Lanssife Technology Co., Ltd. (Stock Code: 6613.HK) successfully listed on the main board of the Hong Kong capital market on July 9, 2025. The company is a leading provider of one-stop precision manufacturing solutions for the entire intelligent terminal industry chain in the sector. It has accumulated profound technical expertise and strength in the fields of consumer electronics and intelligent vehicles, and possesses strong and comprehensive platform capabilities. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provides exclusive industry advisory services for Lanssife Technology Co., Ltd.'s listing on the Hong Kong market, and hereby warmly congratulates it on its successful listing.

Lanss Technology Co., Ltd. (hereinafter referred to as 'Lanss') successfully went public on July 9, 2025. The company plans to issue 262,256,800 Hong Kong shares, of which 233,408,400 will be issued internationally and 28,848,400 in Hong Kong. The issue price per share is HK$18.18, raising approximately HK$4.77 billion in net proceeds.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support and highlight the issuer's competitive advantages, assisting the issuer, investment banks and other intermediaries in completing the writing of relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange.

Frost & Sullivan has always been a leader in helping companies go public in Hong Kong. According to LiveReport's big data (statistical data as of June 30, 2025), from January to June 2025, as well as during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 29 (market share 71%), 52 (market share 64%) and 161 (market share 69%) Hong Kong-listed IPOs respectively, ranking first in terms of number. It has a rich accumulation of industry experience and communication skills with regulatory authorities, exchanges, investment and financing institutions, and various related institutions.

PART/1

Investment Highlights

-

The company is a global leader in one-stop precision manufacturing across the entire industrial chain, ranking first in multiple fields;

-

The company adheres to technology innovation as its core, focusing on R&D for a long time, and leads the transformation of cutting-edge materials and technologies;

-

The company has established long-term strategic cooperation with world-class customers to drive industry development;

-

The company has a comprehensive platform-based layout and vertical integration capabilities across the entire industrial chain, enabling it to perceive and capture market opportunities;

-

The company has taken the lead in developing and manufacturing automated and intelligent manufacturing equipment, and has established a data-driven super intelligent manufacturing system;

-

The company boasts a dedicated founder and an experienced senior management team, leading the company to become a global-leading smart manufacturing enterprise.

According to a report by Frost & Sullivan:

-

Ranked first among global suppliers of precision consumer electronics structural parts and modules based on sales revenue;

-

Ranked first globally in comprehensive intelligent vehicle interaction system solutions based on operating revenue,

PART/2

Global Precision Manufacturing Industry Market Overview

Definition of global precision manufacturing

The precision manufacturing industry refers to the sector that utilizes precision machining technology, rapid prototyping technology, automatic control technology, and other related technologies to design, produce, process, assemble, and sell complex and high-precision structural parts, functional modules, and complete machines.

Precision manufacturing plays a crucial role in driving product innovation and realization. As the platform for product creativity, precision manufacturing undertakes the key task of transforming complex designs into high-quality, mass-producible products within the industrial chain. For example, cutting-edge products such as foldable smartphones cannot do without the technical support of advanced high-end manufacturers. Today, leading precision manufacturing enterprises have transformed from traditional product producers to comprehensive solution providers, capable of supporting the entire product design and manufacturing process from concept design to final product delivery. As an important participant in the industrial chain, precision manufacturers help customers maintain competitive advantage amidst rapid technological development, achieving rapid iteration and optimization of products.

