Frost & Sullivan

Cao Cao Travel Co., Ltd. (Stock Code: 2643.HK) successfully listed on the Hong Kong Capital Market Main Board on June 25, 2025. The company is a leading enterprise in the national shared mobility industry, with the mission of "redefining green shared mobility through technology." It innovatively applies globally leading internet, connected vehicle technology, autonomous driving technology, and new energy technologies to the shared mobility sector. Its brand proposition is "serving the nation's travel with heart," and it is committed to creating the best-performing travel brand in terms of service reputation. Frost & Sullivan (hereinafter referred to as "Frost & Sullivan") provides exclusive industry advisory services for Cao Cao Travel Co., Ltd.'s listing, and we warmly congratulate them on their successful listing.

Cao Cao Travel Co., Ltd. (hereinafter referred to as 'Cao Cao Travel') successfully went public on June 25, 2025. The company plans to issue 4,417.86 million H shares, of which 90% will be international offerings and 10% will be public offerings. The maximum offering price per share is HK$41.94, raising a net amount of approximately HK$1.718 billion.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support and highlight the issuer's competitive advantages, assisting the issuer, investment banks and other intermediaries in completing the writing of relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and providing assistance to the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange.

According to LiveReport's big data (statistical data as of June 1, 2025), from January to May 2025, as well as during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 17 (63%), 48 (63%), and 152 (68%) Hong Kong-listed IPOs respectively, boasting rich industry experience and communication skills with exchanges and investors.

PART/1

Investment Highlights

-

The company is the second-largest online car-hailing platform in China;

-

Through strategic cooperation with Geely Group, the company holds unique control over vehicles;

-

The company has a unique user experience and strong brand recognition;

-

The company empowers drivers by reducing holding costs (TCO) and improving operational efficiency.

According to the Frost & Sullivan report, the company for 2024:

-

Ranked second in the online car-hailing industry in China, measured by GTV;

-

Possesses the largest custom car fleet in China.

PART/2

Overview of the Travel Industry Market in China

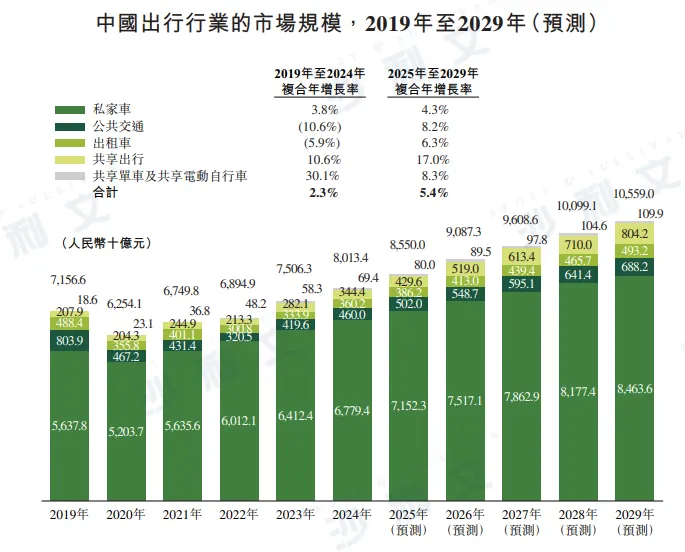

As the world's second-largest economy, China has the world's second-largest population, and it is home to numerous densely populated cities, creating the world's largest travel market today. In 2024, the scale of China's travel market reached RMB 8.0 trillion.

China's travel industry encompasses a variety of modes of transportation to meet individual travel needs. Public transportation (such as buses and rail transit) facilitates travel for multiple people; traditional taxis are suitable for independent one-way trips; shared mobility provides convenient services without the need for personal vehicles; private cars can meet individual transportation needs anytime and anywhere; in addition, there are travel options with different price ranges (such as two-wheeled vehicles) to meet diverse consumer needs.

