Guangzhou Yinnuo Medicine Group Co., Ltd. (Stock Code: 2591.HK) successfully listed on the main board of the Hong Kong capital market on August 15, 2025. The company is the first in Asia and third globally to commercialize a long-acting humanized GLP-1 receptor agonist, and has launched its core product, exenatide & alpha (trade name: Yinoqiang), for the treatment of type 2 diabetes (T2D) in China.®) commercialization, focusing on developing therapies for diabetes and other metabolic diseases. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provides exclusive industry advisory services for the listing of Guangzhou Yinuo Medicine Group Co., Ltd. We hereby extend our warmest congratulations on its successful listing.

Guangzhou Yinnuo Medicine Group Co., Ltd. (hereinafter referred to as 'Yinnuo Medicine') successfully listed on August 15, 2025. The company plans to issue 36,556,400 H shares, of which 90% will be for international sale and 10% for Hong Kong sale. The maximum issue price per share is HK$18.68, raising a net amount of approximately HK$610 million.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing the relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

Frost & Sullivan has always been a leader in helping companies go public in Hong Kong. According to LiveReport's big data (statistical data as of June 30, 2025), from January to June 2025, as well as during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services to 29 (accounting for 71% of the market share), 60 (accounting for 67% of the market share), and 164 (accounting for 69% of the market share) Hong Kong-listed IPOs, ranking first in terms of number. It has rich industry experience and communication experience with regulatory authorities, exchanges, investment and financing institutions, and various related agencies.

PART/1

Investment Highlights

-

The company is the first in Asia and third globally in commercializing a proprietary long-acting human glucagon-like peptide-1 (GLP-1) receptor agonist. It strategically designs a drug pipeline focused on metabolic diseases, aiming to innovate patient treatment methods and seize significant market opportunities.

-

The company's core product, Exenatide & Alpha, is a self-developed human-long-acting GLP-1 receptor agonist used for the treatment of T2D and other metabolic diseases. It has the advantages of rapid onset, strong efficacy and durability, long half-life, and good safety. The company is actively promoting the global commercialization of Exenatide & Alpha and continuously developing new indications for it.

-

The company has formulated and integrated a full-channel commercial strategy for hospitals, retail pharmacies, and other online or offline sales channels, fully preparing for the commercialization of ISISAGLUTIDE & ALPHA. Its commercialization team consists of experienced professionals with an average of about 20 years of expertise in the treatment of metabolic diseases and market launch of pharmaceutical consumer goods;

-

The company continues to develop candidate drugs in preclinical stages and IND preparation phases for the treatment of metabolic diseases such as AD, obesity, overweight, MASH, T1D, and T2D, aiming to provide innovative and effective solutions for these diseases that currently lack effective therapies;

-

The company relies on advanced technology and a one-stop R&D system to continuously discover and develop innovative candidate drugs; its independently developed recombinant fusion protein platform enables it to produce and develop biopharmaceuticals; it has an experienced clinical team capable of effectively and efficiently carrying out clinical research and development, with strong translational medicine capabilities; it also has an experienced management team with profound scientific expertise and industry insight.

PART/2

Overview of the Global Metabolic Disease Drug Market

Metabolic diseases are disorders that occur when the body's cellular level of food absorption is disrupted. Metabolic diseases can hinder cells from carrying out key biochemical reactions, particularly those involving the processing and transport of proteins, carbohydrates (sugars and starches), and lipids (fatty acids). Therefore, metabolic diseases can lead to various health problems such as diabetes, obesity and overweight, and metabolic dysfunction-related fatty liver (MASH). In addition, these diseases can cause neurodegeneration by disrupting key processes such as lipid metabolism, glucose metabolism, and mitochondrial function, thereby significantly increasing the risk of developing neurodegenerative diseases (including Alzheimer's disease (AD)).

