Frost & Sullivan

Haitian Condiment Food Co., Ltd. (Stock Code: 3288.HK) successfully listed on the main board of the Hong Kong capital market on June 19, 2025. The company is a global leading condiment enterprise dedicated to providing high-quality products to meet the seasoning needs of home cooking and dining experiences. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') has provided exclusive industry advisory services for the listing of Haitian Condiment Food Co., Ltd., and hereby warmly congratulates them on their successful listing.

Haitian Flavor Foods Co., Ltd. (hereinafter referred to as 'Haitian Flavor') successfully listed on June 19, 2025. The company plans to issue 2.63 billion H shares, of which 94% will be international offerings and 6% will be public offerings. The maximum selling price per share is HK$36.3, raising approximately HK$9.55 billion in net proceeds.

During the process of listing in Hong Kong, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing the writing of relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business, and other important sections), helping the issuer communicate with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and providing feedback on various industry-related issues to the Hong Kong Stock Exchange for the issuer.

According to LiveReport's big data (statistical data as of June 1, 2025), from January to May 2025, as well as during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 17 (63%), 48 (63%) and 152 (68%) Hong Kong-listed IPOs respectively, boasting rich industry experience and communication skills with exchanges and investors.

PART/1

Investment Highlights

-

The company is China's leading condiment enterprise;

-

The company owns national products and product families familiar to the vast consumer base;

-

The company has built an ultimate supply chain, possessing industry-leading quality, efficiency, and cost advantages;

-

The company has a good market coverage and penetration rate nationwide through its omnichannel sales network;

-

The company adheres to building the enterprise on technology, with an advanced R&D layout leading to high-quality and sustainable development;

-

The company's simple, pragmatic, open, and shared corporate culture, along with its management team, are the ballast stones that ensure its steady and long-term development.

According to the Frost & Sullivan report, in terms of revenue for 2024, the company:

-

Ranked fifth in the global condiment industry;

-

Ranked first in the global soy sauce market;

-

Ranked first in the global oyster sauce market;

-

Ranked first in the Chinese condiment industry;

-

Ranked first in the Chinese soy sauce market;

-

Ranked first in the Chinese oyster sauce market;

-

Ranked first in the Chinese basic condiment market.

PART/2

Global Condiment Industry Market Overview

Condiments refer to products that are widely used in dieting, cooking, and food processing, used to harmonize flavors and have functions such as enhancing aroma, freshness, and removing fishy odors. As one of the most commonly used products in consumers' daily dining, condiments have a stable demand and are less sensitive to changes in the economic environment, exhibiting strong cyclical resistance.

The global condiment market is a huge one. According to Frost & Sullivan the data, calculated by revenue, the global condiment market size was RMB2,143.8 billion in 2024, with a compound annual growth rate of 3.2% from 2019 to 2024. Affected by factors such as post-pandemic recovery, steady consumer demand growth, and increasingly rich condiment categories, the global condiment market size is expected to grow to RMB2,891.7 billion in 2029, with a compound annual growth rate of 6.2% from 2024 to 2029.

Source: Frost & Sullivan report

PART/3

Global Soy Sauce and Soy Sauce Products Industry Market Overview

Soy sauce is a liquid condiment with special color, aroma, and taste made primarily from soybeans and/or defatted soybeans, along with other ingredients such as water and salt. Soy sauce can also serve as a base for making soy sauce products, such as barbecue sauce, grilled sauce, white-braised sauce, cold salad sauce, oil and vinegar sauce, and various other compound condiments. Asian cuisine is gradually becoming more popular globally, driving the demand for soy sauce and soy sauce products among consumers worldwide. In 2024, soy sauce and soy sauce products accounted for about 12.8% of the global condiment market, reaching a scale of RMB 274.7 billion. From 2024 to 2029, the market size is expected to grow at a compound annual growth rate of 7.4%.

