From July 16th to July 18th, the third session of the Boao Forum for Global Health was held at the National Convention Center in Beijing, China. This forum is an event within the framework of the Boao Forum for Global Health, co-hosted by the Boao Forum for Global Health and the People's Government of Beijing Municipality, organized by the Management Committee of Beijing Economic-Technological Development Area, and received strong support from the Chinese government of the host country, Chinese embassies in China, international organizations, multinational corporations, research institutions, and the media.

As a strategic partner of the forum, Frost & Sullivan, in conjunction with the LeadLeo Research Institute and the Organizing Committee of the Boao Forum on Global Health, officially released the '2024 China Healthcare Industry Development White Paper'. The paper provides a detailed analysis of the operating environment of China's healthcare industry both domestically and overseas. It starts from four sub-sectors: biopharmaceuticals, cell and gene therapy, AI healthcare, and traditional Chinese medicine. Through the development map sorting and cutting-edge trend identification, it makes forward-looking judgments on the growth paths of hot tracks.

1

Local Environment: Under the New Situation of High-Quality Development, Multidimensional Innovations in China's Healthcare Industry

With the continuous breakthroughs in China's economic and technological development, the continuous enhancement of comprehensive national strength, and the increasing international influence, the medical industry has made significant progress in areas such as technology research and development, clinical application, and market expansion.

Entering 2024, residents' demand for chronic disease management and early screening for diseases specific to the elderly population has increased, leading to growth in China's healthcare expenditure. In recent years, the proportion of total health expenditure in GDP in China has steadily risen. During this period, government and personal health expenditures increased from 1.2 trillion yuan to 2.4 trillion yuan and 2.3 trillion yuan respectively, while social health expenditures rose from 1.7 trillion yuan to 3.8 trillion yuan during the same period. In addition, the injection of social forces such as enterprises and charitable organizations has provided long-term sustainable internal impetus for the diversified and specialized development of medical services in China.

