Maiwei Biotechnology (Shanghai) Co., Ltd. (hereinafter referred to as 'Maiwei Biotechnology') was successfully listed on January 18, 2022, with an issue of 99.9 million shares at an issue price of 34.80 yuan per share.

Maiwei Biotechnology is a biopharmaceutical company focusing on areas such as autoimmune diseases, oncology, metabolism, ophthalmology, and infectious diseases. It has currently built a rich R&D pipeline in multiple fields. The company takes it as its responsibility to improve the quality of life and health levels for all mankind. Guided by unmet clinical needs in the global pharmaceutical market, it starts with urgently needed biosimilars and adopts a rapid follow-up and first-in-class R&D and commercialization strategy. It strengthens its original innovation capabilities, actively introduces new scientific teams, improves and upgrades existing technology platforms, continuously tracks cutting-edge targets, conducts basic research and translational research in advantageous fields, forms process development and quality research capabilities, and gradually realizes the research and development of innovative drugs with independent intellectual property rights, safety, effectiveness, and benefits to the public. Frost & Sullivan has long been paying attention to the global and Chinese biopharmaceutical industries, has published a large number of research reports, which are widely cited in the prospectuses of leading science and technology innovation board listed companies in the industry, helping customers accelerate their growth.

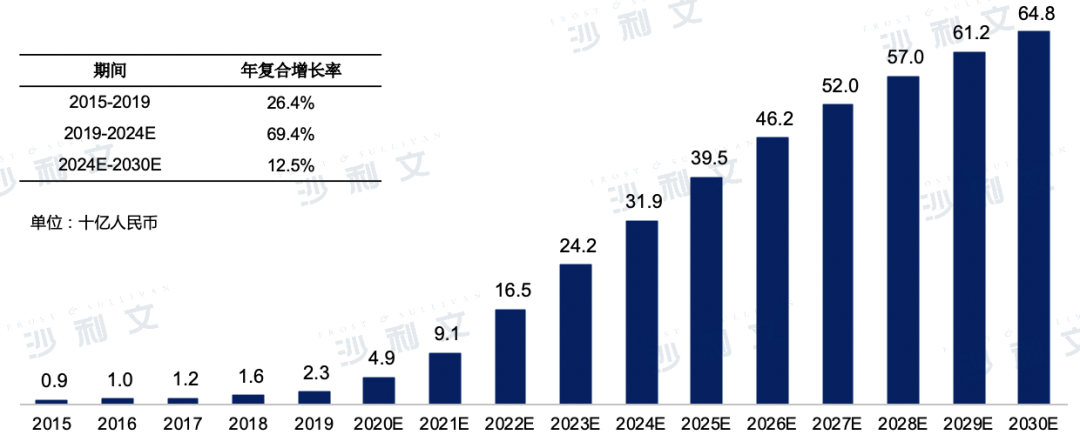

Market scale of biosimilar drugs in China

The sales revenue of the Chinese biosimilar market is expected to grow from RMB 2.3 billion in 2019 to RMB 319 billion in 2024, with a compound annual growth rate of 69.4%. It is also expected to continue growing at a compound annual rate of 12.5%, reaching RMB 648 billion by 2030. The details are shown in the following figure:

Market Scale and Forecast of Biosimilars in China

2015 to 2030 (estimated)

