Yingtong Holdings Limited (Stock Code: 6883.HK) successfully listed on the main board of the Hong Kong capital market on June 26, 2025. The company is a leading enterprise in the perfume industry in China (including Hong Kong and Macau), managing a diversified portfolio of perfume products for several well-known global brands. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provided exclusive industry advisory services for Yingtong Holdings Limited's listing, and we hereby extend a warm congratulations on its successful listing.

Yingtong Holdings Limited (hereinafter referred to as 'Yingtong') successfully listed on June 26, 2025. The company plans to issue 333.4 million H shares, of which 90% will be international offerings and 10% will be public offerings. The maximum issue price per share is HK$3.38, raising approximately HK$1.127 billion in net proceeds.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support and highlight the issuer's competitive advantages, assisting the issuer, investment banks and other intermediaries in completing the writing of relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing various feedbacks from the Hong Kong Stock Exchange regarding industry issues.

According to LiveReport's big data (statistical data as of June 1, 2025), from January to May 2025, and during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 17 (63%), 48 (63%) and 152 (68%) Hong Kong-listed IPOs respectively, boasting rich industry experience and communication skills with exchanges and investors.

PART/1

Investment Highlights

-

The company maintains a leading position in perfumes in China (including Hong Kong and Macau);

-

The company has always been keen on the discerning and resilient sniffing economy of China's mainland structural growth, in order to seize strategic market opportunities;

-

The company has cultivated outstanding product distribution and market deployment capabilities, setting a significant market entry barrier for competitors;

-

The company is a long-term business partner of a globally leading brand;

-

The company has a vast multi-level customer base, including an omnichannel sales and distribution network, continuously covering a wider range of consumer groups;

-

The company is led by a visionary management team, advocating a people-oriented corporate culture.

According to the Frost & Sullivan report, in terms of retail sales for 2023, the company:

-

The company is the fourth largest perfume group in Mainland China;

-

The company ranks first in terms of retail sales of fragrance products among non-brand owner fragrance groups;

-

The company is the third largest perfume group in China (including Hong Kong and Macau).

PART/2

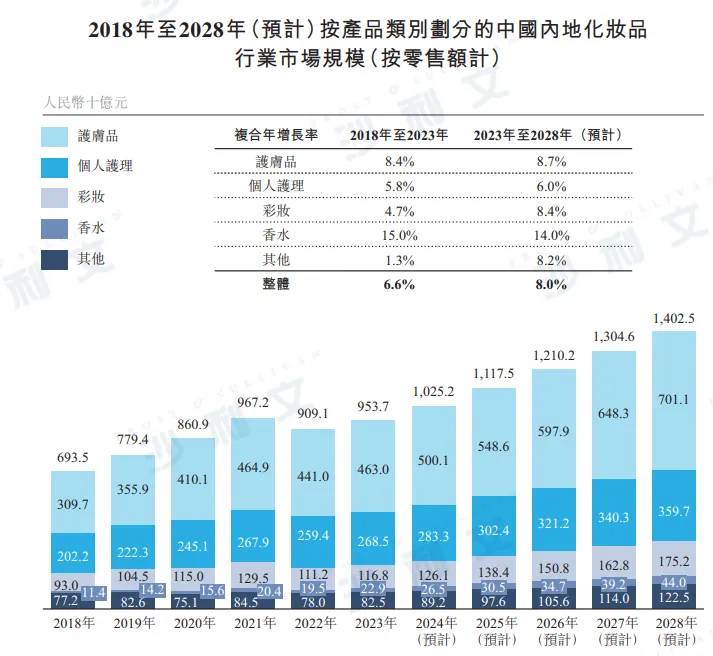

Overview of the Cosmetics Industry in Mainland China

The Chinese mainland has the world's second-largest cosmetics market, accounting for 11.9% of the global international market share in terms of retail sales in 2023. According to Frost & Sullivan's data, due to increased consumer spending, the cosmetics industry in the Chinese mainland experienced growth from 2017 to 2021, which was partially offset by the impact of the COVID-19 pandemic on the industry in 2022. The market scale of the cosmetics industry in the Chinese mainland (in terms of retail sales) increased from RMB 693.5 billion in 2018 to RMB 953.7 billion in 2023, with a compound annual growth rate of 6.6%.