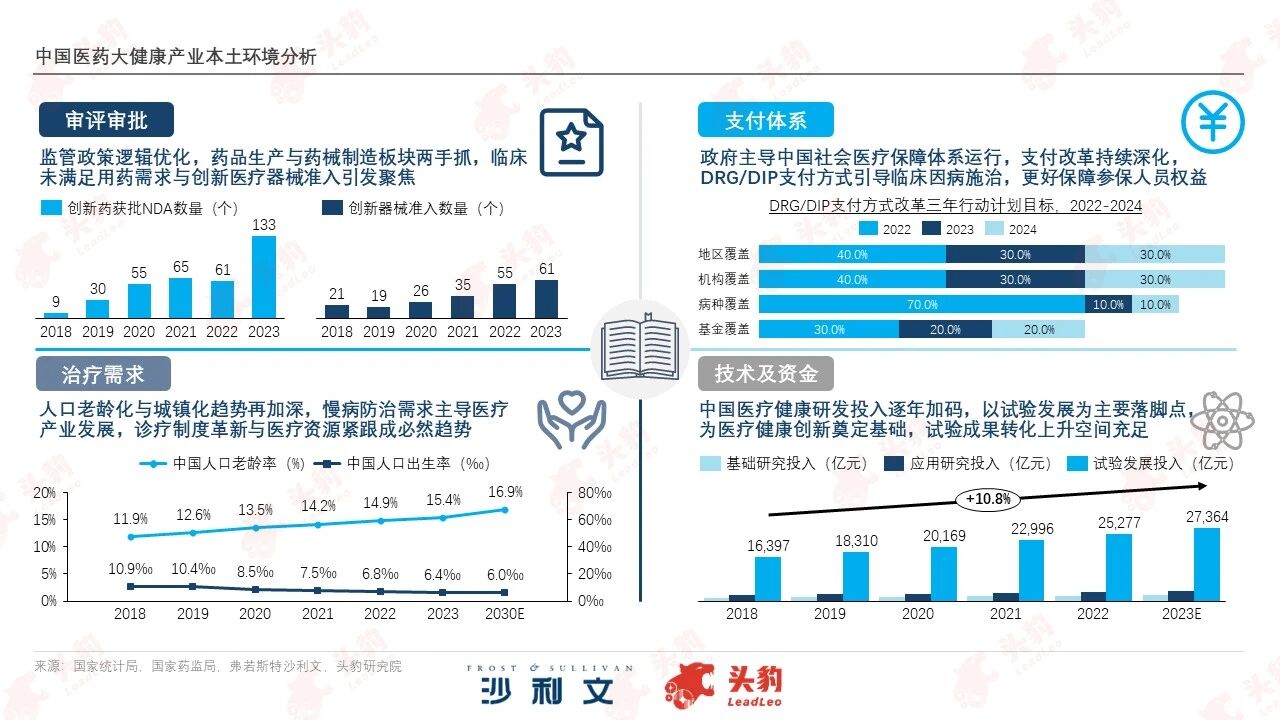

In terms of review and approval, China's drug approval process has been gradually optimized, with the number of registration reviews continuously increasing. Drugs with high clinical value and urgency are expected to pass the review more quickly.In line with the pharmaceutical policy framework, 'replacing inefficient with efficient' and 'encouraging innovation' have become the main themes of medical devices. The pre-purchasing lifecycle of products has been shortened compared to before the healthcare reform. Continuously exploring unmet clinical needs, accelerating product innovation and iteration, and seizing the window period for new products are crucial for the survival and development of enterprises.

In terms of the payment system, the medical insurance system has been continuously optimized. The role of the medical security department has gradually shifted from a post-payment provider to a strategic purchaser. The social medical security system has gradually evolved from 'wide coverage' to 'full coverage'.The operation of the medical insurance fund has remained stable overall, providing a stable guarantee for the operations of medical institutions and promoting the steady development of China's medical industry. The DRG/DIP system is one of the key contents of the reform of the medical insurance system. This payment method has achieved three major transformations: from a post-payment system to a pre-payment system, from the verification of individual institution medical insurance base amounts to regional total budget management, and from single payment to composite payment methods. The reform of the payment method has reduced the burden on patients for seeing a doctor and promoted the rational allocation of medical resources, facilitated medical technology innovation, and strengthened medical supervision.

In terms of treatment needs, compared with the time when the aging rate expanded in major global countries, the aging rate in Asian countries has increased significantly more rapidly.From the perspective of China's population structure, the number of births and birth rates continue to decline, and the population growth rate has slowed down. By 2023, the population aged 65 and above in China had reached 2.168 billion. Due to the impact of population aging, urbanization, and extended survival periods of chronic disease patients on the incidence of chronic diseases, the base number of chronic disease patients in China will continue to expand, characterized by younger patients and a high prevalence among the elderly. The government has introduced national-level special plans to strengthen chronic disease management and lead the improvement of chronic disease prevention and control levels across regions.

In terms of technology and capital, China's healthcare financing rounds are mainly concentrated in Series A, with investors increasingly focusing on the certainty of the companies. The number of early financings has gradually decreased, and financing rounds have moved back later.In the pharmaceutical sector, innovative drugs for respiratory diseases, radioactive drugs, and RNA drugs have become hotspots. Projects in cell and gene therapy, ADC-related fields are also favored by capital. In addition, R&D outsourcing service platforms play an important role in pharmaceutical innovation. In the medical device sector, with the rapid development of information technologies such as artificial intelligence, big data, and mobile internet, precision, intelligence, and personalization have become the main themes of development in the medical device track. Financing mainly focuses on high-end consumables and cardiovascular disease devices, achieving a breakthrough in domestic production of multiple categories of medical devices.