Data source: Analysis by Frost & Sullivan

Autoimmune disease drug market

Overview of Autoimmune Diseases

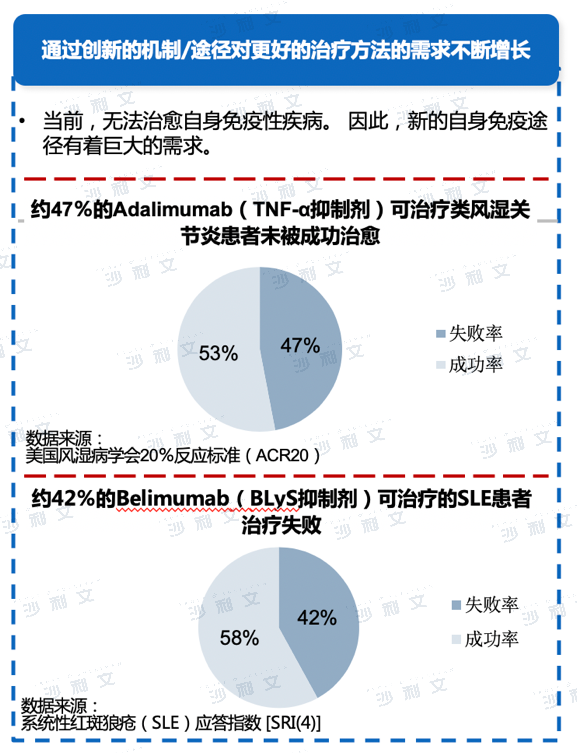

Autoimmunity refers to a disease caused by the immune system of the body responding to its own tissue components, leading to damage to those tissues. Common autoimmune diseases include rheumatoid arthritis, ankylosing spondylitis, psoriasis, lupus erythematosus, and others. These diseases usually have a recurrent course and are characterized by a chronic protracted process. The main drugs for treating autoimmune system diseases include non-steroidal anti-inflammatory drugs (NSAIDs), glucocorticoids, and immunosuppressants. The research and development of drugs for autoimmune diseases is primarily based on biotechnological means, so currently, biological products account for the vast majority of autoimmune drugs. Among the world's best-selling drugs, the autoimmune disease drug adalimumab has been in dominant position for seven consecutive years.

Data source: Analysis by Frost & Sullivan

Systemic steroids and immunosuppressants can help control hyperactive immune responses, reduce inflammation, and alleviate symptoms such as pain, swelling, fatigue, and rashes. Although they can effectively reduce pain, fever, and inflammatory reactions, their efficacy is limited to treating the symptoms caused by autoimmune diseases. In contrast, targeted biologics aim to treat diseases at the root cause of the disease, thereby improving bodily functions and preventing irreversible damage, leading to a remission of the disease. Compared to drugs such as steroids and immunosuppressants, targeted biologics can achieve greater effects, but there are still problems with their application in clinical practice. For example, although TNF-α inhibitors have dominated the global autoimmune therapy biologics market in recent years, studies have shown that about 47% of rheumatoid arthritis patients experience treatment failure due to TNF-&alpha.

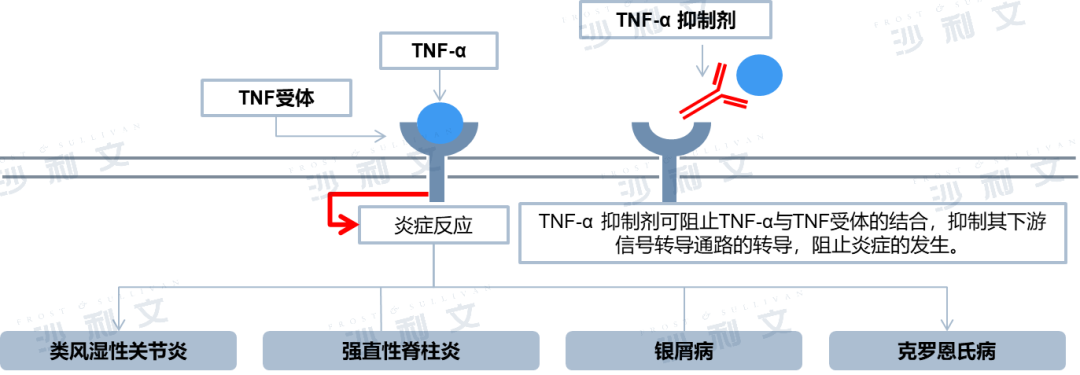

Overview of TNF-α inhibitors

TNF-α is a potent inducer of inflammatory responses and a key regulator of innate immunity, involved in autoimmune and immune-mediated diseases such as rheumatoid arthritis, ankylosing spondylitis, and psoriasis. Anti-TNF-α monoclonal antibodies that inhibit the immune response to TNF-α are a new generation of therapies for treating immune-mediated inflammatory diseases, characterized by high efficacy, safety, and convenient administration.