According to Frost & Sullivan's data, cosmetics can be divided into five categories: skin care, personal care, makeup, fragrance, and others. Others mainly include baby and maternity care, deodorants, and hair removal products.

Source: National Bureau of Statistics of China, Frost & Sullivan report

PART/3

Overview of the Global Perfume Industry

Perfume refers to aromatic liquids, usually made from essential oils extracted from fresh flowers and spices, used to provide pleasant scents for hair, body, or clothing. The main components of perfume are alcohol, fragrance, and a small amount of water. Depending on the volatility of the essential oils, the aroma of perfume is generally divided into three stages: base note, middle note, and top note.

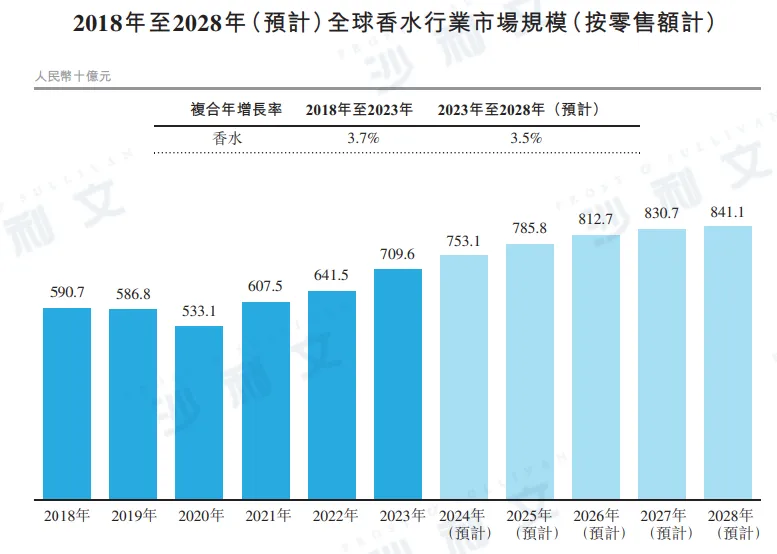

The United States, Brazil, France, Germany, and the United Kingdom are the top five countries in terms of perfume market size in 2023. The global perfume market size (in terms of retail sales) increased from RMB 590.7 billion in 2018 to RMB 709.6 billion in 2023, with a compound annual growth rate of 3.7%. It is expected to grow to RMB 841.1 billion in 2028, with a compound annual growth rate of 3.5%.

Source: Frost & Sullivan report

PART/4

Overview of the Perfume Industry in China (Including Hong Kong and Macau)

According to Frost & Sullivan's data, the perfume industry in China (including Hong Kong and Macau) has gone through the following stages: (i) The budding stage before 1978, when perfume consumption was not yet widespread and there were very limited international perfume brands entering the market; (ii) The development stage from 1978 to 2000, during which China (including Hong Kong and Macau) was in the early stages of market reform, with slow development of the perfume market. International perfume brands began to enter China (including Hong Kong and Macau), but the variety of products was limited; (iii) The accelerated development stage from 2000 to 2015, when major international perfume groups entered China (including Hong Kong and Macau) rapidly, and the number of local perfume production enterprises began to rise. During this stage, international brands dominated the high-end market, while local brands in China (including Hong Kong and Macau) focused on the mass market. In addition, local perfume companies began to rely on online channels for product sales; (iv) The high-quality development stage from 2015 to the present, when the perfume market in China (including Hong Kong and Macau) has become relatively mature, industry norms have gradually improved, and consumer awareness of perfumes in China (including Hong Kong and Macau) has rapidly increased. During this stage, international brand perfumes still occupy a significant market share and are the main driving force for the growth of the perfume market in China (including Hong Kong and Macau). In addition, the growth in sales on e-commerce platforms has accelerated the development of the perfume market in China (including Hong Kong and Macau).

