in China will increase to 880 million yuan, with a compound annual growth rate of about 17.1% during the period from 2020 to 2025.

-

Global and Chinese Electronic Price Tag Market Competition Landscape

The global electronic price tag market is highly concentrated, with the top five suppliers accounting for approximately 93.1% of the market share based on shipments in 2020. The top five electronic price tag suppliers globally are SES, Pricer, Hanshow (Han Schäuble), SoluM, and DisplayData. The global EPD electronic price tag market is also highly concentrated, with the top five suppliers accounting for approximately 92.6% of the market share based on EPD electronic price tag shipments in 2020.

The top five global EPD electronic price tag suppliers are SES, Hanshow, Pricer, SoluM, and DisplayData.

There are about more than 30 major electronic price tag suppliers in China. Based on the shipments of electronic price tags in 2020, the top five electronic price tag suppliers together shipped approximately 6.3 million pieces, accounting for nearly 80% of the market share, indicating a high concentration of the Chinese electronic price tag market. Among them, Hanshou occupies more than half of the market share in the Chinese electronic price tag market.

-

Global e-tagging market drivers

Regarding the driving factors of the e-signature market, firstly, this isThe development of new retail drives the demand for store digitization and efficient management;Secondly,The continuously climbing labor cost will also lead more retailers to use electronic price tag systems in their stores.To effectively improve management efficiency and enhance corporate competitiveness; thirdly,Technological progress has rapidly enhanced the performance and functionality of electronic price tags systems.This enables the implementation of rich features such as rapid picking, precise marketing, traffic integration, and shared warehousing, thereby enhancing business value for customers.

-

Future Trends of the Global Electronic Price Label Market

According to Frost & Sullivan research, the development trend of the electronic price tag market will include the following points: Electronic price tags will collaborate with other related products to promote the digital development of retailing. Additionally, as the prices of electronic price tags continue to decrease, more scenarios will be empowered to achieve precise marketing, significantly increasing the retail conversion rate.

-

Global e-tagging market entry barriers

Barriers to entry into the e-price tag market andExperience in raw material supply and supply chain system managementanddownstream cooperation relationshipsRelevant.

The upstream of the electronic price tag market industry chain consists of raw material manufacturers. Leading global electronic price tag suppliers, relying on their strong cost control and market expansion capabilities, have established long-term stable supply relationships with major electronic paper display manufacturers. They make full use of the scale advantage of cooperation to ensure stable shipments and prices. For new entrants into the competition, the ability to penetrate the upstream raw material supply system is particularly important. At the same time, it is also crucial for new industry entrants to have a deep understanding of new retail and the new generation of information technology, possess capabilities covering raw material procurement, electronic price tag production and processing, intelligent hardware and software management operations, as well as establish close cooperative relationships with downstream global retail giants.

II. Global Digital Store Market Overview

-

Definition and Introduction to Digital Stores

A digital store is composed of 'physical' stores and 'digital' software and hardware. Stores typically base themselves on electronic price tags that connect to goods, reaching out to customers through digital interactive screens, mobile checkout counters, in-store self-service checkout, facial recognition, electronic price tags, virtual reality (VR), augmented reality (AR), and robot services. Operations such as consumer behavior big data analysis, precise marketing and intelligent placement, and efficient centralized store management are completed within cloud platforms and digital store software systems, thereby realizing the empowerment of stores by digitization.

-

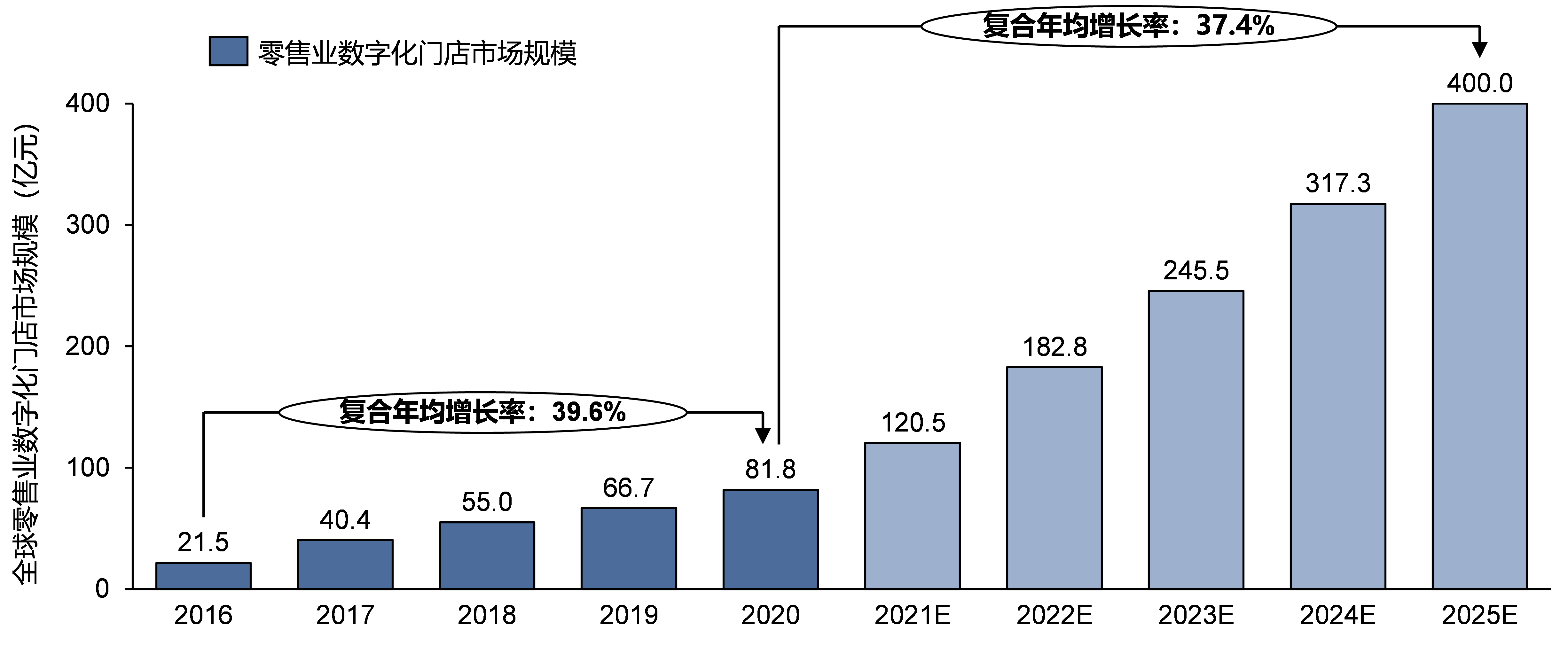

Global retail digital store market size

The market scale of digital stores in the global retail industry represents the total investment made by retailers around the world to build these digital stores. The investments mainly include the procurement of various intelligent software and hardware such as electronic price tags, digital interactive screens, mobile checkout counters, in-store self-service checkout terminals, service robots, AI cameras, etc. In recent years, as global retailers have begun their digital transformation, the market scale of digital stores in the global retail industry has grown from 2.15 billion yuan in 2016 to 8.18 billion yuan in 2020, with a compound annual growth rate of 39.6%. In the future, with more retailers undergoing digital transformation and continuous optimization of digital solutions, the market scale of digital stores in the global retail industry will further expand, reaching 40 billion yuan by 2025.

Source: Frost & Sullivan report