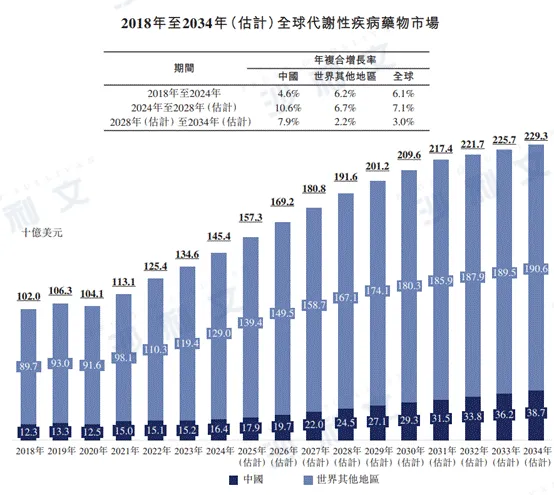

● Global and China's Metabolic Disease Drug Market Size and Growth

The global metabolic disease drug market grew from $102 billion in 2018 to $1454 billion in 2024, with an annual compound growth rate of 6.1%. It is expected to reach $1916 billion by 2028, with an annual compound growth rate of 7.1% from 2024 to 2028, $2293 billion by 2034, and 3.0% from 2028 to 2034.

The metabolic disease drug market in China shows an overall growth trend, increasing from $12.3 billion in 2018 to $16.4 billion in 2024, with an annual compound growth rate of 4.6%. It is expected to reach $245 billion by 2028, with a compound annual growth rate of 10.6% from 2024 to 2028, and $387 billion by 2034, with a compound annual growth rate of 7.9% from 2028 to 2034. The growth rate is higher than that of the global metabolic disease drug market.

The following figure lists the scale of the global and Chinese metabolic disease drug markets for the indicated years.

Data sources: annual reports, literature reviews, Frost & Sullivan analysis

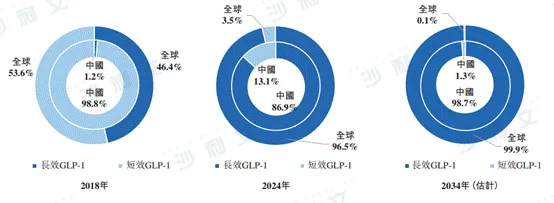

●GLP-1-based therapies

GLP-1-based therapies are reshaping the treatment paradigm for metabolic diseases. GLP-1 exerts its biological function by activating its receptor. GLP-1 receptors are expressed in various organs and tissues within the body, including adipose tissue, liver, cardiovascular system, and central nervous system. In the islets of Langerhans, GLP-1 stimulates insulin secretion and inhibits glucagon release. Importantly, GLP-1 can increase the regeneration of pancreatic beta-cells. In addition, GLP-1-based therapies can also suppress appetite, delay gastric emptying, regulate lipid metabolism, and reduce fat deposition.

In 2018, long-acting GLP-1-based therapies accounted for almost zero of the market share in China's GLP-1-based therapy market; this market share increased to 86.9% by 2024 and is expected to rise to 98.7% by 2034. Compared with the global market, the market share of long-acting GLP-1-based therapies in China from 2018 to 2024 was relatively low. However, this gap is expected to narrow in the future, indicating strong growth potential in the Chinese market.

The following figure lists the details and trends of the long-acting and short-acting GLP-1-based therapy markets in China and globally for the years shown.

Data sources: Annual reports of Eli Lilly, Novo Nordisk and AstraZeneca, and Frost & Sullivan analysis

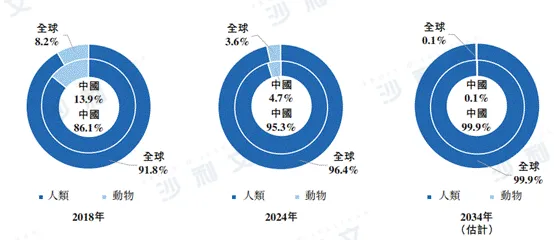

●Humanized GLP-1-based therapy

Compared with animal-derived GLP-1-based therapies, humanized GLP-1-based therapies have convincing advantages in terms of safety and duration of action. For example, humanized GLP-1-based therapies can reduce immunogenicity, thereby reducing the risk of developing drug-resistant antibodies and maintaining long-term blood glucose control. These humanized therapies also exhibit the best in vivo clearance rates, preventing drug accumulation over long-term use and minimizing related risks. Therefore, humanized GLP-1-based therapies have become a major development trend for GLP-1-based therapies.

The following figure lists the breakdown and trends of China's and global GLP-1-based therapies market by humanized and animal-derived therapies for the years shown.

