Frost & Sullivan

Ten-League International Holdings Limited (stock code: Nasdaq: TLIH) successfully listed on the US NASDAQ on July 8, 2025. The company is from Singapore and operates as a turnkey engineering solutions provider. Its main businesses include: sales of heavy equipment and parts, leasing of heavy equipment, and providing engineering consulting services for ports, construction, civil engineering, and underground infrastructure industries. The equipment provided by the company is divided into four categories based on function and application scenarios: foundation engineering equipment, lifting equipment, excavation equipment, and port machinery. In addition, the company also provides value-added engineering solutions through engineering consulting services, aiming to solve potential safety problems, improve reliability and production efficiency, and help customers evaluate equipment performance, project quality, and project progress. Frost & Sullivan (hereinafter referred to as "Frost & Sullivan") provides exclusive industry advisory services for Ten-League International Holdings Limited's listing on the US market, and hereby warmly congratulates them on their successful listing.

Ten-League International Holdings Limited (hereinafter referred to as "Ten League") successfully listed on July 8, 2025, issuing 1.60784 million shares at a price of $4 per share, raising $6.43 million.

During this listing process in the US, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business, and other important chapters), helping the issuer communicate with the SEC and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the issuer in completing feedback from regulatory authorities on various industry issues.

PART/1

Heavy Equipment Market Overview

Definition and Classification

Heavy equipment refers to heavy vehicles specifically designed for performing specific tasks. Heavy equipment usually includes five equipment systems: working device, traction, structure, power transmission, and control/information.

Construction engineering equipment refers to tools and machinery used in projects including civil, construction, electrical, and mechanical (E&M) as well as maintenance, repair, renovation, and addition (RMAA) projects. Examples of construction machinery and equipment include but are not limited to: (i) Drills, a comprehensive system for drilling underground holes for pile driving or other construction purposes, or drilling wells or oil wells; (ii) crawler and mobile cranes designed for convenient transportation, lifting, and moving heavy objects; (iii) Excavators used for excavation purposes, moving large amounts of materials (such as rocks and soil) and performing various lifting and handling tasks in various applications; (iv) Wheel loaders, used for excavation, transportation, handling, and transportation, participating in road construction, preparation sites, and assisting in cleaning after projects are completed.

Port equipment refers to machinery and other equipment used for loading and unloading passengers and cargo. Examples include but are not limited to: (i) Stackers, used for handling multimodal container traffic at small or medium-sized ports; (ii) Empty container stackers, used for transporting empty containers with different tonnage lifting capabilities; (iii) Forklifts, industrial power vehicles used for short-distance lifting and moving small materials.