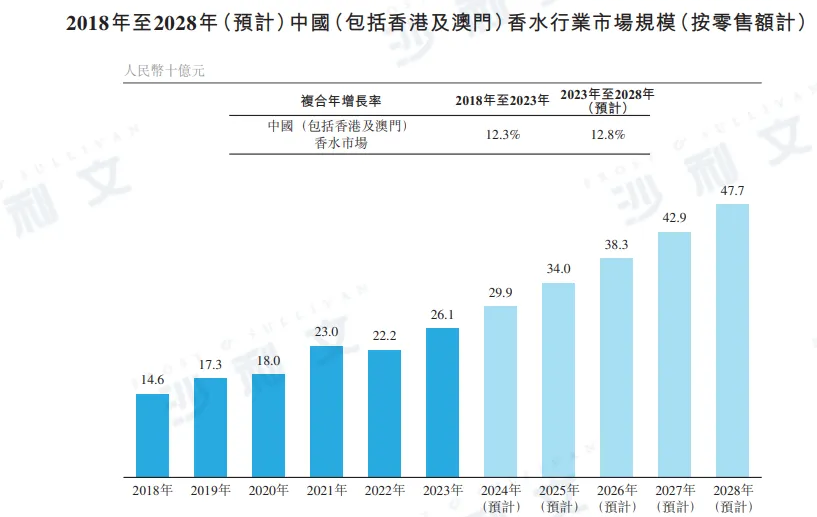

The total market scale of perfumes in China (including Hong Kong and Macau) (in terms of retail sales) increased from RMB 146 billion in 2018 to RMB 261 billion in 2023, with a compound annual growth rate of about 12.3%. It is expected to further grow to RMB 477 billion by 2028, with a compound annual growth rate of about 12.8% from 2023 to 2028.

Source: National Bureau of Statistics of China, Hong Kong Government Statistical Service, Macao Census and Survey Department, Frost & Sullivan report

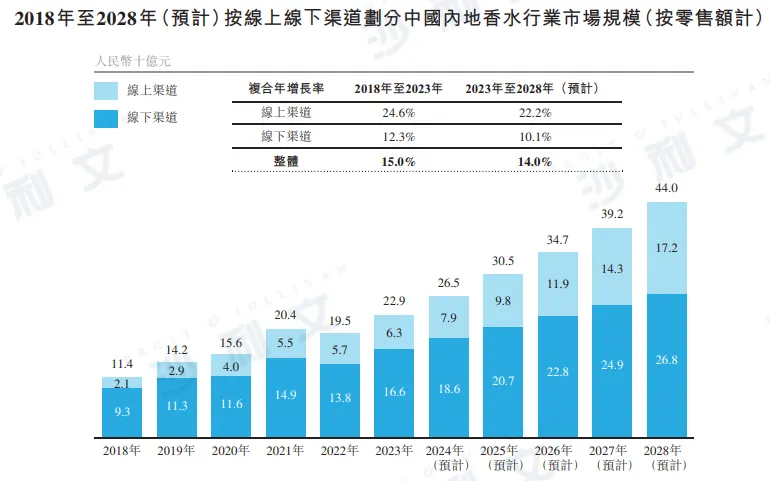

The market scale of perfumes in Mainland China (by retail sales) increased from RMB 114 billion in 2018 to RMB 229 billion in 2023, with a compound annual growth rate of about 15.0%. It is expected that by 2028, the market will grow to RMB 440 billion, with a compound annual growth rate of about 14.0%.

Source: National Bureau of Statistics of China, Frost & Sullivan report

The perfume raw materials sold in Mainland China mainly include ethanol and glycerin. According to Frost & Sullivan's data, the price of ethanol increased from RMB 5,482 per ton in 2018 to RMB 6,690 per ton in 2023, with a compound annual growth rate of about 4.1%. Meanwhile, the price of glycerin decreased from RMB 6,869 in 2018 to RMB 4,338 in 2023, with a compound annual growth rate of about -8.8%.

