Shanghai Shangmei Cosmetics Co., Ltd. (hereinafter referred to as 'Shanghai Shangmei') successfully went public on December 22, 2022. The company plans to issue a total of 36.958 million shares globally, including 3.6958 million shares in Hong Kong, China, and 33.2622 million shares internationally, with an additional 15% over-allotment rights. The final issue price is HK$25.20 per share, and the net proceeds from the company's fundraising are approximately HK$835.1 million.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing the relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business, and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

Investment highlights

The company is a leading domestic cosmetics company, transcending cycles and remaining forever youthful;

The company's outstanding R&D capabilities continue to empower innovation and sustainable development;

The company's outstanding cross-border supply chain management capabilities ensure product quality and meet flexible production needs;

The company has a wide and active omnichannel retail and distribution network, achieving efficient consumer reach;

The company's continuously innovative marketing strategies have continuously enhanced brand strength, making the brand image deeply rooted in people's hearts;

The experienced management team is highly visionary and encourages a dynamic corporate culture.

According to the Frost & Sullivan report, in terms of retail sales in 2021, the company:

Ranked fourth among Chinese domestic cosmetics companies;

Ranked third among skin care products of domestic brands in China;

Ranked first among Chinese domestic brand facial mask products;

Ranked first among domestic branded maternal and infant care products in China.

