Jiangxi Jinli Yongci Technology Co., Ltd. (hereinafter referred to as 'Jinli Yongci') successfully went public on January 14, 2022. The global number of shares issued was 125 million, with an offer price of HK$33.80 per share, raising approximately HK$4.045 billion.

During the Hong Kong listing process, Frost & Sullivan mainly undertook the following tasks: helping the company accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the company's competitive advantages, assisting in the writing of relevant parts of the prospectus (such as an overview, competitive advantages and strategy, industry overview, business, and other important sections) in collaboration with the company, investment banks, and other intermediaries, facilitating communication between the company and the Hong Kong Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting in the company's feedback on various industry-related issues with the Hong Kong Stock Exchange.

Overview of the Global and Chinese Rare Earth Markets

China holds the largest reserves of rare earths. In 2020, global rare earth reserves were about 116 million tons, while China's reserves were about 44 million tons, accounting for approximately 37.9% of the global rare earth reserves. Most major heavy rare earth elements (such as holmium, dysprosium, and terbium) are located in South China regions such as Jiangxi Province, Fujian Province, Hunan Province, and Guangdong Province. In 2020, global rare earth production was about 243,300.0 tons, with China's production accounting for about 57.5% of the global rare earth production. In China, the rare earth market is dominated by six rare earth manufacturing groups. Ganzhou Rare Earths, located in Jiangxi Province, is the parent company of rare earths from southern China, and its mining quota in 2020 accounted for about 30% of China's total rare earth mining quota.

Global and Chinese Rare Earth Permanent Magnet Materials Market Analysis

A permanent magnet is an object made from a material that has been magnetized and generates its own persistent magnetic field. There are various types of permanent materials. Rare earth permanent magnets are made from rare earth element lanthanide alloys.

Neodymium iron boron permanent magnetic materials can be considered as one of the most widely used rare earth permanent magnetic materials. Generally speaking, neodymium iron boron permanent magnetic materials are mainly made from alloys of neodymium, iron, and boron to form a Nd2Fe14B tetragonal crystal structure. The basic structure of neodymium magnets consists of rectangular prisms with high potential for storing magnetic energy. In addition, the principle of neodymium iron boron permanent magnetic materials is the same as that of any other permanent magnets. Neodymium iron boron permanent magnetic materials rotate electrons to repel each other in order to disperse and gain more potential energy. A magnetic field is generated when electrons move around atomic nuclei in an arranged manner. Neodymium iron boron permanent magnetic materials can be divided into sintered neodymium iron boron permanent magnetic materials and bonded neodymium iron boron permanent magnetic materials. Sintered neodymium iron boron permanent magnetic materials can be further divided into high-performance neodymium iron boron permanent magnetic materials and ordinary neodymium iron boron permanent magnetic materials. In China, only a few manufacturers possess the capability to produce high-performance neodymium iron boron permanent magnetic materials. In the downstream market, high-performance neodymium iron boron permanent magnetic materials are mainly used in energy-saving and environmentally friendly products such as wind turbines and new energy vehicles, while other neodymium iron boron permanent magnetic materials are mainly used in magnetic separators and electroacoustic applications. In addition to neodymium iron boron permanent magnetic materials, another form of rare earth permanent magnetic material is samarium cobalt magnetic material, which accounts for only about 1% of all rare earth permanent magnetic materials and is mainly used for military applications. Theoretically, samarium cobalt magnetic materials can serve as an alternative to the downstream applications of neodymium iron boron permanent magnetic materials. In reality, due to the scarcity and extremely high price of samarium cobalt magnetic raw materials, they cannot be widely used. For example, Co (cobalt) is a strategic material in China, mainly used in military and aerospace applications. Compared with samarium cobalt magnetic materials, high-performance neodymium iron boron permanent magnetic materials are more cost-effective, and compared with ordinary neodymium iron boron permanent magnetic materials, they have higher efficiency, lower energy consumption, and stronger thermal stability. They are more attractive than other types of rare earth permanent magnetic materials and are widely used.

