CNC machine tools refer to machine tools equipped with a program control system, where the operation and movement of the machine follow instructions composed of specific codes and symbols issued by this program control system. CNC machine tools typically consist of a CNC system, servo system, measurement feedback system, the main body of the machine tool, and auxiliary devices. Among them, the CNC system is the core part of the CNC machine tool, mainly converting processing information expressed by part machining programs into processing instructions, controlling the machining trajectory and logical actions, and producing parts that meet the requirements. Since 2020, China's machine tool exports have shown an annual growth trend. Overseas has become an incremental market for China's CNC machine tool industry. The upgrading of downstream industries such as consumer electronics, precision molds, and automotive manufacturing has given rise to a number of high-speed and high-precision CNC machine tool enterprises.

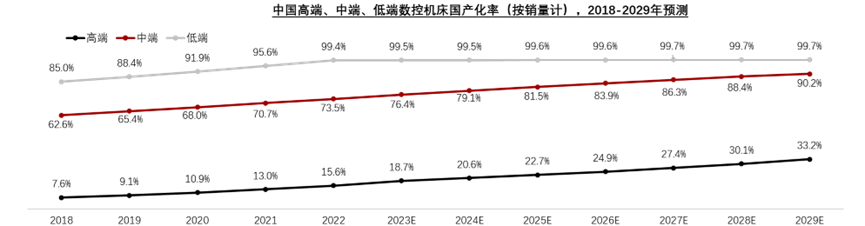

Between 2018 and 2022, the localization rate of CNC machine tools in China continued to rise. The localization rate of low-end CNC machine tools has reached complete self-sufficiency, with the rate increasing from 62.6% to 73.5%, basically achieving domestic substitution. Currently, domestic CNC machine tool enterprises mainly including Century CNC and Haitian Precision Engineering are basically able to produce mid-range CNC machine tools that meet the needs of domestic manufacturing. Domestic CNC machine tools have weaker competitiveness in the high-end market, with a localization rate of 15.6% for high-end CNC machine tools in 2022.

With the upgrading of downstream industry demand and the development of technologies such as big data and the Internet of Things, the market's demand for machine tools is also evolving. In the future, global machine tools will develop in the direction of high speed, high precision, intelligence, high efficiency and systematization, as well as integration.

Chart 1: Global High-End CNC Machine Tool Market Size (by Sales), Forecast for 2018 - 2029

Data source: Frost & Sullivan, LeadLeo Research Institute

From 2018 to 2022, the global machine tool output value maintained an upward trend overall. Metal cutting machine tools are currently the mainstream type of machine tools produced and used in the market, accounting for about 70% of the total global machine tool output value. As a major manufacturing country, China is the world's largest machine tool producer. From 2018 to 2022, global machine tool consumption increased from 74.4 billion euros to 81.3 billion euros, showing an obvious upward trend. China and the United States have high manufacturing demands and high machine tool consumption due to their large manufacturing industries. Japan and Germany mainly produce high-end machine tools, exporting a large amount of products, with consumption significantly lower than output value.

With the upgrading of downstream industry demand and the development of technologies such as big data and the Internet of Things, the market's demand for machine tools is also evolving. In the future, global machine tools will develop in the direction of high speed, high precision, intelligence, high efficiency and systematization, as well as integration.

The countries where the world's leading machine tool enterprises are located mainly include Japan, Germany, and the United States. These companies' machine tool products are mainly metal cutting machines, mostly large machining centers, and they feature a high degree of automation, often being high-end CNC machine tools. In terms of enterprise echelons, the first tier of global machine tool companies consists mostly of high-end brands, mainly from Japan, Switzerland, and Germany. The second tier represents enterprises with leading quality machine tool products and a high market share. The third tier is dominated by South Korean and Taiwanese companies, with relatively lower prices.