2

Overseas Environment: International influence has significantly increased, and Chinese pharmaceutical and medical device manufacturing is venturing into overseas markets

Through continuous technological innovation and international cooperation, medical enterprises have not only met the basic needs of the Chinese market that are constantly iterating and updating, but also actively expanded overseas markets on this basis, steadily increasing the international recognition of domestic brands. Relying on the solid development of local medical technology and innovation capabilities, China's healthcare industry has shown remarkable performance on the world stage in recent years. The adjustment of national medical insurance policies and the intensification of market competition have prompted some Chinese medical enterprises to seek breakthroughs in overseas development. China's healthcare industry is actively improving in terms of comprehensive drug innovation capabilities, R&D technology accumulation in pharmaceuticals and medical devices, and market expansion in multiple fields, narrowing the gap with advanced overseas markets.

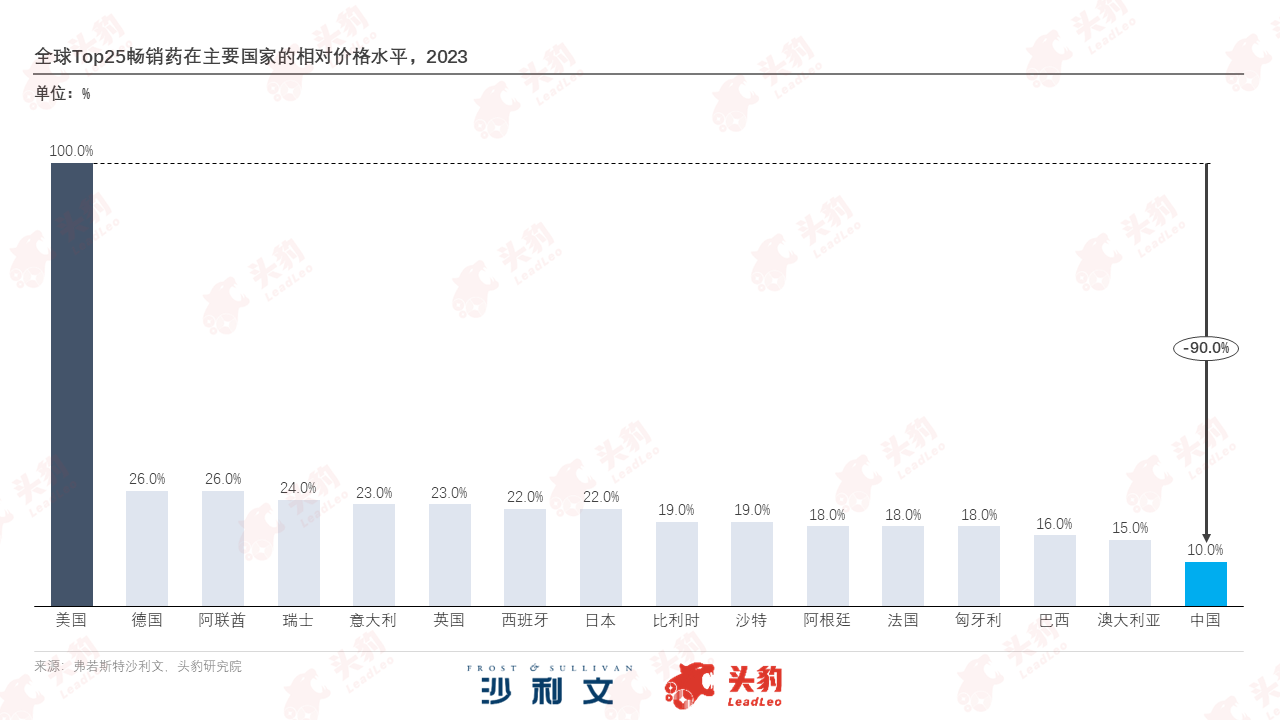

In terms of pharmaceuticals, in advanced markets represented by Europe and America, facing high R&D costs and continuously rising market access barriers, the prices of best-selling drugs remain high.In the Chinese market, based on the pricing logic of medical insurance negotiations and favorable policies for the large-scale use of generic drugs, there has been a market-driven competition for low prices, leading to continuous price cuts. Price differences provide potential incremental exports for Chinese pharmaceutical companies on their internationalization path. With the continuous optimization of China's drug structure under the 'combination of imitation and innovation' model, domestic innovative drugs, which are highly concentrated in research and development and patent technology, are expected to gain more market share globally.

