China Graphite Group Co., Ltd. (hereinafter referred to as 'China Graphite') was successfully listed on July 18, 2022, with a global issuance of 400 million shares at a price of HK$0.325 per share.

During the Hong Kong listing process, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, sponsor, and other professional intermediary institutions in completing the writing of relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important sections), assisting the issuer in communicating with the Hong Kong Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on industry-related issues from the Hong Kong Stock Exchange.

Overview of China's Graphite Industry

Definition and Classification

Graphite is a mineral composed of carbon atoms arranged in a hexagonal crystal structure, appearing gray to black in color, opaque, and having a metallic luster. Natural graphite is mined from deposits in metamorphic rocks such as marble, gneiss, and schist, originating from the accumulation of vein deposits. Natural graphite is usually formed by the metamorphism of organic matter accumulated in sedimentary rocks. Due to its important applications in the aviation and energy sectors, especially in emerging non-carbon energy fields, graphite is considered a strategic mineral.

Graphite flakes with good crystallization have a metallic black luster, while microcrystalline materials appear as a black earthy substance with an amorphous appearance. Flake graphite concentrate can also be further processed into spherical graphite.

-

flake graphite concentrate

Sphalerite concentrate refers to the commercial name for graphite crystals that are between 40 micrometers and 4 centimeters in size and well-formed. Sphalerite concentrate can exist in specific metamorphic rocks, such as limestone, gneiss, and schist, in flaky or scaly forms. Sphalerite concentrate is extracted by flotation. Most sphalerite concentrates are produced through chemical beneficiation processes. Sphalerite concentrate is produced in many locations around the world. Major producing areas include China, Brazil, India, Madagascar, Germany, Austria, Norway, Canada, Zimbabwe, etc. The main uses of sphalerite concentrate include refractory materials, brake discs, lubricants, batteries, and expanded graphite applications.

-

spherical graphite

Spherical graphite is made from flake graphite concentrate produced from graphite ore and is one of the key raw materials for lithium-ion batteries. Under normal circumstances, flake graphite concentrate is formed into spherical shapes through mechanical abrasion processes. The smooth shape of spherical graphite allows the negative electrode of lithium-ion batteries to more effectively encapsulate particles, thereby improving the energy and charging capacity of the battery. Lithium-ion batteries require spherical graphite of different sizes because particle size affects the performance indicators of the battery. For example, small spherical graphite particles are used for lithium-ion batteries with faster charging requirements, while larger spherical graphite particles are needed for those with higher power demands.

The cleaning technology for spherical graphite involves the continuous application of comprehensive preventive environmental protection strategies in operations and manufacturing to reduce risks to human health and the workplace environment. As the world transitions towards a clean and green energy platform, many lithium-ion battery manufacturers are actively seeking alternative supply solutions. Leading graphite suppliers are committed to adopting sustainable and safe spherical graphite production procedures for green energy and clean technologies.

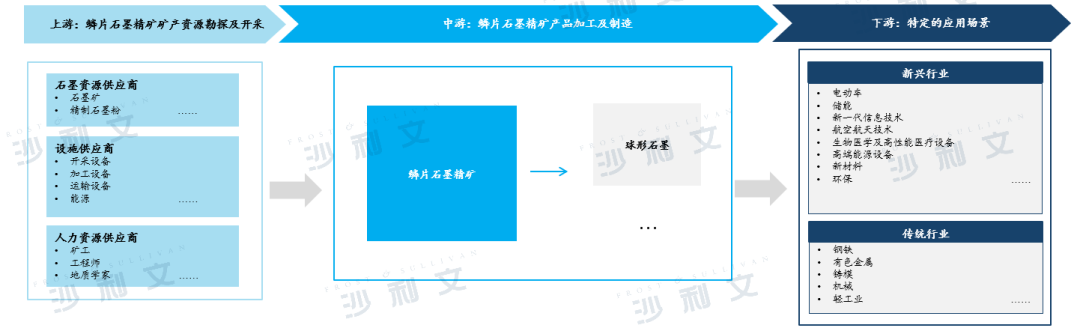

Analysis of the Industrial Chain in the Flake Graphite Concentrate Industry

The industry participants in the industrial chain of flake graphite concentrate mainly include mine owners, flake graphite concentrate distributors, flake graphite concentrate product manufacturers, and end consumers.