Data sources: Annual reports of Eli Lilly, Novo Nordisk and AstraZeneca, and Frost & Sullivan analysis

PART/3

Overview of the Global and Chinese Diabetes Drug Markets

Diabetes is a major chronic disease globally. It not only leads to serious health complications but also imposes a heavy economic burden on the healthcare system. In China, the number of diabetes patients increased from 1.257 billion in 2018 to 1.48 billion in 2024, with an annual compound growth rate of 2.8%. It is expected to reach 1.637 billion by 2028 and 1.741 billion by 2034. Among them, the number of T2D patients increased from 1.2 billion in 2018 to 1.411 billion in 2024, with an expected increase to 1.551 billion by 2028 and 1.644 billion by 2034. Despite the large and growing patient population, by 2024, only 1.9% of diabetes patients in China received GLP-1-based therapies. This low penetration rate highlights significant market opportunities for GLP-1-based therapies in China.

The global diabetes prevalence increased from 4.583 billion in 2018 to 5.89 billion in 2024, with an annual compound growth rate of 4.3%. It is projected that by 2028, the number will reach 6.4 billion, and by 2034, it will reach 6.976 billion.

Among them, the number of T2D patients increased from 4.197 billion in 2018 to 5.493 billion in 2024, and it is expected to reach 5.993 billion by 2028 and 6.572 billion by 2034.

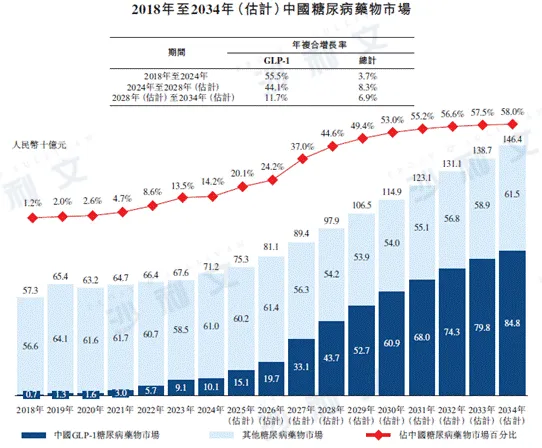

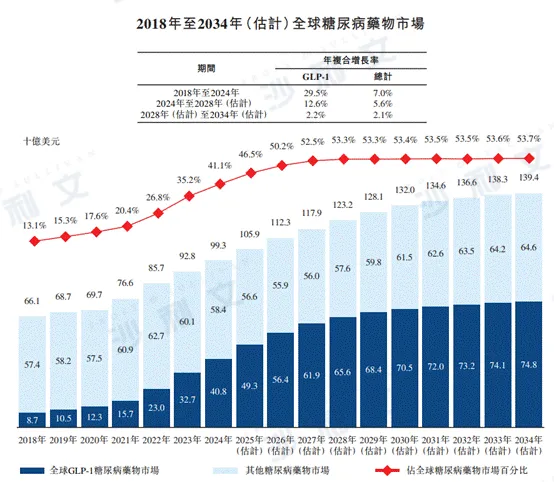

● Global and China Diabetes Drug Market Size and Growth

The Chinese diabetes drug market grew from RMB 57.3 billion in 2018 to RMB 712 billion in 2024, with an annual compound growth rate of 3.7%. It is expected that the market will continue to expand, reaching RMB 979 billion by 2028, with a compound annual growth rate of 8.3% from 2024 to 2028, and RMB 1464 billion by 2034, with a compound annual growth rate of 6.9% from 2028 to 2034. The Chinese GLP-1 diabetes drug market increased significantly from RMB 700 million in 2018 to RMB 101 billion in 2024, with an annual compound growth rate of 55.5%, and is expected to continue growing rapidly, reaching RMB 437 billion by 2028, with a compound annual growth rate of 44.1% from 2024 to 2028, and RMB 848 billion by 2034, with a compound annual growth rate of 11.7% from 2028 to 2034.

