Shengneng Group Co., Ltd. (hereinafter referred to as 'Shengneng Group') successfully listed on January 17, 2023. The company plans to issue 1.72 billion H shares, of which 90% will be international offerings and 10% will be public offerings, with an additional 15% being in excess allotments. The issue price per share is HK$1.60, raising a net amount of approximately HK$18.67 billion.

During the Hong Kong listing process, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, sponsor, and other professional intermediary institutions in completing the writing of relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important sections), facilitating communication between the issuer and the Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on industry-related issues from the Stock Exchange.

Investment highlights

The company has global presence and a diverse customer base consisting of highly reputable clients;

The company can provide high-quality graphite electrode products produced under demanding environmental standards;

The company has strong technical capabilities to deliver optimized products;

The company has stable raw material supply resources;

The company has a management team with rich experience and a deep understanding of the graphite electrode industry and market.

According to the Frost & Sullivan report, in terms of production volume in 2021, the company:

Ranked seventh among global ultra-high power graphite electrode producers;

Ranked fourth among China's ultra-high power graphite electrode producers.

Global Graphite Electrode Market Overview

Graphite electrodes are a type of high-temperature resistant graphite conductive material. Graphite electrodes can conduct current and generate electricity, thereby melting scrap iron or other raw materials in blast furnaces to produce steel and other metal products, mainly used for manufacturing steel. Graphite electrodes are the only material with low resistivity that can withstand the thermal gradient inside an electric arc furnace. According to the different raw materials and physical and chemical indicators of finished products, graphite electrodes can be divided into three categories: ordinary power graphite electrodes, high-power graphite electrodes, and ultra-high power graphite electrodes. Ultra-high power graphite electrodes have better specifications and performance.

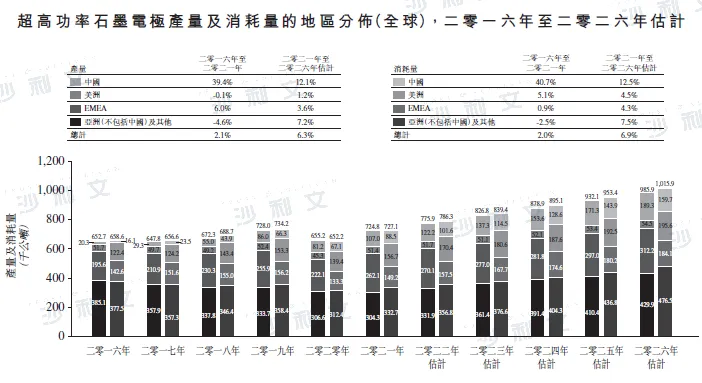

Between 2016 and 2021, the global (excluding China) graphite electrode production capacity decreased due to the demolition of low-capacity factories, long-term environmental rectification, and the redevelopment of low-capacity facilities. The gap between graphite electrode production and consumption was mainly filled by importing graphite electrodes from China.

Source: Frost & Sullivan report

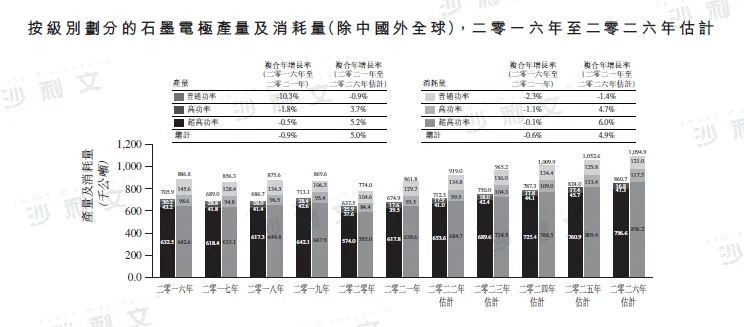

Apart from the temporary decline in graphite electrode production and consumption due to the COVID-19 pandemic in 2020, the global (excluding China) market for ultra-high power graphite electrodes has been on an upward trend since 2016, with a projected continuous increase from 2021 to 2026. Especially during the period from 2016 to 2018, the global (excluding China) production of ultra-high power graphite electrodes decreased continuously from about 632.5 thousand tons in 2016 to about 617.3 thousand tons in 2018, resulting in a severe shortage of capacity. In addition, the recovery of the global arc furnace steel market in 2017 drove a surge in demand for graphite electrodes, which also exacerbated the imbalance between supply and demand and price fluctuations for ultra-high power graphite electrodes.