Compared to other rare earth permanent magnetic materials, neodymium iron boron (NdFeB) has several advantages. NdFeB permanent magnetic materials are stronger than other rare earth materials, allowing them to generate the same magnetic field with a smaller scale of use. In addition, they have strong anti-magnetic loss properties, while weaker rare earth permanent magnetic materials sometimes demagnetize under certain conditions. Moderate temperature stability enables NdFeB permanent magnetic materials to operate in relatively high-temperature environments. NdFeB motors are widely used in various industries such as wind turbines and new energy vehicle manufacturing due to their high efficiency, low energy consumption, good control performance, strong stability, as well as small size, light weight, and diverse structures.

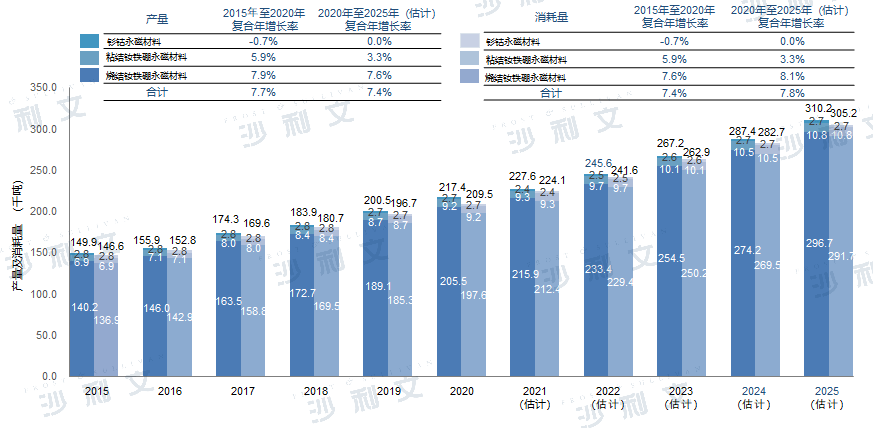

Global rare earth permanent magnet material production and consumption by type

2015 to 2025 (estimated)

Source: Frost & Sullivan report

From 2015 to 2020, the global production of rare earth permanent magnets increased from about 149,900.0 tons to about 217,400.0 tons, with a compound annual growth rate of about 7.7%. In the future, it is expected that the global production of rare earth permanent magnets will reach about 310,200.0 tons by 2025, with a compound annual growth rate of about 7.4% from 2020 to 2025.

From 2015 to 2020, the global consumption of rare earth permanent magnetic materials increased from about 146,600.0 tons to about 209,500.0 tons, with a compound annual growth rate of approximately 7.4%. In the future, the consumption of rare earth permanent magnetic materials may grow at a compound annual rate of about 7.8%, reaching approximately 305,200.0 tons by 2025.

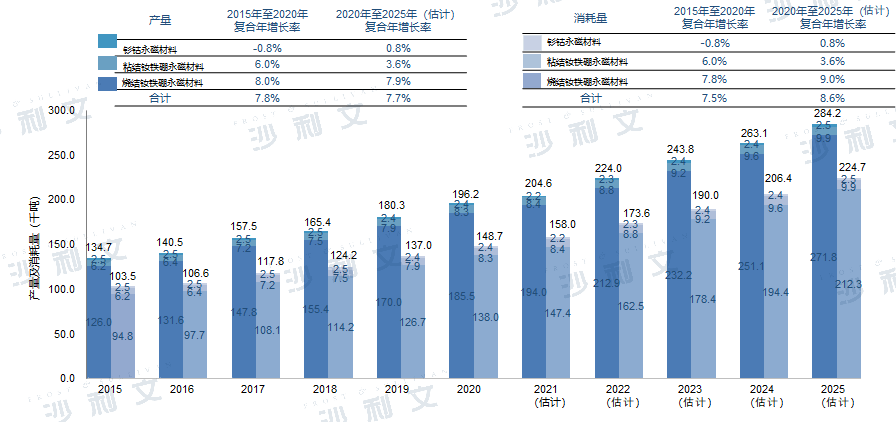

Output and Consumption of Rare Earth Permanent Magnets in China by Type

2015 to 2025 (estimated)