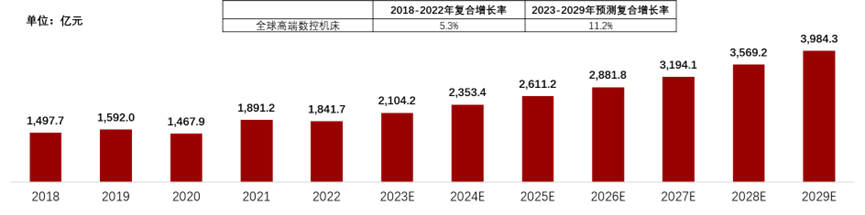

From 2018 to 2022, the global market scale of high-end CNC machine tools increased from 149.77 billion yuan to 184.17 billion yuan, with an annual compound growth rate of 5.3%. It is estimated that the market scale will reach 398.43 billion yuan in 2029, and the annual compound growth rate from 2023 to 2029 will be 11.2%.

Chart 2: Global high-end CNC machine tool market size (by sales), forecast for 2018 - 2029

Data source: Frost & Sullivan, LeadLeo Research Institute

-

The localization rate of CNC machine tools in China is continuously increasing. The domestic production of low-end CNC machine tools has reached complete self-sufficiency, while mid-range CNC machine tools have basically achieved domestic substitution.

The localization rate of CNC machine tools in China is continuously increasing. The production of low-end CNC machine tools domestically has reached complete self-sufficiency, while mid-range CNC machine tools have basically achieved domestic substitution. However, the competitiveness of domestic high-end CNC machine tools is still weak. In 2022, the sales volumes of high-end, mid-range, and low-end CNC machine tools in China were 28,000 units, 113,000 units, and 142,000 units respectively. China is promoting the transformation and upgrading of the manufacturing industry, and it is expected that by 2029, the sales volumes of high-end and mid-range CNC machine tools will rise to 57,000 units and 207,000 units respectively.

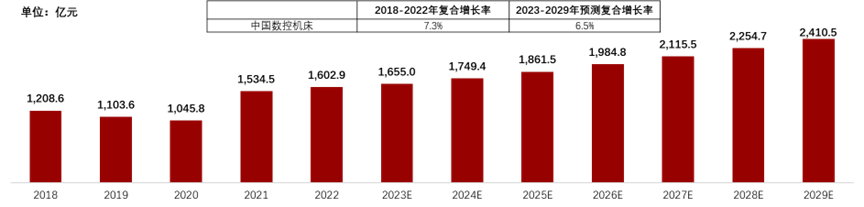

From 2018 to 2022, the market scale of CNC machine tools in China increased from 120.86 billion yuan to 160.29 billion yuan, with an annual compound growth rate of 7.3%. It is estimated that by 2029, the market scale of CNC machine tools in China will grow to 241.05 billion yuan, with a compound growth rate of 6.5% from 2023 to 2029.

Chart 3: China CNC Machine Tool Market Size (by Sales), Forecast for 2018 - 2029

Data sources: General Administration of Customs, National Bureau of Statistics, Machine Tool and Tooling Association, Frost & Sullivan, LeadLeo research institute

Data sources: General Administration of Customs, National Bureau of Statistics, Machine Tool and Tooling Association, Frost & Sullivan, LeadLeo research institute

The upstream of the CNC machine tool industry chain mainly includes various casting, precision parts and functional components, CNC systems, and other component manufacturers; the midstream is primarily composed of CNC machine tool manufacturing enterprises; the downstream applications are mainly in consumer electronics, automotive industry, and other manufacturing sectors that have high demand for precision parts.

The cost structure of CNC machine tools consists of the CNC system, structural parts, drive system, transmission system, and functional components. Most high-end products in key links have not yet achieved domestic substitution. Century CNC and Haitian Precision Machinery are among the first-tier listed companies in China's CNC machine tool industry, with a relatively large revenue scale for machine tool products ranging from 3 billion to 4 billion yuan. Most Chinese CNC machine tool enterprises focus on mid- to low-end products while continuously penetrating into the high-end market. The demand for CNC machine tools varies among different manufacturing industries downstream of the industrial chain. Aerospace equipment, power equipment, consumer electronics, precision molds, semiconductors, and optical components industries have a high demand for high-end CNC machine tools, while industries such as railway transportation and petrochemical equipment have a greater demand for mid- to low-end CNC machine tools.