Overview of the Cosmetics Industry in China

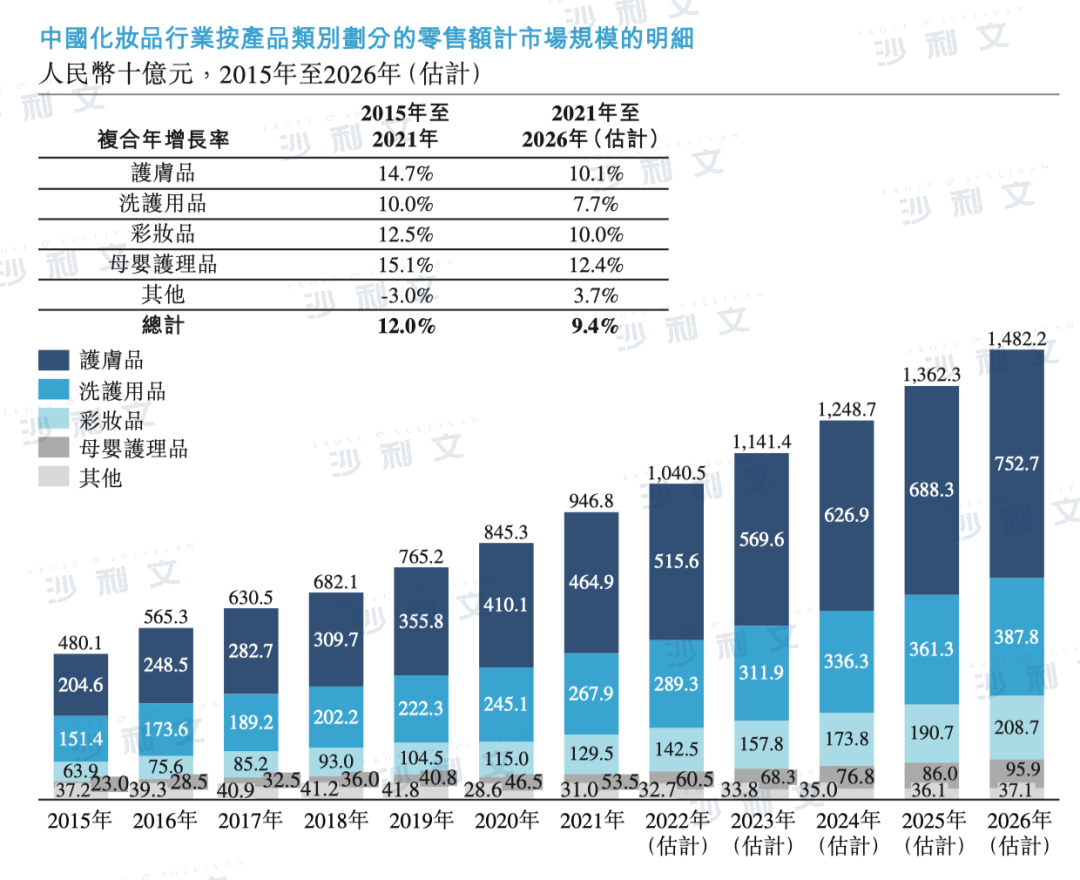

China has the world's second-largest cosmetics market. Due to China's economic development and increased personal consumption expenditure, the cosmetics market in China experienced rapid growth from 2015 to 2021. In terms of retail sales, the market size of the cosmetics market in China increased from 480.1 billion yuan in 2015 to 946.8 billion yuan in 2021, with a compound annual growth rate of 12.0%. During the same period, the global cosmetics market size grew at a compound annual growth rate of 2.2%. Among all major economies in the world [1], China's cosmetics industry has the fastest growth rate. It is estimated that the market size of the cosmetics market in China (by retail sales) will reach 1.4822 trillion yuan in 2026, growing at a compound annual rate of 9.4% starting from 2021.

[1] Major economies refer to countries with nominal GDP exceeding $2 trillion in 2021.

Source: Frost & Sullivan report

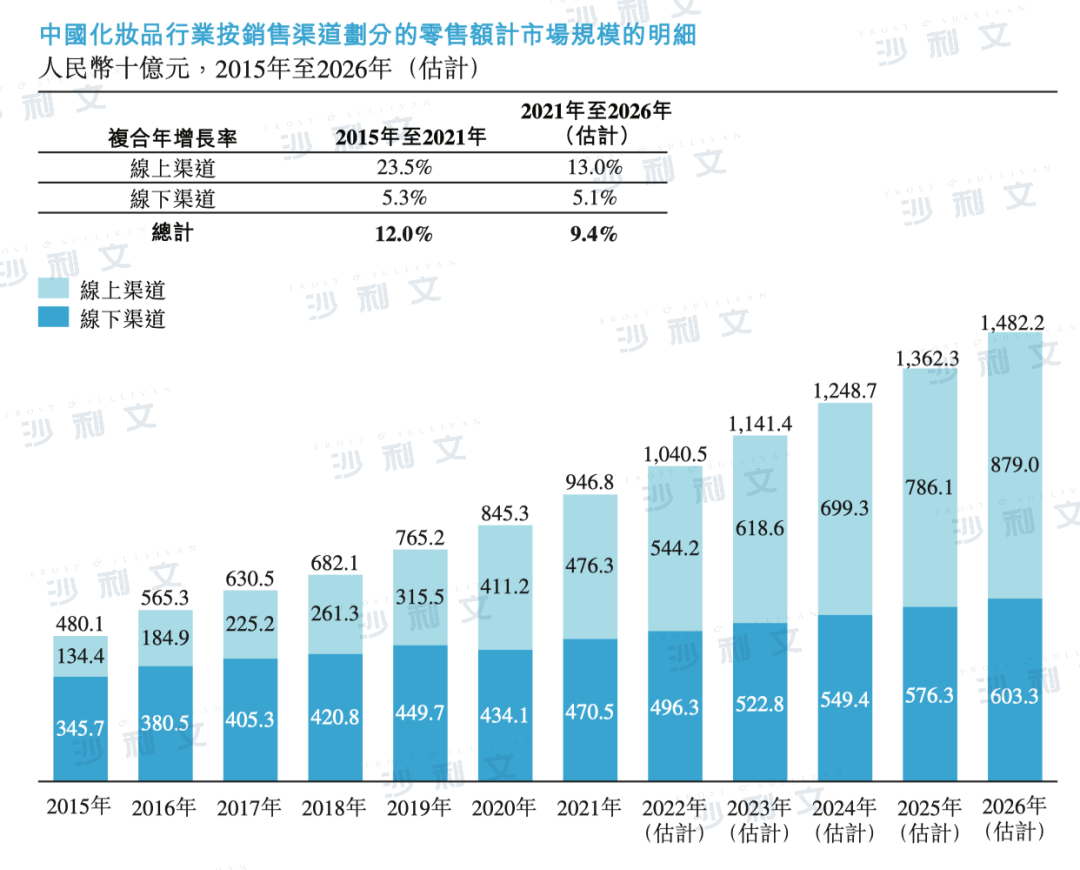

The sales of cosmetics through offline channels have maintained a steady growth and are expected to reach 603.3 billion yuan by 2026. Thanks to the development of e-commerce platforms in China, retail sales of cosmetics have rapidly increased through online channels. According to a Frost & Sullivan report, the compound annual growth rate of online channel retail from 2015 to 2021 was 23.5%. In 2021, the total retail sales of cosmetics generated online in China reached 476.3 billion yuan, beginning to surpass offline channels.