Source: Frost & Sullivan report

China is not only the largest producer of rare earth permanent magnets but also the largest consumer and net exporter. The surplus production after consumption is used for exports. In 2015, China's export quotas for rare earth permanent magnets were officially abolished. With the increasing demand from other countries, exports of rare earth permanent magnets are expected to increase. From 2015 to 2020, China's production of rare earth permanent magnets increased from about 134,700.0 tons to about 196,200.0 tons, with a compound annual growth rate of about 7.8%. In the future, it is estimated that China's production of rare earth permanent magnets will reach about 284,200.0 tons by 2025, with a compound annual growth rate of about 7.7% from 2020 to 2025.

In recent years, stimulated by the continuous increase in demand from downstream industries, China's consumption of rare earth permanent magnets has shown a rapid growth trend. From 2015 to 2020, China's consumption of rare earth permanent magnets increased from about 103,500.0 tons to about 148,700.0 tons, with a compound annual growth rate of approximately 7.5%. In the future, the consumption of rare earth permanent magnets may grow at a compound annual rate of about 8.6%, reaching about 224,700.0 tons by 2025. China's past consumption of rare earth permanent magnets grew in tandem with the global market, but current estimates suggest that the growth rate in the next five years will exceed global consumption due to the increasing demand for high-performance neodymium-iron-boron permanent magnets in China.

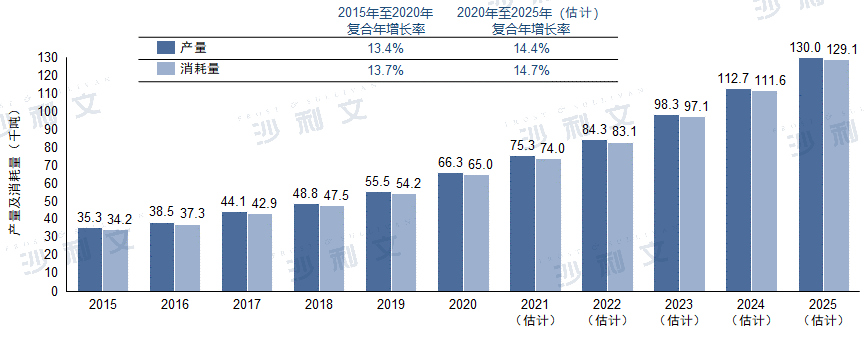

Global production and consumption of high-performance neodymium-iron-boron permanent magnetic materials

2015 to 2025 (estimated)

Source: Frost & Sullivan report

High-performance neodymium-iron-boron permanent magnet materials refer to those with an intrinsic coercivity (unit: Koe) and magnetic energy product (unit: MGOe) sum greater than 60. These materials are mainly used in wind turbines, energy-saving variable-frequency air conditioners, energy-saving elevators, new energy vehicles, industrial robots, etc. From 2015 to 2020, the global production of high-performance neodymium-iron-boron permanent magnet materials increased from about 35,300.0 tons in 2015 to about 66,300.0 tons in 2020, with a compound annual growth rate of approximately 13.4%. In the future, with the continuous increasing demand from downstream industries, it is expected that the global production of high-performance neodymium-iron-boron permanent magnet materials will reach about 130,000.0 tons by 2025, with a compound annual growth rate from 2020 to 2025 of about 14.4%.

The global consumption of high-performance neodymium-iron-boron permanent magnets increased from about 34,200.0 tons in 2015 to about 65,000.0 tons in 2020, with a compound annual growth rate of about 13.7% from 2015 to 2020. Looking ahead, the global consumption of high-performance neodymium-iron-boron permanent magnets is likely to grow at a compound annual rate of about 14.7%, reaching about 129,100.0 tons by 2025. Due to strong growth in the end markets, the growth of the high-performance neodymium-iron-boron permanent magnet market is expected to be much faster than the overall growth of the rare earth permanent magnet market. In 2020, the consumption of high-performance neodymium-iron-boron permanent magnets accounted for about 31.0% of the total consumption of rare earth permanent magnets in 2020, and it is expected to account for about 42.3% by 2025. The slight difference in global production and consumption is due to inventory.