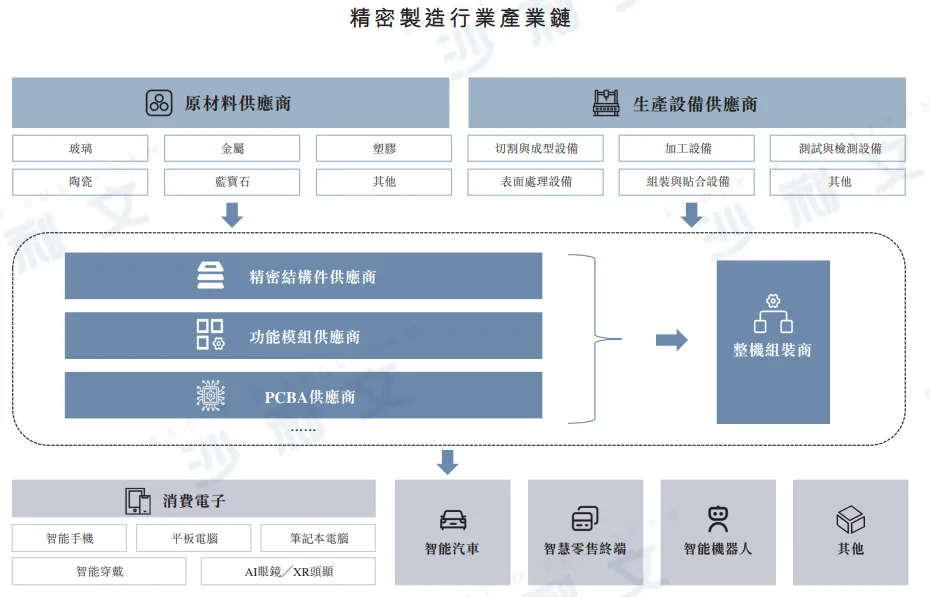

Analysis of the Industrial Chain in the Precision Manufacturing Industry

The upstream of the precision manufacturing industry chain includes raw material and production equipment suppliers, providing materials such as glass, metal, ceramics, and equipment for cutting, processing, and testing to midstream manufacturers. Leading enterprises improve efficiency, reduce costs, and shorten delivery cycles by deploying raw materials and intelligent production equipment, such as independently developing or investing in the construction of high-precision industrial robots and intelligent production equipment. Midstream manufacturers are responsible for processing high-precision structural parts and functional modules, and providing PCBA and complete machine assembly. The downstream application areas of the precision manufacturing industry include consumer electronics, intelligent vehicles, smart retail terminals, intelligent robots, and other fields.

Leading precision manufacturing enterprises cooperate deeply with customers in product design, research and development, production, and manufacturing. They provide customized solutions according to customer needs, gradually achieving vertical coverage across the entire industrial chain, thus forming a one-stop precision manufacturing platform. In addition, in terms of product design, leading precision manufacturing solution providers actively propose conceptual designs for customers to evaluate and choose from. Through this approach, enterprises can continuously deepen their long-term strategic partnership with customers.

Data source: Analysis by Frost & Sullivan

PART/3

Global Market Overview of Precision Manufacturing Industry in Consumer Electronics

Definition of comprehensive solutions for precision electronic components and modules

The comprehensive solution for precision structural parts and modules in consumer electronics refers to a one-stop solution that provides design, manufacturing, and related services for structural parts (mainly including front and rear protective covers and middle frames) and functional modules for consumer electronic products. To better support the requirements of downstream customers, leading providers of comprehensive solutions for precision structural parts and modules in consumer electronics usually participate in the product research and development process several years before the release of consumer electronics products. The industry participants and downstream customers are highly bound, and orders are generally quite saturated.

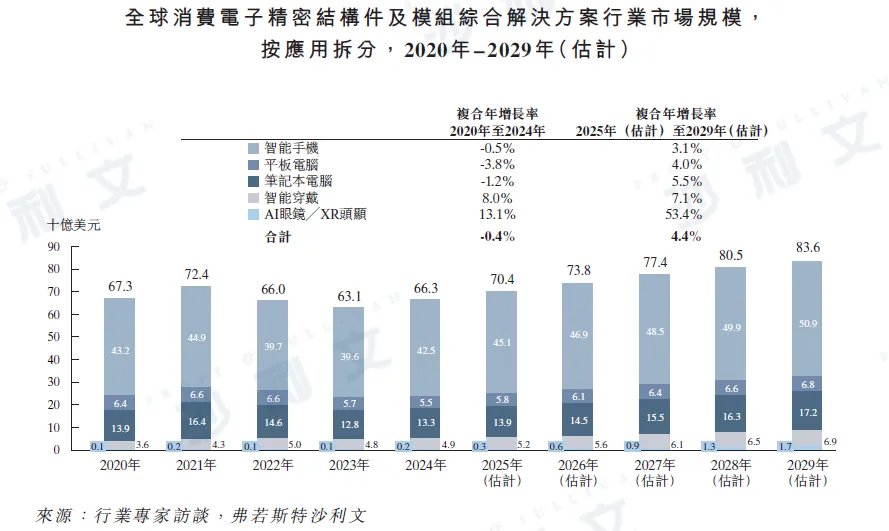

Global Market Size Analysis of Precision Consumer Electronics Components and Modules: Comprehensive Solutions