In 2024, the global diabetes drug market was $993 billion. It is expected that the global diabetes drug market will grow to $1232 billion by 2028 and $1394 billion by 2034, with a compound annual growth rate of 5.6% from 2024 to 2028 and 2.1% from 2028 to 2034. From 2018 to 2024, the global GLP-1 diabetes drug market size increased from $8.7 billion to $40.8 billion, with a compound annual growth rate of 29.5%. In the future, the global GLP-1 diabetes drug market size will continue to grow steadily, with an expected 2028 market size of $656 billion, a compound annual growth rate of 12.6%.

The following figure lists the market size of diabetes drugs in China and globally for the indicated years.

Data sources: annual reports, literature reviews, China Pharmaceutical Affairs, Frost & Sullivan analysis, interviews with key opinion leaders, Diabetes Branch of the Chinese Medical Association, World Bank, Chinese Journal of Epidemiology

Data sources: annual reports, literature reviews, Frost & Sullivan analysis, World Bank

PART/4

Overview of the Global and Chinese Markets for Overweight and Obesity Drugs

Overweight and obesity are risk factors for a range of chronic diseases and can also lead to various social and psychological problems. In 2021, China's medical expenses related to these diseases exceeded 200 billion yuan, accounting for 21.5% of the total national healthcare costs. It is estimated that by 2030, this number will further rise to 418 billion yuan. Globally, the burden caused by overweight and obesity is equally significant. In 2020, the economic cost of these diseases was estimated at $1.96 trillion, accounting for 2.9% of global GDP. It is projected that by 2035, this figure will rise to $4 trillion.

In China, the number of obese and overweight patients increased from 5.318 billion in 2018 to 6.394 billion in 2024, with an annual compound growth rate of 3.1%. It is estimated that by 2028, the number will reach 7.101 billion, and by 2034, it will reach 8.183 billion. The global number of obese and overweight patients has increased from 28.695 billion in 2018 to 35.75 billion in 2024, with an annual compound growth rate of 3.7%. It is estimated that by 2028, the number will reach 39.532 billion, and by 2034, it will reach 45.184 billion.

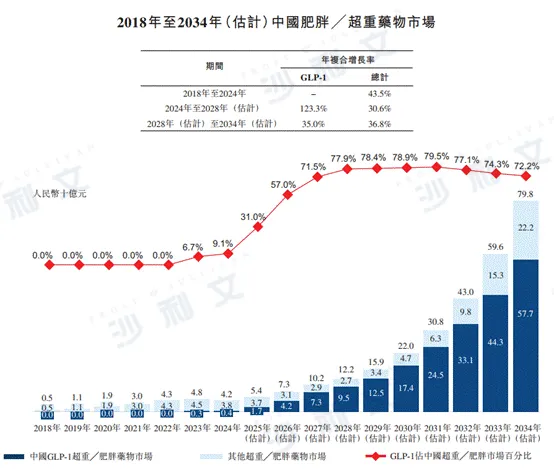

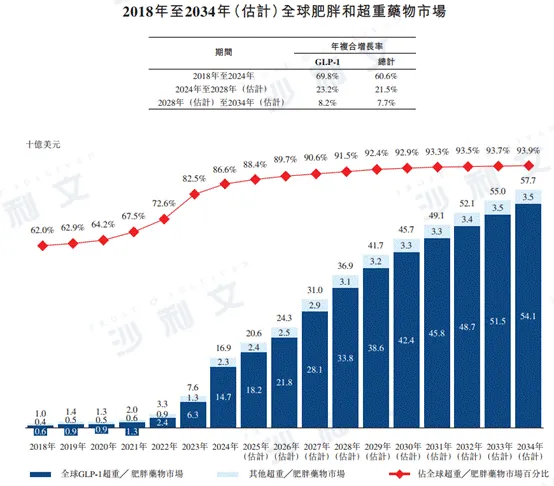

● Global and China's markets for overweight and obesity medications: size and growth

From 2018 to 2024, the Chinese obesity and overweight medication market grew from RMB 500 million to RMB 42 billion, with an annual compound growth rate of 43.5%. It is expected that the market size will continue to grow to RMB 122 billion by 2028 and RMB 798 billion by 2034. The annual compound growth rates from 2024 to 2028 and from 2028 to 2034 are 30.6% and 36.8%, respectively.