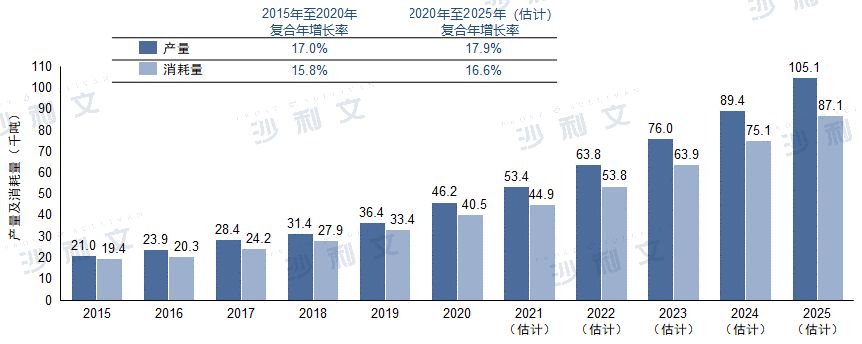

China's output and consumption of high-performance neodymium-iron-boron permanent magnetic materials

2015 to 2025 (estimated)

Source: Frost & Sullivan report

From 2015 to 2020, the production of high-performance neodymium-iron-boron permanent magnetic materials in China increased from about 21,000.0 tons in 2015 to about 46,200.0 tons in 2020, with a compound annual growth rate of about 17.0%. In the future, with the increasing demand from downstream industries, it is expected that the production of high-performance neodymium-iron-boron permanent magnetic materials in China will reach about 105,100.0 tons by 2025, with a compound annual growth rate of about 17.9% from 2020 to 2025.

The consumption of high-performance neodymium-iron-boron permanent magnetic materials increased from about 19,400.0 tons in 2015 to about 40,500.0 tons in 2020, with a compound annual growth rate of about 15.8%. To achieve carbon neutrality targets, governments around the world are taking various measures to increase the popularity of energy-saving and environmentally friendly products, including but not limited to wind turbines, energy-efficient elevators, energy-efficient variable-frequency air conditioners, and new energy vehicles, all of which are downstream applications of neodymium-iron-boron permanent magnetic materials (especially high-performance ones). The demand for such energy-saving products is expected to stimulate the demand for high-performance neodymium-iron-boron permanent magnetic materials. It is estimated that China's consumption of high-performance neodymium-iron-boron permanent magnetic materials will grow at a compound annual growth rate of about 16.6%, reaching about 87,100.0 tons by 2025. In addition to the relatively high global consumption growth rate compared to rare earth permanent magnetic materials, China's consumption growth of high-performance neodymium-iron-boron permanent magnetic materials is expected to be particularly faster than the global growth rate.

Market-driven factors

The enhancement of carbon neutrality targets boosts the demand for rare earth permanent magnetic materialsIn 2020, the Chinese government announced that it would achieve carbon peak by 2030 and carbon neutrality by 2060. To achieve this goal, the Chinese government has set specific targets in its '14th Five-Year Plan', such as a 18% reduction in carbon emissions per unit of GDP. In addition to China, most developed countries (such as the United States, Japan, the United Kingdom, Germany, Canada, and Singapore) aim to significantly reduce carbon emissions around 2030 and ultimately achieve net-zero emissions by 2050. To achieve this goal, governments around the world are taking various measures to increase the popularity of energy-saving products to reduce carbon emissions and better protect the environment in the coming years. Therefore, the popularization of products such as wind turbines, energy-saving elevators, energy-saving variable-frequency air conditioners, and new energy vehicles (all using neodymium-iron-boron permanent magnets, especially the downstream applications of high-performance neodymium-iron-boron permanent magnets) is expected to increase demand for sintered neodymium-iron-boron magnets. For example, from 2015 to 2020, the global consumption of high-performance neodymium-iron-boron permanent magnets for new energy vehicles increased at a compound annual growth rate of about 45.9%, and is expected to grow at a compound annual growth rate of about 30.9% from 2020 to 2025.