Xiumei Le®Adalimumab, developed by AbbVie, is a humanized monoclonal antibody targeting TNF-α. It was approved for marketing in the United States in 2002 and has been successively approved for more than 10 indications over the past decade, including rheumatoid arthritis, ankylosing spondylitis, psoriasis, Crohn's disease, juvenile idiopathic arthritis, and uveitis. It was launched in China in 2010, with approved indications in China including ankylosing spondylitis, rheumatoid arthritis, plaque psoriasis, juvenile idiopathic arthritis of the joint type, moderate to severe active adult Crohn's disease, non-infectious intermediate uveitis, posterior uveitis, and panuveitis. Multiple new indications are currently under application. Humira®The patent expired in China in 2016, and currently several Chinese pharmaceutical companies have conducted clinical trials and started production applications for adalimumab biosimilars, such as Myovant Biologics' MW01. With the launch of biosimilars and the expansion of indications for original drugs, the adalimumab market will achieve rapid growth.

Mechanism of action of TNF-α inhibitors

Data source: Literature review, Frost & Sullivan analysis

Antitumor Drug Market Overview

Overview of Tumor Diseases and Epidemiological Analysis

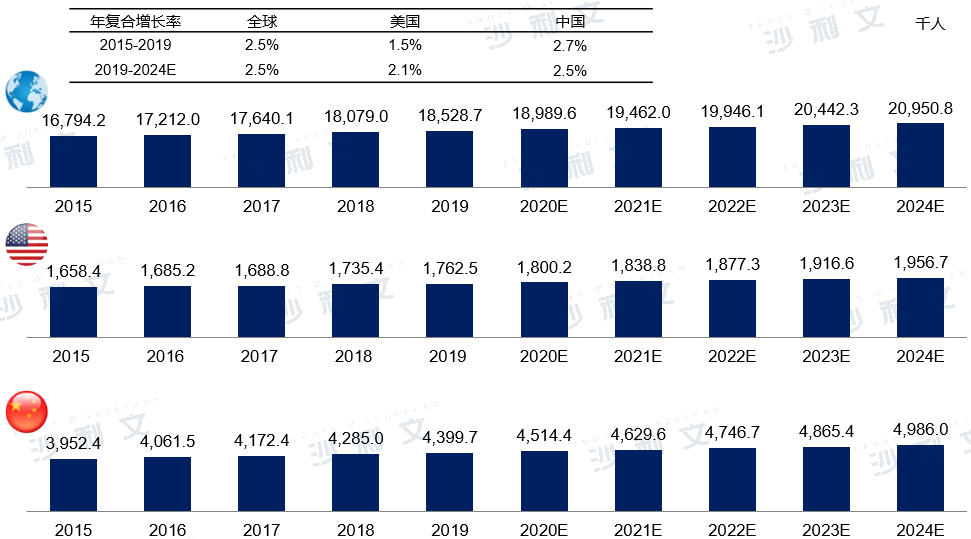

Affected by various objective factors such as lifestyle changes, environmental changes, and increased work pressure, the global incidence of cancer has been steadily increasing since 2015. By 2019, there were 18.529 million new cases globally. It is estimated that by 2024, the number of new cancer cases worldwide will reach 20.951 million, with a compound annual growth rate of 2.5% from 2019 to 2024. In the United States, the number of new cancer cases in 2019 was 1.763 million, with an annual compound growth rate of 1.5% from 2015 to 2019. It is expected that in 2024, there will be 1.957 million new cancer patients in the United States. The growth rate of new cancer cases in China has exceeded the global and US levels for the same period over the past five years. It is expected that in the next five years, with the aging population process, the number of new cancer cases in China will still increase rapidly. In 2019, the number of new cancer patients in China reached 4.4 million, with a compound annual growth rate of 2.7% from 2015 to 2019. It is estimated that in 2024, there will be 4.986 million new cancer patients in China.

