Wuhan Dazhong Stomatological Healthcare Co., Ltd. (Stock Code: 2651.HK) successfully listed on the main board of the Hong Kong capital market on July 9, 2025. The company is a private oral healthcare service provider focusing on Hubei and Hunan provinces in Central China. It operates an expanding network of oral healthcare services through a direct-operated chain model in this booming market. The company provides reliable and accessible oral care to communities, dedicated to serving the public. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') has provided exclusive industry advisory services for the listing of Wuhan Dazhong Stomatological Healthcare Co., Ltd., and hereby warmly congratulate them on their successful listing.

Wuhan Dazhong Stomatological Healthcare Co., Ltd. (hereinafter referred to as 'Dazhong Stomatological') successfully went public on July 9, 2025. The company plans to issue 10.8618 million H shares, of which 90% will be international offerings and 10% will be Hong Kong offerings. The maximum offering price per share is HK$21.4, with a maximum net raise of HK$232 million.

During the process of listing in Hong Kong, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing the writing of relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business, and other important sections), helping the issuer communicate with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and providing feedback on various industry-related issues to the Hong Kong Stock Exchange.

Frost & Sullivan has always been a leader in helping companies go public in Hong Kong. According to LiveReport's big data (statistical data as of June 30, 2025), from January to June 2025, as well as during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 29 (market share 71%), 52 (market share 64%), and 161 (market share 69%) Hong Kong-listed IPOs respectively, ranking first in terms of volume. It has rich industry experience and communication skills with regulatory authorities, exchanges, investment and financing institutions, and various related institutions.

PART/1

Investment Highlights

-

The company is a direct-operated chain model private oral healthcare service provider in Central China. With years of development experience and profound insights in the industry, it provides the public with reliable and convenient oral care;

-

The company's business scale and financial performance rank among the leading in private oral healthcare service providers;

-

The centralized and lean headquarters operation capabilities empower dental medical institutions comprehensively, ensuring operational efficiency and sustainable profitability;

-

Strategic partner programs and employee stock ownership platforms help motivate high-quality healthcare professionals and other talents, supporting the company's business growth while building an oral healthcare service network into a talent entrepreneurship platform;

-

Mature, scalable, and replicable business models benefit from organic growth and strategic acquisitions;

-

An outstanding professional talent team led by renowned dental experts, with medical technology as its core competitiveness;

-

With outstanding professional and management skills, led by a visionary and experienced management team, unified management is implemented.

According to the Frost & Sullivan report, the company:

-

Ranked first among all private oral healthcare service providers in Central China, based on 2024 revenue;

-

Ranked 14th among all private oral healthcare service providers in China, based on 2024 revenue;

-

Based on net profit for 2024, the company ranks third among all private oral healthcare service providers in China.