In 2024, the global obesity/overweight drug market was $16.9 billion. It is expected that by 2028 and 2034, the global obesity/overweight drug market will grow to $36.9 billion and $57.7 billion respectively, with annual compound growth rates of 21.5% and 7.7% from 2024 to 2028 and from 2028 to 2034.

The following figure lists the market size of overweight and obesity medications in China and globally for the indicated years.

Data source: Annual report, Frost & Sullivan analysis

Data sources: annual reports, literature reviews, Frost & Sullivan analysis, World Bank

PART/5

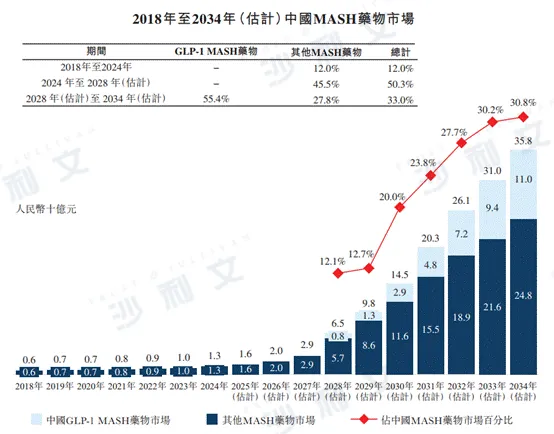

Overview of the Global and Chinese MASH Drug Markets

MASH is a serious liver disease caused by inflammation and damage due to fat accumulation in the liver. It is a more severe form of metabolic-related fatty liver disease (MAFLD). If not treated in time, MASH can lead to scarring (fibrosis) of the liver, which may progress to cirrhosis and even liver cancer.

In China, the prevalence and impact of MASH are also on the rise. Epidemiological studies and model projections indicate that the number of deaths related to MASH in China will increase from 25,580 in 2016 to 55,740 by 2030. In addition, a systematic review of liver cirrhosis-related deaths in China shows that 32.6% of the deaths are associated with MASH, accounting for 1.25% of the total mortality rate in China. In China, the annual mortality rate from liver disease in MASH patients is 11.77%, with a total mortality rate of 25.56%. Moreover, MASH is often accompanied by several other chronic diseases, including obesity, diabetes, and cardiovascular diseases, making treatment more complex and increasing the overall health burden on patients and the healthcare system.

In China, the number of MASH patients increased from 3.62 million in 2018 to 4.40 million in 2024, with an annual compound growth rate of 3.3%. It is expected to reach 5.03 million by 2028 and 6.11 million by 2034. The global number of MASH patients increased from 3.3 million in 2018 to 4.005 billion in 2024, with an annual compound growth rate of 3.3%. It is expected to reach 4.531 billion by 2028 and 5.376 billion by 2034.

● Global and China MASH drug market size

From 2018 to 2024, the market scale of MASH drugs in China increased from RMB 600 million to RMB 1.3 billion, with an annual compound growth rate of 12.0%. In the future, the market scale of MASH drugs in China will continue to grow steadily. It is expected that by 2028, it will reach RMB 65 billion. The annual compound growth rate from 2024 to 2028 is 50.3%, and by 2034, it will reach RMB 358 billion. The annual compound growth rate from 2028 to 2034 is 33.0%. In 2024, 2028, and 2034, the penetration rates of GLP-1 drugs used to treat MASH were 0.0%, 12.1%, and 30.8% respectively.

In 2024, the global MASH drug market was $3.4 billion. It is expected that the global MASH drug market will grow to $16.4 billion and $53.6 billion in 2028 and 2034 respectively, with annual compound growth rates of 48.3% and 21.9% from 2024 to 2028 and from 2028 to 2034.

The following figure lists the market size of MASH drugs in China for the indicated years.