Market Scale and Forecast of Biosimilars in China

2015 to 2030 (estimated)

Data source: Analysis by Frost & Sullivan

Overview of the Bone Metastasis Drug Market

Bone metastases are a common complication of cancer. The most common primary cancers that lead to bone metastases include breast cancer, prostate cancer, lung cancer, kidney cancer, and thyroid cancer. In addition, multiple myeloma can also involve the bones. When cancer metastasizes to the bones, it is named after the corresponding body part; for example, breast cancer that has metastasized to the bones is referred to as breast cancer bone metastases. Sometimes, bone metastases occur at the time of the patient's initial cancer diagnosis or are discovered before the primary tumor is found. Bone metastases occur in different locations and cause different clinical manifestations, mainly characterized by bone damage and pain. Typical symptoms of bone metastases include pain, loss of normal mobility or ability to live a lifestyle, fractures, and elevated calcium levels in the blood.

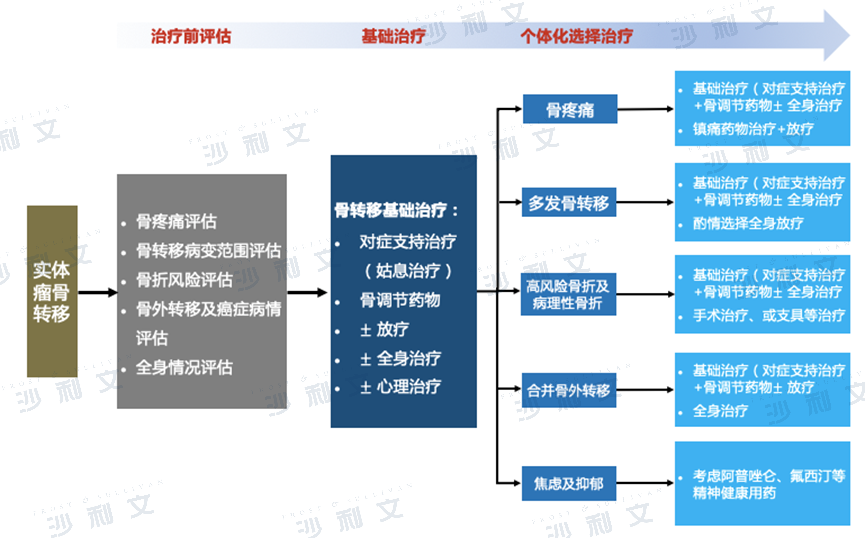

The goals of treating bone metastases from solid tumors are to improve quality of life, prolong life, alleviate symptoms and psychological distress, prevent or delay pathological fractures, etc. When bone metastases occur in solid tumors, it is a systemic disease that requires a comprehensive treatment approach primarily based on systemic therapy, including: systemic treatment for the primary disease (chemotherapy, molecular targeted therapy or immunotherapy), radiotherapy, surgery, drug analgesia (osteoclast inhibitors such as bisphosphonates, denosumab, etc.), and psychological support therapy. Treatment principle: Primarily based on systemic therapy, where chemotherapy, molecular targeted therapy, and immunotherapy can be used as individualized anti-tumor treatment methods for lung cancer, breast cancer, colorectal cancer, etc. Specific principles can refer to the diagnostic and treatment guidelines for related primary cancers.