Consumer electronics precision structural parts and modules are closely related to the functionality, intelligence, and usage scenarios of consumer electronic products. Among them, smartphones are the largest application sector. It is estimated that by 2029, the global market size for comprehensive solutions for precision structural parts and modules of smartphones will reach $50.9 billion. In addition, driven by continuous progress in AI technology and the increasing number of AI glasses products launched by various brands, the global market size for comprehensive solutions for precision structural parts and modules of AI glasses/XR headsets is expected to reach $1.7 billion in 2029, with a compound annual growth rate of up to 53.4% starting from 2025.

Data source: Analysis by Frost & Sullivan

Analysis of Industry Drivers and Development Trends for Global Precision Consumer Electronics Components and Modules

● Breakthroughs in emerging technologies and materials

With the accelerated iteration of consumer electronics products, the application of emerging technologies and materials is continuously driving innovation in the industry of precision structural parts and modules for consumer electronics. For example, leading companies continue to explore the research and development of emerging technologies, developing industry-leading fingerprint-resistant coating technology, special chemical tempering processes, and ultra-thin, highly adhesive ink application technology. In the field of emerging materials, UTG has gradually replaced transparent polyimide (CPI) materials with its various performance advantages, becoming the mainstream flexible cover material for foldable screens in the current market. Leading enterprises are also developing the next generation of foldable ultra-thin glass technology—VTG (Variable Thin Glass). Compared to UTG, VTG offers higher strength, impact resistance, and scratch resistance while maintaining the same light transmittance and excellent bending performance. For the materials used in smartphone frames, leading solution providers have mature aluminum alloy frame production processes, including die-casting or CNC methods, achieving high product yield, relatively low costs, lightweighting, and excellent thermal conductivity. In addition, sapphire, as a high-strength, scratch-resistant material, provides better protection for smartphone camera covers and smartwatches, while enhancing the appearance design and user experience.

● Driven by the integration of intelligent manufacturing and automation

Intelligent manufacturing hardware and automation technology are driving the global consumer electronics precision structure parts and modules comprehensive solution industry into a new phase. Through the construction and application of industrial robots, intelligent devices, intelligent inspection systems, automated production lines, and industrial internet, as well as system integration, solution providers have significantly improved production efficiency and product quality, while reducing costs and ensuring product consistency. Leading solution providers independently develop automation equipment and industrial robots, and through the application of technical tools such as artificial intelligence, big data, and cloud computing, they have achieved software and hardware compatibility throughout the entire production process, ensuring high precision and stability of products and matching customers' customized production line needs. At the same time, the application of intelligent inspection systems enables data monitoring and quality traceability in all production links, effectively reducing factory system losses and facilitating the integration and progress of the industrial chain.

Analysis of the Competitive Landscape in the Global Comprehensive Solutions for Precision Consumer Electronics Components and Modules

In 2024, the global market size for comprehensive solutions for precision electronic components and modules reached $66.3 billion. The combined market share of the top five participants was 40.0%, indicating a relatively concentrated market share. Among them, our group's revenue reached $8.6 billion in 2024, ranking first among global suppliers of precision electronic components and modules comprehensive solutions, with a market share of 13.0%.

Data source: Analysis by Frost & Sullivan

PART/4

Global Intelligent Vehicle Interaction System Comprehensive Solution Industry Market Overview