In terms of medical devices, the volume-based procurement policy dominated by the 'national procurement + provincial alliances' model has been widely implemented. By centralizing procurement and trading volume for discounts, the procurement cost of medical devices has been reduced, alleviating the burden on patients and the pressure on healthcare insurance expenditures.Significant price cuts have squeezed the profit margins of local medical device companies, making market competition more intense. Therefore, it has become a necessary strategic choice for local enterprises to go global. By expanding their overseas presence, companies can gain more development space and achieve a dual increase in profit amount and brand influence.

3

Biopharmaceuticals: Domestic innovation accelerates, with unmet clinical needs driving market expansion

Since the 21st century, countries around the world have focused on biotechnology research to empower the development of the health industry and ensure the smooth operation of the pharmaceutical supply chain. With government funding support and high-end talent cultivation as the main driving forces, they have regarded the biopharmaceutical industry as an important part of national strategic layout.

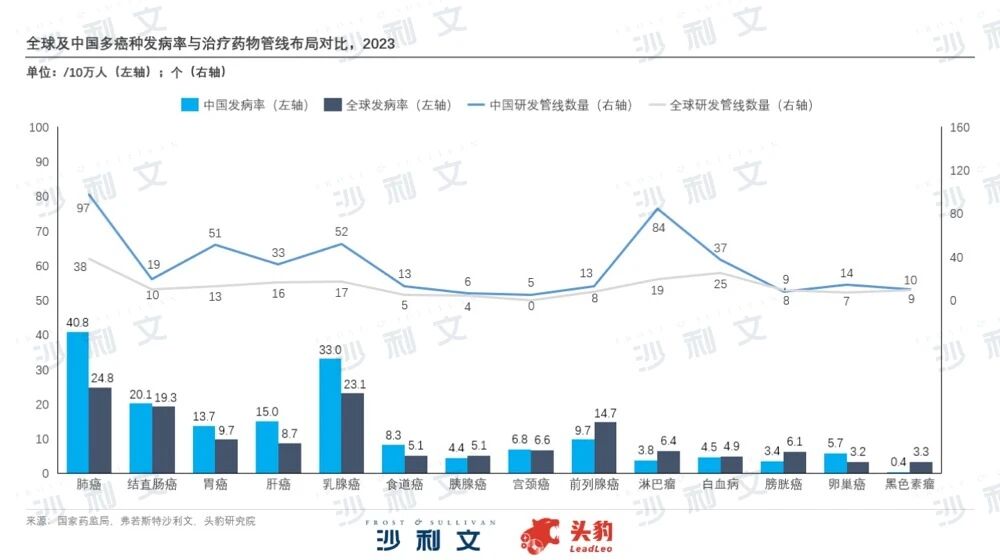

From the perspective of approval status, the clinical trial projects and new drug launches approved by the National Medical Products Administration mainly involve oncology drugs, with the proportion of oncology drugs in the IND and NDA stages exceeding 60% and 30% respectively. In terms of oncology drug research and development and indication coverage, lung cancer, colorectal cancer, and breast cancer are high-incidence cancers with high medication demand. However, there is homogenization in the pathogenic sites and research directions of anti-cancer drugs currently on the market, resulting in a supply that does not fully meet local medication needs and leaving some cancer patients without treatment options. Chinese biopharmaceutical companies urgently need to leverage their technical advantages and fully apply past product research and development innovation experience to treatment areas not covered by their existing drug pipelines. Based on improving access to medications for patients with serious and rare diseases, they should drive an enhancement of the market position of drug brands.