Diagnosis and treatment pathway for bone metastases of solid tumors

Data source: Diagnosis and Treatment Guidelines, Frost & Sullivan analysis

Overview of the Neutropenia Drug Market after Chemotherapy

Neutropenia after chemotherapy is a hematological toxic reaction that occurs during chemotherapy, after the use of myelosuppressive drugs, resulting in a peripheral blood neutrophil absolute value (ANC) less than 1.5×10^9/L. Patients clinically present with symptoms such as fever exceeding 38°C, abdominal pain and diarrhea, coughing, difficulty breathing, frequent urination and urgency, altered consciousness, headache, redness and edema at the puncture site, and abnormal vaginal discharge. In severe cases, it can lead to complications such as sepsis syndrome, septic shock, and even death, thereby increasing treatment costs and reducing the effectiveness of chemotherapy.

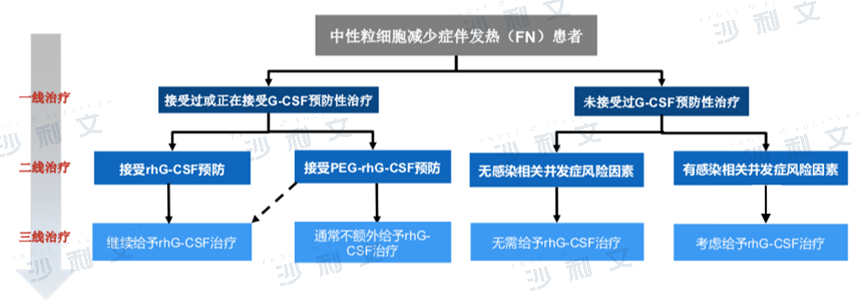

The treatment pathway for neutropenia is as follows: a) If prophylactic use of granulocyte colony-stimulating factor (G-CSF) has not been received, an infection complication risk assessment must be conducted first. If the risk of infection is assessed to be present, rhG-CSF therapy should be considered. b) For those who have received or are receiving G-CSF prophylaxis, it is recommended to use rhG-CSF therapy or pegylated rhG-CSF therapy. c) For patients receiving pegylated rhG-CSF therapy, if their ANC remains less than 0.5×109/L for 3 days or more, rhG-CSF therapy should be considered.

Treatment pathway for neutropenia after chemotherapy

Source: 'Guidelines for the Standardized Management of Neutropenia Related to Tumor Radiotherapy and Chemotherapy 2017', analysis by Frost & Sullivan

Overview of the Anti-PD-L1 Bispecific Antibody Drug Market

Dual-specific antibodies recognize and specifically bind to two antigens or epitopes. Theoretically, they block the biological functions mediated by both antigens/epitopes simultaneously, or bring two antigens closer together and enhance their interaction. In recent years, a deeper understanding of the pathogenesis of various diseases and the rapid development of therapeutic monoclonal antibodies have also promoted the development and progress of dual-specific antibodies. With the advancement of antibody construction, expression, and purification technologies, dozens of structures have emerged in dual-specific antibodies. Currently, the application and research of existing dual-specific antibodies are mainly concentrated in the field of tumor treatment.