Source: Frost & Sullivan report

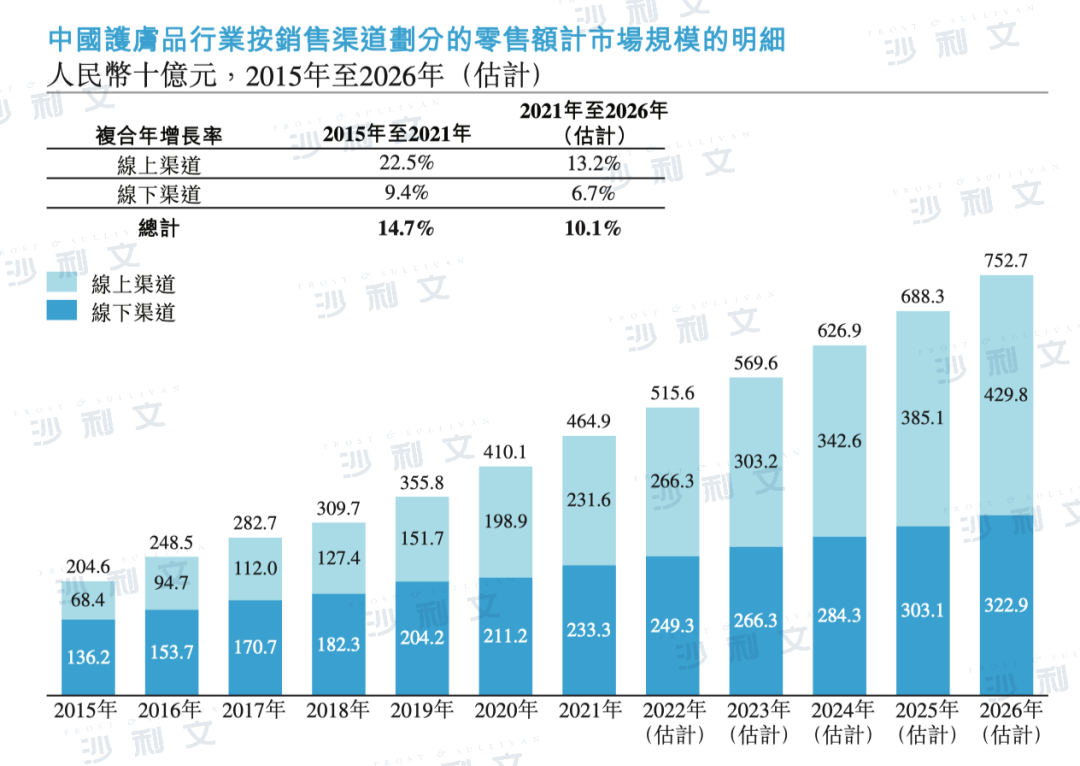

Overview of the Chinese skincare industry

Skin care products refer to those that can improve the overall condition of the skin, soothe skin conditions, and address specific skin concerns such as acne, pigmentation, fine lines, and inflammation. Skin care products are the largest category in the entire cosmetics market, accounting for 49.1% of the market share based on retail sales in 2021.

(i) Consumers have generally formed a long-term skincare concept, preferring to use skincare products to solve skin problems;

(ii) There is a trend towards younger consumers starting to come into contact with and use skincare products;

(iii) E-commerce platforms are thriving, with the Z generation and millennials becoming one of the main purchasing forces for cosmetics. The rise of social media and live streaming sales has stimulated consumers' online consumption and improved their shopping experience;

Source: Frost & Sullivan report

Overview of China's Maternal and Infant Care Products Industry

Maternal and Infant Care Products are defined as skin and personal care products specifically designed for pregnant women, newborn mothers, and children (under 12 years old). With the improvement of living standards, Chinese consumers' demand for high-quality and safe products designed for pregnant women and children is increasing, which will drive the development of the maternal and infant care product market. The increasingly mature e-commerce environment also provides more convenient purchasing channels for pregnant women and newborn mothers.

