Frost & Sullivan

Zhejiang Sanhua Intelligent Control Co., Ltd. (Stock Code: 2050.HK) successfully listed on the main board of the Hong Kong capital market on June 23, 2025. The company is the world's largest manufacturer of refrigeration and air-conditioning control components and a global leader in automotive thermal management system parts. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provides exclusive industry advisory services for the listing of Zhejiang Sanhua Intelligent Control Co., Ltd., and hereby warmly congratulates them on their successful listing.

Zhejiang Sanhua Intelligent Control Co., Ltd. (hereinafter referred to as 'Sanhua Smart Control') successfully listed on June 23, 2025. The company plans to issue 3.6033 billion H shares, of which 93% will be international offerings and 7% will be public offerings. The maximum offering price per share is HK$22.53, and the net proceeds from the fundraising are expected to be approximately HK$7.741 billion.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing the relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business, and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

According to LiveReport's big data (statistical data as of June 1, 2025), from January to May 2025, as well as during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 17 (63%), 48 (63%) and 152 (68%) Hong Kong-listed IPOs respectively, boasting rich industry experience and communication skills with exchanges and investors.

PART/1

Investment Highlights

-

The company is the world's largest manufacturer of refrigeration and air-conditioning control components, as well as a global leader in automotive thermal management system parts;

-

The company attaches great importance to R&D investment, achieving rapid product iteration and forward-looking industrial layout;

-

The company adheres to implementing lean production concepts and pursues excellent and efficient resource allocation;

-

A comprehensive quality management system and quality control measures to ensure the delivery of high-quality products;

-

The company is a pioneer in global layout, possessing a complete global sales, R&D, and manufacturing system;

-

The company has long-term customer partners with a high industry standing, jointly leading the development of the industry;

-

Rich industry and management experience, a value concept that keeps pace with the times, and a visionary management team.

According to Frost & Sullivan's data, ranked by 2024 revenue:

-

The company holds a market share of approximately 45.5% in the global refrigeration and air-conditioning control component market;

-

The company holds a market share of approximately 4.1% in the global automotive thermal management system parts market, ranking fifth globally;

-

The company's four-way directional control valves, electronic expansion valves, micro-channel heat exchangers, globe valves, solenoid valves, Omega pumps, and ball valves rank first in their respective global markets, with market shares of 55.4%, 51.4%, 43.4%, 39.1%, 47.7%, 53.6%, and 32.8% respectively. In the same year, in terms of revenue, pressure sensors ranked second in the global sensor market, with a market share of 15.9%;

-

The company's automotive electronic expansion valves and integrated components rank first in their respective global markets, with market shares of 48.3% and 65.6%, respectively. In the same year, by revenue, battery coolers and automotive electronic water pumps ranked third and fourth in their respective global markets, with market shares of 5.9% and 5.5%, respectively;

PART/2

Analysis of the Refrigeration and Air-conditioning Control Components Market

Refrigeration and air-conditioning control components are essential parts of air conditioners and other refrigeration facilities used in residential and commercial settings, providing necessary functions such as controlling the heating and cooling processes, regulating refrigerant flow, and measuring pressure. The main categories of components that perform these necessary functions include valves, heat exchangers, controllers, and pumps. According to a Frost & Sullivan report, globally, the market size of refrigeration and air-conditioning control components increased from RMB 275 billion in 2020 to RMB 364 billion in 2024, with a compound annual growth rate of 7.4%. With the increasing demand for refrigeration and air-conditioning, the market size of global refrigeration and air-conditioning control components is expected to reach RMB 516 billion by 2029, with a compound annual growth rate from 2024 to 2029 of 7.2%. In terms of revenue in 2024, the global market sizes of valves, heat exchangers, controllers, and pumps accounted for 49.2%, 16.5%, 19.2%, and 3.0% of refrigeration and air-conditioning control components, respectively, totaling 87.9%.

Data source: Analysis by Frost & Sullivan

PART/3

Market Drivers and Future Opportunities for Refrigeration and Air Conditioning Control Components

● The requirements for product performance are constantly increasing, driving product iteration and upgrades.

Consumers place increasing emphasis on the quality and functionality of air conditioners, aiming to create a healthy, comfortable, and environmentally friendly home environment. As a result, the demand for product performance of refrigeration and air conditioning control components is becoming higher and higher. To meet the increasingly demanding product performance requirements, manufacturers of refrigeration and air conditioning control components have been committed to product iteration and upgrading. For example, technological upgrades to microchannel heat exchangers (such as innovative designs in bending areas) can achieve miniaturization of core components and significantly improve energy efficiency by increasing the heat exchange surface area.

● Global warming has led to a surge in demand for air conditioners.