Development history of bispecific antibodies

Data source: Literature review, Frost & Sullivan analysis

Antibody-conjugated drug market overview

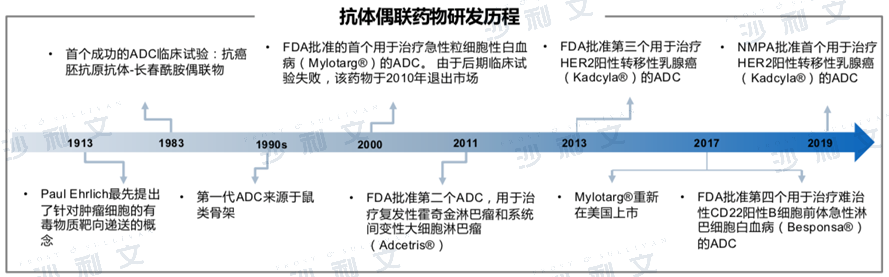

Antibody-drug conjugates (ADCs) are complex molecules composed of monoclonal antibodies and bioactive cytotoxic chemotherapeutic drugs. They represent a promising new type of targeted drug for tumor treatment. Unlike chemotherapy, ADCs aim to target and kill only cancer cells. These modified antibodies can selectively deliver activated cytotoxic drugs into tumor cells by specifically binding to antigens on the surface of cancer cells, thereby enhancing anti-cancer efficacy and ultimately reducing drug toxicity. The main mechanism of action is as follows: First, the antibody part of the ADC specifically binds to the antigenic epitope on the cancer cell surface. Then, through endocytosis, it enters the interior of the cancer cell, where it is released into the active cytotoxic drug in a special environment within lysosomes or at low pH values, ultimately specifically killing the cancer cells.

Although the concept of antibody conjugate drugs was proposed as early as 1913, its research has undergone a rather tortuous development process.

Data source: Literature review, Frost & Sullivan analysis

Metabolic drug market

Postmenopausal osteoporosis

Postmenopausal osteoporosis refers to a metabolic disease in postmenopausal women where bone density decreases and bone tissue structure changes due to the decline in estrogen levels. The main cause is the reduction of estrogen, which leads to greater bone resorption by osteoclasts than bone formation by osteoblasts, resulting in decreased bone density. This affects calcium salt deposition, leading to increased bone resorption and significant bone loss, forming osteoporosis. Postmenopausal osteoporosis usually has no clinical symptoms until it is triggered by mild stress such as hunchback or bone pain, which can lead to fractures. The pathogenesis involves a decrease in the expression of osteoprotegerin (OPG) due to estrogen deficiency, an increase in the expression of nuclear factor-kappa B receptor activator (RANKL) from the tumor necrosis factor family, leading to a disruption of the RANKL-RANK-OPG axis. This results in an increase in osteoclasts and a decrease in osteoblasts, ultimately causing bone loss.

For most osteoporosis patients with high fracture risk, bisphosphonate drugs such as alendronate and ibandronate can be selected as initial treatment. For patients with very high fracture risk or who cannot use oral treatment, parathyroid hormone/related peptide analogues such as teriparatide and abaloparatide can be considered for initial treatment. In addition, ibandronate or selective estrogen receptor modulators such as raloxifene can be used as initial treatment drugs for patients requiring spinal-specific treatment.

ophthalmic drug market

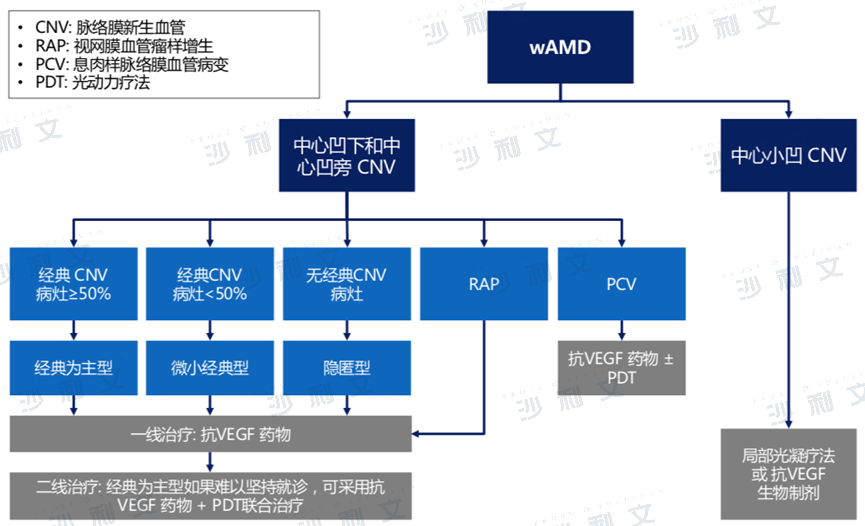

Overview of Wet Age-Related Macular Degeneration (WAMD)