Chart 4: Schematic Diagram of China's CNC Machine Tool Industry Chain

Data source: Frost & Sullivan, LeadLeo Research Institute

-

The concentration of China's CNC machine tool industry is relatively low, and competition among enterprises is fierce.

In terms of sales revenue in 2022, the top five manufacturers of CNC machine tools in the Chinese mainland accounted for a total market share of 14.4%. Currently, CNC machine tools in China are still mainly mid- to low-end products, and the localization rate of high-end CNC machine tools remains low.

In 2022, the top five enterprises in China's CNC machine tool sales accounted for 32.0%; the top five enterprises in terms of CNC machine tool sales revenue accounted for 14.4%. The domestic CNC machine tool sales share was 68.5%; the sales share was 56.8%.

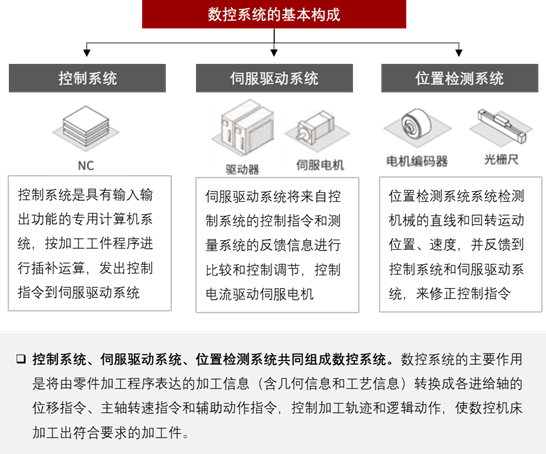

The control system, servo drive system, and position detection system together constitute a numerical control system. The main function of the numerical control system is to convert the machining information (including geometric and technological information) expressed by the part processing program into displacement commands for each feed axis, spindle speed commands, and auxiliary action commands. It controls the machining trajectory and logical actions, enabling CNC machine tools to produce parts that meet the required specifications.

Chart 5: Basic Components of CNC Systems

Source: Frost & Sullivan, LeadLeo Research Institute

Source: Frost & Sullivan, LeadLeo Research Institute

-

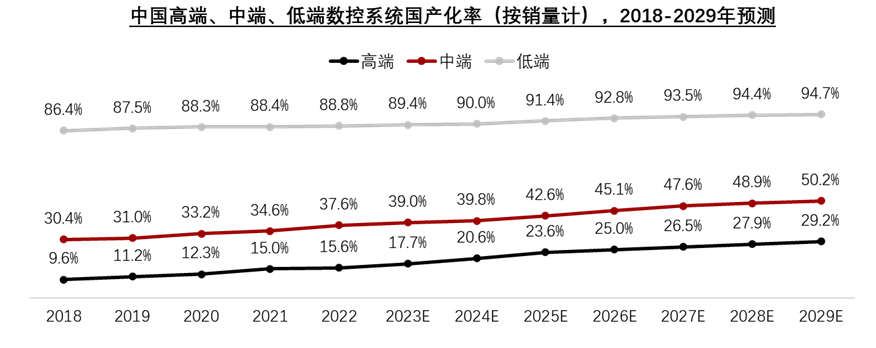

The midstream of CNC systems includes controllers, drives, servo motors, and CAM software. Low-end CNC systems have been basically localized, and some mid-range CNC systems have achieved partial domestic substitution. The localization rate of high-end CNC systems is less than 20%.

In terms of sales volume, China's low-end CNC systems have basically achieved domestic substitution, while some mid-range CNC systems have partially been replaced domestically. The localization rate of high-end CNC systems is relatively low. In 2022, the localization rates of high-end, mid-range, and low-end CNC systems in China were 15.6%, 37.6%, and 88.8% respectively.