Data sources: annual reports, literature reviews, Frost & Sullivan analysis

PART/6

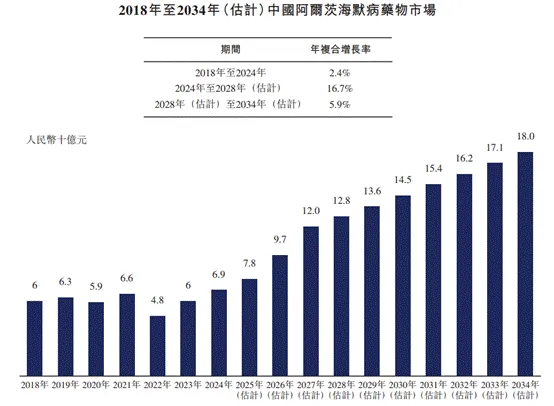

China's Alzheimer's Disease (AD) Drug Market

Alzheimer's disease (AD) is a progressive neurodegenerative disorder and the main cause of dementia, accounting for 60% to 70% of global dementia cases. The main risk factor for AD is advanced age, making the elderly population most susceptible. The number of AD patients in China increased from 1.13 million in 2018 to 1.45 million in 2024, with an annual compound growth rate of 4.3%. It is estimated that by 2028, the number will reach 1.68 million, and by 2034, it will reach 2.08 million.

● Market Size of Alzheimer's Disease (AD) Drugs in China

From 2018 to 2024, the market size of Alzheimer's drugs in China increased from RMB 6 billion to RMB 6.9 billion, with an annual compound growth rate of 2.4%. In the future, the market size of Alzheimer's drugs in China will grow steadily and is expected to reach RMB 128 billion by 2028, with a compound annual growth rate of 16.7% from 2024 to 2028, reaching RMB 180 billion by 2034, and with a compound annual growth rate of 5.9% from 2028 to 2034.

The following figure lists the market size of Alzheimer's disease drugs in China for the indicated years.

Data sources: annual reports, literature reviews, Frost & Sullivan analysis

Frost & Sullivan, integrating 64 years of global consulting experience, has dedicated 27 years to serving the booming Chinese market. With a global perspective, it helps clients accelerate their business growth and achieve benchmark positions in industry growth, innovation, and leadership. The healthcare industry is one of Frost & Sullivan's core areas of focus. Over the past 20-plus years, the Frost & Sullivan team has provided financing and financial advisory, IPO industry advisory, strategic consulting, management consulting, and other services to hundreds of outstanding domestic and international biopharmaceutical, medical device, healthcare services, and internet healthcare companies. Successful listings include: Zhonghuiyuantong (2627.HK), Dongguangyang Medicine (6887.HK), Weilizhibo (9887.HK), Bokangshiyun (2592.HK), Yunzhisheng (9678.HK), TED Medicine (3880.HK), Baize Medical (2609.HK), Yaojie Ankang (2617.HK), Jiangsu Hengrui Medicine (1276.HK), Mire (2629.HK), Ying'en Biology (9606.HK), Weisheng Pharmaceutical (2561.HK), Yasheng Medicine Group (NASDAQ:AAPG), Brain Motion Aurora (6681.HK), Health Road (2587.HK), Huahao Zhongtian (2563.HK), Yinosi (688710.SH), Jingta Technology (2228.HK), Yimai Sunshine (2522.HK), Shenghe Biology (2898.HK), Quanxin Biology (2509.HK), Meizhong Jiahé (2453.HK), WuXi AppTec (2268.HK), Neusoft Xikang (9686.HK), Youzhiyou (2496.HK), Yiming Angke (1541.HK), Kerenbo Tai (6990.HK), LaiKai Medicine (2105.HK), Lzhu Biology (2480.HK), Meis Health (2415.HK), PHECR, Zhongjin Medical (NASDAQ:ZJYL), Meiliyuan (2373.HK), Kangfeng Biology (6922.HK), Bao'an Biology (6955.HK), Sididi (1244.HK), Meihao Medical (1947.HK), Gaoshi Medical (2407.HK), Lepu Xintai (2291.HK), Jianshi Technology (9877.HK), Health Yuan (JCARE.SW), Lepu Medical (LEPU.SW), Dingdang Health (9886.HK), Bao'osuitu (2315.HK), Zhiyun Health (9955.HK), MeinGene (6667.HK), PRE.NASDAQ, Yunkang Group (2325.HK), Ruike Biology (2179.HK), Lepu Biology (2157.HK), Baxin Anhuan (2185.HK), Yonghe Medical (2279.HK), Kailai Ying (6821.HK), Beihai Kangcheng (1228.HK), Gusheng Tang (2273.HK), Yingpeng Technology (2251.HK), Minimally Invasive Robotics (2252.HK), Harmony Kamman (2256.HK), Xianruida (6669.HK), Kangsheng Global (9960.HK), Yimai Tong (2192.HK), Tengsheng Bopharm (2137.HK), Canopy (2162.HK), Chaoyuju Eye Hospital (2219.HK), Guichuang Tongqiao (2190.HK), Hefang Medicine (0013.HK), Koji Pharmaceutical (2171.HK), Zhaoke Eye Hospital (6622.HK), Nature Pharmaceuticals (UPC.NASDAQ), Sainfo Pharmaceutical (6600.HK), Zhaoyan New Drugs (6127.HK), Novogene Health (6606.HK), Tianyan Pharmaceutical (ADAG.NASDAQ), Beikang Medical (2170.HK), Jianbimiao Miao (2161.HK), Minimally Invasive Xin Tong (2160.HK), Jiaosisi Pharmaceutical (1167.HK), HepB Pharma (2142.HK), JD Health (6618.HK), Deqi Pharmaceutical (6996.HK), Rongchang Biology (9995.HK), WuXi AppTec (2126.HK), Xiansheng Pharmaceutical (2096.HK), Yunding Newray (1952.HK), Jiahe Biology (6998.HK), Zai Ding Medicine (9688.HK), Ou Kang Weishi (1477.HK), Yongtai Biology (6978.HK), Haipure Pharmaceutical (9989.HK), Kaidao Pharmaceutical (9939.HK), Peijia Medical (9996.HK), Kangfang Biology (9926.HK), Nuo Cheng Jianhua (9969.HK), Tianjing Biology (IMAB.NASDAQ), Kanglong Chemical (3759.HK), China Antibody (3681.HK), Dongyao Pharmaceutical (1875.HK), Yasheng Medicine (6855.HK), Fuhong Hanlin (2696.HK), Hansoh Pharmaceutical (3692.HK), Mabot Pharmaceutical (2181.HK), Fangda Holdings (1521.HK), Via Biotech (1873.HK), CStone Pharmaceuticals (2616.HK), Junshi Biosciences (1877.HK), WuXi AppTec (2359.HK), Xinda Biotech (1801.HK), Hualing Medicine (2552.HK), BeiGene (6160.HK), Gilead Sciences (1672.HK), WuXi AppTec (2269.HK), China Resources Medicine (3320.HK), Yakugen Scientific Research Pharmaceutical (2633.HK), Hefang China Medicine (HCM.NASDAQ), Biotechnology (1548.HK), BBI Life Sciences (1035.HK), Tongyuan Kang Medicine (2410.HK), etc. In terms of the number of filings, the Frost & Sullivan healthcare team maintains an absolute leading position in Hong Kong's healthcare IPO market, consistently ranking first in market share from 2018 to 2023.