Age-related macular degeneration (AMD) is a degenerative retinal disease that leads to gradual loss of central vision and is also the main cause of irreversible blindness in the elderly. Wet age-related macular degeneration (wAMD) is a clinical manifestation of AMD, characterized by the growth of new blood vessels under the macular cortex that bleed and leak fluid, leading to retinal detachment, scar formation, and irreversible blindness. The main risk factors for the disease include aging, genetics, smoking, and having AMD symptoms in one eye. Although wet AMD accounts for only about 10% of AMD patients, 80% to 90% of blindness cases come from patients with wet AMD. In addition, although AMD usually occurs in one eye at a time, about 50% of patients with wet AMD experience the same condition in their other eye within 5 years after symptoms appear in one eye.

Diagnostic and Therapeutic Pathway for WAMD

Source: Diagnostic and Therapeutic Guidelines, Literature, Frost & Sullivan analysis

Overview of Infectious Diseases

Infectious diseases are usually caused by microscopic pathogens such as bacteria, viruses, fungi, or parasites that directly or indirectly spread from one person to another and are widely prevalent. The pathogenesis involves the invasion of microorganisms into the host, where they adhere and replicate extensively within the host, producing toxins or other metabolites that damage the host. Infectious diseases can be classified into three categories based on the type of pathogen: viral infections, bacterial infections, and fungal infections. Common viral types and symptoms include: common colds caused by rhinovirus, coronavirus, and adenovirus; encephalitis and meningitis caused by enterovirus and HSV or West Nile virus; warts and skin infections caused by HPV and HSV; gastroenteritis caused by norovirus; and lung infections caused by COVID-19, among others. Common bacterial pathogens include streptococcus, staphylococcus, and pneumococcus, which can cause pharyngitis, scarlet fever, septicemia, pneumonia, meningitis, and other diseases. Fungal infections such as various mushrooms and molds can cause tinea, athlete's foot, ergotism, histoplasmosis, and some other eye and skin infections after infecting the human body. Antimicrobial drugs include antibacterial (for bacteria, fungi, etc.) drugs and antiviral drugs. Antibacterial drugs are further divided into natural antibiotics, semi-synthetic antibiotics, and fully synthetic antibacterial drugs. Common antibacterial drugs include β-lactam antibiotics, cephalosporins, macrolide antibiotics, vancomycin, and aminoglycoside antibiotics, among others.