In terms of regional markets, Asian countries including China, Japan, South Korea, and Southeast Asian nations dominate the production and consumption of soy sauce and soy sauce products. With the integration of dietary cultures, consumers in North America and Europe have continuously incorporated soy sauce and soy sauce products into their daily diets, further driving market growth.

Source: Frost & Sullivan report

PART/4

Global Oyster Sauce Industry Market Overview

Oyster sauce is a condiment made from the concentrated juice after steaming or boiling raw oysters, or by enzymatic hydrolysis of raw oyster meat, combined with sugar, salt, and other additives. Originating in Guangdong Province, China, oyster sauce has developed rapidly in China and overseas regions. In 2024, the global oyster sauce market size reached RMB 191 billion, with a compound annual growth rate expected from 2024 to 2029 of 8.1%.

Source: Frost & Sullivan report

PART/5

Overview of the Chinese Condiment Industry Market

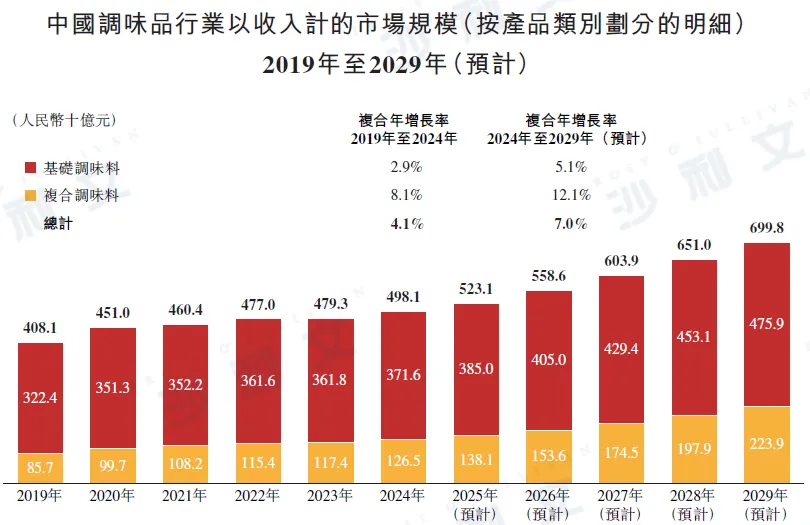

The Chinese condiment industry has experienced rapid development and has become the second-largest in the global condiment industry. According to Frost & Sullivan's data, China's condiment market size was RMB 498 billion in 2024, calculated by revenue. However, compared to the United States and Japan, China's per capita condiment consumption is only RMB 354 per year, which is about one-fifth of that in the US and one-third of that in Japan. Since 2023, the growth rate of China's condiment market has slowed down due to factors such as relatively slow recovery of consumer demand and the ongoing digestion of the impact of the pandemic on channels. Looking ahead, driven by per capita disposable income growth, urbanization rate improvement, diversification of condiment categories and sales channels, and increased market concentration, the market size of China's condiment industry is expected to increase to RMB 699 billion by 2029, with a compound annual growth rate of 7.0% from 2024 to 2029.

Chinese cuisine has many regional cuisines, each with different preferences for seasonings, providing a broad space for various seasoning categories. Seasonings are mainly divided into (i) basic seasonings, which refer to seasonings made from one material as the main ingredient, combined with other auxiliary materials. Common basic seasonings include soy sauce, basic seasoning paste, vinegar, cooking wine, oyster sauce, salt, sugar, monosodium glutamate, etc.; and (ii) compound seasonings, which refer to seasonings made from two or more materials as the main ingredient, combined with other auxiliary materials. Common compound seasonings include compound seasoning paste represented by chili paste and spaghetti sauce, liquid compound seasonings represented by soy sauce and hot pot sauce, as well as solid compound seasonings represented by hot pot base and chicken essence.