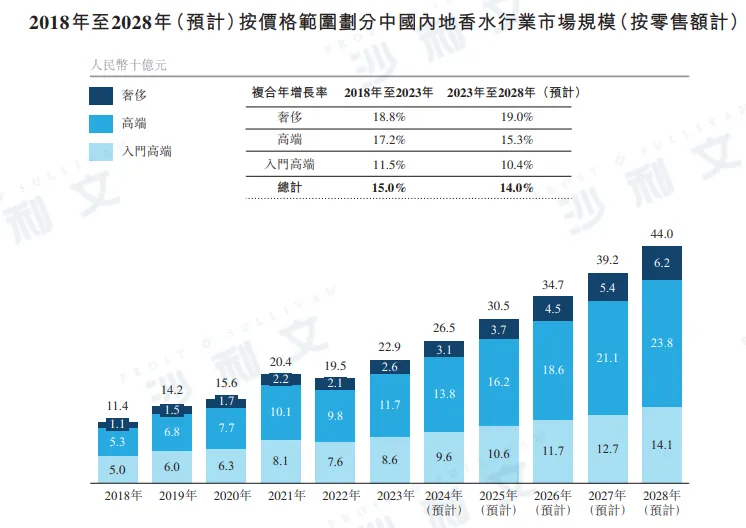

According to Frost & Sullivan's data, the perfume market in Mainland China can be divided into three categories based on price range: (i) entry-level high-end perfumes, typically priced at RMB 599 or less per 50 milliliters; (ii) mid-range high-end perfumes, usually priced between RMB 600 and RMB 1,199 per 50 milliliters; (iii) luxury perfumes, typically priced at RMB 1,200 or more per 50 milliliters.

Source: National Bureau of Statistics of China, Frost & Sullivan report

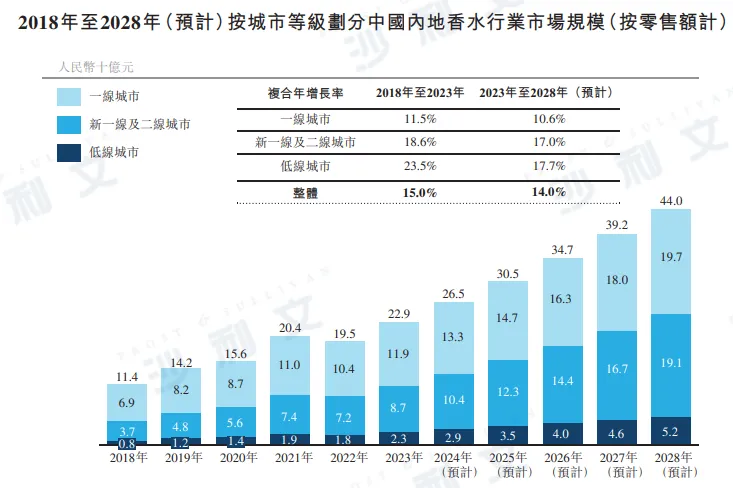

According to Frost & Sullivan's data, cities in mainland China can generally be divided into first-tier cities, new first-tier cities, second-tier cities, and low-tier cities.

Source: National Bureau of Statistics of China, Frost & Sullivan report

PART/5

Business Model of the Fragrance Industry

The perfume industry encompasses: (i) upstream, including raw material supply and product manufacturing; (ii) midstream, including brand market deployment and other business activities, which can be carried out by the brand owner perfume group or non-brand owner perfume groups. Non-brand owner perfume groups include first-tier distributors directly authorized by the brand owner, or second-tier distributors authorized by first-tier distributors; (iii) downstream, including distributing products to end consumers through various sales channels.

