scope of the study

- Global and China's wind power market

- China's onshore wind power market

- China's onshore wind power operation and maintenance market

- China offshore wind power market

- China offshore wind power operation and maintenance market

Time range

- Base year: 2021

- Historical Years: 2017 - 2021

- Forecast Years: 2022 - 2026

1. Overview of Wind Power Market Development

1.1. Definition and Classification of Wind Power

Wind power is the abbreviation for wind-driven electricity generation, which is a type of renewable and clean energy. Wind energy drives the rotation of wind turbine blades, which then increases speed through a gearbox, and generators convert this wind energy into electrical energy.

Based on different geographical locations, including onshore and offshore wind power.

Offshore wind power can be divided into intertidal zones, subtidal mudflats, nearshore areas, and farshore areas based on the different water depths of the sea area where the wind farm is located.

Due to differences in wind energy resources, power grids, load conditions, and other factors among different countries around the world, there is no internationally unified standard for the classification of onshore wind power.

1.2. Wind Power Industry Industrial Chain

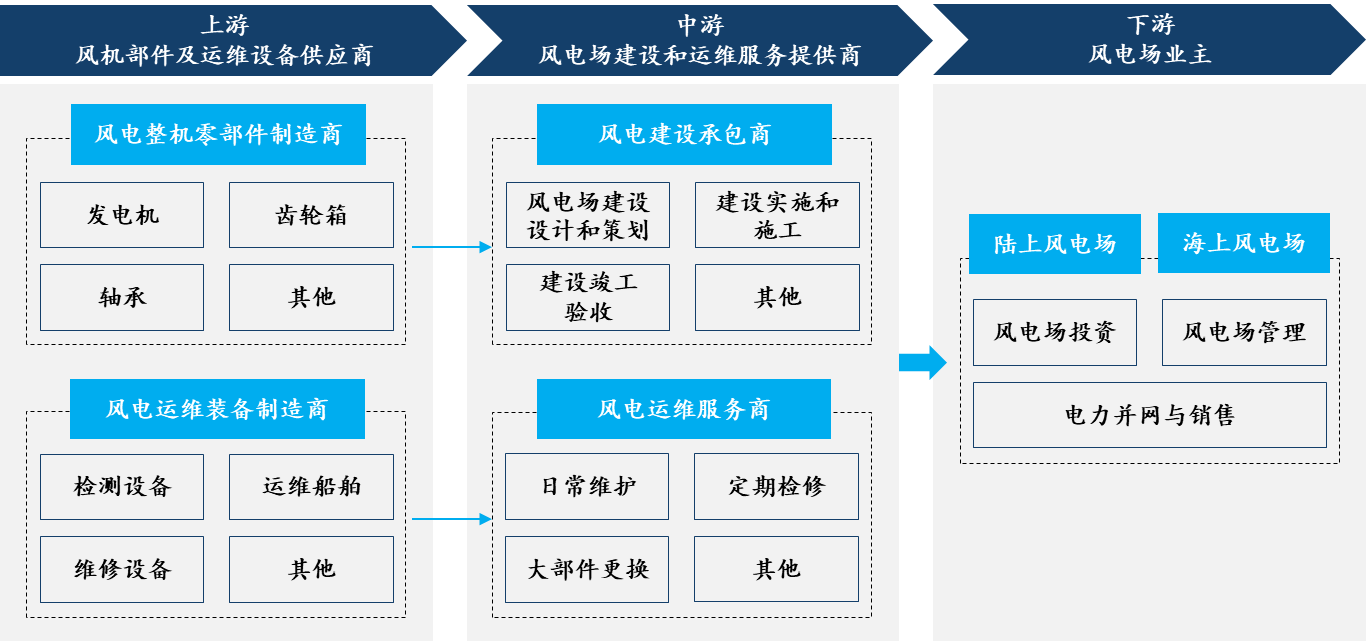

The industrial chain of the wind power industry includes two major parts: wind power construction and wind power operation and maintenance. The upstream of wind power construction includes wind turbine components, the midstream includes wind farm construction, and the downstream includes onshore and offshore wind farms; the upstream of wind power operation and maintenance includes operation and maintenance equipment manufacturers, the midstream includes operation and maintenance service providers, and the downstream includes onshore and offshore wind farm owners.