Source: Frost & Sullivan report

Competitive landscape of the global graphite electrode market

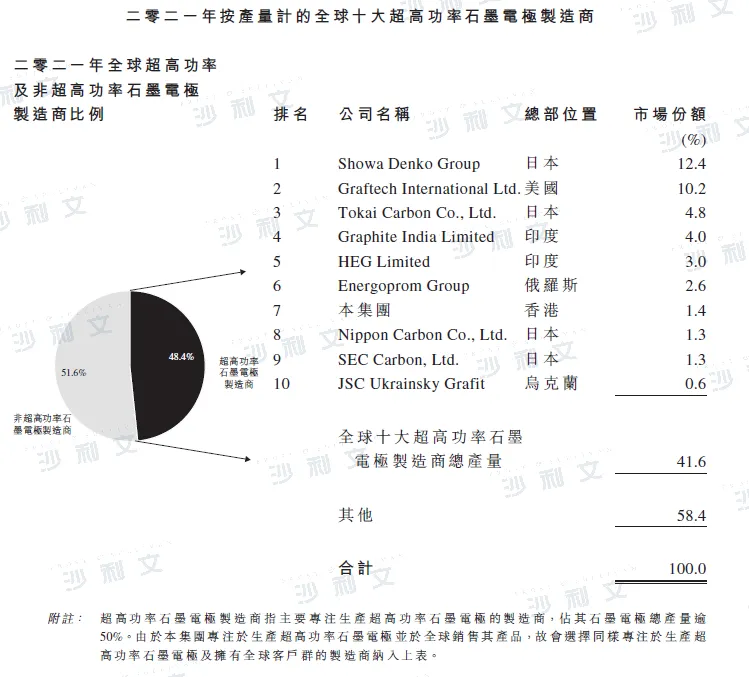

In 2021, according to a Frost & Sullivan report, globally, the top 10 ultra-high power graphite electrode producers accounted for approximately 41.6% of the market share, with Shengneng Group holding about 1.4% of the market share.

Source: Frost & Sullivan report

Graphite electrode market price

The price of ultra-high power graphite electrodes globally (excluding China) continued to rise from 2017 to 2018, reaching a peak at the end of 2018 of about $18,370.0 per ton. The price of ultra-high power graphite electrodes in China also peaked at the beginning of 2018 at about RMB 140,640.7 per ton. Since the end of 2020, with the stable development of the steel industry and its downstream industries (such as the real estate industry), tight supply, and continuously rising raw material prices for graphite electrodes, the market demand for graphite electrodes has been increasing, driving a continuous rise in the price of graphite electrodes.