Frost & Sullivan, integrating 61 years of global consulting experience, has dedicated 24 years to serving the booming Chinese market. With a global perspective, we help clients accelerate their business growth and achieve benchmark positions in industry growth, innovation, and leadership. The healthcare industry is one of Frost & Sullivan's core areas of focus. Over the past seventeen years, the Frost & Sullivan healthcare team has provided financing and financial advisory, IPO industry advisory, strategic consulting, management consulting, and other services to hundreds of outstanding domestic and international biopharmaceuticals, medical devices, healthcare services, and internet healthcare companies. Successful listings include: Bexcellence (2185.HK), Yonghe Medical (2279.HK), Kailiang (6821.HK), Beihai Kangcheng (1228.HK), Gushengtang (2273.HK), Yingpeng Technology (2251.HK), Clover Biotech (2197.HK), Minimally Invasive Robotics (2252.HK), Harmony Kamman (2256.HK), Kunbo Medical (2216.HK), Xianruida (6669.HK), Kangsheng Global (9960.HK), Yimaitong (2192.HK), Tengsheng Bopai (2137.HK), CanSino (2162.HK), Chaoyu Ophthalmology (2219.HK), Guichuang Tongqiao (2190.HK), Huihuang Medicine (0013.HK), Koi Pharmaceutical (2171.HK), Zhaoke Ophthalmology (6622.HK), Nature's Way Pharmaceuticals (UPC.NASDAQ), Sainfo Pharmaceuticals (6600.HK), Zhaoyan New Drugs (6127.HK), Novogene Health (6606.HK), Tianyan Pharmaceuticals (ADAG.NASDAQ), Beikang Medical (2170.HK), Jianbimiao Miao (2161.HK), Minimally Invasive Heart Center (2160.HK), Ruili Medical Beauty (2135.HK), Jiaosisi Pharmaceutical (1167.HK), Hepcon Pharma (2142.HK), JD Health (6618.HK), Deqi Pharmaceuticals (6996.HK), Rongchang Biotech (9995.HK), WuXi AppTec (2126.HK), Sino Biologics (2096.HK), Yunding New Energy (1952.HK), Jiahe Biotech (6998.HK), ZaiDing Pharmaceuticals (9688.HK), Ocumvix (1477.HK), Yongtai Biotech (6978.HK), Haipure Pharmaceuticals (9989.HK), Kechuang Pharmaceutical (9939.HK), Peijia Medical (9996.HK), Kangfang Biotech (9926.HK), NuoCheng Jianhua (9969.HK), IMAB.NASDAQ, Kanglong Chemical (3759.HK), China Antibody (3681.HK), Dongyao Pharmaceuticals (1875.HK), Yasheng Pharmaceutical (6855.HK), Fuhong Hanlin (2696.HK), Hansoh Pharmaceutical (3692.HK), Mabtech Pharmaceuticals (2181.HK), Fangda Holdings (1521.HK), Via Biotech (1873.HK), CStone Pharmaceuticals (2616.HK), Junshi Biosciences (1877.HK), WuXi AppTec (2359.HK), Innovent Biologics (1801.HK), Hualing Medicine (2552.HK), BeiGene (6160.HK), Gilead Sciences (1672.HK), WuXi AppTec (2269.HK), China Resources Pharmaceutical (3320.HK), Jacobus Pharmaceutica (2633.HK), Huihuang China Medicine (HCM.NASDAQ), Gensent Bio-Tech (1548.HK), BBI Life Sciences (1035.HK), etc. In terms of the number of filings, the Frost & Sullivan healthcare team maintains an absolute leading position in Hong Kong's healthcare IPO market, continuously occupying more than 90% of the market share from 2018 to 2021.

Since the listing of the first batch of companies on the Sci-tech Innovation Board in July 2019, Frost & Sullivan reports have been widely cited in the prospectuses of leading Sci-tech Innovation Board listed companies, including: Yarong Medicine (688176.SH), BeiGene (688235.SH), Jiahe Meikang (688246.SH), Dizhe Medicine (688192.SH), Novogene (688105.SH), Chengda Biology (688739.SH), Geke Microelectronics (688728.SH), Huaxi Biotechnology (688363.SH), Junshi Biosciences (688180.SH), Zhejiang Genomics (688266.SH), BeiGene-TheraSight (688177.SH), and Shenzhou Cells (688520.SH). They are considered the most powerful, professional, and influential industry research institutions in the sector. We hope to work with enterprises to understand industry trends, seize development opportunities, jointly promote innovation and upgrading of China's healthcare industry, and build a healthy future.

Recommended Reading

Frost & Sullivan helps Saisun Pharma successfully go public in Hong Kong (6600.HK)

38. Frost & Sullivan assists Zai Lab to successfully list on the Hong Kong Stock Exchange (9688.HK)

46. Frost & Sullivan assisted Tianjing Biology in successfully going public in the US (IMAB.NASDAQ)

51. Frost & Sullivan helps Fosun Pharma successfully list on the Hong Kong Stock Exchange (2696.HK)

55. Frost & Sullivan helps Via Biologics successfully list on the Hong Kong Stock Exchange (1873.HK)

58. Frost & Sullivan helps WuXi AppTec successfully list on the Hong Kong Stock Exchange (2359.HK)

61. Frost & Sullivan helps BeiGene successfully list on the Hong Kong Stock Exchange (6160.HK)