Market Size

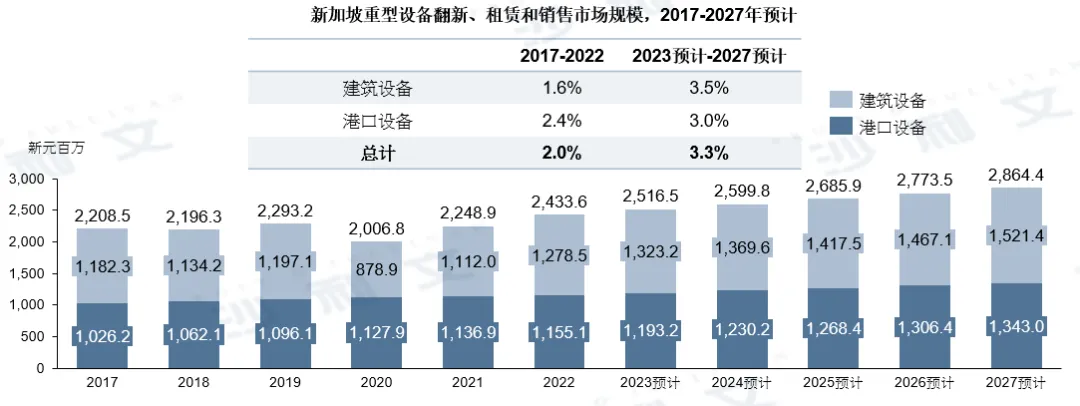

The market size of heavy equipment renovation, leasing, and sales moderately increased from S$22.085 billion in 2017 to S$24.336 billion in 2022, with a compound annual growth rate of 2.0%. In particular, due to the outbreak of the COVID-19 pandemic in 2020, the market size of construction equipment was suppressed, leading to a halt in construction activities that year. In the port equipment sector, the market size grew at a compound annual growth rate of 2.4% from 2017 to 2022, thanks to the continuous growth in container port traffic over the past few years and favorable policy support for promoting heavy equipment upgrades, replacements, and renovations to improve operational efficiency.

Looking ahead, given the strong investment commitments of real estate developers and the government in Singapore's strong economic foundation, combined with expected stable port traffic, goods, and commodity trade, the market size of heavy equipment renovation, leasing, and sales in Singapore is expected to reach S$28.644 billion in 2027, with a compound annual growth rate of about 3.3% from 2023 to 2027.

Source: Frost & Sullivan report

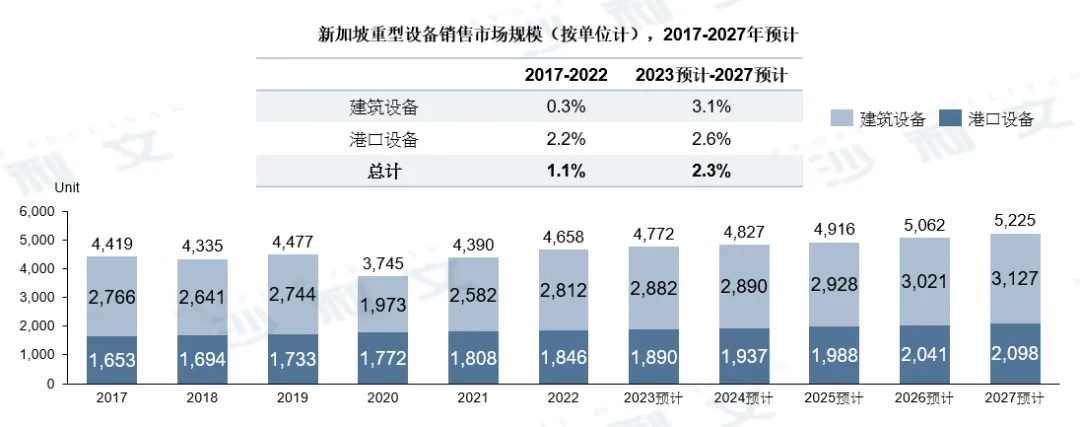

The sales of construction equipment and port equipment per unit refer to the sales of all types of equipment, including large construction equipment (such as excavators and bulldozers) and large port equipment (such as forklifts and loaders), as well as small equipment. The sales unit of construction equipment steadily increased from 2,766 units in 2017 to 2,812 units in 2022, with a compound annual growth rate of about 0.3%. It is expected to grow at a compound annual growth rate of 3.1% from 2023 to 2027. The sales unit of port equipment steadily increased from 1,653 units in 2017 to 1,846 units in 2022, with a compound annual growth rate of about 2.2%. It is expected to grow at a compound annual growth rate of 2.6% from 2023 to 2027.

Source: Frost & Sullivan report

Market Drivers and Opportunities

●Government Support for the Construction Industry

In order to encourage the construction industry, the Singapore Building Authority (BCA) launched an investment allowance scheme in 2021, providing tax relief for beneficial construction equipment, aiming to improve productivity in the industry by accelerating mechanization. The scheme allows enterprises to deduct up to 50% of their approved fixed capital expenditures (for construction equipment and machinery) from their taxable income, reducing the burden on construction companies to purchase or lease the machinery and equipment required to expand service capabilities and capacity. In addition, the Singapore Housing Development Board (HDB) has been increasing the supply of build-to-order (BTO) apartments. In 2022 and 2023, the HDB increased the construction volume of BTO apartments by 35%, reaching about 23,000 units per year, a significant increase compared to 17,100 units in 2021. The completion of residential units and surrounding auxiliary infrastructure (such as public transportation systems) is expected to stimulate demand for construction machinery use. The collective efforts of these government initiatives are expected to increase the leasing and sales of construction machinery and equipment, both in terms of frequency of use and investment.