Due to its long history and wide application range, basic condiments have always been an important part of China's condiment industry and have maintained relatively stable growth. Among them, soy sauce is the largest subcategory, with a market scale reaching 104.1 billion yuan in 2024, accounting for about 28.0% of basic condiments and about 20.9% of the overall condiment industry. In recent years, with the improvement of residents' income and consumption levels, compound condiments have grown rapidly due to their convenience. Among them, compound condiment paste accounted for about 19.9% of compound condiments in 2024, while soy sauce products accounted for about 15.9%.

Source: Frost & Sullivan report

PART/6

Overview of the Chinese Soy Sauce Industry Market

In China, soy sauce has a stable and substantial consumer demand. According to Frost & Sullivan's data, the market size of soy sauce in China was RMB 104 billion in 2024, with a compound annual growth rate of 2.6% from 2019 to 2024. It is expected that the compound annual growth rate from 2024 to 2029 will be 4.8%.

Source: Frost & Sullivan report

PART/7

Overview of the Chinese Oyster Sauce Industry Market

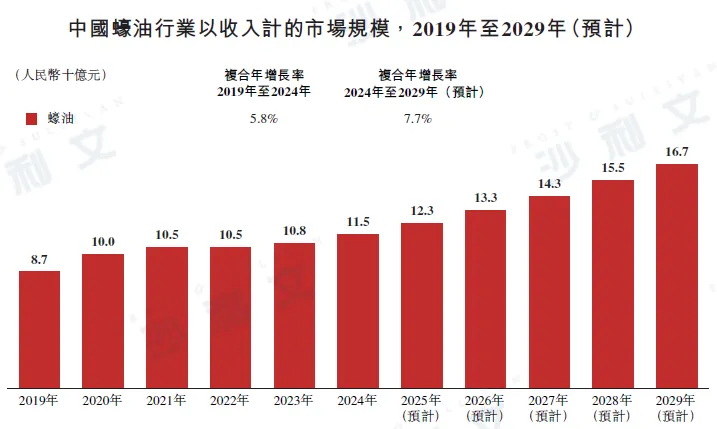

With the mutual penetration of eating habits across the country, oyster sauce has broken through traditional southern production areas and appeared on dining tables nationwide. Its accelerated penetration into daily cuisine has greatly promoted the rapid expansion of market size. According to Frost & Sullivan's data, in terms of revenue, the Chinese oyster sauce market size was RMB 115 billion in 2024, with a compound annual growth rate of 5.8% from 2019 to 2024, and it is expected to grow at a compound annual rate of 7.7% from 2024 to 2029.