In recent years, due to the frequent occurrence of extreme weather events such as global warming and high-temperature heatwaves, the demand for air conditioners has significantly increased. For example, in Europe, unprecedented high temperatures have led to an average summer temperature reaching a historical high, which has accelerated the popularization of air conditioners. From 2020 to 2024, the total revenue of household air conditioners in Europe increased from RMB 435 billion to RMB 688 billion, with an annual compound growth rate of 12.1%. Therefore, the surge in demand for air conditioners in Europe has driven an increase in the demand for refrigeration air-conditioning control components.

● Expanding overseas demand has driven China's export growth.

Due to the strict implementation of energy conservation and emission reduction policies, coupled with consumers' preference for high-performance products, the demand for refrigeration and air-conditioning control components in overseas markets continues to expand. Chinese manufacturers of refrigeration and air-conditioning control components lead global supply, continuously expanding their brand influence through excellent product quality, efficient supply chain management, and price advantages, thereby accelerating global business expansion. Therefore, driven by the continuous expansion of overseas market demand, China's export of refrigeration and air-conditioning control components will maintain stable growth in the future. With its first-mover advantage, global recognition, global R&D bases, localized production and sales networks, cooperation with many internationally renowned enterprises, and high-quality products and services that meet the needs of overseas market customers, the company can benefit from the growing demand in overseas markets.

PART/4

Global competition landscape of refrigeration and air-conditioning control components

According to a Frost & Sullivan report, the global refrigeration and air-conditioning control component market is highly concentrated. As of December 31, 2024, there were approximately 60 manufacturers of refrigeration and air-conditioning control components globally. With the increasing prominence of technical barriers and scale advantages in the refrigeration and air-conditioning control component market, the global market concentration is on the rise. Leading manufacturers continue to consolidate their dominant position through technological, product quality, and cost-effectiveness advantages. In contrast, small component manufacturers face difficulties competing with leading manufacturers due to insufficient technical reserves, limited production scale, and relatively weak supply chain integration capabilities. In terms of revenue in 2024, the top three global refrigeration and air-conditioning control component manufacturers accounted for about 81.0%, with one of them ranking first globally and holding a market share of about 45.5%.

Data source: Analysis by Frost & Sullivan

PART/5

Analysis of the Auto Thermal Management System Parts Market

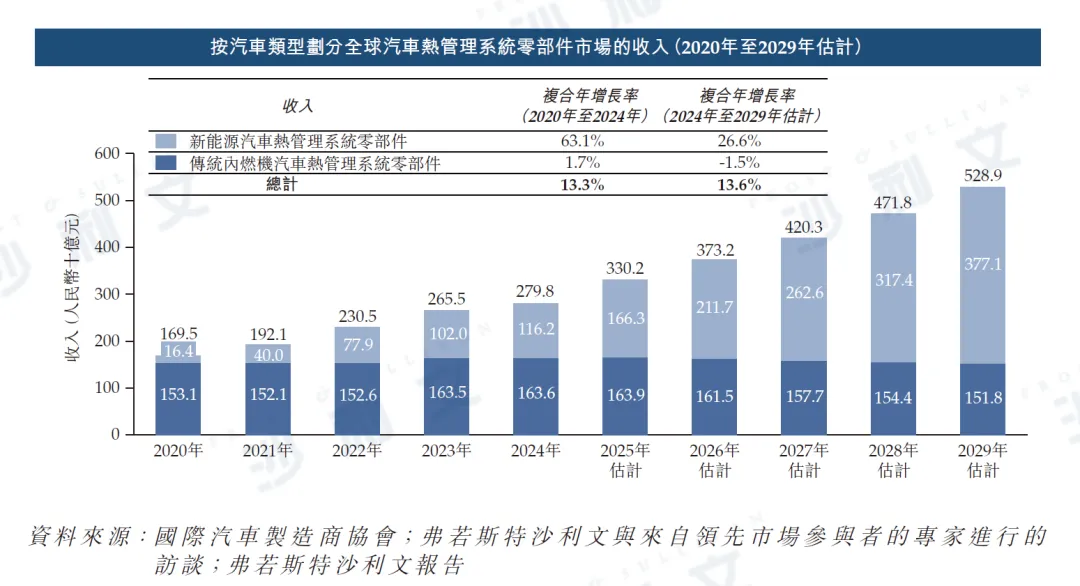

Automotive thermal management system components are a core automotive part. The thermal management system consists of components that monitor and control the operating temperatures of various automotive systems (such as engines and passenger cabins) to improve efficiency and prevent component damage. In terms of revenue, the global market size for automotive thermal management system components increased from RMB 169.5 billion in 2020 to RMB 279.8 billion in 2024, with an annual compound growth rate of 13.3%. Specifically, driven by the rapid development of the new energy vehicle industry, the revenue generated from new energy vehicle thermal management system components increased from RMB 16.4 billion in 2020 to RMB 116.2 billion in 2024, with an annual compound growth rate of 63.1%. By 2029, the global market size for automotive thermal management system components is expected to reach RMB 528.9 billion, with an annual compound growth rate of 13.6% from 2024 to 2029. Specifically, the revenue generated from new energy vehicle thermal management system components is expected to reach RMB 377.1 billion, with an annual compound growth rate of 26.6% from 2024 to 2029. China is the largest market for the global automotive thermal management system components market, accounting for about 48.4% of the revenue in 2024.