The upstream of the flake graphite concentrate industry mainly includes suppliers of graphite resources, including suppliers of graphite ore and refined graphite powder, mining equipment, processing equipment, and other facilities, transportation equipment, and energy sources, as well as human resource suppliers. Flake graphite concentrate is sold to midstream graphite product manufacturers after ore mining and primary processing, which are further processed into material-grade graphite products. Flake graphite concentrate can also be sold by mine owners to graphite distributors, who in turn sell it to graphite manufacturers. Midstream manufacturers further process the graphite. The downstream of the flake graphite concentrate industry is the broad application field of various graphite products.

Driven by continuous technological upgrades and policy incentives, the application scope of flake graphite concentrate products has expanded to many emerging fields such as electric vehicles, consumer electronics, energy storage, information technology, aerospace, and more. The following figure presents the industrial chain of the flake graphite concentrate industry:

Serpentine graphite concentrate industry industrial chain

Source: Frost & Sullivan report

Market scale of China's graphite industry

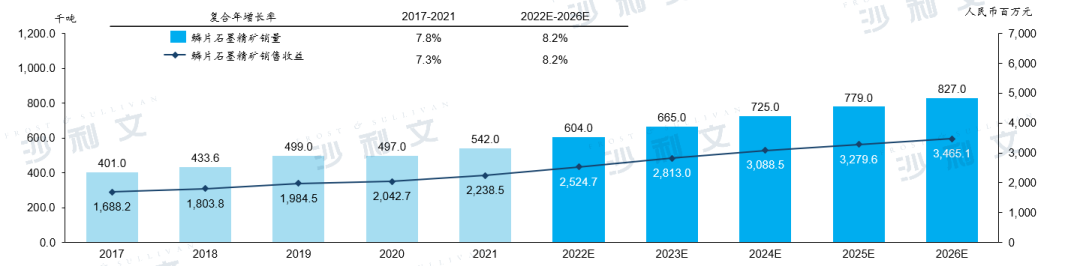

Currently, due to its unique chemical and physical properties, the possibility of graphite being replaced by other minerals is relatively low. Spinel graphite concentrate is very suitable for a variety of industrial and technological applications. The main uses of spinel graphite concentrate include batteries, refractory materials, casting, lubricants, and so on. The battery sector is expected to be one of the fastest-growing application areas during the forecast period. Due to the increasing use of new energy vehicles and energy storage systems, the Chinese lithium-ion battery market is expected to grow rapidly. Therefore, the demand for spinel graphite concentrate will further rise. Since 2017, the sales volume and revenue of spinel graphite concentrate in China have been steadily increasing. In 2021, the sales volume and revenue of spinel graphite concentrate were 542,000 tons and RMB 22.385 billion respectively.

Graphite mining technology is continuously improving and being refined, with emerging technologies such as the Internet of Things, drones, and automation already being adopted. As the core material for electric vehicle batteries, coupled with the active promotion of policies such as the '14th Five-Year Plan for National Economic and Social Development (2021-2025) and the Outline of Long-Range Objectives Through the Year 2035', as well as the increasing demand from downstream markets, the graphite industry is expected to see higher growth rates in the coming years.

Driven by favorable industry policies, technological progress in graphite manufacturing, and increased demand from downstream industries, it is expected that the sales volume of flake graphite concentrate will increase to about 827,000 tons in 2026, with a compound annual growth rate of about 8.2% starting from 2022. It is also expected that the sales revenue from flake graphite concentrate will further increase to about RMB 34.651 billion in 2026, with a compound annual growth rate of about 8.2% starting from 2021. The following chart shows the past and forecasted sales volume and revenue of flake graphite concentrate in China:

Sales volume and revenue of China's flake graphite concentrate2017 - 2026E

Source: Frost & Sullivan report

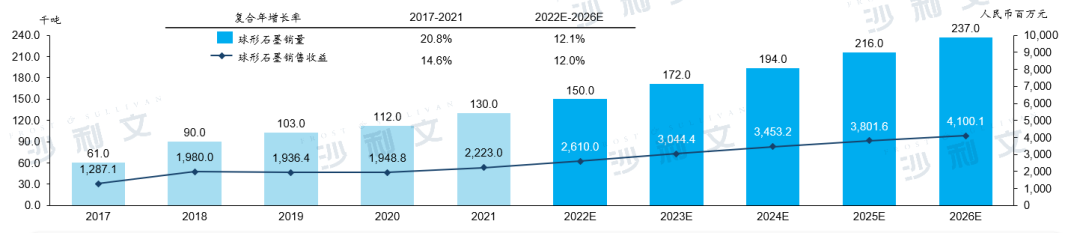

Spherical graphite is made from flake graphite concentrate and can be used as one of the main raw materials for producing lithium-ion batteries. Driven by continuous policies in electric vehicle manufacturing and the electronic information industry, as well as the ongoing carbon neutrality and green energy initiatives, sales of electric vehicles continue to increase. The booming development of the electric vehicle industry has promoted the growth in demand for lithium-ion batteries over the past few years, further driving the market development of spherical graphite.

In the past five years, the sales volume of spherical graphite in China has risen rapidly at a compound annual growth rate of about 20.8%, increasing significantly from about 61,000 tons in 2017 to about 130,000 tons in 2021. Similarly, sales revenue has also benefited from the huge market demand, rising from about 12.871 billion yuan in 2017 to about 22.23 billion yuan in 2021, with a compound annual growth rate of about 14.6% during the same period.

China accounts for the vast majority of battery-grade spherical graphite processing and consumption in the world. It is expected that in the near future, due to the huge demand from downstream markets, the precision processing technology of spherical graphite will continue to improve. The encouragement policies for new energy vehicles, especially the 'Notice on Further Improving the Fiscal Subsidy Policy for the Promotion and Application of New Energy Vehicles' issued by the Ministry of Finance, the Ministry of Industry and Information Technology, the Ministry of Science and Technology, and the National Development and Reform Commission in December 2020, will further promote the production of new energy vehicles and the demand for lithium-ion batteries. Seven departments including the National Development and Reform Commission issued the 'Implementation Plan for Promoting Green Consumption' on January 21, 2022, proposing to vigorously develop green transportation consumption.

In the future, China's sales volume of spherical graphite is estimated to surge from about 150,000 tons in 2022 to about 237,000 tons in 2026, with a compound annual growth rate of about 12.1%. Sales revenue is expected to increase from about RMB 26.1 million in 2022 to about RMB 41.001 billion in 2026, with a compound annual growth rate of about 12.0%. The following chart illustrates the past and forecasted sales volume and revenue of spherical graphite in China:

China's spherical graphite sales volume and revenue, 2017 - 2026E

Source: Frost & Sullivan report

Market-driven factors and development trends

According to the Frost & Sullivan report, the main drivers and development trends of China's graphite industry include the following aspects:

(1) Wide application and increasing downstream demand:

The largest consumption of graphite is in steelmaking and refractory materials applications in the metallurgical field; however, the use of emerging technologies in batteries, large-scale fuel cells, and lightweight high-strength composite materials may significantly increase global demand for graphite.

-

There is a high demand for refractory material manufacturing.

The development of the refractory materials manufacturing industry has increased demand for graphite. One of the main uses of natural graphite is the production of refractory materials (such as magnesia-carbon refractory bricks, crucibles, ladles, and molds containing molten metal), closely linking graphite demand with industries such as metallurgy, steelmaking, chemical engineering, petroleum, machinery manufacturing, silicates, and electricity. According to the World Steel Association, China's crude steel output reached 10.328 billion tons in 2021 and is expected to increase to about 12 billion tons by 2025. Although the graphite industry has made significant progress in other emerging application areas in recent years, the refractory materials manufacturing industry remains the largest consumer of graphite. As the metallurgical and steelmaking industries continue to prioritize their roles in economic development, future graphite demand will remain strong.