The scale of China's travel market grew from RMB 6.9 trillion in 2018 to RMB 7.2 trillion in 2019. From 2020 to 2022, affected by the COVID-19 pandemic, consumer travel demand declined, causing a certain impact on market growth. Despite the adverse effects of the pandemic, the scale of the travel market only slightly fell from RMB 7.2 trillion in 2019 to RMB 6.9 trillion in 2022. As the economy gradually recovers from the pandemic, China's travel market rebounded strongly in 2023, growing by 8.9% compared to 2022, reaching RMB 7.5 trillion, and further increasing to RMB 8.0 trillion in 2024.

Looking ahead, driven by factors such as the continuous increase in travel demand in underserved cities, consumers' growing preference for pure electric vehicles, and the ongoing recovery of commercial activities, it is expected that China's travel market will grow from RMB 8.6 trillion in 2025 to RMB 10.6 trillion in 2029, with a compound annual growth rate of 5.4%. Among them, shared mobility is expected to become the fastest-growing mode of travel between 2025 and 2029.

Data source: Ministry of Transport of China, China Association of Automobile Manufacturers, Frost & Sullivan analysis

PART/3

Overview of the China Shared Mobility Industry Market

Shared mobility allows people to enjoy personalized travel services without owning their own vehicles, creating a hybrid mode between private car ownership and public transportation. For this reason, compared to owning a private car, shared mobility helps alleviate urban traffic congestion and reduce per-unit travel costs; whereas, compared to public transportation, shared mobility is more convenient and efficient, enhancing the overall travel experience. The main forms of shared mobility in China include online car-hailing services () and carpooling services ( ride). Online car-hailing services match users' travel needs with registered drivers and vehicles on an online platform in real time. Carpooling services refer to private car owners sharing their travel route information online in advance, allowing passengers with similar itineraries to board and share their journeys.

China is one of the most suitable markets in the world for developing shared mobility. China has a large number of densely populated cities, where population density poses challenges to existing travel infrastructure, thus generating demand for upgrades in travel solutions. For example, to improve traffic conditions and air quality, many local governments across China have implemented restrictions on the number of vehicles owned or usage time, such as license plate restrictions. Many cities also face shortages of parking spaces. At the same time, with the acceleration of urbanization and consumption upgrading, Chinese consumers' requirements for travel experiences are constantly increasing. In addition, private cars in China are mostly used for daily commuting and are idle for most of the time, with an average utilization rate of less than 30% in 2024, resulting in a large waste of resources. Therefore, shared mobility with low costs and better service experiences has great commercial potential in China.

The rapid development of the shared mobility industry has also driven the digital transformation of the traditional taxi industry and has received multiple government support policies. These policies have promoted the integrated development of taxi and online car-hailing services, facilitated the integration of traditional taxi models with online car-hailing platforms, reduced idle travel time for taxis, improved operational efficiency, and enhanced passenger experience. Leading shared mobility platforms are integrating traditional taxis into their systems and promoting taxi online-hailing solutions, while the traditional taxi industry is also actively advancing service upgrades. In addition, as an important part of integrated development, taxi companies need to promote fleet modernization, including purchasing customized models equipped with intelligent functions, optimizing the total cost of ownership (TCO) of vehicles, and enhancing passenger experience. The renewal of taxi fleets has also brought new market opportunities for enterprises focusing on developing such customized vehicles. The upgraded taxi service and the innovative integration of online car-hailing services are expected to further drive the development of China's shared mobility industry.