Source: Frost & Sullivan report

PART/8

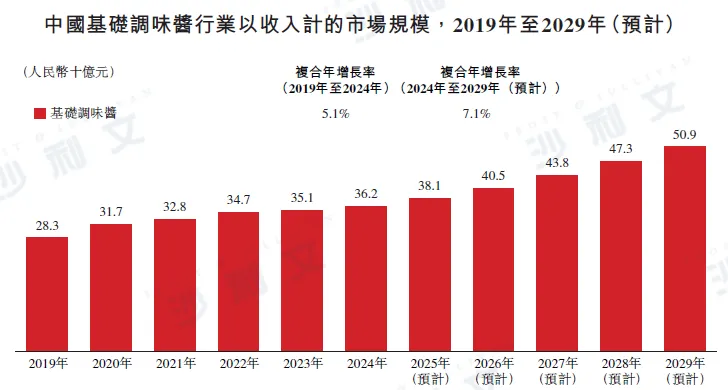

Overview of the Chinese Basic Condiment Market

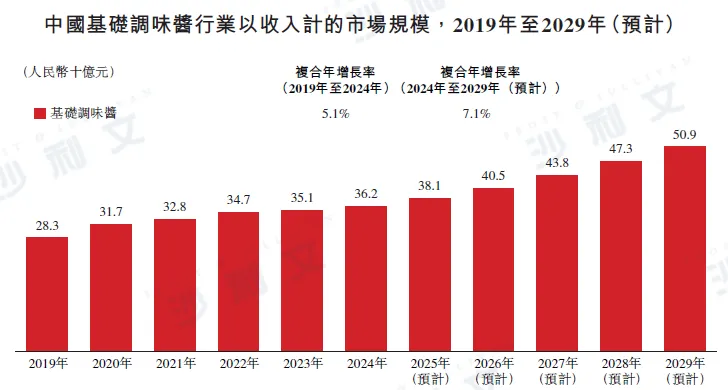

Condiments are mainly divided into basic condiments and compound condiments. Basic condiments refer to sauces made primarily from one material, combined with other additives, including soy sauce, flour sauce, etc., which have a large consumer base and demand. According to Frost & Sullivan's data, calculated by income, the market size of basic condiments in China was RMB 362 billion in 2024. From 2019 to 2024, the compound annual growth rate of basic condiments was 5.1%, and it is expected that the compound annual growth rate from 2024 to 2029 will be 7.1%.

Source: Frost & Sullivan report

PART/9

Competitive landscape of the global condiment industry

According to Frost & Sullivan's data, ranked by flavoring business revenue for 2024, the company is fifth in the global flavoring industry.

Source: Public information or documents of each company, Frost & Sullivan reports

PART/10

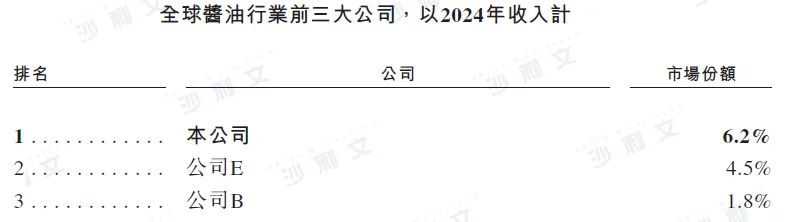

Competitive landscape of the global soy sauce and soy sauce products industry

According to Frost & Sullivan's data, ranked by 2024 revenue, the company is the largest player in the global soy sauce market, with a market share of 6.2%.

Source: Public information or documents of each company, Frost & Sullivan reports

PART/11

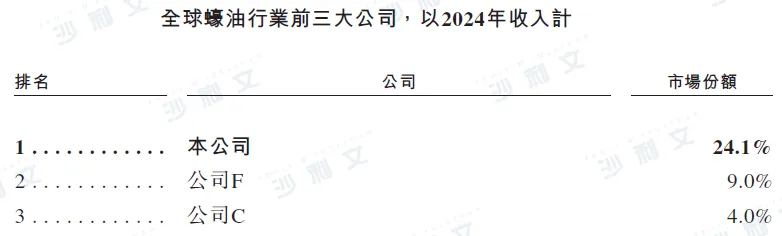

The competitive landscape of the global oyster sauce industry

According to Frost & Sullivan's data, ranked by 2024 revenue, the company is the largest in the global oyster sauce market, holding a market share of 24.1%.

Source: Public information or documents of each company, Frost & Sullivan reports

PART/12

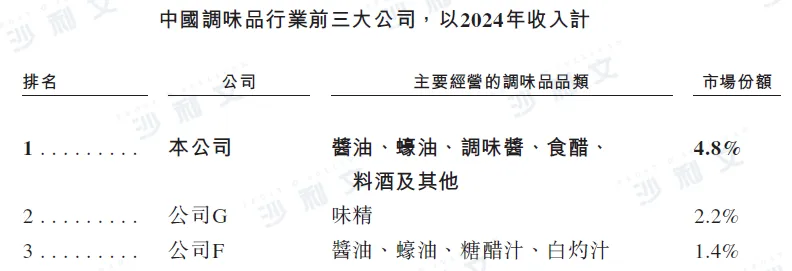

The competitive landscape of the Chinese condiment industry

According to Frost & Sullivan's data, the company has maintained its leading position as the number one seller in the Chinese condiment industry for 28 consecutive years. In terms of revenue for 2024, our market share was 4.8%.