●Urban Development Demand Surge

According to the forecast of the Singapore Building Authority (BCA), future construction projects in the private and public sectors will increase, with the total value of construction contracts exceeding S$298 billion in 2022. The BCA expects that the total value of construction contracts awarded in 2023 will be between S$27 billion and S$32 billion. This strong demand is due to the continuous strong supply of public housing projects, subway line construction, and other infrastructure projects. The strong construction demand for infrastructure and buildings in the next few years is expected to drive the leasing, sales, and renovation of heavy equipment in Singapore.

●Electrification of Port Equipment

The electrification and automation of port equipment are becoming increasingly popular in the market because environmental protection has become a common goal for both the country and the Singapore government. The Singapore government actively supports relevant environmental protection operation proposals through regulations, financial support, and tax relief. The Port Authority of Singapore (PSA) is one of the pioneers in adopting electric vehicles to promote large-scale applications. In particular, the PSA has partnered with Hyundai Motor Group to start jointly developing the production, implementation, and deployment of electric vehicles in Singapore. In addition, significant progress in battery performance and cost, global and local environmental issues, and better and more accessible charging technologies have also driven the shift from diesel equipment to electrification equipment. Therefore, many leading port equipment manufacturers and ports are actively purchasing electric equipment. Manufacturers and port logistics companies are continuously accelerating the introduction of new technologies to achieve national net-zero emission goals and carbon neutrality, while improving the maneuverability and driving performance of equipment. This transformation is expected to bring opportunities for new equipment purchases and machinery replacements, thereby driving the development of the port equipment sales market.

●New Port Construction

At the end of 2022, the new generation container terminal - Dass Terminal - built by the Singapore Maritime and Port Authority was officially commissioned. The Dass Terminal has a handling capacity of 6,500 TEUs, twice that of 3,750 TEUs in 2021, covering active commercial and industrial areas in the western region such as Yuen Long Lake District, Yuen Long Innovation District, and Dass Industrial Area. In addition, artificial intelligence and automation technologies are integrated into the operation of the new port, using flexible and highly mobile electrified automated yard cranes and automated guided vehicles (AGVs) to transport containers between yards and terminals. Therefore, with Singapore's active development in port facilities and locations, the demand for port equipment is growing.

●Technology Integration into Machinery and Operations

The Internet of Things (IoT) and data analysis are advanced, computerized, and digital technologies that are increasingly being adopted in the construction and port equipment industries because these technologies provide extensive help in improving operational efficiency and achieving business sustainability. Due to the limited space and labor shortage in the construction and port operation industries in Singapore, highly complex technologies such as artificial intelligence and computer vision have become key development directions in recent years. The government plans to increase manufacturing productivity by 50% by 2030. The government has established a Global Innovation Alliance that allows local technology and manufacturing companies to cooperate with global manufacturers to improve productivity through technological collaboration in Singapore.

●The Rise of Environmental Protection Awareness

Essentially, pollutants emitted by heavy equipment significantly exacerbate air pollution by releasing carbon monoxide, hydrocarbons, nitrogen oxides, and particulate matter. Therefore, environmental protection continues to receive attention in the heavy equipment industry. Contractors and port logistics companies are increasingly using more environmentally friendly equipment and strategies to reduce emissions of various pollutants. With the continuous enhancement of environmental protection awareness, it is expected that this trend will continue in the near future. Some measures include using high-quality power machinery and equipment at construction sites, using the driven-in method for silent pile driving to reduce noise and vibration impacts; replacing handheld impact crushers with blasting systems.

●The Growth in Machinery Leasing and Renovation Demand

Due to the high costs of purchasing and maintaining heavy construction equipment, many construction service providers in Singapore generally adopt a light-asset model, choosing to lease equipment rather than purchase, and using renovated equipment rather than new equipment has become common practice. Cost issues have increased the motivation of contractors to lease and use renovated equipment, thereby driving the development of the leasing market.