-

The demand for lithium-ion batteries has increased

The graphite consumption growth structure is gradually shifting from traditional industries to strategic emerging industries such as new energy vehicles, energy storage, nuclear energy, and electronics, with rapid growth. Graphite has significantly better electrical conductivity than other non-metals and is currently the most widely used anode material for lithium-ion batteries. Lithium-ion batteries are smaller, lighter than traditional batteries, but have greater power and a flatter voltage curve, almost providing full power before discharge. As the world transitions towards clean energy in the fields of new energy vehicles and energy storage, the global demand for cost-effective energy storage solutions will continue to drive the growth of both the lithium-ion battery market and the graphite market. Specifically, China's electric vehicle industry has developed rapidly over the past few years. Driven by policy incentives and technological progress, the application market space for graphite in the electric vehicle sector will be further unleashed.

In addition, lithium-ion batteries have high energy density, large power density, and high efficiency, making them one of the main energy storage systems globally. They are widely used in various energy storage fields such as grid energy storage, household energy storage, and communication energy storage. With the continuous development of industries such as clean energy, distributed grids, microgrids, and new energy vehicle charging stations, the market demand for lithium-ion batteries will further increase, which will also promote the application of graphite. Therefore, under the global trend of energy conservation and environmental protection, the driving force for future lithium-ion battery market demand will mainly come from transportation and industrial energy storage, thereby promoting the continuous rapid growth of the graphite industry.

-

Emerging demand for expanded graphite

Expanded graphite, like lithium-ion batteries, is one of the fastest-growing markets, but its market size is currently quite small. The manufacturing of expanded graphite involves treating flake graphite with a dilute acid solution, heating it to cause the flakes to split and expand, increasing their volume by hundreds of times. This material is pressed into sheets and has a wide range of applications, including thermal management in consumer electronics, advanced building materials, heat-resistant and corrosion-resistant gaskets, flow batteries, and fuel cells. The amount of graphite consumed in the future may be equivalent to the total for all other uses. In addition, expanded graphite has been the only category in the graphite market that has seen price increases in recent years. The emerging commercial applications and unpredictable potential of expanded graphite are important new forces driving the development of the graphite industry.

(2) Improvement and innovation in mining and production technology:

-

Develop advanced technology for deep processing of high-end products

With continuous breakthroughs in deep processing technologies such as chemical and thermal purification techniques, coating technology, carbonization technology, etc., the mass production and wide application of high-end graphite products such as spherical graphite, expanded graphite, high-purity graphite, flexible graphite, and graphene can be achieved in the near future. For example, applying chemical purification technology to further purify graphite concentrate to a total graphitic carbon content (TGC) of 99.99% for producing high-tech products such as fuel cells requires a purity higher than that typically achieved after flotation optimization. To obtain ultra-high purity graphite, it is necessary to remove fine impurities between graphite layers, which can be achieved through single-stage or multi-stage pickling using different acids or combinations. An alternative method for acid treatment is to heat graphite above 2,000 degrees Celsius for thermal purification.

High-end graphite products have become an indispensable key material in strategic emerging industries such as aerospace, nuclear energy, new energy vehicles, energy storage, nuclear power, environmental protection, and new materials. The industrialization and successful application of graphene have once again elevated the strategic status of graphite. Modern high-end deep processing of graphite will be an important driving force for promoting the upgrading of China's graphite industry and one of the most important ways for Chinese graphite manufacturers to enter the global market.

-

Improvement of graphite mining technology

In the process of graphite mining, the application of technologies such as automation, Internet of Things (IoT), and underground drone 3D surveying and mapping is becoming increasingly widespread. These technologies improve safety, enhance performance and productivity, and reduce mining costs. The use of highly automated and efficient equipment for rough processing and flotation of graphite is beneficial for the beneficiation of high-carbon flake graphite concentrates without severely damaging the graphite crystals. IoT enables machines and equipment to be smarter and more efficient by using sensors, which also helps save time, achieve safer mining, predictive maintenance, and obtain other benefits related to automation, energy, and cost.

In addition, 3D surveying and mapping of graphite mines allows engineers and designers to plan layouts and action plans before entering the mine site, thereby shortening the preparation period. The 3D surveying and mapping of graphite mines is carried out by deploying underground survey drones equipped with sensors that can scan the surrounding environment of the mining area and establish 3D diagrams. In addition to 3D surveying and mapping, the sensors on underground survey drones can also be used to monitor the liquid level, temperature, and vibration of the mining area, allowing for timely maintenance based on evidence without waiting for scheduled routine operations.