Source: Public information or documents of each company, Frost & Sullivan reports

PART/13

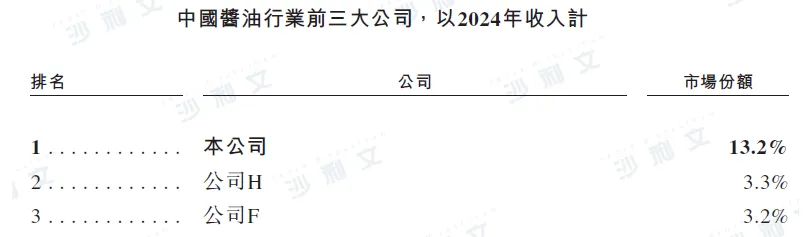

The competitive landscape of the soy sauce industry in China

According to Frost & Sullivan's data, the company has maintained its leading position as the number one seller in the Chinese soy sauce market for 28 consecutive years. In terms of revenue for 2024, our market share was 13.2%.

Source: Public information or documents of each company, Frost & Sullivan reports

PART/14

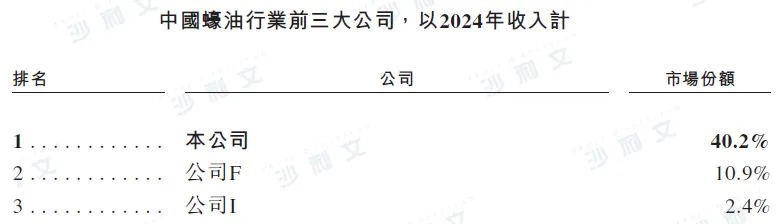

The competitive landscape of China's oyster sauce industry

According to Frost & Sullivan's data, the company has maintained its leading position as the top-selling brand in the Chinese oyster sauce industry for twelve consecutive years. In terms of revenue for 2024, our market share was 40.2%.

Source: Public information or documents of each company, Frost & Sullivan reports

PART/15

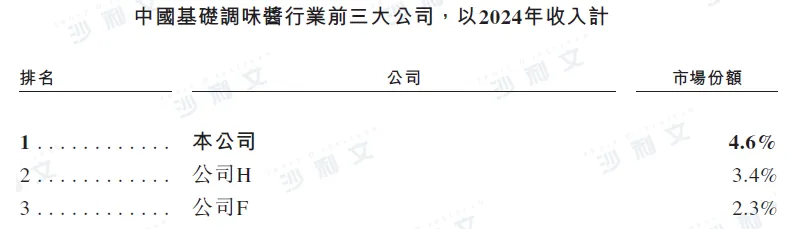

Competitive landscape of the Chinese base seasoning sauce industry

According to Frost & Sullivan's data, ranked by 2024 revenue, we are the number one player in the Chinese basic condiment market, with a market share of 4.6%.

Source: Public information or documents of each company, Frost & Sullivan reports

PART/16

Driving Factors and Future Trends of the Chinese Condiment Industry

●Diverse dietary cultures and consumer demands drive the development of multiple categories of condiments

China has a vast territory, and the dietary cultures and taste preferences of various regions exhibit rich diversity. The diverse cuisines and differentiated cooking habits provide ample space for the development and diversification of condiments. At the same time, with the improvement of living standards, consumers' demands for dietary health, taste, convenient packaging, and other aspects are constantly becoming more refined. For example, consumers carefully select condiments during cooking based on different dishes to enhance the flavor of the dishes, such as using cold soy sauce for cold dishes and steamed fish sauce for steamed fish. In addition, consumers' attention to healthy diets is increasing, and their demand for organic and low-salt condiment products is rising, driving the healthy development of condiments. Under the combined effect of these factors, condiments are becoming increasingly diverse in variety.