The prospects for overseas development have become another hot topic that has attracted widespread attention among biopharmaceutical companies. After China joined the International Council for Harmonisation (ICH) in 2017, domestic drugs have received endorsement in terms of quality, safety, and effectiveness. Subsequently, China's priority review and approval policies, as well as global new drug licensing policies, have gradually heated up the trend of innovative drugs going global. Domestic pharmaceutical companies have strengthened their comprehensive R&D and innovation capabilities, making innovative drugs the main focus and driving force for most companies going global.

4

Cell and Gene Therapy: With accumulated technical expertise, investors prefer products with broad applicability

Based on the accumulation of research personnel in basic research and drug discovery, the industry has gradually formed and led a new wave of the pharmaceutical industry focusing on 'multispecific drugs + cell and gene therapy'. As the clinical prospects of cellular and gene therapies (CGT) become increasingly prominent, the CGT track is about to enter a new chapter of vigorous development.

The investment and financing in CGT treatment in China are concentrated in the logic of universal application and market pursuit of hotspots. Among them, the field of immunocyte ex vivo gene therapy, mainly for tumor treatment, is the hottest, accounting for about 50% of investment and financing amounts, with CAR-T therapy accounting for nearly 90%. Currently, autologous cell ex vivo treatment in China is the main investment direction in the field of immunocyte therapy, and there is still room for the application space of immunocyte therapy to be unleashed.

Cell and gene therapy, as a new generation of breakthrough precision treatment methods, hold great promise in the biomedical field, especially in the treatment of cancer, genetic diseases, and rare diseases. The demand for accessibility drives the large-scale production of CGT drugs to become a future trend. 'Generic drugs' have an even better prospect than 'customized drugs.' At the same time, the high incidence of cancer among Chinese residents has led to the focus on CGT drug research and development and production mainly in the field of solid tumor treatment.

With the gradual maturation of CGT treatment technology, cell-level treatment regimens have entered a period of rapid development. In recent years, global research and development efforts have focused on solid tumor therapies and allogeneic therapies. Induced pluripotent stem cells (iPSCs) have a similar differentiation potential to embryonic stem cells and can be induced from adult human cells. They possess both general-purpose and personalized therapeutic product capabilities. Developing allogeneic 'ready-made' therapies using iPSC technology may provide new opportunities for CGT developers.

5

AI Healthcare: A global transformation sweeping through, with multiple medical application areas accelerating penetration