Rich rare earth resources:As the main raw material for sintered neodymium-iron-boron permanent magnets, rare earths play a crucial role in the manufacturing of these materials. For high-performance sintered neodymium-iron-boron permanent magnets, the content of heavy rare earths even determines their performance and downstream applications. In 2020, China accounted for the largest proportion of global rare earth reserves, with nearly 60% of the world's rare earth production coming from China. China is rich in rare earth resources, especially heavy rare earths, which can ensure a stable supply of rare earths to Chinese manufacturers of neodymium-iron-boron permanent magnets and relatively stable raw material prices compared to foreign manufacturers. Additionally, the new giant of rare earths, China National Rare Earth Group Co., Ltd., was established on December 23, 2021, through the merger of top state-owned enterprises. China National Rare Earth Group Co., Ltd. was jointly funded by China Aluminum Corporation Limited, China Minmetals Corporation Limited, Ganzhou Rare Earth, China Iron and Steel Research Institute Science & Technology Group Co., Ltd., and Yanyuan Technology Group Co., Ltd. Furthermore, the newly established China National Rare Earth Group Co., Ltd. will operate under the direct supervision of the State-owned Assets Supervision and Administration Commission. The establishment of China National Rare Earth Group Co., Ltd. is conducive to resource integration, improving the application level of new technologies and materials, and promoting the long-term healthy development of the rare earth industry.

Government regulations and policies support the development of the rare earth permanent magnet material market:As the main production center of the global rare earth permanent magnet material market, China has multiple regulatory policies to support and promote the development of this industry. For example, the "Guidelines for the Development of New Material Industries" issued in 2017 emphasize that high-performance rare earth permanent magnet materials, as key strategic materials, should be promoted and applied in fields such as high-speed rail permanent magnet motors, rare earth permanent magnet energy-saving motors, and servo motors. In 2020, Jiangxi Province, the main production area of rare earths in China, issued the "Implementation Opinions on Promoting the High-quality Development of the Rare Earth Industry," aiming to cultivate a group of deep-processing enterprises, accelerate the transformation and upgrading of the rare earth industry, and promote the integrated development of the rare earth permanent magnet industry, the permanent magnet motor industry, and the energy-saving equipment industry.

Future opportunities

Further development of downstream industries: In the future, it is expected that governments around the world will optimize their industrial and energy structures, accelerating the development of green and low-carbon industries such as energy conservation and environmental protection, new energy equipment, and new energy vehicles. In particular, they have made tremendous efforts to achieve future carbon neutrality, as detailed below:

-

China: The Chinese government expects to achieve carbon peak before 2030 and plans to achieve carbon neutrality by 2060;

-

United States: The U.S. government has officially committed to reducing carbon pollution by 50% to 52% by 2030 compared to 2005;

-

UK: The UK Government's official advisor on climate change, the Committee on Climate Change, claims that by 2050, the UK's net greenhouse gas emissions should be reduced to zero;

-

Canada: The Canadian Senate adopted the Net Zero Emissions Accountability Act in June 2021, officially setting Canada's net zero emissions target for 2050. The law requires the Canadian government to establish carbon emission targets and plans to achieve them every five years between 2030 and 2050;

-

Japan: Japan aims to reduce emissions by 46% compared to the 2013 level by 2030 and achieve carbon neutrality by 2050.

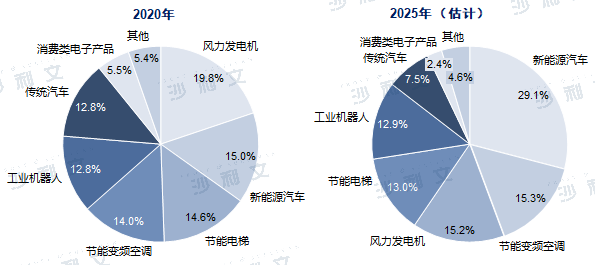

The strengthening of energy-saving and environmental protection awareness, along with technological progress, is expected to stimulate the demand for new energy vehicles, promote large-scale development of wind turbines, and accelerate the popularization rate of energy-saving variable-frequency air conditioners. New energy vehicles are becoming the largest application segment for high-performance neodymium-iron-boron permanent magnets, followed by energy-saving variable-frequency air conditioners. Wind turbines, which were previously the largest end-user segment, are expected to drop to third place. These three segments together account for about 37.6% of the total consumption in 2015, increasing to about 48.8% by 2020, and are expected to continue growing, accounting for about 59.6% of the total consumption by 2025. It is anticipated that the development of downstream industries will stimulate the consumption of rare earth permanent magnets, especially high-performance neodymium-iron-boron permanent magnets.