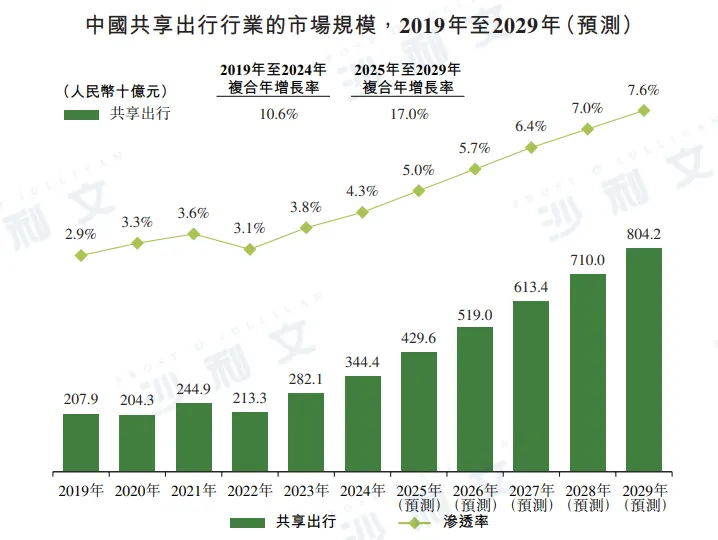

Although the China shared mobility market currently has a considerable scale, there is still broad room for growth in the future. It is estimated that between 2025 and 2029, as consumers' demand for cost-effective travel methods continues to rise, and shared mobility gradually becomes more popular in lower-tier cities, the penetration rate of shared mobility in the overall travel industry (measured as the proportion of shared mobility GTV to total travel GTV during the same period) will increase significantly from 4.3% in 2024 to 7.6% in 2029. As the share of shared mobility in the overall travel industry continues to grow, it is expected that the market size of China's shared mobility will grow significantly from 2025 to 2029, reaching RMB 804.2 billion, with a compound annual growth rate of 17.0%.

Source: Ministry of Transport of China, China Association of Automobile Manufacturers, Frost & Sullivananalysis

PART/4

The competitive landscape of China's online car-hailing industry

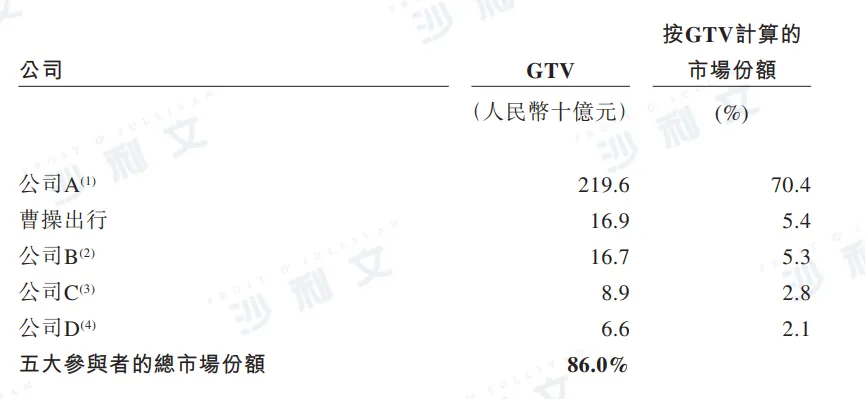

The shared mobility market consists of online car-hailing services and ride-sharing services. Among them, online car-hailing services are the largest sub-market with significant growth potential, accounting for about 90% of the total shared mobility market size in 2024. The market structure of online car-hailing service providers is dominated by a single major participant, which holds a market share of 70.4% based on GTV in 2024, with the remaining market share occupied by several major participants. Based on GTV in 2024, the top five market participants combined account for 86.0% of the market share.

According to GTV calculations, the company has always ranked among the top three online car-hailing platforms in China over the past three years.