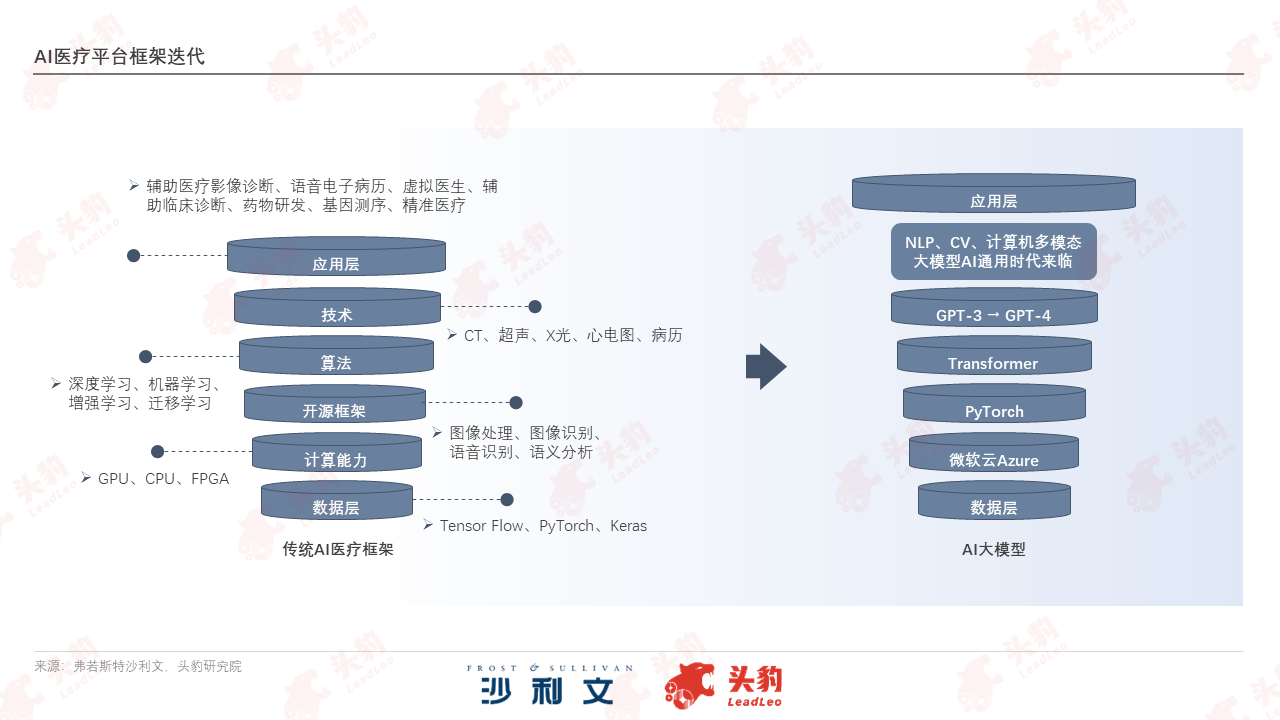

AI technology empowers the healthcare industry, accelerating its development towards intelligence, digitization, and informatization. The generalization of multimodal AI has become a future trend in the AI healthcare industry.

The rise of cloud computing has greatly promoted the iteration of medical AI models. By providing large-scale data processing capabilities, elastic computing resources, and high-performance computing clusters, AI large models equipped with cloud computing excel in computational efficiency and accuracy when facing complex tasks. In cutting-edge medical fields such as emergency medical services, real-time monitoring by medical staff, and personalized clinical diagnosis and treatment, basic data is complex and requires higher processor response times. The evolution of AI large models has thus helped to further improve the quality of medical services.