Data source: Analysis by Frost & Sullivan

PART/6

Market Drivers and Future Opportunities for Automotive Thermal Management System Components

● The rapid development of the new energy vehicle industry.

The decarbonization goals of the global automotive industry, the advancement of new energy vehicle technology, and the development of new energy vehicle charging infrastructure have driven rapid growth in the global new energy vehicle industry. Global new energy vehicle sales increased from 5.2 million units in 2020 to 21.4 million units in 2024, with an annual compound growth rate of 42.7%. In contrast, global fuel vehicle sales decreased from 72.8 million units in 2020 to 69.2 million units in 2024, with an annual compound growth rate of -1.3%. At the same time, technological progress (such as 5G and the Internet of Things) is accelerating the development of intelligent connected vehicles, and the commercialization of autonomous driving technology is continuously advancing, further increasing the penetration rate of new energy vehicles. From 2020 to 2024, the global penetration rate of new energy vehicles rose from 6.7% to 23.6%. The continuously developing new energy vehicle industry has driven rapid expansion of the automotive thermal management system parts market.

● The demand for reliable thermal management systems is growing continuously.

The advancement of new energy vehicle batteries and charging technology requires more reliable thermal management systems to ensure charging safety. Batteries are prone to overheating during charging, and improper temperature control can affect performance or even lead to safety issues. Therefore, an efficient thermal management system is crucial for maintaining the optimal operating temperature of batteries to ensure safety and performance. With the development of high-voltage fast charging and battery technology, the demand for rapid heat dissipation has correspondingly increased, thereby driving the demand for efficient automotive thermal management systems and the growth in demand for thermal management system components.

●Integrated and modular design.

With the advancement of automotive thermal management technology, automotive thermal management system components are developing towards integrated and modular designs. Integrated thermal management systems connect some or all of the circuits of the motor system, battery system, electronic control system, and air conditioning system into a loop, which not only achieves comprehensive thermal management, reduces energy waste, but also effectively lowers the overall vehicle weight and space occupancy. The modular design of automotive thermal management systems can shorten assembly time, improve the versatility of different vehicle models, and reduce maintenance costs for such systems.

PART/7

Competitive landscape of global automotive thermal management system components

According to a Frost & Sullivan report, the global automotive thermal management system (TMS) parts market is highly concentrated. Leading companies leverage their first-mover advantage to accumulate expertise in core parts and system development capabilities, while also possessing technical advantages in system integration. As of December 31, 2024, there were over 400 market participants in the global automotive TMS parts market. By revenue in 2024, the world's top five automotive TMS parts providers accounted for approximately 77.9%, with the fifth-ranked company holding a market share of about 4.1%.

Data source: Analysis by Frost & Sullivan

PART/8

Analysis of the Bionic Robot Electromechanical Actuator Market

Electromechanical actuators are one of the core components of bionic robot systems, responsible for converting electrical signals into corresponding mechanical movements to achieve precise control of bionic robot joints or moving parts. From 2020 to 2024, in terms of revenue, the global market size of electromechanical actuators for bionic robots increased from RMB 9.39 billion to RMB 13.761 billion, with an annual compound growth rate of 95.7%. With the continuous growth of downstream demand, in terms of revenue, the global market size of electromechanical actuators for bionic robots is expected to reach RMB 628 billion by 2029, with an annual compound growth rate of 114.7% from 2024 to 2029.

PART/9

Market Drivers and Future Opportunities for Bionic Robot Electromechanical Executives

● Population aging and rising labor costs.

As many countries enter an aging society, labor resources are becoming increasingly scarce. In 2023, the proportion of the global population aged 60 and above reached 14.2%, and it is expected to reach 16.7% by 2030. Bionic robots, due to their ability to mimic human movements, adapt to complex environments, and perform delicate tasks, have become an option for replacing labor. At the same time, labor costs are gradually rising with economic development. To maintain competitiveness, companies need to find effective ways to reduce labor costs. Bionic robots equipped with efficient electromechanical actuators can help companies reduce long-term operating costs, improve production flexibility and responsiveness. Therefore, the aging population and rising labor costs stimulate demand for bionic robots, thereby accelerating the development of the bionic robot electromechanical actuator market.