In the future, Chinese high-end CNC system enterprises will continue to increase investment in technology research and development and innovation to meet the manufacturing industry's demand for high precision and long-term stable operation. By optimizing key technologies such as control algorithms and servo drives, they aim to improve the motion accuracy of workbenches and reduce issues such as errors and vibrations. It is expected that by 2029, the localization rate of high-end CNC system sales in China will reach 29.2%, achieving partial domestic substitution in key areas.

Chart 6: Market Size of CNC Systems in China, Forecast for 2018 - 2029

Data source: Frost & Sullivan, LeadLeo Research Institute

Data source: Frost & Sullivan, LeadLeo Research Institute

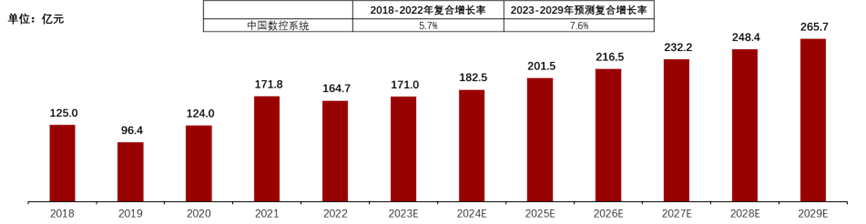

From 2018 to 2022, the market scale of CNC systems in China increased from 12.5 billion yuan to 16.47 billion yuan, with an annual compound growth rate of 5.7% during this period. From 2020 to 2021, the supply chain of overseas manufacturing was disrupted, leading to shortages in product supply, while China's manufacturing industry was less affected. As a result, the export demand for China's manufacturing industry grew rapidly. The demand for CNC machine tools, industrial robots, and other CNC manufacturing equipment in industries such as precision molds, automotive, aerospace, and consumer electronics was rapidly released, thereby driving growth in the upstream CNC system market. In 2021, the market scale of CNC systems in China was 17.18 billion yuan, a year-on-year increase of 35.4%.

In the future, driven by the development of intelligent manufacturing and high-end manufacturing industries, China's demand for numerical control systems in manufacturing will continue to grow. It is estimated that by 2029, the market scale of numerical control systems in China will reach 26.57 billion yuan. From 2023 to 2029, the annual compound growth rate of the market scale of numerical control systems in China will be 7.6%.

Chart 7: Market Size of CNC Systems in China, Forecast for 2018 - 2027

Data source: Frost & Sullivan, LeadLeo Research Institute

The upstream core components of a numerical control system include computing chips such as FPGA and DSP, power modules, operating systems, grating scales, encoders, etc. A numerical control system is a collection of software and hardware, with the core components being controllers, drives, and servo motors, which are usually sold as a set. The downstream of a numerical control system are manufacturers of CNC machine tools and industrial robots.

The technical barriers for computing chips are high, and domestic substitution has not been achieved, with foreign manufacturers dominating the market. Power modules, high-precision gratings, and high-precision encoders have partially achieved domestic substitution. The midstream of CNC systems consists of controllers, drives, servo motors, and CAM software. Low-end CNC systems have basically been localized, while some mid-range systems have achieved partial domestic substitution, with the localization rate of high-end systems being less than 20%. In 2022, the localization rates of sales for high-end, mid-range, and low-end CNC systems in China were 7.9%, 28.3%, and 75.3% respectively. It is expected that by 2029, the localization rates of sales for high-end, mid-range, and low-end CNC systems in China will reach 19.2%, 47.9%, and 87.2% respectively. From 2018 to 2022, the sales of high-end CNC systems in China increased from 1.81 billion yuan to 2.44 billion yuan, with an annual compound growth rate of 6.2% during this period. It is expected that from 2023 to 2029, the sales of high-end CNC systems in China will increase from 2.55 billion yuan to 4.34 billion yuan, with an annual compound growth rate of 9.2% during this period. CNC machine tool manufacturers mainly have three modes for their CNC systems: self-made, purchased, and secondary development, with current machine tool manufacturers primarily purchasing from external sources. The purchased CNC systems have a high degree of standardization and strong versatility, which is conducive to forming specialized and large-scale production.