Source: Frost & Sullivan report

Market deployment and other business activities are at the midstream level within the perfume industry, encompassing two main business models: (i) Brand owners' perfume groups operating independently, where the brand owners handle all aspects of the business, including product development, marketing, and the establishment and supervision of sales channels. The brand owners' perfume groups have full control over the entire value chain to shape and maintain the brand image; (ii) Non-brand owners' perfume groups operating under direct authorization from the brand owners or second-level authorization from first-level authorized dealers to handle the brand's business in designated regions. Brand owners' perfume groups may choose to operate the brand themselves or grant licenses for brand operations to non-brand owners' perfume groups for reasons including: (i) They only have expertise in perfume development and must leverage external expertise to manage product promotion and sales; (ii) They lack in-depth knowledge of local consumer markets or have limited sales networks in those markets; (iii) Some of them are large conglomerates with perfume business being a relatively small part of their overall operations, leading them to prefer hiring third-party professional non-brand owners' perfume groups to handle brand product marketing and sales, allowing them to focus more on other areas of their business.

The market deployment and other business activities carried out by the non-branded owner fragrance group provide various benefits to the branded owner fragrance group, including but not limited to: (i) reducing their financial pressure and operational burden by leveraging the resources of the non-branded owner fragrance group and the mature sales and distribution networks of local partners to quickly enter local markets; (ii) leveraging the local expertise of the non-branded owner fragrance group in marketing strategies, brand positioning, product management, sales strategies, and distribution management to facilitate sales by understanding the specific preferences and behaviors of target consumers in relevant regions; (iii) sharing operational risks with the non-branded owner fragrance group.

PART/6

The competitive landscape of the perfume industry in Mainland China

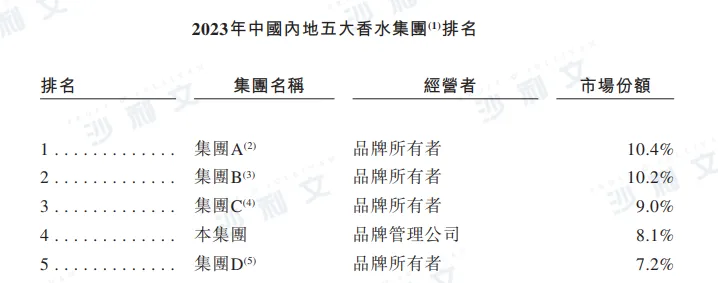

In terms of retail sales in 2023, the company is the fourth-largest perfume group in Mainland China, with a market share of about 8.1%. In 2023, the company ranked first among non-branded owner perfume groups in terms of retail sales of perfume products.

Source: Frost & Sullivan report

PART/7

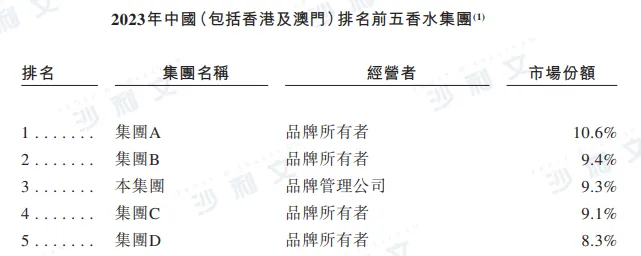

Competitive landscape of the perfume industry in China (including Hong Kong and Macau)

In terms of retail sales in 2023, the company is the third-largest perfume group in China (including Hong Kong and Macau), with a market share of about 9.3%.

Source: Frost & Sullivan report

PART/8

The main growth drivers of the perfume market in Mainland China

● Economic growth and e-commerce development synergistically promote the penetration of perfumes into lower-tier cities

With the development of low-tier city economies and rapid urbanization, the financial situation of the emerging middle class in these cities has improved, and their personal image and taste awareness have been cultivated. Perfumes have become an integral part of the daily life of the middle class in low-tier cities on the Chinese mainland. In addition, online channels provide perfume brands with a broad and convenient platform for precise targeting of consumer groups, targeted marketing, and personalized recommendations, enhancing consumers' desire to buy and fostering strong brand loyalty. Therefore, the development of e-commerce has enabled perfume brands to further penetrate the Chinese mainland market, especially in low-tier cities, where online channels can still achieve effective coverage without physical stores.