Overview of the Intelligent Vehicle Industry

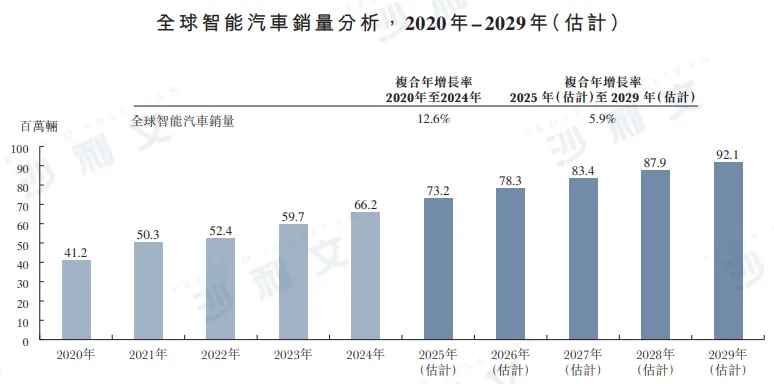

In recent years, driven by both policy support and technological progress, the global intelligent vehicle market has grown rapidly, with electrification and autonomous driving accelerating their popularization. 'Hybrid intelligence' has become an industry trend, and automotive interaction systems are becoming increasingly intelligent to meet consumers' higher demands for driving experiences. Global intelligent vehicle sales are expected to grow from 73.2 million units in 2025 to 92.1 million units in 2029, with a compound annual growth rate of 5.9% from 2025 to 2029.

Data source: Analysis by Frost & Sullivan

Definition of the comprehensive solution for intelligent vehicle interaction systems

The comprehensive solution for intelligent vehicle interaction systems refers to a one-stop solution that revolves around the design, manufacturing, and integration of core exterior structural components and related functional modules. These interaction systems include central control screens, intelligent B-pillars, intelligent instrument panels, HUDs, streaming rearview mirrors, etc. In addition, with technological development, multifunctional glass applied to car windows and windshields is gradually becoming popular in intelligent vehicles. This type of glass offers a variety of intelligent and functional services, bringing users a better interactive experience and becoming an important structural component of intelligent vehicles. Providers of comprehensive solutions for intelligent vehicle interaction systems integrate material innovation and precision manufacturing capabilities to provide automotive companies with high-performance, highly reliable comprehensive solutions for interaction systems, promoting a comprehensive improvement in the safety, convenience, and user experience of intelligent vehicles.

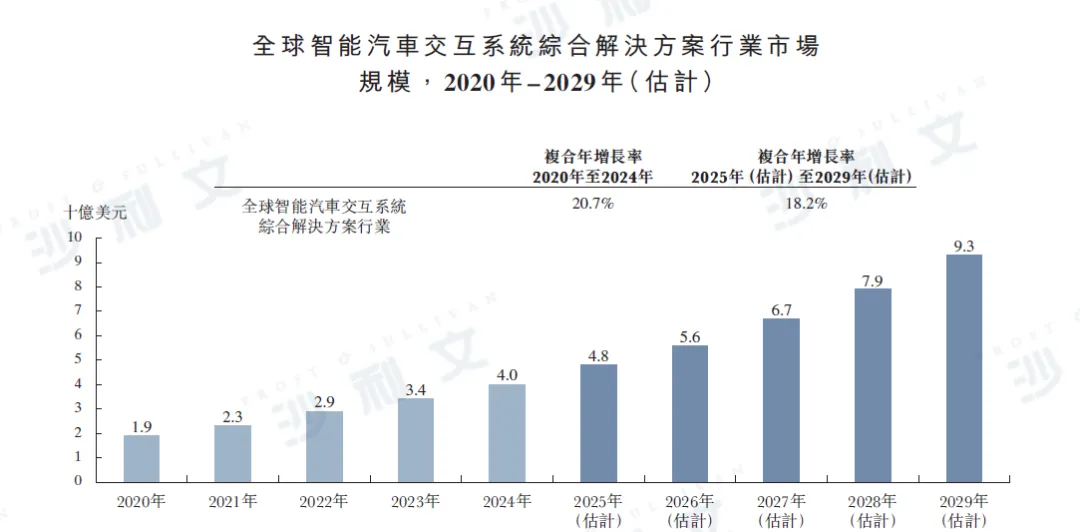

Analysis of the Global Intelligent Vehicle Interaction System Comprehensive Solution Industry Market Scale

Driven by the growing demand for intelligent cockpits, autonomous driving technology, and in-vehicle intelligence technology, the market for comprehensive intelligent vehicle interaction system solutions is rapidly expanding. With continuous advancements in display technology, multifunctional glass, and sensing systems, the market demand for integrated solutions is steadily increasing. Suppliers of comprehensive intelligent vehicle interaction system solutions need to provide a full range of services from one-stop design to manufacturing to gain an advantage in the fierce competition. In the future, innovative technology, high-quality service, and strong R&D capabilities will become key factors leading the market. The global market size for comprehensive intelligent vehicle interaction system solutions is expected to grow from $1.9 billion in 2020 to $4 billion in 2024, and is projected to reach $9.3 billion by 2029, with a compound annual growth rate of 18.2% from 2025 to 2029.