PART/2

Overview of the Chinese Oral Medical Service Industry Market

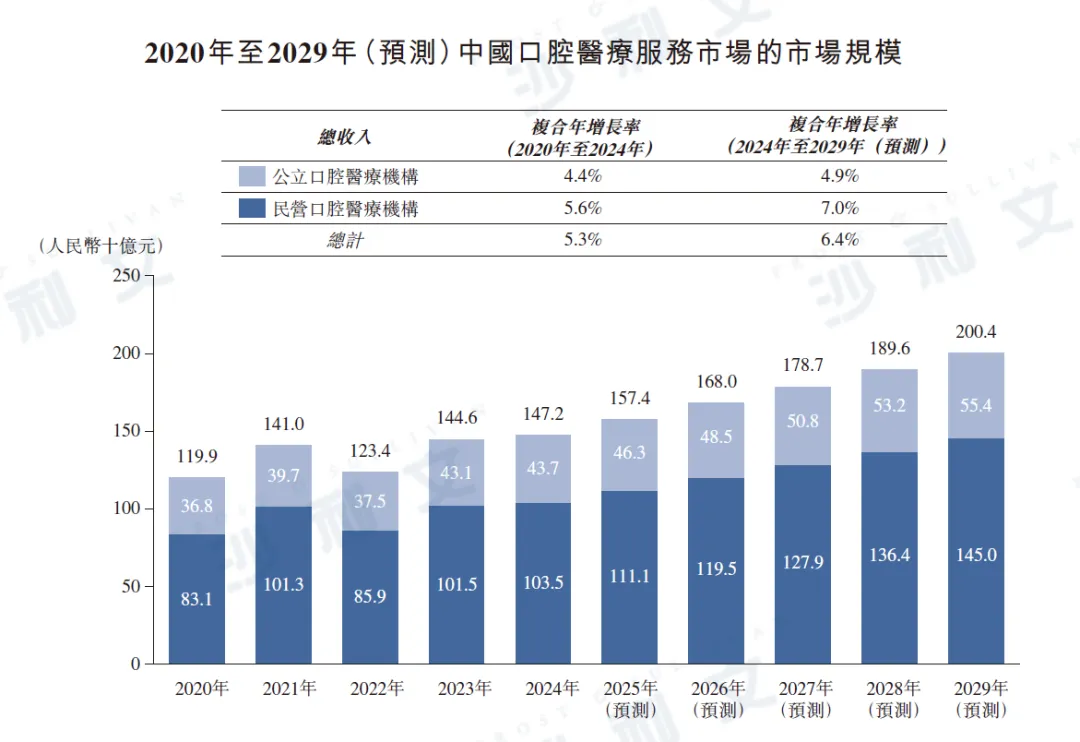

Oral healthcare services mainly include comprehensive dental diagnosis and treatment services, dental implant services, and orthodontic services. In terms of the total revenue generated by Chinese oral healthcare service providers, the market size of the Chinese oral healthcare service market increased from RMB 119.9 billion in 2020 to RMB 147.2 billion in 2024. Due to the economic recovery after the pandemic being less than expected, the growth of the market size of the Chinese oral healthcare service market has slowed down. However, in the long run, driven by favorable policies such as the 'Opinions on Promoting the High-Quality Development of Service Consumption' and the 'Measures to Create New Consumption Scenarios and Cultivate New Consumption Growth Points' introduced in 2024, the market size of the Chinese oral healthcare service market will reach RMB 200.4 billion by 2029, growing at a compound annual growth rate of 6.4% from 2024 to 2029. Among them, the total revenue generated by private Chinese oral healthcare service providers will reach RMB 145 billion in 2029, with a compound annual growth rate of 7.0% from 2024 to 2029. In contrast, the total revenue generated by public Chinese oral healthcare service providers is expected to grow at a compound annual growth rate of 4.9% from 2024 to 2029, reaching RMB 55.4 billion by 2029.

Data source: Analysis by Frost & Sullivan

PART/3

Market Drivers and Development Trends of Oral Healthcare Services in China

Government's favorable policies

The Chinese government has introduced a series of favorable policies to promote the development of China's oral healthcare service market. For example, the National Health Commission issued the 'Healthy Oral Health Action Plan (2019-2025)' in 2019, advocating for the high-quality development of the oral healthcare service market and encouraging private providers to participate in the prevention and treatment of oral diseases. The State Council released the '14th Five-Year Plan' for National Health in 2022, promoting the comprehensive prevention and control of chronic diseases, with a focus on common oral diseases. The promulgation of these policies indicates that the Chinese government attaches great importance to oral health, thereby promoting the development of China's oral healthcare service market.