(3) Favorable policy environment:

-

The regulatory system for the graphite industry is more scientific and comprehensive.

Recently, China has been committed to improving and upgrading the graphite industry by establishing regulatory foundations. The 'Graphite Industry Specification Conditions' promulgated by the Ministry of Industry and Information Technology in July 2020 set high standards for processing technology, product quality, and resource protection in the graphite industry. With the strategic importance of graphite resources increasing, the graphite industry chain is undergoing integration and upgrading trends. Currently, the domestic graphite industry is still in a state of low-end and mixed development, with supply exceeding demand for low-end products. The promulgation of new regulations is expected to promote the industry's transformation towards high-value-added products and technological innovation as the foundation.

In addition, the project 'Key Technologies and Demonstrations for Reducing the Source of Graphite Resource Mining and Processing' has been successfully approved by the Ministry of Science and Technology. The project focuses on solving bottlenecks in deep processing technology, proposing solutions and technical approaches for producing high-end graphite products, and is expected to enhance the technology for using and recycling solid graphite waste.

-

Support measures for the downstream graphite industry

Graphite and the emerging material graphene are widely used in many downstream sectors, such as new-generation information technology, energy conservation and new energy vehicles, power generation equipment, and new materials. This is the main development area promoted by 'Made in China 2025'. According to the newly released 'New Energy Vehicle Industry Development Plan (2021-2035)' in November 2020, key technologies such as batteries, automotive engines, and vehicle driving systems are expected to make significant breakthroughs by 2025. Based on policy support and technological development, the market space for graphite applications in the electric vehicle sector will further expand.

In addition, China has also promulgated a series of policies to support the development of the graphite industry, including 'Several Opinions on Accelerating the Innovative Development of the Graphene Industry', 'Development Guidelines for New Materials Industries', 'First Batch of Application Demonstration Guidance Catalogs for Key New Materials (2019 Edition)', etc. These policies have established graphene's important strategic position in electrochemical energy storage, offshore engineering, flexible electronic devices, major environmental protection technologies and equipment, automotive and aerospace industries.

Competitive landscape analysis

According to a Frost & Sullivan report, in 2021, the sales revenue of China's flake graphite concentrate industry reached RMB 22.385 billion. The flake graphite concentrate business of China Graphite Group Co., Ltd. ranked fifth in terms of sales revenue and accounted for 4.4% of the overall flake graphite concentrate market share.

According to a Frost & Sullivan report, in 2021, the sales revenue of China's spherical graphite industry reached 22.23 billion yuan. The spherical graphite business of China Graphite Group Co., Ltd. ranked sixth in terms of sales revenue, accounting for 4.1% of the overall spherical graphite industry market share.

Frost & Sullivan has extensive research experience in the chemical and materials industries, assisting well-known enterprises in successfully accessing capital markets. Successful listings include Jinli Yongci (6680.HK), Avia Avian (IDX: AVIA), Global New Materials (6616.HK), Dafeng Equipment (2153.HK), Yihai International (8659.HK), GHW (9933.HK), Sanhe Fine Chemicals (0301.HK), Xingyu Holdings (2346.HK), Xinghe Holdings (1891.HK), Xuyang Group (1907.HK), Long Resources (1712.HK), Shandong Gold (1787.HK), Henan Jinma (6885.HK), Xingye New Materials (8073.HK), Dongguang Chemicals (1702.HK), Zhongqi Group (1932.HK), Xinbang Holdings (1571.HK), Meigu Technology (8349.HK), Huajin International (2738.HK), Flot Glass (6865.HK), Dinos (01452.HK), Caike Chemicals (1986.HK), Chang'an Renheng (8139.HK), Sansida (01337.TWSE), Born NYSE, CPC NYSE, Gu NYSE, Tianhe Chemicals (01619.HK), Yihua Holdings (02121.HK), Sijia Group (01863.HK), and others.

Recommended Reading

02. Frost & Sullivan assisted Avia Avian in successfully going public in Indonesia (IDX: AVIA)

06. Frost & Sullivan assists GHW in successfully listing on the Hong Kong Stock Exchange (9933.HK)

16. Frost & Sullivan assists Zhongqi Group in successfully going public in Hong Kong (1932.HK)