Data source: Analysis by Frost & Sullivan

Driving Forces and Development Trends in the Global Intelligent Automotive Interaction System Comprehensive Solution Industry

● Driven by the demand for automotive intelligence

With continuous breakthroughs in autonomous driving technology, the penetration rate of intelligent cockpits is steadily increasing, and the human-machine interaction systems of complete vehicles are developing towards personalization, convenience, and multimodal capabilities. In addition, the development of intelligent connected technology has accelerated the interconnection of real-time vehicle information. For example, smart cockpits are evolving towards multi-screen collaboration and multimodal interaction—multi-screen collaboration technology improves information sharing and operational convenience, and is expected to drive an increase in demand for multi-screen integration and interactive solutions from automotive interface manufacturers. At the same time, favorable policies have created new growth opportunities for intelligent vehicle component suppliers. For instance, the 'Innovative Development Strategy for Intelligent Vehicles' released in 2020 proposed to build a relatively complete intelligent vehicle system by 2035 to 2050, promote breakthroughs in core intelligent vehicle technologies, and become a long-term goal for the development of intelligent vehicles in China. In 2024, the Ministry of Industry and Information Technology (MIIT) and other five ministries jointly issued the 'Notice on Carrying Out Pilot Work for Intelligent Connected Vehicles "Vehicle-Road-Cloud Integration" Applications," accelerating technological innovation and industrialization in the field of intelligent connected vehicles. These measures are expected to drive demand from related automotive component manufacturers. Therefore, under the dual impetus of policy support and technological innovation, automotive intelligence will continue to deepen, which will further drive the continuous growth of market demand for comprehensive solutions for intelligent vehicle interaction systems.

● Advances in glass technology

The progress and innovation of structural components such as glass are important factors driving the growth of the market for comprehensive solutions for intelligent vehicle interaction systems. The interior display interfaces of cars are continuously evolving towards larger screens, touch capabilities, curved surfaces, and transparency. The popularization of in-vehicle touchscreens and HUDs has made the car interaction interface more tech-savvy and enhanced the driving experience. At the same time, the application of multifunctional glass in car windows, sunroofs, and sunscreens is developing rapidly. Glass used in side windows and sunscreens not only has traditional transparent functions but also provides a variety of intelligent and functional services, bringing better interaction experiences such as automatically adjusting light transmittance according to light changes, window protection against ultraviolet rays, heat insulation, water resistance, fog prevention, conductivity, image reflection, etc., as well as in conjunction with in-car display information, bringing a more comfortable, safe, and efficient experience to car owners. Companies with rich experience in advanced glass manufacturing and who have deployed these cutting-edge automotive glass technologies earlier will have a good competitive advantage. The ability to meet the ever-changing needs of intelligent vehicles and provide integrated functional glass solutions will become a key differentiator in the technology-driven automotive supply chain.

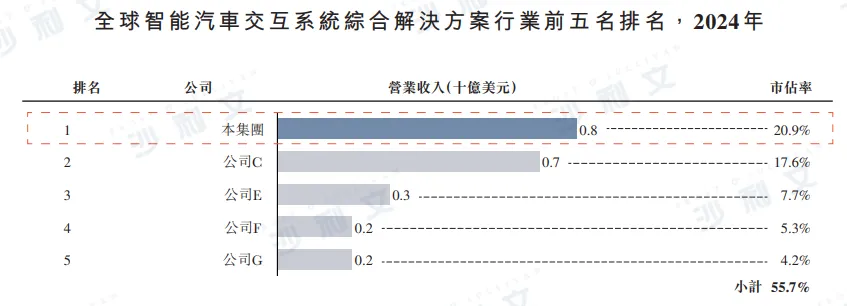

Industry Competition Landscape of Comprehensive Solutions for Global Intelligent Vehicle Interaction Systems

In 2024, the global market size for comprehensive solutions for intelligent vehicle interaction systems reached approximately $4 billion. The top five participants accounted for a combined market share of 55.7%, among which our group had revenues of $800 million in 2024, ranking first with a market share of 20.9%.

Data source: Analysis by Frost & Sullivan