The prevalence of oral diseases has increased

The prevalence of oral diseases in China (i.e., the proportion of oral disease cases to the total population during a specific period) has been continuously rising. According to the third and fourth national oral health epidemiological surveys conducted by the National Health and Family Planning Commission in 2007 and 2017, the overall prevalence of oral diseases in China exceeds 90%. The number of oral disease cases in China increased from 6.382 million in 2020 to 7.577 million in 2024, with a compound annual growth rate of 4.4%. In recent years, changes in diet patterns and excessive daily sugar intake have increased the risk of oral diseases. The total retail sales of tobacco and alcohol in China increased from RMB 412.4 billion in 2020 to RMB 589.9 billion in 2024, at a compound annual growth rate of 9.4%. In addition, the sugar consumption of food and beverages in China increased from 810,000 tons in 2020 to 900,000 tons in 2024, at a compound annual growth rate of 2.7%. Moreover, long-term stress may weaken the immune system and increase the risk of oral diseases. At the same time, as people age, the natural repair ability of teeth also shows a downward trend, making the elderly more susceptible to a series of oral problems due to physiological aging. Therefore, as of December 31, 2024, the prevalence of oral diseases in China exceeds 95%. The increase in oral disease cases and incidence has driven strong demand for oral medical services in China.

Growth in the demand for community oral healthcare services

As an important part of China's healthcare system, community healthcare provides basic medical care and convenient services to residents. Private community healthcare refers to the community healthcare services provided by private medical institutions located or near communities, covering a wide range of medical services to meet the common healthcare needs of residents. In 2024, the total revenue of private community healthcare services in China reached approximately 403 billion yuan, accounting for 31.2% of the total revenue of private healthcare services in China, with oral healthcare services accounting for about 10% of the total revenue of private community healthcare services. The characteristics of oral healthcare services include high frequency and follow-up needs, mainly due to the complexity of oral disease conditions, lengthy treatment processes, and increased preventive healthcare needs. Specifically, dental implant services usually involve multiple treatment stages, including preliminary consultation, pre-operative examination, surgical implantation, and final crown installation, with the entire process lasting 3 to 12 months. Complex oral conditions require longer treatment processes and multiple follow-ups, further increasing the frequency of customer visits. In addition, with the continuous enhancement of oral health awareness, more and more customers choose preventive care, such as regular teeth cleaning and dental check-ups. These high-frequency basic oral healthcare services further increase the customer follow-up rate. The growing demand of community residents for convenient and high-quality oral healthcare services has driven the penetration of high-quality oral healthcare services into communities. Oral healthcare service providers respond to residents' daily oral treatment needs by being located close to communities. As the demand for community oral healthcare services continues to grow, oral healthcare service providers focusing on community oral healthcare face more development opportunities.

PART/4

The competitive landscape of the private oral healthcare service market in China

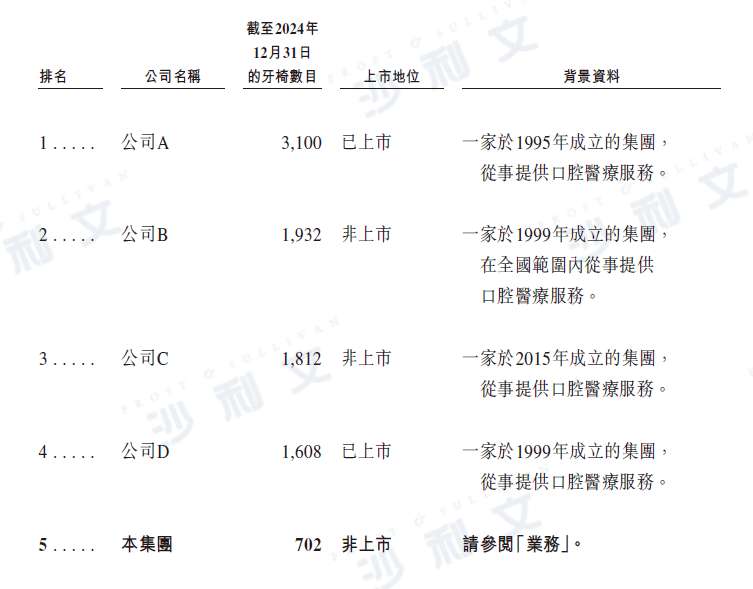

The private oral healthcare service market in China is highly fragmented and competitive. As of December 31, 2024, there were approximately 99,300 private oral healthcare institutions in China. Major cities such as Beijing, Shanghai, and Wuhan have become important oral healthcare service centers due to their abundant medical resources and large customer demand. In terms of the number of dental chairs as of December 31, 2024, the company ranked fifth among all private oral healthcare service providers in China.