Chart 8: Schematic Diagram of China's CNC System Industry Chain

Data source: Frost & Sullivan, LeadLeo Research Institute

The CNC system industry in China is highly concentrated. In terms of sales volume in 2022, the top five manufacturers accounted for a total market share of 78.2%. In terms of sales revenue in 2022, the top five manufacturers also accounted for an 87.3% market share.

The high-end market is still dominated by foreign CNC system manufacturers, with competition between domestic and foreign CNC system manufacturers concentrated in the mid-range market. In terms of sales volume in 2022, the localization rate of CNC systems was 58.2%. However, in terms of sales revenue in 2022, the localization rate of CNC systems was only 28.8%. This indicates that there are more high-end products from foreign CNC systems, and market prices are significantly higher than those of domestic CNC systems with similar performance.

-

The PWM numerical control system adopts PWM drive and control technology, capable of meeting the high dynamic accuracy requirements at controllable high speeds, and is suitable for high-speed and high-precision CNC machine tools. The future demand for high-speed and high-precision machining of CNC machine tools will drive the development of PWM numerical control systems.

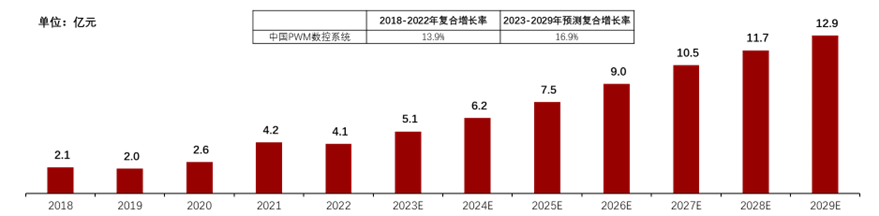

The PWM numerical control system can replace the bus-type numerical control system in high-speed and high-precision fields. Compared to the bus-type numerical control system, the servo response cycle of the PWM numerical control system is shorter, enabling it to quickly respond to position commands. The PWM numerical control system has extremely short control cycles for current, speed, and position loops, which can significantly reduce dynamic errors caused by command speed, acceleration, and jerk, addressing the pain points of high-speed and high-precision machining with CNC machine tools. The PWM numerical control system, paired with high-end CNC machine tools, has been verified in multiple scenarios, and industry customers' awareness of PWM numerical control systems products continues to increase. From 2018 to 2022, the market size of China's PWM numerical control system increased from 210 million yuan to 410 million yuan, with an annual compound growth rate of 13.9%. From 2023 to 2029, the market size of China's PWM numerical control system grew from 510 million yuan to 1.29 billion yuan, with an annual compound growth rate of 16.9% during this period.

Chart 9: Market Size of PWM CNC Systems in China (by Sales), Forecast for 2018 - 2029

Data source: Frost & Sullivan, LeadLeo Research Institute

In the Chinese market, Heidenhain and Röning are the main suppliers of PWM numerical control systems. In terms of sales volume, in 2022, Heidenhain's market share exceeded 70%, while Röning's market share was over 20%. In terms of sales amount, in 2022, Heidenhain's market share was around 90%, and Röning's market share was about 9%. It is expected that the market share of Röning will further increase to nearly 10% in 2023. Heidenhain is a German measurement and control technology company with a profound accumulation of measurement and motion control technology, and it has a strong brand influence. Röning focuses on core technology research and development of high-end numerical control systems and application solutions, and can provide professional linear motor drive control solutions. Its brand influence in the Chinese high-end numerical control system market is growing day by day.

In addition, we have also provided a complete analysis of the CNC machine tools and CNC system industry in China in our report. You can click on the link to view the full report:

https://www.leadleo.com/report/reading?id=662b17635e81457a76ba8bc8&position=9