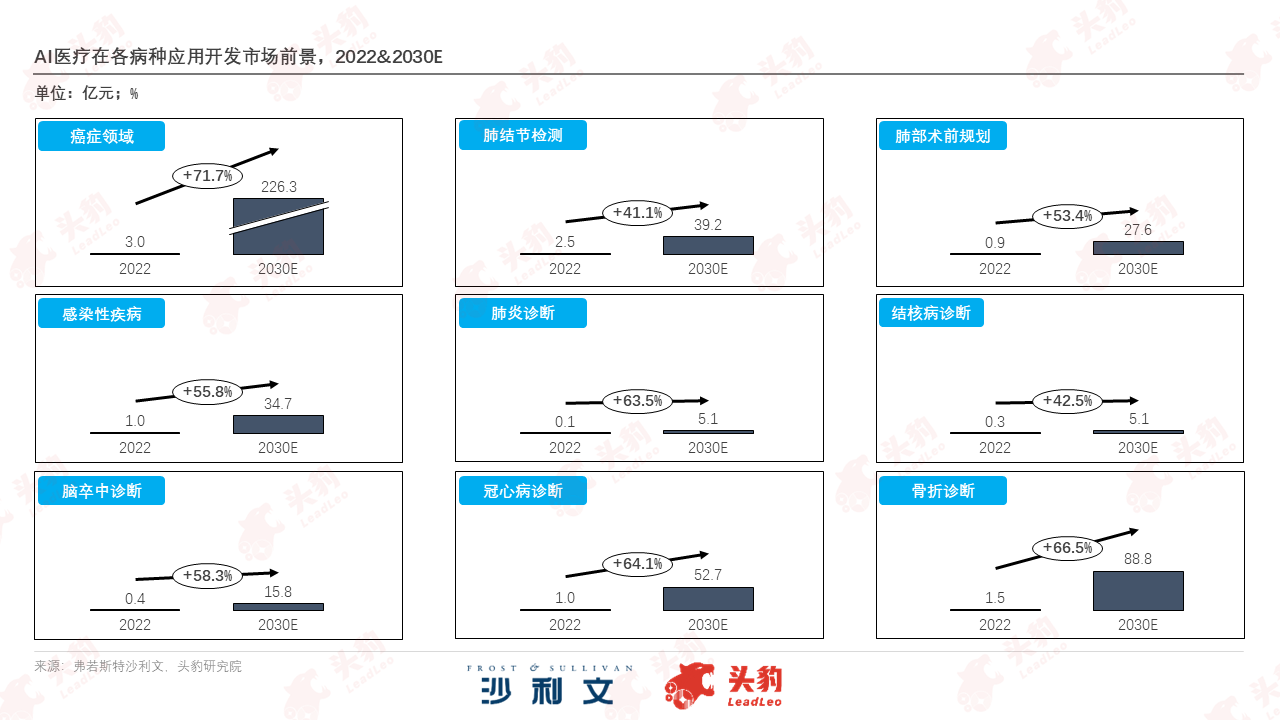

Looking at the segmented diagnostic field, given the high cancer risk among Chinese residents, early cancer screening and clinical treatment and scenarios have become the main flow of medical resources. The market scale for AI medical services in this field is expected to accelerate from 300 million yuan in 2022 to 22.63 billion yuan in 2030, with an annual compound growth rate of 71.7% during this period. The potential of AI diagnosis and treatment in orthopedics and cardiovascular disease treatment is also evident. The market for fracture and coronary heart disease diagnosis services equipped with AI large models is expected to achieve annual compound growth rates of 66.5% and 64.1% respectively during this period.

The fields of medical devices, medical imaging, and pharmaceuticals have also benefited from the computing power upgrade of AI large models. As of October 2023, 119 AI medical devices in China have obtained market access, and various intelligent surgical robot planning and navigation applications have been successively approved. The main application scenarios of AI medical devices have shifted from "auxiliary diagnosis" to "parallel auxiliary diagnosis and treatment." In terms of medical imaging technology, the penetration rate of artificial intelligence technology in CT, MRI, and ultrasound scans is continuously strengthening, with an expected increase to 41.3% by 2030, and imaging examinations are expected to achieve large-scale coverage of multiple diseases by then. In comparison, AI in pharmaceuticals is still in the initial stage of preparation, with nearly a hundred AI-enabled drug pipelines advancing to clinical trials, and the future prospects for AI-driven independent research and development of new drugs are promising.

6

Traditional Chinese Medicine: Promote the integration of treatment and health preservation, with investors preferring broad-based market application areas