Data source: Public information collation, Frost & Sullivan

(1) Upstream: Manufacturers of wind turbine components and operation and maintenance equipment

Wind power component manufacturers mainly provide suitable parts for wind power construction services, such as generators, gearboxes, bearings, etc. Wind power operation and maintenance equipment manufacturers primarily offer a variety of operation and maintenance equipment for wind power operation and maintenance services, including operation and maintenance ships, inspection equipment, repair equipment, etc., such as operation and maintenance mother ships, drones, underwater robots, etc. Among them, operation and maintenance ships are one of the important tools for offshore wind farm operation and maintenance, creating convenient conditions for offshore wind turbine operation and maintenance services.

(2) Midstream: Wind farm construction and operation service providers

The main participants in the midstream of the wind power industry chain are wind power construction contractors, subcontractors, and operation and maintenance service providers. The core parts of wind farm construction implementation include: preliminary project preparation stage design (including subcontract bidding, personnel training, etc.), construction project implementation and construction, construction completion acceptance, and other links. The main contents of wind turbine operation and maintenance include daily maintenance, regular inspections, equipment tours, technical upgrades, major component replacements, safety management, etc. The quality and effectiveness of wind turbine operation and maintenance work are directly related to the reliability of the unit's operation, which in turn affects power generation.

(3) Downstream: Wind farm owners

The wind farm owner is the investor and developer of the wind farm, responsible for the construction, grid connection, and operation of the wind farm. Currently, there are few entities in China participating in wind farm investments; most are enterprises with state-owned capital backgrounds and strong financial strength, including China Huaneng Group, China Datang Group, China Huadian Group, China Guodian Group, China Power Investment Group, State Power Investment Corporation and CGN Nuclear Power. The market concentration is relatively high. According to statistics from CWEA (Chinese Wind Energy Association, Wind Energy Professional Committee of the Renewable Energy Society), as of the end of 2021, the cumulative installed capacity of the top 15 wind farm owners exceeded 250 million kilowatts, accounting for a total of 73.2%. The concentration of offshore wind power installed capacity is even higher. According to CWEA statistics, as of the end of 2021, there were a total of 31 offshore wind farm owners, among which six had cumulative installed capacity reaching over one million kilowatts. The six enterprises with a million-kilowatt installed capacity scale are: Three Gorges Group, Huaneng Group, State Power Investment Corporation, Guodian Investment Corporation, CGN Nuclear Power and Guangdong Electric Power. Their combined installed capacity accounts for 72.6% of the total offshore wind power cumulative installed capacity, indicating a high market concentration.

2. Global wind power market development history and market scale overview

2.1 Development History of the Global Wind Power Market

The global wind power industry originated in Europe, and with technological progress, increasingly mature markets, and growing energy pressure, wind power, as one of the important clean energies, has gained a consensus for development worldwide.

From 2001 to the present, the global wind power market has gone through four stages of development. The first stage was from 2001 to 2009, a period of accelerated development; the second stage was from 2010 to 2014, a period of phased adjustment; the third stage was from 2015 to 2020, a period of large-scale development; and the fourth stage is from 2021 to the present, a period of mature development.