Consumption of Global High-Performance NdFeB Permanent Magnets by Application

(Compared with 2020 and 2025)

Source: Frost & Sullivan report

Technical improvement of manufacturing processes:The rare earth permanent magnet material market is a typical technology-intensive industry, and the technical level is crucial for the future development of participants in this industry. In the future, grain boundary penetration technology, as the core technology for manufacturing high-performance rare earth permanent magnet materials, is expected to become an important development direction for manufacturing technologies in the rare earth permanent magnet material market. In addition, surface treatment technology and equipment will develop towards more environmentally friendly and efficient directions.

Accelerated industry concentration:Currently, high-performance rare earth permanent magnet materials account for less than 50% of China's total rare earth permanent magnet material production. In the future, manufacturers lacking core competitiveness and focusing only on producing low-performance rare earth permanent magnet materials are likely to be eliminated due to fierce industry competition. On the other hand, well-known participants that possess core technologies and can provide high-quality products are expected to gain a larger market share.

Competitive landscape of the global and Chinese rare earth permanent magnet materials market

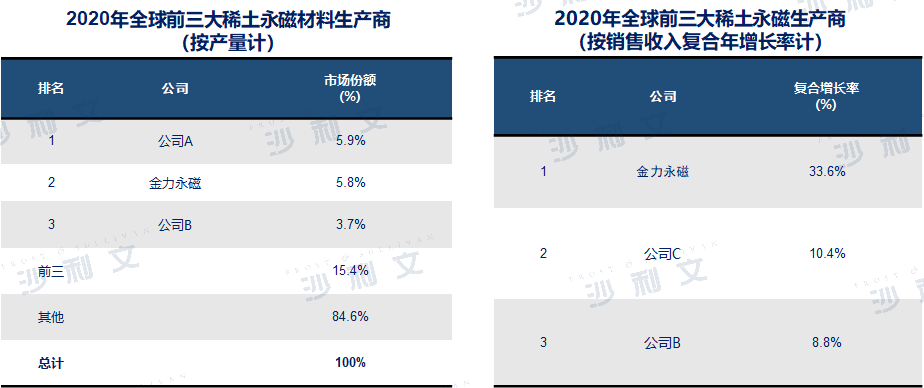

Market share of the top three participants in the global rare earth permanent magnet material market in 2020

Source: Frost & Sullivan report

The global rare earth permanent magnet material market is relatively fragmented, with the top three producers accounting for about 15.4%. Among all global rare earth permanent magnet material producers, Jinli Magnetics ranked second in terms of production volume in 2020.

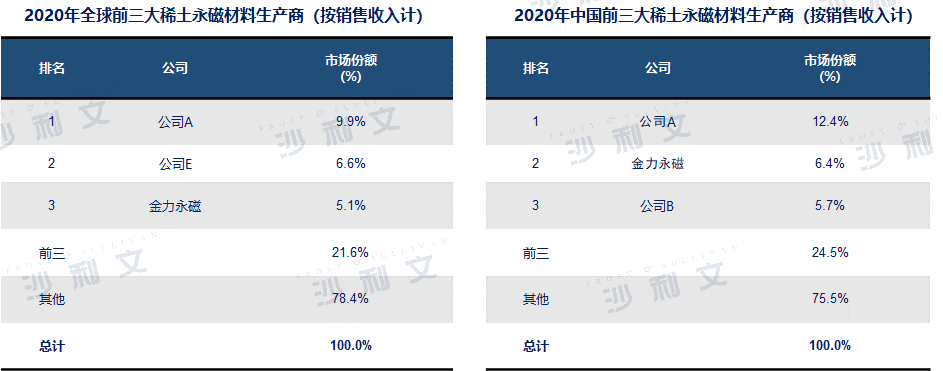

Global and Chinese Rare Earth Permanent Magnet Materials Market in 2020

Market share of the top three participants(Calculated based on sales revenue)