Data source: Public information or documents of each company, Frost & Sullivananalysis

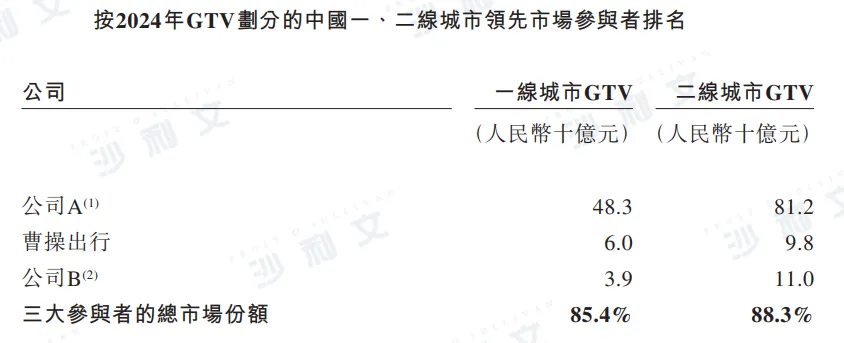

Shared mobility is a highly localized business, with each city being an independent market with its unique challenges and opportunities. This regional nature is reflected in differences in consumer preferences, infrastructure conditions, and market competition patterns. Therefore, gaining a deep understanding of local conditions and adapting flexibly to them is key for shared mobility companies to succeed. Calculated based on GTV for 2024, the company is one of the top three online car-hailing platforms in first- and second-tier cities in China.

Data source: Public information or documents of each company, Frost & Sullivananalysis

PART/5

The future development trend of China's shared mobility industry

●Traffic dispersion

After years of development, China's shared mobility market has transformed from a pattern dominated by a single participant to one where user traffic is more dispersed. Eight years ago, China's largest shared mobility service provider accounted for nearly 90% of all online car-hailing orders; today, this proportion has dropped to about 70%, with user traffic becoming more dispersed. Part of the reason for the dispersion of user traffic is the rise of aggregators. Aggregators include map navigation apps and local lifestyle services, such as Gaode, Meituan, Tencent Travel, and Baidu Maps. These platforms integrate user traffic and direct it to various mobility service providers. From 2019 to 2024, the proportion of online car-hailing orders completed through aggregators increased from 7.0% to 31.0%, and it is expected to rise further to 53.9% by 2029. The rise of aggregators has also brought growth opportunities to mobility service providers still in the early stages of development. Even if these companies do not enjoy the scale and network effects of the largest participants, they can still attract and retain users with high-quality services.

●Improved supervision

In recent years, the shared mobility market in China has developed rapidly, and regulatory requirements have become increasingly stringent. When providing shared mobility services, travel service providers and aggregators need to comply with multiple levels of compliance requirements in various aspects such as drivers, vehicles, and online platforms. Currently, due to numerous practical difficulties in obtaining the necessary licenses and permits, no major shared mobility service providers have achieved a 100% compliance rate. Over time, the focus of competition in the shared mobility market has shifted from competing for user traffic on the demand side to competing for compliant vehicles and drivers on the supply side. The lack of compliant drivers and vehicles is one of the reasons for the slowdown in growth rates of the shared mobility market from 2019 to 2024. As regulatory requirements tighten, the compliance costs borne by travel service providers continue to rise. With the market gradually acquiring more compliant drivers and vehicles, the shared mobility market is expected to expand further. In addition, affected by compliance and safety issues as well as the impact of COVID-19, the growth space of the ride-hailing market has been relatively limited in recent years. Online car-hailing has become the main driving force behind the growth of the entire shared mobility market.

●Travel operation vehicles

Characteristics of travel operation vehiclesTravel operation vehicles include those used for shared mobility and traditional taxi services, which differ from private cars in many aspects. Firstly, compared to private cars, travel operation vehicles typically depreciate faster, thus accelerating the replacement cycle and leading to a continuous demand for new vehicles. Secondly, several local government agencies in China have introduced relevant compliance standards, requiring travel operation vehicles to meet certain specific parameter requirements, including the number of seats, installation of satellite positioning devices, and wheelbase standards. Therefore, the market's demand for travel operation vehicles that comply with these compliance standards is increasing day by day, and customized models designed specifically to meet local government vehicle parameter requirements are becoming increasingly favored because they better meet the compliance standards. Finally, recent trends show that a large number of travel operation vehicles are purchased by enterprises (including shared mobility service providers and taxi service providers) rather than individuals. In 2024, 85.4% of travel operation vehicles were purchased by enterprises.