Click on the end of the article

Read the original article

View the complete prospectus

Frost & Sullivan has rich research experience in the construction industry and has assisted well-known enterprises to successfully list on the capital market. Successful listing cases include: Rongli Construction (9639.HK), Hongji Group (2535.HK), Zhongshen Jianye (2503.HK), Shanxi Installation (2520.HK), Yijun Group (2442.HK), Zhongtian Hunan Group (2433.HK), GC Construction (1489.HK), Fengcheng Holdings (2295.HK), Yinghui Holdings (2195.HK), Zhixin Group (2187.HK), Guanglian Engineering (1413.HK), Dehe Group (0368.HK), Raffles Interior (1376.HK), Xinwei Engineering (8676.HK), Yinglan Group (1162.HK), Jianzhong Construction (0589.HK), Shengxing Holdings (1472.HK), Weny Group (1802.HK), Deyi Holdings (9900.HK), Tailin Construction (6193.HK), Fengcheng Holdings (8216.HK), WMCH Global (8208.HK), Huaji Global (2296.HK), Wanya Holdings (8173.HK), China Tianbao (1427.HK), Beng Soon (1987.HK), Far East Construction (2163.HK), Anle Engineering (1977.HK), Kun Group (924.HK), Pujiang International (2060.HK), Lejia Holdings (1867.HK), Weihong Group Holdings (8522.HK), Pipeline Engineering (1865.HK), Hon Corp (8259.HK), Hengyi Holdings (1894.HK), Bao Yan Holdings (8601.HK), Aobang Construction (1615.HK), Renhe Technology (8140.HK), Wanshun Group (1746.HK), Liang Zhitian (2262.HK), Tangji (8305.HK), Rongfeng Group Asia (8526.HK), Deyi Holdings (8522.HK), Aoneng Construction (1183.HK), Yingde Holdings (8535.HK), Hengyu Group (2448.HK), WT Group (8422.HK), Jianpeng Holdings (1722.HK), Hebei Construction (1727.HK), Shouyi Holdings (2227.HK), Yinglan Group (8470.HK), Yikang Tai (8445.HK), Wantong Garden (8199.HK), Haobo International (8431.HK), Progressive Development (1667.HK), Yongmian Development (8423.HK), ECI Technology (8013.HK), Shanle International (1660.HK), Li's Enterprise Holdings (2266.HK), Aisuo Holdings (8341.HK), Aidev Construction (6189.HK), Kuangwenji (8023.HK), Fengsheng Electromechanical (0331.HK), Kono Verde (1206.HK), Hongxing · Makelion (1528.HK), Tianjin Construction Development (2515.HK).

Recommended Reading (scroll up and down for more)

Frost & Sullivan helps Rongli Ying successfully list on the Hong Kong stock market (9639.HK)

Frost & Sullivan helps Hongji Group successfully list on the Hong Kong stock market (2535.HK)

Frost & Sullivan helps Zhongshen Jianye successfully list on the Hong Kong stock market (2503.HK)

Frost & Sullivan helps Shanxi Installation successfully list on the Hong Kong stock market (2520.HK)

Frost & Sullivan helps Yijun Group successfully list on the Hong Kong stock market (2442.HK)

Frost & Sullivan helps GC Construction successfully list on the Hong Kong stock market (1489.HK)

Frost & Sullivan helps Yinghui Holdings successfully list on the Hong Kong stock market (2195.HK)

Frost & Sullivan helps Zhixin Group successfully list on the Hong Kong stock market (2187.HK)

Frost & Sullivan helps Dehe Group successfully list on the Hong Kong stock market (0368.HK)

Frost & Sullivan helps Raffles Interior successfully list on the Hong Kong stock market (1376.HK)

Frost & Sullivan helps Xinwei Engineering successfully list on the Hong Kong stock market (8676.HK)

Frost & Sullivan helps Yinglan Group successfully list on the Hong Kong stock market (1162.HK)