Source: Frost & Sullivan report

Among all rare earth permanent magnet material producers globally, Golden Magnetic ranked third in terms of sales revenue from rare earth permanent magnet materials in 2020. Among all rare earth permanent magnet material producers in China, Golden Magnetic ranked second in terms of sales revenue from rare earth permanent magnet materials in 2020.

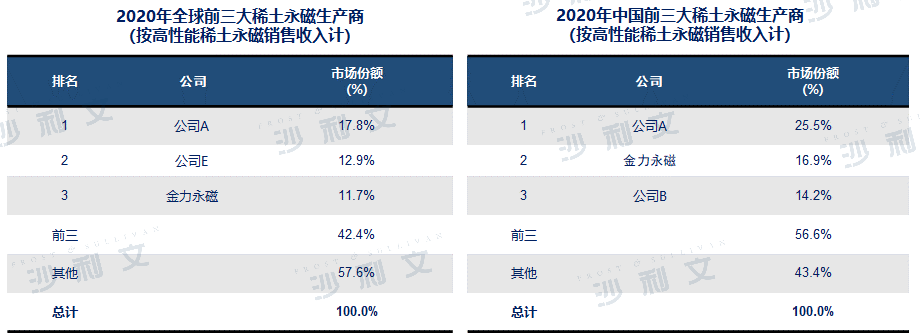

Market share of the top three participants in the global rare earth permanent magnet material market in 2020

(By output of high-performance rare earth permanent magnetic materials)

Source: Frost & Sullivan report

In 2020, among all rare earth permanent magnet material producers globally, Jinliyuanqi ranked first in terms of high-performance rare earth permanent magnet material production, with a market share of about 14.5%.

Global and Chinese Rare Earth Permanent Magnet Materials Market in 2020

Market share of the top three participants

(Calculated based on sales revenue from high-performance rare earth permanent magnetic materials)

Source: Frost & Sullivan report

Among all rare earth permanent magnet material producers globally, based on the sales revenue of high-performance rare earth permanent magnet materials in 2020, Jinli Permanent Magnet ranked third with a market share of about 11.7%. Among all rare earth permanent magnet material producers in China, based on the sales revenue of high-performance rare earth permanent magnet materials in 2020, Jinli Permanent Magnet ranked second with a market share of about 16.9%.

Frost & Sullivan has extensive research experience in the chemical and materials industries, assisting well-known enterprises in successfully accessing the capital market. Successful listings include: Avia Avian (IDX: AVIA), Global New Materials (6616.HK), Dafeng Equipment (2153.HK), Yihai International (8659.HK), GHW (9933.HK), Sanhe Fine Chemicals (0301.HK), Xingyu Holdings (2346.HK), Xinghe Holdings (1891.HK), Xuyang Group (1907.HK), Long Resources (1712.HK), Shandong Gold (1787.HK), Henan Jinma (6885.HK), Xingye New Materials (8073.HK), Dongguang Chemicals (1702.HK), Zhongqi Group (1932.HK), Xinbang Holdings (1571.HK), Meigu Technology (8349.HK), Huajin International (2738.HK), Flot Glass (6865.HK), Dynos (01452.HK), Caike Chemicals (1986.HK), Chang'an Renheng (8139.HK), Sansida (01337.TWSE), Born NYSE, CPC NYSE, Gu NYSE, Tianhe Chemicals (01619.HK), Yihua Holdings (02121.HK), Sijia Group (01863.HK), etc.

Recommended Reading

01. Frost & Sullivan assisted Avia Avian in successfully going public in Indonesia (IDX: AVIA)

05. Frost & Sullivan assists GHW in successfully listing on the Hong Kong Stock Exchange (9933.HK)

20. Frost & Sullivan assists Dinos in successfully listing on the Hong Kong Stock Exchange (1452.HK)