● Increased perfume usage leads to an increase in purchase frequency

As Chinese consumers' awareness of perfume products continues to improve, more and more consumers are starting to use the same perfume multiple times a day or different types of perfume at different occasions. The increased use of perfume has led to an increase in purchasing frequency, stimulating the growth momentum of the perfume industry in mainland China.

● The diversification of consumption scenarios has stimulated more consumer demand

In recent years, as the social and collectible value of perfumes has increasingly received attention, Chinese consumers have gradually increased their frequency of purchasing perfumes. They use them not only for personal daily use but also for collection and gift-giving purposes. The continuous diversification of perfume consumption scenarios will continue to stimulate growth in consumer demand, thereby further promoting the expansion of the market scale of the perfume industry in the Chinese mainland.

● Favorable government policies

Positive government policies have driven the growth of tax-free shopping channels in Mainland China, with perfumes being a major category benefiting from this trend. In June 2020, the Ministry of Finance, the State Taxation Administration, and the General Administration of Customs jointly issued the "Hainan Island Tourist Duty-Free Shopping Policy," which stipulates the duty-free shopping policy for island tourists in Hainan Province. This policy has increased the annual duty-free shopping limit per person to RMB 100,000, expanded the variety of duty-free goods, abolished the RMB 8,000 limit on individual items, and raised the maximum number of cosmetics that passengers can purchase per journey to 30 pieces. Such favorable adjustments have enhanced the attractiveness of Hainan's duty-free shopping, increased consumption limits, and expanded product choices, which is conducive to promoting the growth of tax-free channels and benefiting related industries such as perfumes. In August 2024, the Ministry of Finance, the Ministry of Commerce, the Ministry of Culture and Tourism of China, the General Administration of Customs, and the State Taxation Administration jointly issued the "Interim Measures for the Management of City Duty-Free Stores." This new policy strengthens the supervision of city duty-free stores to promote orderly and sustainable growth. In addition, duty-free stores in 13 cities (including Beijing and Shanghai) on Mainland China will transform from foreign exchange duty-free stores to city duty-free stores, and eight new duty-free stores will be launched in other major cities (such as Guangzhou, Chengdu, and Shenzhen). This policy indicates a steady expansion of the duty-free industry, and we believe it will stimulate the growth of related industries such as perfumes that sell through tax-free channels.

PART/9

Main Development Trends of the Perfume Market in Mainland China

● Mainland China is becoming the global frontier for perfume

The Chinese mainland is one of the fastest-growing perfume markets in the world and is expected to continue this momentum in the future. Existing perfume brands have previously launched exclusive perfume products for Chinese consumers, and more brands are planning to explore exclusive product lines in the Chinese market. In addition, an increasing number of international brands are entering the Chinese market. According to Frost & Sullivan, more international brands aspire to enter the Chinese market in the near future.

● International perfume brands collaborating with local manufacturers

International perfume brands are widely recognized for their excellent quality, long-standing business history, and inspiring brand philosophy. However, there are several entry barriers in establishing and expanding operations in the Chinese mainland, including weak relationships with major retailers, limited distribution networks, and a lack of understanding of the Chinese market and consumer preferences. Cooperation between international perfume brands and local manufacturers forms a strong mutually beneficial partnership. Local manufacturers are one of the key factors in the success of international perfume brands.

● Integration of online and offline channels

Unlike other consumer industries, offline experience is crucial for the perfume industry, where consumers need to understand the characteristics of perfumes through smelling and experiencing them. Similarly, online platforms are the main channels for news push and shopping. Offline stores and online platforms will increasingly integrate, allowing consumers to learn detailed product information online and then physically experience products of interest offline. As pricing converges across online and offline channels, offering better experiences in offline stores remains the preferred choice for most end consumers purchasing perfumes.

● International brands continue to dominate the market

International brands continue to maintain their dominant position by virtue of outstanding quality, strong brand influence, and advanced market strategies. In addition, international brand enterprises possess rich R&D, technical, and product innovation capabilities to meet the diverse needs of consumers. These brands also skillfully employ various marketing strategies to enhance brand awareness and influence, effectively attracting consumers and further consolidating their market dominance. Chinese consumers are paying more and more attention to personal image and quality of life, leading to a continuous growth in demand for daily products such as perfumes, taking into account both quality and brand reputation.