TCO comparison of shared mobility operating vehiclesIn the shared mobility value chain, vehicle TCO is the largest cost component affecting driver income and the profitability of travel service providers. In 2024, vehicle TCO accounted for about 55% of drivers' average total income. Reducing vehicle TCO has become a key to improving driver income levels and the profitability of travel service providers.

Vehicle TCO includes: (i) purchase cost or lease cost, (ii) energy replenishment cost, and (iii) vehicle maintenance cost. The purchase cost or lease cost is amortized evenly over its useful life. Energy replenishment cost refers to the direct expenses associated with refueling, charging, or battery swapping. Vehicle maintenance cost includes insurance expenses and repair costs.

There are a wide variety of vehicle models used for shared mobility. Among them, the TCO of pure electric vehicles is usually significantly lower than that of fuel vehicles. The lower TCO is mainly due to lower electricity prices and the relatively simple body structure of pure electric vehicles, which makes their energy replenishment and maintenance costs lower. However, the purchase cost of pure electric vehicles is usually higher than that of fuel vehicles because their R&D costs are still relatively high. With continuous progress in battery technology and the continuous expansion of scale by pure electric vehicle manufacturers to achieve economies of scale, it is expected that their average marginal production costs will continue to decline, further reducing the purchase cost of pure electric vehicles. In addition to TCO savings, pure electric vehicles with battery swapping modes can also bring other advantages to drivers, including shorter energy replenishment times, extended operating hours, and reduced initial purchase prices through vehicle battery separation models.

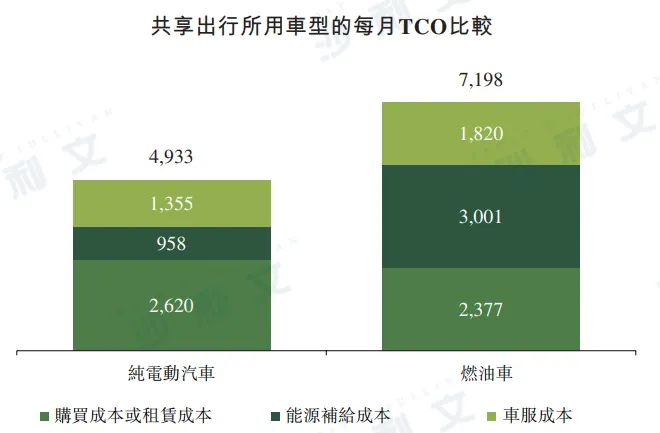

Considering the commonly used vehicle models in various travel services in China, the following figure shows a schematic comparison of vehicle TCO between fuel vehicles and pure electric vehicles under the car purchase model.

Source: Ministry of Transport of China, Frost & Sullivananalysis

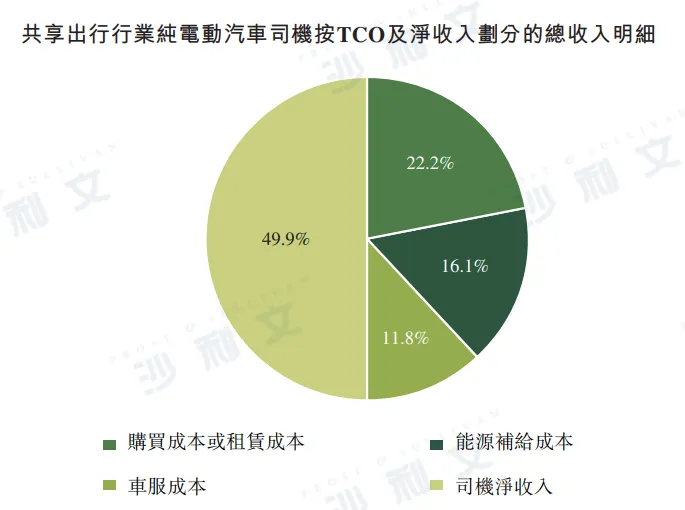

Considering the most commonly used pure electric vehicle models in China's shared mobility services, the following figure further illustrates a schematic breakdown of the total income of pure electric vehicle drivers by TCO and revenue:

Source: Ministry of Transport of China, Frost & Sullivananalysis

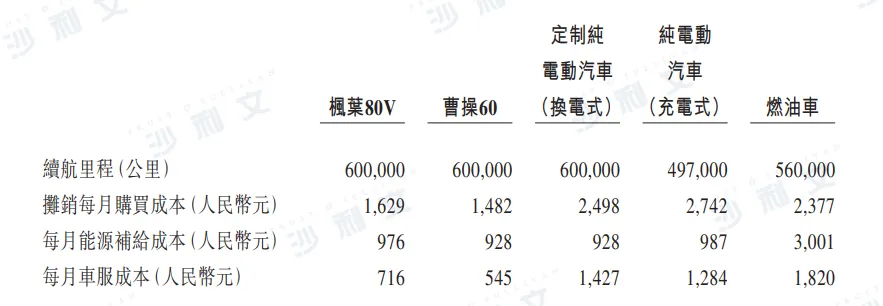

The company's Fengye 80V and Cao Cao 60 are considered two cost-effective models in shared mobility services. The expected TCOs for the Fengye 80V and Cao Cao 60 are RMB 0.53 per kilometer and RMB 0.47 per kilometer respectively, both equipped with battery swapping capabilities. The following table further illustrates the TCO comparison between the Fengye 80V, Cao Cao 60, and other typical mobility operation models:

Source: Ministry of Transport of China, Frost & Sullivananalysis

PART/6

Market opportunities for the sale of outbound operating vehicles

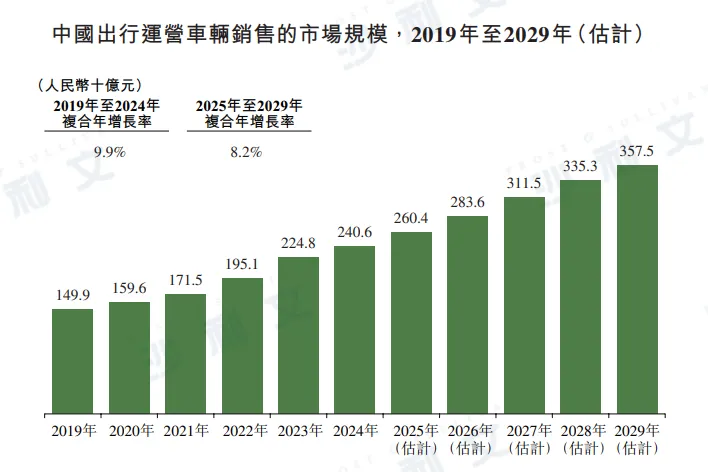

In terms of total vehicle sales for travel services, the sales market for travel operation vehicles has seen a significant increase in recent years and is expected to continue this upward trend. The market scale for travel operation vehicle sales increased from RMB 149.9 billion in 2019 to RMB 240.6 billion in 2024, and is expected to further grow at a compound annual growth rate of 8.2% from RMB 260.4 billion in 2025 to RMB 357.5 billion in 2029.

Data sources: National Bureau of Statistics of China, Ministry of Transport of China, China Association of Automobile Manufacturers, Frost & Sullivananalysis

The key to successful sales of travel operation vehicles lies in having the opportunity to reach drivers who use travel services, as these drivers are essentially potential customers and end-users of travel operation vehicles. Shared mobility service providers that have a large number of drivers using their services have a natural advantage, enabling them to occupy a favorable position in the travel operation vehicle sales market.