Data source: Analysis by Frost & Sullivan

PART/5

Overview of the Oral Medical Service Market in Central China

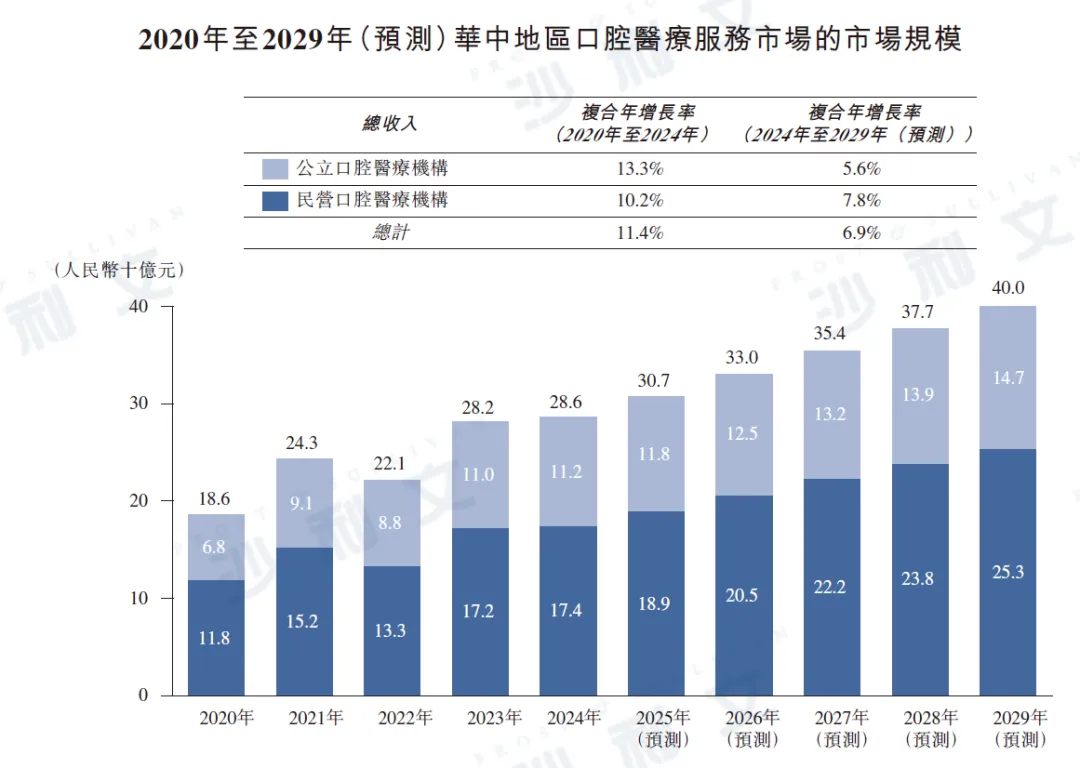

Central China mainly includes Hubei Province, Hunan Province, Henan Province, and Jiangxi Province. In terms of revenue generated by oral healthcare service providers in Central China, the market size of the oral healthcare service market in Central China increased overall by a compound annual growth rate of 11.4% from 2020 to 2024, rising from RMB 186 billion to RMB 286 billion. By 2029, the market size of the oral healthcare service market in Central China is expected to reach RMB 400 billion, with a compound annual growth rate from 2024 to 2029 of 6.9%. The total revenue generated by private oral healthcare service providers in Central China is expected to grow at a compound annual growth rate of 7.8% from 2024 to 2029, reaching RMB 253 billion in 2029.

Data source: Analysis by Frost & Sullivan

PART/6

Market Drivers and Development Trends of Oral Medical Services in Central China

Good policies in Central China

The governments of Central China have issued a series of policies to promote oral health, such as the 'Notice on Doing a Good Job in Integrating Oral Implant Medical Services and Price Regulation' and the 'Hubei Provincial Health Development 14th Five-Year Plan'. These policies aim to allocate more resources to improve dental health, including the establishment of oral medical institutions and subsidies, making it easier for local residents to access oral medical services. In addition, Henan Province has issued the 'Work Plan for the Elderly Oral Health Action in Henan Province in 2024', etc., to publicize the importance of regular dental check-ups and maintaining oral hygiene, thereby increasing the demand for oral medical services in Central China.