Source: Frost & Sullivan report

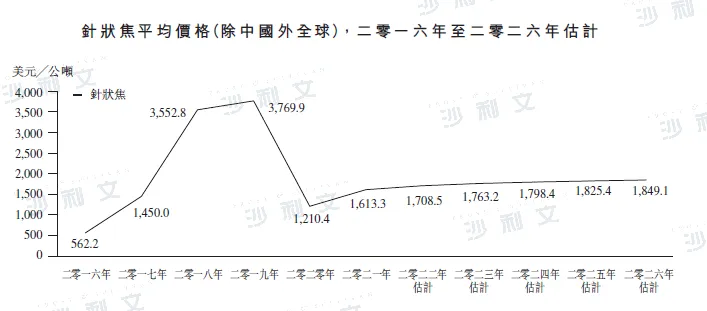

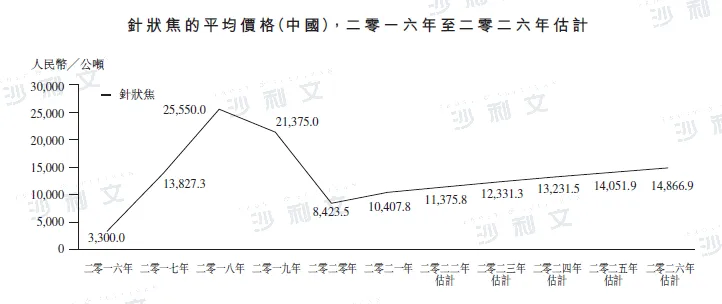

Market prices of main raw materials for graphite electrodes

Needled coke is a type of carbon material that has a series of advantages such as a low thermal expansion coefficient, low porosity, low sulfur content, low metal content, high electrical conductivity, and easy graphitization. Depending on the raw materials, needle coke can be divided into oil-based needle coke and coal-based needle coke. Oil-based needle coke is made from clarified oil and is mainly produced in the United States, the United Kingdom, and Japan. Coal-based needle coke is made from coal tar pitch and is mainly produced in Japan and India. The needle coke produced in China is mainly coal-based. Due to the different raw materials used in oil-based and coal-based needle coke, the differences in production processes mainly lie in the pre-treatment of raw materials.

In 2016, the price of needle coke globally (excluding China) was about $562.2 per ton. Since China is a net importer of needle coke, its demand has had a significant impact on global (excluding China) needle coke prices. The demand in China's graphite electrode market surged in the second half of 2016, causing needle coke prices to rise sharply starting from 2017. By 2026, the prices of needle coke globally (excluding China) and in China are expected to reach about $1,849.1 per ton and about RMB 14,866.9 per ton, respectively.

Source: Frost & Sullivan report

Source: Frost & Sullivan report

Overview of China's Graphite Electrode Market

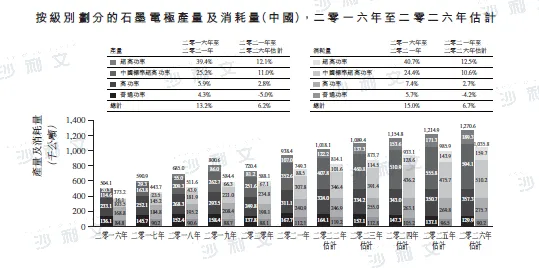

Compared to global (excluding China) ultra-high power graphite electrode producers, only a few manufacturers in China are capable of producing ultra-high power graphite electrodes. More produce graphite electrodes that meet China's standards at a lower performance level.

In 2020, affected by the COVID-19 pandemic, China's graphite electrode production decreased significantly. In 2021, graphite electrode production has rebounded to pre-COVID-19 levels, with an annual growth rate of about 30.2%. The growth in graphite electrode production mainly benefited from the increase in ultra-high power graphite electrodes and ultra-high power graphite electrodes meeting Chinese standards, as well as the recovery of operating rates for arc furnace steel producers.

In the future, with the continuous recovery of operating rates and government policy support for the development of arc furnace steel, it is expected that China's graphite electrode production will reach about 1,270.6 thousand tons by 2026, with a compound annual growth rate of about 6.2% from 2021 to 2026. Since 2016, China's consumption of graphite electrodes has shown an upward trend, reaching about 740,000 tons in 2021. The compound annual growth rate from 2016 to 2021 was about 15.0%. In 2026, China's consumption of graphite electrodes is expected to reach about 1.04 million tons.