Frost & Sullivan has extensive research experience in the consumer industry and has assisted many well-known companies in successfully listing on the capital market. Successful listings include Haitian Flavor Industry (3288.HK), Titanium (Nasdaq: PTNM), Niu Daren (Nasdaq: MB), Newman's (2530.HK), Grasshopper Group (2593.HK), Mao Ge Ping (1318.HK), Mengjin Yuan (2585.HK), Laopu Gold (6181.HK), Fugang China (2497.HK), Yan's House (1497.HK), Daily Cooking (NYSE:DDC), Youbao Online (2429.HK), Feifanlingyue (0933.HK), Shanghai Shangmei (2145.HK), Ju Zi Biotech (2367.HK), China COSCO (1880.HK), Midea Group (9896.HK), Jiulongwang Food (1927.HK), Vesync (2148.HK), Blue Moon (6993.HK), Popomart (9992.HK), Midea Group (NYSE:MNSO), Nongfu Spring (9633.HK), Fengxiang Food (9977.HK), China Feihai (6186.HK), Taobo Sports (6110.HK), China National Tobacco International (6055.HK), Youpin 360 (2360.HK), Wugu Mofang (1837.HK), Baby Tree (1761.HK), Deying Holdings (2250.HK), Bingshi International (1705.HK), Golden Cat and Silver Cat (1815.HK), Miming Life Department Store (8473.HK), Nissin Foods (1475.HK), Debao Group (8436.HK), Seiko China (NASDAQ:SECO), Barbie Bebe (8297.HK), Asia Grocery (8413.HK), Chowking Duck (1458.HK), COFCO Foods (1610.HK), Dali Foods (3799.HK), Vientiane International (0288.HK), Chow Tai Fook (1929.HK), Jumei Youpin (NYSE:JMEI), and others.

Recommended Reading

Frost & Sullivan assists Pitanium in successfully going public in the US (Nasdaq: PTNM)

Frost & Sullivan helped Mr. Niu successfully go public on the US stock market (Nasdaq: MB)

Frost & Sullivan helps Newman's S.A. successfully go public in Hong Kong (2530.HK)

Frost & Sullivan helps Maogoping successfully go public in Hong Kong (1318.HK)

Frost & Sullivan helps Mengjin Garden successfully go public in Hong Kong (2585.HK)

Frost & Sullivan helps the established brand Gold successfully go public in Hong Kong (6181.HK)

Frost & Sullivan assists Yanzhiwu in successfully listing on the Hong Kong Stock Exchange (1497.HK)

Frost & Sullivan helps Rizhao Dadi Cook successfully go public in the US (NYSE:DDC)

Frost & Sullivan assists Vesync in successfully listing on the Hong Kong Stock Exchange (2148.HK)

Frost & Sullivan assists Blue Moon in successfully listing on the Hong Kong Stock Exchange (6993.HK)

Frost & Sullivan helps Pop Mart successfully go public in Hong Kong (9992.HK)

Frost & Sullivan helps famous innovative products successfully go public in the US (NYSE:MNSO)

Frost & Sullivan helps China's Feihai succeed in listing on the Hong Kong Stock Exchange (6186.HK)

Frost & Sullivan helps Top Glove Sports S.A. successfully go public in Hong Kong (6110.HK)

Frost & Sullivan helps Youpin 360 successfully go public in Hong Kong (2360.HK)

Frost & Sullivan helps Baby Tree successfully go public in Hong Kong (1761.HK)

Frost & Sullivan helps Golden Cat and Silver Cat successfully go public in Hong Kong (1815.HK)

Frost & Sullivan helps Nippon Sake & Foods Co., Ltd. successfully go public in Hong Kong (1475.HK)

*The above order is not sequential and is arranged in reverse chronological order based on listing time.