The demand for oral medical services exceeds supply

In recent years, people's attention to oral health issues has been continuously increasing, driving the demand for oral medical services. With the aging population and the implementation of the two-child and three-child policies, the child and elderly populations in Central China will increase, leading to a huge demand for oral medical services in this region. However, the oral medical service market in Central China faces the problem of a shortage of dentists. According to data from the National Health Commission, in 2024, the number of dentists per million population in Central China reached 197, which is lower than China's 283. The gap between the demand for oral medical services and the supply of oral medical resources is expected to drive the development of the oral medical service market in Central China.

Penetrating into county-level cities

In recent years, the number of oral healthcare service providers in developed cities in Central China such as Wuhan and Changsha has been increasing, leading to fierce competition in the local market. For example, as leading oral healthcare service providers continue to expand their operations, the number of oral healthcare institutions in Wuhan is expected to reach 1,800 by 2029. Due to the near saturation of the oral healthcare service market in these developed cities, more and more providers are gradually penetrating into county-level cities. In addition, as the oral health awareness of residents in Central China (especially county-level cities) continues to improve, future demand for oral healthcare services will significantly grow. Considering the large population of county-level cities in Central China and the growing demand for oral healthcare services, oral healthcare service providers will have broad development potential and greater market share by expanding their operations into county-level cities.

PART/7

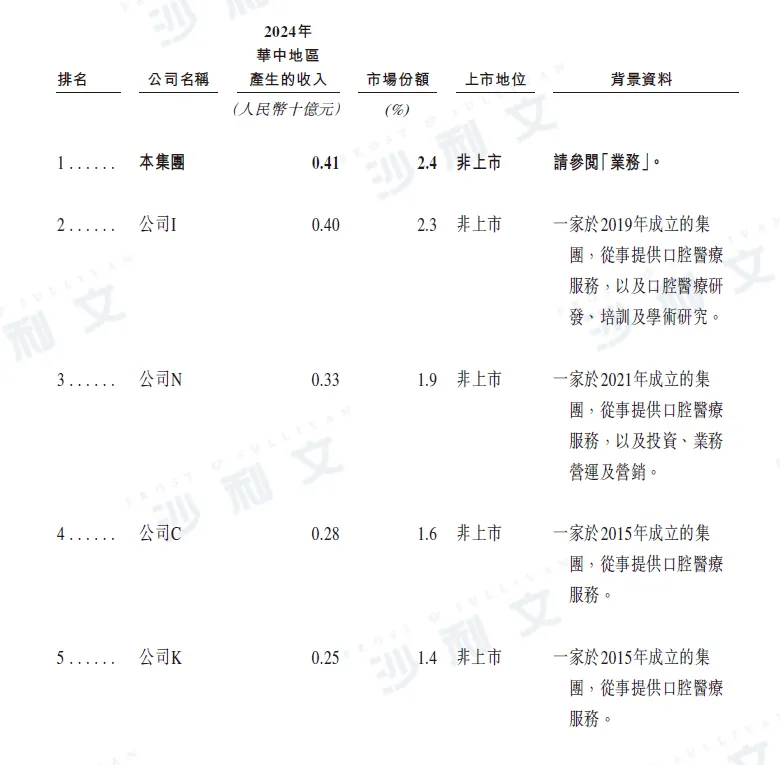

Competitive landscape of the private oral healthcare service market in Central China

The oral healthcare service market in Central China is relatively fragmented and highly competitive. As of December 31, 2024, there were approximately 17,000 private oral healthcare service institutions in Central China. Based on the revenue generated in Central China in 2024, the top five oral healthcare service providers accounted for about 9.6% of the market share, with the company ranked first holding a market share of about 2.4%.

Data source: Analysis by Frost & Sullivan