Source: Frost & Sullivan report

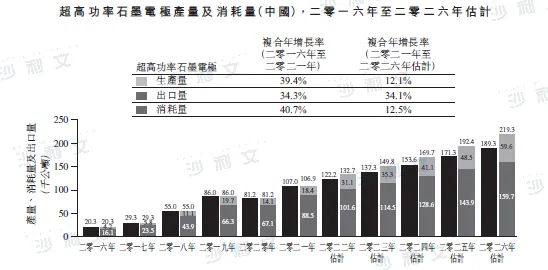

Ultra-high power graphite electrodes are mainly used in large-capacity arc furnaces and special steel arc furnaces. These arc furnaces have extremely strict performance requirements for ultra-high power graphite electrodes according to Chinese standards. There are almost no manufacturers in China capable of producing ultra-high power graphite electrodes (Shengneng Group is one of the Chinese producers that can produce them). Since 2017, China's steel market has gradually phased out backward production capacity because arc furnace steelmaking accounts for an increasingly high proportion of total crude steel output. At the same time, steel producers have increased the use of high-end arc furnaces, leading to a continuous growth in demand for ultra-high power graphite electrodes in the market.

In 2021, China's production and consumption of ultra-high power graphite electrodes reached 107,000 tons and 88,500 tons respectively. In the future, (i) it is expected that China's production and consumption of ultra-high power graphite electrodes will show an upward trend, reaching 189,300 tons and 159,700 tons in 2026 respectively, with a compound annual growth rate of 12.1% and 12.5% from 2021 to 2026; and (ii) as Chinese graphite electrode producers continue to increase their production capacity, the output of graphite electrodes is also expected to grow rapidly. To meet the global demand for graphite electrodes (excluding China), it is anticipated that more and more Chinese graphite electrode producers will actively expand their production capacity, thereby increasing the output of ultra-high power graphite electrodes.

Source: Frost & Sullivan report

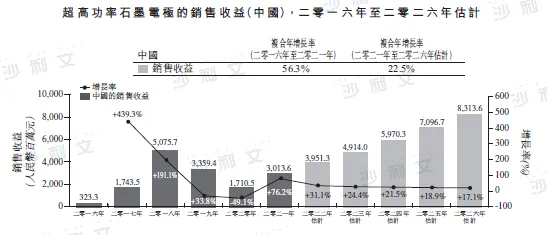

From 2016 to 2018, the sales revenue of ultra-high power graphite electrodes in China saw a significant increase, mainly due to a substantial rise in the price of these electrodes. From 2019 to 2020, due to the decline in the price of ultra-high power graphite electrodes and the impact of the COVID-19 pandemic, the sales revenue of graphite electrodes in China dropped significantly. In the future, with the recovery of ultra-high power graphite electrode prices and the growth in downstream demand from arc furnace steel, the sales revenue of ultra-high power graphite electrodes in China is expected to reach RMB 831.36 billion by 2026.

Source: Frost & Sullivan report

Key market drivers of the graphite electrode market in China

-

Stable industrial development

From 2016 to 2021, China's industrial added value increased from approximately RMB 24.5 trillion to RMB 34.3 trillion, with a compound annual growth rate of 7.0%. This also reflects the good development trend of China's industry. The development of China's industry has promoted the steady development of downstream applications of graphite electrodes, such as the arc furnace steel market, the industrial silicon market, and the yellow phosphorus market. Therefore, stable industrial development is one of the main driving forces for the development of China's graphite electrode market.

-

Strict environmental protection regulations and policies

In recent years, the Chinese government has promulgated a series of environmental protection-related regulations and policies, accelerating technological innovation among graphite electrode producers. The aim is to promote industrial integration and eliminate backward production capacity. For example, the 'Action Plan for the Comprehensive Control of Air Pollution in Autumn and Winter 2019-2020 in the Beijing-Tianjin-Hebei Region and Surrounding Areas' issued by Chinese government agencies in October 2019 stipulates that carbon producers that do not meet the requirements of pollution discharge permit management need to suspend production. Affected by this policy, Chinese graphite electrode producers that fail to meet environmental protection requirements must shut down their production facilities. This move is beneficial for leading graphite electrode producers (such as Shengneng Group) with environmentally friendly production processes and the ability to produce high-quality graphite electrodes, further increasing their market share and competitiveness.