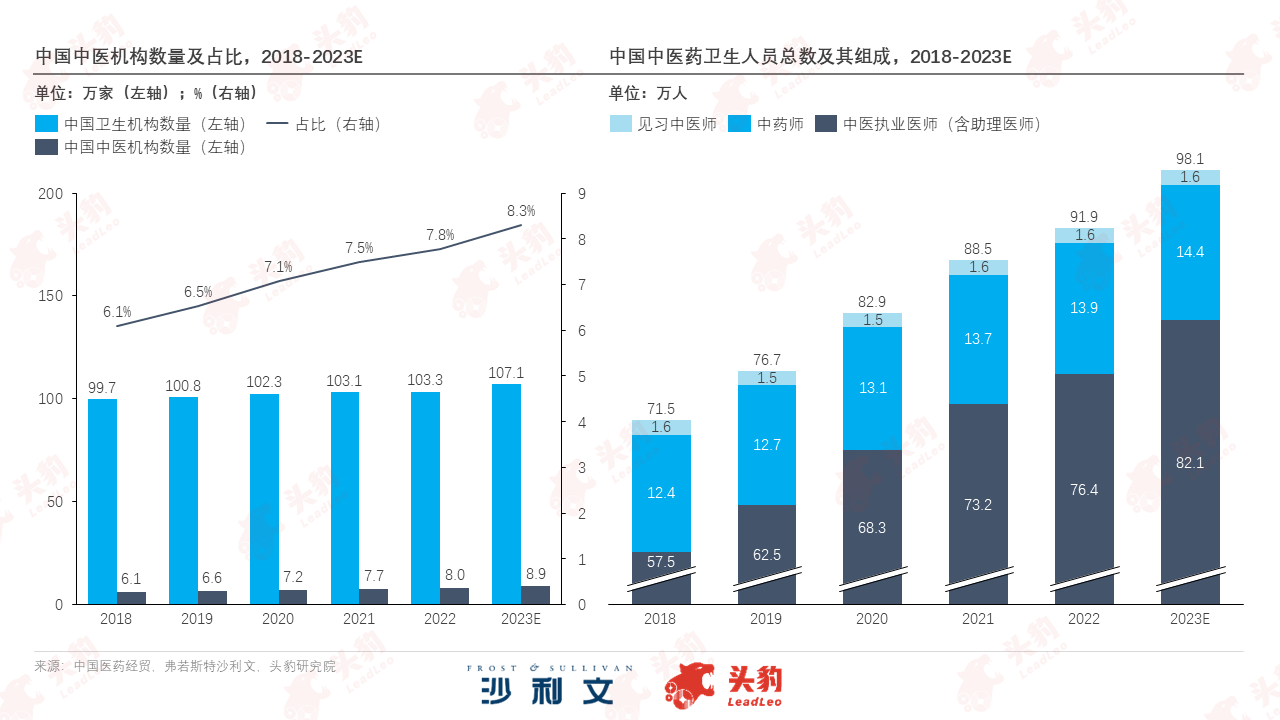

In recent years, government departments such as the National Health Commission and the General Office of the State Council have promulgated multiple policies proposing the concept of 'integrating traditional Chinese and Western medicine for preventive treatment'. Driven by these policies, the number of traditional Chinese medicine (TCM) diagnosis and treatment institutions across the country has shown a steady upward trend in recent years. In 2022, TCM diagnosis and treatment institutions accounted for 7.8% of the total number of health institutions nationwide, an increase of 1.7 percentage points compared to 2018. Based on this trend, it is estimated that the number of TCM diagnosis and treatment institutions in China will further increase to 89,000 in 2023.

To keep up with the expansion of medical institutions and effectively expand the coverage of traditional Chinese medicine (TCM) diagnosis and treatment resources, the National Administration of Traditional Chinese Medicine issued the "14th Five-Year Plan for the Development of TCM Talents" in 2022. The policy emphasizes the selection and cultivation of key TCM talents to form a tiered talent team. With the implementation of the government's talent project, the number of practicing TCM doctors in China, as the backbone force providing TCM diagnosis and treatment services, reached 764,000 by 2022, a 32.9% increase compared to 2018, and they dominate the growth rate of various health personnel engaged in TCM diagnosis and treatment.

In the wave of global digital transformation, the infrastructure for traditional Chinese medicine (TCM) informatization is rapidly upgrading. The construction of national and provincial TCM data centers has received attention, and the development and application of emerging information technologies such as big data, artificial intelligence, and the Internet of Things are gradually deepening. Medical institutions are building and improving information platform functions by integrating internal information systems. On the premise of ensuring network and data security, the digital transformation of the TCM industry lays the foundation for future intelligent and intensive management.

With the in-depth optimization of national and provincial data center operations and maintenance, iterative information technology will be more widely applied in the field of traditional Chinese medicine. Through artificial intelligence and big data analysis, the value of traditional Chinese medicine data will be further explored and utilized to assist in the development of precision medicine and personalized health management. At the same time, participation in international standardization activities will accelerate the narrowing of the gap between traditional Chinese medicine information standards and global levels, helping traditional Chinese medicine quickly enter the world.