●The increase in the catering chain rate drives the demand for condiments

The chain restaurant penetration rate in China has increased from 13.3% in 2019 to 22.0% in 2024. However, it is still relatively low compared to developed market countries and is expected to continue to rise. Chain restaurant enterprises have a high demand for condiments, which directly drives the expansion of the scale of condiment enterprises and an increase in product sales. Chain restaurant enterprises have high requirements for the standardization of condiment solutions, and the demand for customization is also growing day by day. Therefore, condiment enterprises that can provide standardized and large-scale products as well as the ability to quickly respond to customized needs can better help chain restaurant enterprises achieve taste consistency and standardized meal preparation by providing complete solutions, thereby enhancing their competitiveness and gaining more market share.

●Diversification of distribution channels unleashes consumer potential

Offline channels, due to their convenience and vast geographical coverage, will continue to dominate the sales of condiments. In addition, the development of emerging channels such as community group buying, fresh e-commerce, and online shopping platforms has provided consumers with more diverse product access methods. Condiment companies are increasingly using emerging channels to reach more consumers. For enterprise customers such as catering and food processing companies, specialized online procurement platforms offer them a more convenient shopping experience. Combined with new media marketing, diversified channels bring the potential for consumption growth to the condiment market.

●The demand for compound seasonings has increased

Currently, with the continuous acceleration of life rhythms and the increasing working hours, people's demand for convenient living has risen. Compound seasonings can solve the seasoning problems of consumers with insufficient cooking experience, and with their convenience of use, compact packaging, and reduction in cooking time, they meet consumers' demand for efficiency. In addition, chain catering enterprises have high requirements for the standardization and customization of seasonings, driving the demand for highly standardized and efficient compound seasonings among catering enterprises. With the increasing demand for compound seasonings, soy sauce, as an important base for many compound seasonings, has also seen a corresponding increase in demand.

PART/17

Key Success Factors in China's Condiment Industry

●A trustworthy brand image

With the improvement of living standards and the popularization of quality-conscious consumption concepts, brand recognition has become an important basis for consumers to choose condiments. Consumers' trust in brands needs to be built over a long period. A brand image with a long history, professionalism, and credibility can distinguish a company from competitors and maintain competitive advantage for the long term.

●R&D capabilities and the unique taste memory it has created

The brewing process and fermentation technology of major condiment categories such as soy sauce and vinegar are relatively complex. Mature condiment companies have invested a large amount of capital and manpower in product research and development, forming unique product flavors. Condiments, as an indispensable dining element for consumers throughout the year, bring consumer stickiness through long-term taste memories, leading to continuous repurchases and brand trust, and constituting a unique competitive barrier.

●Multi-category layout, product iteration, and innovation capabilities

The market structure of Chinese condiments is diversified. A multi-category layout can help condiment companies meet the diverse needs of consumers, strengthen consumer brand recognition, and thus enhance the overall market competitiveness of the companies. A multi-category layout can also cover a wider range of consumer groups and increase attractiveness to distributors. In addition, condiment companies also need to quickly capture market trends and iterate product updates to meet changing consumer needs and maintain brand vitality.

●Diverse and extensive sales network

The coverage and stability of the sales network are crucial for seasoning companies. Leading seasoning companies in the industry, through years of accumulation of channel resources, possess a vast sales network, a professional team, mature channel management capabilities, and rich operational experience. They can cover the national market extensively and deeply. At the same time, a comprehensive layout of sales channels enables seasoning companies to promptly grasp trends in channel changes and seize sales opportunities that grow rapidly in channels or regions.

●Efficient supply chain and strong production capacity

The seasoning industry is an asset-intensive sector with a long input-output cycle, significant capital investment required for capacity building, and the need for long-term accumulation of production technology. Leading seasoning companies in the industry have invested for a long time in upgrading production equipment, research and development, and talent introduction, and have a clear scale economy advantage. In addition, by constructing an end-to-end supply chain system from procurement to sales and creating a flexible production system, seasoning companies can further improve production efficiency, flexibly meet the diversified market needs, and enhance operational efficiency.