According to a Frost & Sullivan report, from 2015 to 2021, the market size of China's maternal and infant care products industry grew at a compound annual rate of 15.1%, reaching 535 billion yuan in 2021. The market size is expected to reach 959 billion yuan by 2026, growing at a compound annual rate of 12.4% starting from 2021. The growth rate is mainly driven by Chinese consumers' increasing willingness to spend on maternal and infant care products. From 2015 to 2021, the market size of online channels rose at a compound annual rate of 30.1%. It is estimated that over the next five years, it will further increase at a compound annual rate of 17.1%, making online channels the main driving force for expanding the Chinese maternal and infant care product market.

Source: Frost & Sullivan report

The competitive landscape of the Chinese cosmetics industry

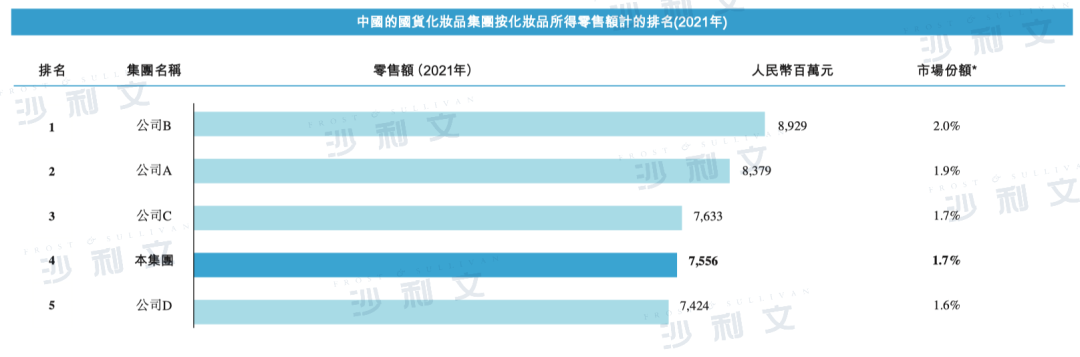

According to a Frost & Sullivan report, the cosmetics market in China is relatively fragmented, with the top five participants accounting for 21.9% of the market share, all of which are international groups. In 2021, Shanghai Shangmei Cosmetics had a retail turnover of 7.556 billion yuan, accounting for 1.7% of the domestic cosmetics market share and ranking fourth among Chinese domestic cosmetics companies.