Since the listing of the first batch of companies on the Sci-tech Innovation Board in July 2019, Frost & Sullivan reports have been widely cited in the prospectuses of leading Sci-tech Innovation Board listed companies in the industry. These include: Hanbang Technology (688755.SH), Zhongyan Shares (688716.SH), Optics Technology Group Co., Ltd. (688450.SH), Jinghe Integration (688249.SH), Wuxi Rilian (688531.SH), Maolai Optics (688502.SH), Kangwe Century (688426.SH), Jinkang Protein (688137.SH), Novogene Biologics (688428.SH), Aopuima Biotechnology Co., Ltd. (688293.SH), MicroPort Neurosurgery (688351.SH), Mengke Pharmaceutical Co., Ltd. (688373.SH), Yifang Biotechnology Co., Ltd. (688382.SH), Jicui Pharmaceutical (688046.SH), Haichuang Pharmaceutical Co., Ltd. (688302.SH), Rongchang Biotechnology (688331.SH), Rendu Biotechnology (688193.SH), Shouyao Holdings (688197.SH), Heyuan Biotechnology Co., Ltd. (688238.SH), Yaxin Security (688225.SH), Xidi Microelectronics (688173.SH), Mawei Biotechnology Co., Ltd. (688062.SH), Yahong Medicine (688176.SH), BeiGene (688235.SH), CHERA Pharma (688246.SH), Dizhe Pharma (688192.SH), Novogene (688105.SH), Chengda Biotechnology (688739.SH), Geke Microelectronics (688728.SH), Huaxi Biotechnology (688363.SH), Junshi Biosciences (688180.SH), Zhejiang Oncology Pharmaceuticals (688266.SH), BeiGene (688177.SH), Shenzhou Cells (688520.SH), etc., are considered to be one of the most powerful, professional, and influential industry research institutions in the sector. We hope to work with enterprises to understand industry trends, seize development opportunities, jointly promote innovation and upgrading of China's big health industry, and build a healthy future.