Data source: Public information compiled by Frost & Sullivan

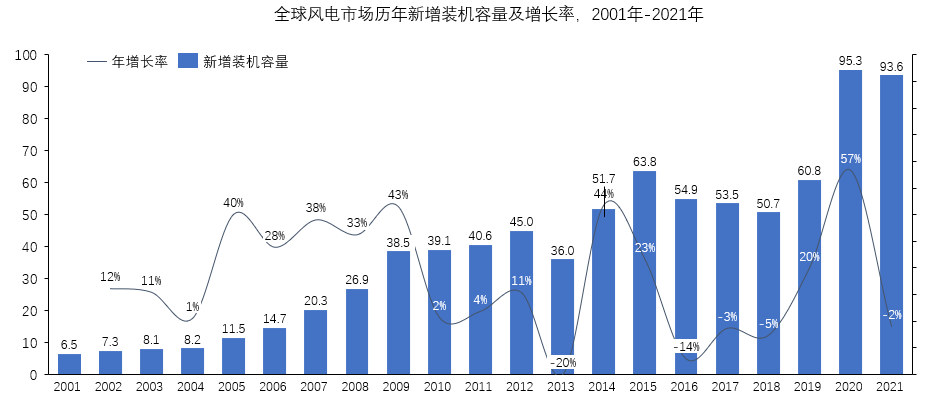

The first phase of wind power development was between 2001 and 2009. During this period, the wind power market went through a transition from start-up to accelerated development. Major countries around the world promoted market development through mechanisms such as policy support and market subsidies. The wind power market during this time mainly focused on onshore wind energy. Calculated by new installed capacity, the global wind power market was 6.5 GW in 2001 and 38.5 GW in 2009, with an annual compound growth rate of 24.9%.

The second phase of wind power development was between 2010 and 2014. Due to the rapid development in the early stages, the wind power market entered a stage of adjustment during this period. During this time, the growth rate of new installed capacity significantly slowed down. For example, in 2010 and 2011, the growth rate was less than 5% for two consecutive years, and in 2013 it even dropped to -20%, indicating that the wind power market was in a volatile period. The annual compound growth rate during this period decreased from 24.9% in the first phase to 7.2%.

The third phase of wind power development is between 2015 and 2020. The wind power market has gone through a market adjustment period in the second phase and entered a new period of large-scale growth. During this phase, relevant technologies for the wind power market gradually matured, including the development and design of wind turbines, and the construction of wind farms, all of which have been improved to a certain extent. Starting from this period, the offshore wind power market began to enter a rapid development phase, gradually showing a higher installed capacity growth rate than onshore wind power. The annual compound growth rate of new installed capacity in the third phase was 8.4%, higher than that in the second phase.

The fourth phase of wind power development spans from 2021 to the present. Due to the global energy crisis, wind power generation has been applied to varying degrees in various countries around the world. The global wind power market as a whole is gradually entering a mature development stage, especially with a slowdown in growth rates in the onshore wind market. In the coming period, the global wind power market will generally show a stable development trend, gradually shifting from a market dominated by onshore wind power to one characterized by large-scale offshore wind development.

2.2. Global wind power market new installed capacity and growth rate over the years, 2001 - 2021

According to the data from the Global Wind Energy Council (GWEC), the new installed capacity and growth rate of the global wind power market over the years are shown in the following chart.

From 2001 to 2009, the global wind power market entered its first phase, with a total installed capacity of 142 GW; from 2010 to 2014, it entered the second phase, with a total installed capacity of 212.4 GW; from 2015 to 2020, it entered the third phase, with a total installed capacity of 379.0 GW; since 2021, the global wind power market has entered the fourth phase, and it is expected that the scale of installed capacity will continue to increase.

Source: GWEC, Frost & Sullivan

2.3. Global wind power market new installed capacity, by onshore and offshore wind power, 2016-2021

In recent years, countries and regions around the world have gradually increased their attention to carbon emissions. Accelerating the pace of energy transformation and continuously building green and sustainable economic models have greatly promoted the rapid development of the wind power market. As a clean energy source, the cost of wind power has decreased rapidly with the expansion of installed capacity and technological improvements, further driving it to become a key development measure for various countries and regions to reduce carbon emissions and achieve carbon neutrality goals.

The global wind power market, calculated by new installed capacity, saw a slow growth from 54.9 GW in 2016 to 72.5 GW in 2021, with an annual compound growth rate of 6.6%. The offshore wind power market, on the other hand, grew rapidly from 2.2 GW in 2016 to 21.1 GW in 2021, with an annual compound growth rate of 57.2%, far exceeding that of the onshore wind power market. In terms of annual compound growth rate, the global offshore wind power market is in a stage of rapid growth.

Other regions of the global wind power market account for a smaller proportion, such as Latin America and the Middle East, which have a low share in the new installed capacity of the global wind power market and are less significant in terms of volume.