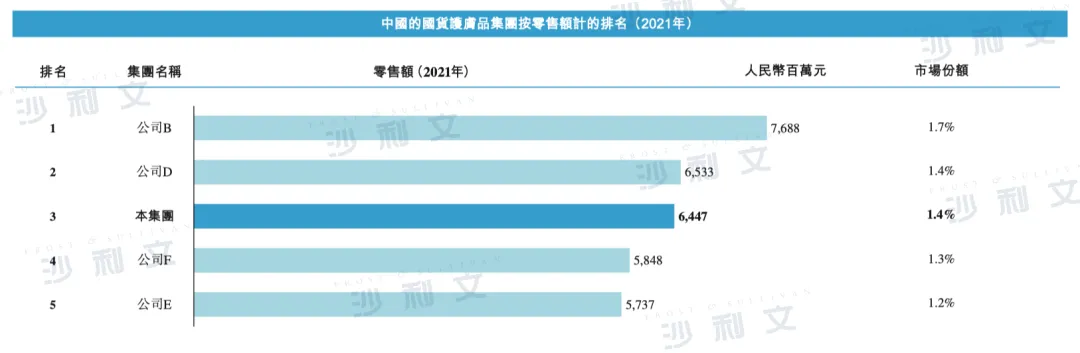

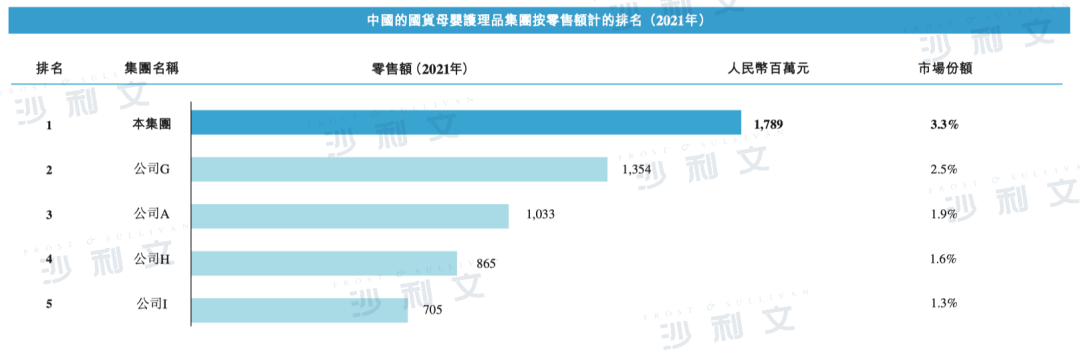

In terms of segmented categories, according to a Frost & Sullivan report, in 2021, Shanghai Shangmei ranked third among domestic brands for skin care products with retail sales of 6.447 billion yuan; first among domestic brands for facial masks with retail sales of 1.842 billion yuan; and first among domestic brands for maternity and infant care products with retail sales of 1.789 billion yuan.

Source: Frost & Sullivan report

Source: Frost & Sullivan report

Source: Frost & Sullivan report

Source: Frost & Sullivan report

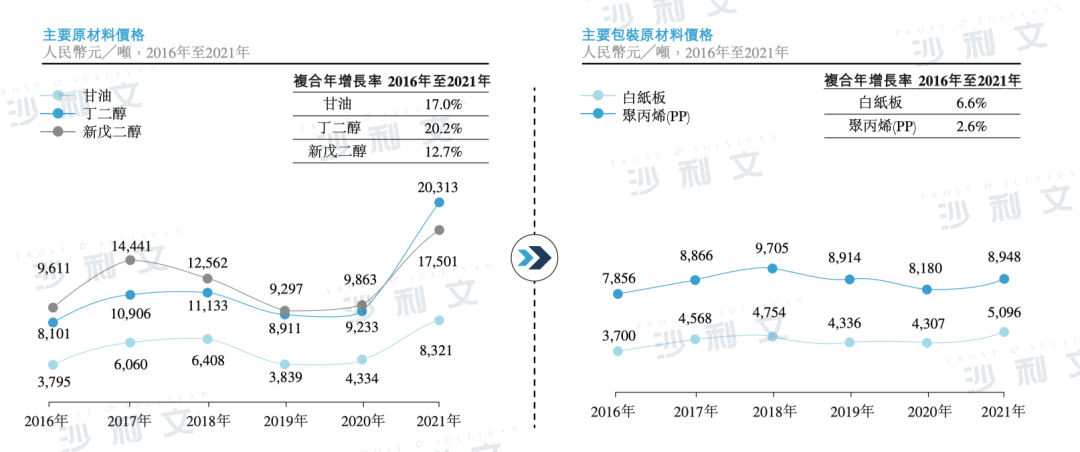

Market prices of major cosmetic raw materials in China

Raw material costs are a major cost item for cosmetic companies. The main ingredients of skincare products include moisturizers, oils, and active ingredients. Packaging materials include glass bottles, plastics, paper boxes, etc.

According to a Frost & Sullivan report, from 2016 to 2021, the price per ton of glycerin increased from 3,795 yuan to 8,321 yuan, with a compound annual growth rate of 17.0%. In 2021, the prices per ton of butylene glycol and neopentyl glycol reached 20,313 yuan and 17,501 yuan respectively, with compound annual growth rates of 20.2% and 12.7% from 2016 to 2021.

Since 2016, the Chinese government has implemented a series of environmental protection policies, phasing out some backward production facilities in the chemical industry. This led to the suspension of raw material production and supply shortages, causing prices of glycerin, butanediol, and neopentadiene to rise. Since 2018, manufacturers of such raw materials have resumed operations after several years of structural adjustment in the chemical industry, resulting in a decline in raw material prices. In 2021, major global economies continued their monetary easing policies. Coupled with supply logistics disruptions due to overseas epidemic prevention and control, domestic restrictions on the production of high-polluting and high-energy-consuming industries, etc., these factors indirectly pushed up the prices of main raw materials such as butanediol and glycerin.