-

Demand growth in the steel industry

Since the main downstream application of graphite electrodes is in electric arc furnace steelmaking, the graphite electrode market is thus affected by the development of the steel industry. In recent years, the Chinese government has promulgated a series of policies aimed at reducing excess steel production capacity, such as the 'Opinions on Resolving Excess Capacity and Achieving Decent Development in the Steel Industry' issued in 2016, which aim to replace outdated crude steel production capacity with electric arc furnace steelmaking. This policy has promoted the development of China's electric arc furnace steel market. As graphite electrodes are essential consumables for electric arc furnace steelmaking, the development of China's electric arc furnace steel market has also stimulated demand for graphite electrodes.

-

Advanced and mature technology

Technological innovation has greatly promoted the industrial transformation and upgrading of China's graphite electrode market. Most graphite electrode producers, especially some leading enterprises in the industry, focus on applying environmental protection technologies to graphite electrode production. Advanced and mature technology is very important for producing high-quality graphite electrodes and reducing energy consumption during the graphite electrode production process. Therefore, advanced and mature technological innovation plays a crucial role in the healthy development of China's graphite electrode market.

Competitive landscape of the graphite electrode market in China

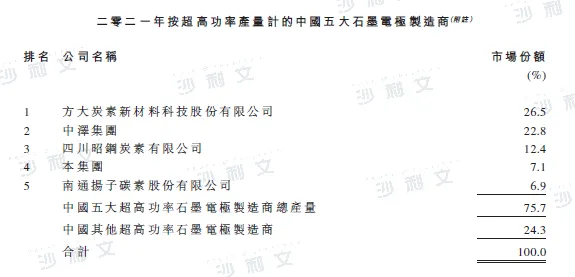

In China, only a few graphite electrode manufacturers can produce ultra-high power graphite electrodes. In 2021, by ultra-high power output, the top five ultra-high power graphite electrode manufacturers in China accounted for about 75.7% of the market share of ultra-high power graphite electrodes in China, among which Shengneng Group's market share was about 7.1%.

Note: The output of ultra-high power graphite electrodes only includes those factories operated by these companies in China.

Data source: Annual report of the company, Frost & Sullivan report

Frost & Sullivan has extensive research experience in the chemical and materials industries, assisting well-known enterprises in successfully accessing the capital market. Successful listings include: China Graphite (2237.HK), Jinli Yongci (6680.HK), Avia Avian (IDX: AVIA), Global New Materials (6616.HK), Dafeng Equipment (2153.HK), Yihai International (8659.HK), GHW (9933.HK), Sanhe Fine Chemicals (0301.HK), Xingyu Holdings (2346.HK), Xinghe Holdings (1891.HK), Xuyang Group (1907.HK), Long Resources (1712.HK), Shandong Gold (1787.HK), Henan Jinma (6885.HK), Industrial New Materials (8073.HK), Dongguang Chemicals (1702.HK), Zhongqi Group (1932.HK), Xinbang Holdings (1571.HK), Meigu Technology (8349.HK), Huajin International (2738.HK), Flot Glass (6865.HK), Dinos (1452.HK), Caike Chemicals (1986.HK), Chang'an Renheng (8139.HK), Sansida (1337.TWSE), Born.NYSE, CPC.NYSE, Gu N.YSE, Tianhe Chemicals (1619.HK), Yihua Holdings (2121.HK), Sijia Group (1863.HK), and others.

Recommended Reading

03. Frost & Sullivan assisted Avia Avian in successfully going public in Indonesia (IDX: AVIA)

07. Frost & Sullivan assists GHW in successfully listing on the Hong Kong Stock Exchange (9933.HK)

22. Frost & Sullivan assists Dinos in successfully listing on the Hong Kong Stock Exchange (1452.HK)

*The above order is not sequential and is arranged in reverse chronological order based on listing time.