Recommended Reading

Frost & Sullivan assists VantageV in successfully listing on the Hong Kong Stock Exchange (9887.HK)

Frost & Sullivan helps Dukang Vision Cloud successfully go public in Hong Kong (2592.HK)

Frost & Sullivan helps Mirae achieve successful listing on the Hong Kong Stock Exchange (2629.HK)

Frost & Sullivan helps Health Road successfully go public in Hong Kong (2587.HK)

Frost & Sullivan assisted Yipui Sunshine to successfully go public in Hong Kong (2522.HK)

Frost & Sullivan assists Tsuen Shin Bio to successfully go public in Hong Kong (2509.HK)

Frost & Sullivan Eastsoft in motherboard listed(9686.HK)

Frost & Sullivan assisted Yuzhiyou in successfully going public in Hong Kong (2496.HK)

Frost & Sullivan helps Yiming Angke successfully go public in Hong Kong (1541.HK)

Frost & Sullivan assists Lüzhoubio in successfully listing on the Hong Kong Stock Exchange (2480.HK)

Frost & Sullivan helps MesHealth successfully go public in Hong Kong (2415.HK)

Frost & Sullivan assists Zhongjin Medical in successfully going public in the US (NASDAQ: ZJYL)

Frost & Sullivan assists Meiliyuan in successfully listing on the Hong Kong Stock Exchange (2373.HK)

Frost & Sullivan helps Thundersoft successfully go public in Hong Kong (1244.HK)

Frost & Sullivan assists Lepucent in successfully listing on the Hong Kong Stock Exchange (2291.HK)

Frost & Sullivan helps Bio-TheraPlex successfully list on the Hong Kong Stock Exchange (2315.HK)

Frost & Sullivan helps Zhiyun Health successfully go public in Hong Kong (9955.HK)

Frost & Sullivan assists MeinGene in successfully listing on the Hong Kong Stock Exchange (6667.HK)

Frost & Sullivan assists Prenetics in successfully going public on the NASDAQ (NASDAQ:PRE)

Frost & Sullivan assists Kaleido in successfully listing on the Hong Kong Stock Exchange (6821.HK)

Frost & Sullivan helps Gushengtang successfully go public in Hong Kong (2273.HK)

Frost & Sullivan helps minimally invasive robots successfully go public in Hong Kong2252.HK)

Frost & Sullivan assists Conocoalt in successfully listing on the Hong Kong Stock Exchange (2162.HK)

Frost & Sullivan assists Nature Pharma in successfully going public in the US (NASDAQ):UPC)

Frost & Sullivan helps Jianbaimiao Miao successfully go public in Hong Kong (2161.HK)

Frost & Sullivan helps JD Health successfully go public in Hong Kong (6618.HK)

Frost & Sullivan assists Oculent in successfully listing on the Hong Kong Stock Exchange (1477.HK)

Frost & Sullivan helps develop PharmaCure successfully go public in Hong Kong (9939.HK)

Frost & Sullivan assisted Tianjing BIO in successfully going public on the NASDAQ (NASDAQ:IMAB)

Frost & Sullivan assists ViaBio in successfully listing on the Hong Kong Stock Exchange (1873.HK)

Frost & Sullivan helps Cornerstone Pharmaceuticals successfully go public in Hong Kong (2616.HK)

Frost & Sullivan helps WuXi AppTec successfully go public in Hong Kong (2359.HK)

Frost & Sullivan helps BeiGene successfully go public in Hong Kong (6160.HK)

Frost & Sullivan helps WuXi AppTec Biologics successfully go public in Hong Kong (2269.HK)

Frost & Sullivan assisted Hua Huang China Medicine in successfully going public on the NASDAQ (HCM)

*The above order is not sequential and is arranged in reverse chronological order based on listing time.