Source: Frost & Sullivan report

Key market drivers of the cosmetics industry in China

-

Consumption willingness and ability have improved

Compared with developed countries (such as the United States, Japan, and South Korea), China's per capita consumption of cosmetic products is still relatively low. According to a Frost & Sullivan report, there is a strong positive correlation between per capita disposable income and per capita expenditure on cosmetic products. With the steady growth of the Chinese economy and the improvement in living standards of the Chinese people, China's per capita expenditure on cosmetics is expected to continue to grow in the future.

-

Functional product requirements are increasing

With the development of the cosmetics market, more niche markets have emerged in the industry, focusing on meeting consumers' various functional needs. Cosmetics companies are encouraged to innovate and further enrich their product offerings. Products with specific functions such as anti-aging effects, sensitive skin care, whitening, oil control and acne treatment, anti-wrinkle, and hydration can provide Chinese consumers with more choices, thereby increasing their purchasing frequency.

-

Consumer base expands

The emergence of innovative marketing methods such as Rednote, Weibo, Douyin, and live streaming platforms has improved the shopping experience for internet users and cultivated consumers' interest in cosmetics. Diversified online shopping channels and marketing activities can better match the consumption habits of younger consumer groups such as Generation Z and Millennials, who are becoming the main force in cosmetic consumption.

-

Supply chain maturity

China has formed a comprehensive supply chain for the cosmetics industry. A mature supply chain will enable domestic and foreign cosmetic companies to develop and produce products more effectively and efficiently, in order to meet the ever-changing market demands.

-

Policy benefits

Both the central and local governments of China have issued favorable policies to encourage the development of the cosmetics industry. For example, the '14th Five-Year Plan' clearly states that it is necessary to cultivate domestic high-end cosmetic brands and products in China. In addition, the 'Shanghai Cosmetics Industry High-Quality Development Action Plan (2021-2023)' proposes to strive for a cosmetics market scale of 300 billion yuan by 2023, forming 10 leading enterprises with annual operating income exceeding 5 billion yuan, as well as having 3 to 5 leading brands that are heading towards international markets. The 'Several Opinions on Promoting the Development of Shanghai's Beauty and Health Industry' propose that by 2025, Shanghai's beauty and health industry should form an industrial level worth hundreds of billions, cultivating 10 key industry enterprises with annual sales revenue exceeding 10 billion yuan. Moreover, local governments in Zhejiang, Guangdong, and other places have introduced favorable policies for the cosmetics industry, such as the 'Zhejiang Province Cosmetics Industry High-Quality Development Implementation Plan (2020-2025)' and the 'Guangdong Province Cosmetics Industry High-Quality Development Implementation Plan'.

Frost & Sullivan has extensive research experience in the consumer retail industry and has assisted many well-known enterprises in successfully listing on capital markets. Successful listings include: JuZi Biotech (2367.HK), China COSCO (1880.HK), MingChuang Youpin (9896.HK), Jiulongwang Food (1927.HK), Vesync (2148.HK), Blue Moon (6993.HK), PopMart (9992.HK), MingChuang Youpin (NYSE:MNSO), Nongfu Spring (9633.HK), Fengxiang Food (9977.HK), China Feihai (6186.HK), Taobao Sports (6110.HK), China National Tobacco International (6055.HK), Youpin 360 (2360.HK), Wugu Mofang (1837.HK), BABO Tree (1761.HK), Deying Holdings (2250.HK), Bins International (1705.HK), Golden Cat Silver Cat (1815.HK), Miming Life Department Store (8473.HK), Nissin Foods (1475.HK), Debao Group (8436.HK), Seiko China (NASDAQ:SECO), Barbie Bebe (8297.HK), Asia Grocery (8413.HK), Chowking Duck (1458.HK), COFCO Meat (1610.HK), Dali Foods (3799.HK), Vientiane International (0288.HK), Chow Tai Fook (1929.HK), Jumei Youpin (NYSE:JMEI), and others.

Recommended Reading

09. Frost & Sullivan assists Mingchuangyoupin in successfully going public in the US (NYSE:MNSO)

Frost & Sullivan helps Barbie Beige successfully go public in Hong Kong (8297.HK)

*The above order is not sequential and is arranged in reverse chronological order based on listing time.