Hainan Junda New Energy Technology Co., Ltd. (Stock Code: 2865.HK) successfully listed on the main board of the Hong Kong capital market on May 8, 2025. The company is a leading professional photovoltaic cell manufacturer in the industry, dedicated to the research, development, production, and sales of high-efficiency photovoltaic cells. Frost & Sullivan (hereinafter referred to as "Frost & Sullivan") provided exclusive industry advisory services for the listing of Hainan Junda New Energy Technology Co., Ltd., and hereby warmly congratulate them on their successful listing.

Hainan Junda New Energy Technology Co., Ltd. (hereinafter referred to as "Hainan Junda") successfully listed on May 8, 2024. In this IPO, the company issued a total of 63,432,300 H shares, of which 90% were international offerings and 10% were public offerings. The maximum offering price per share was HK$28.6, and the net raised funds were approximately HK$1.434 billion.

During the process of listing in Hong Kong, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing the writing of relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business, and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange.

According to LiveReport's big data (statistical data as of April 3, 2025), in the first quarter of 2025, as well as during the past 12 and 36-month statistical periods, Frost & Sullivan provided listing industry advisory services for 11 (73%), 47 (64%), and 147 (68%) Hong Kong stock IPOs, respectively, possessing rich industry experience and communication experience with exchanges and investors.

PART/1

Investment Highlights

-

Among professional manufacturers, the company's N-type TOPCon battery shipments rank first globally;

-

Among professional manufacturers, the company's photovoltaic cell shipments rank second globally;

-

In the global photovoltaic cell industry, among professional and integrated manufacturers, the company's N-type TOPCon battery market share is about 7.5%, and its photovoltaic cell market share is about 5.6%.

PART/2

Global Renewable Energy Power Generation Market Overview

Addressing climate change has gradually become a global common goal, and renewable energy plays a crucial role in addressing climate change. Countries around the world are implementing policies and initiatives to prioritize the development of renewable energy in order to achieve carbon neutrality.

Compared with other renewable energy sources, solar power generation has multiple advantages such as being applicable to various scales (from small residential installations to large public utility projects), having a wide range of resource sources, and minimal geographical limitations. In addition, solar power generation has a high commercial maturity, stable power generation, and low cost. These advantageous factors have laid the foundation for the rapid growth of solar energy as a renewable energy source.

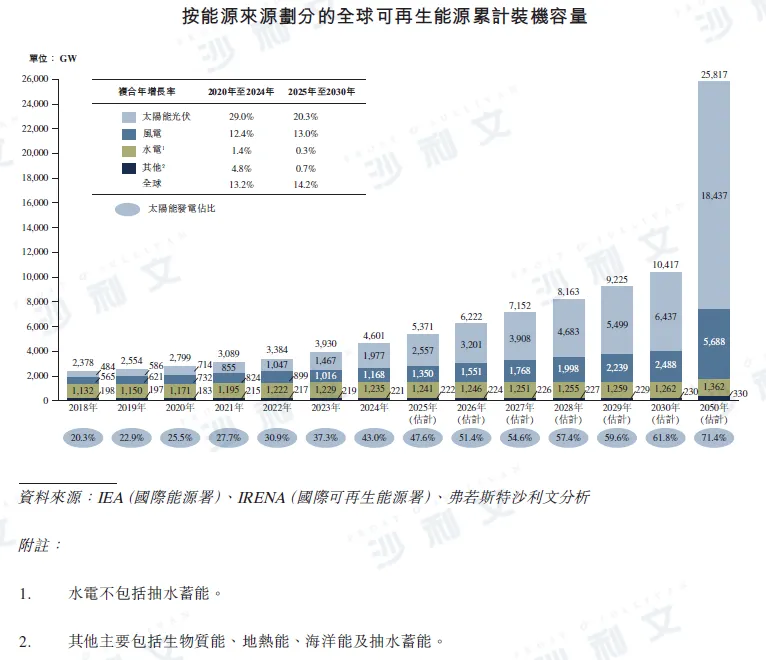

From 2020 to 2024, in terms of the cumulative installed capacity of global renewable energy, the market scale of global renewable energy power generation increased from 2,799.0 GW to 4,600.5 GW, with a compound annual growth rate of 13.2%. With the advancement of clean energy transformation, it is expected that the cumulative installed capacity of global renewable energy will reach 10,416.8 GW by 2030, with a compound annual growth rate of 14.2% from 2025 to 2030, among which the growth rate of solar power generation is faster than that of other major renewable energy sources. By 2050, it is expected that the cumulative installed capacity of global renewable energy will be nearly six times higher than the level in 2024.

PART/3

Global Photovoltaic Cell Market Overview

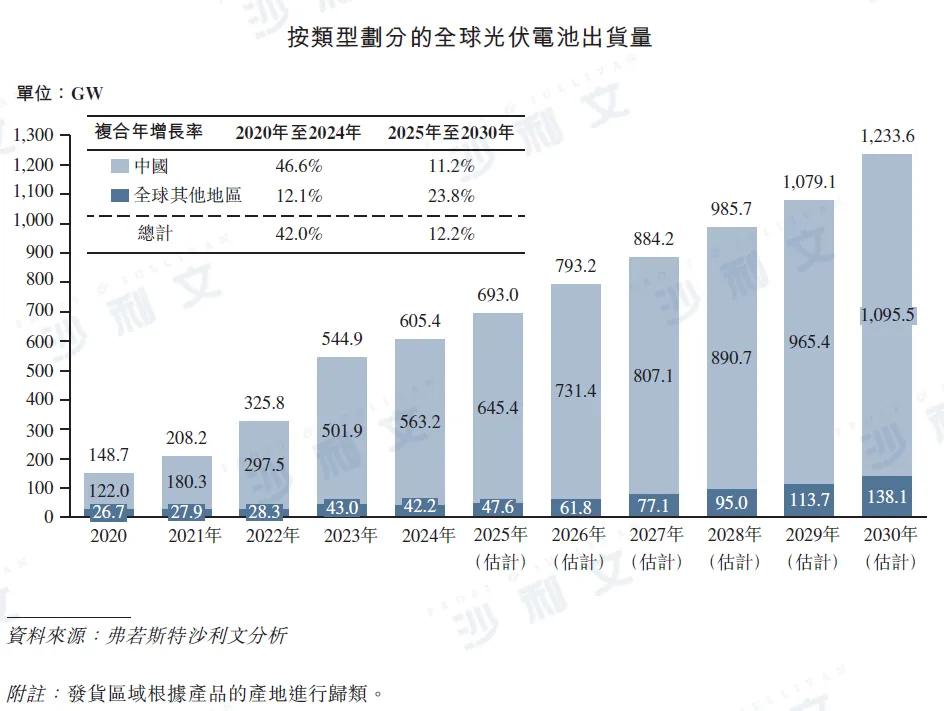

The global carbon neutrality goal and energy transformation strategy have driven the rapid growth of photovoltaic cell demand. Therefore, in 2024, the market scale of global photovoltaic cells reached 605.4 GW in terms of shipments. The global demand for renewable energy, mainly represented by solar energy, continues to grow steadily. In addition, with technological progress and cost reduction, solar energy has become the most competitive energy source for more and more countries. Therefore, it is expected that the global photovoltaic market will maintain rapid growth and continue to drive the expansion of the photovoltaic cell market. It is expected that by 2030, the global photovoltaic cell shipments will reach 1,233.6 GW, with a compound annual growth rate of 12.2% from 2025 to 2030.

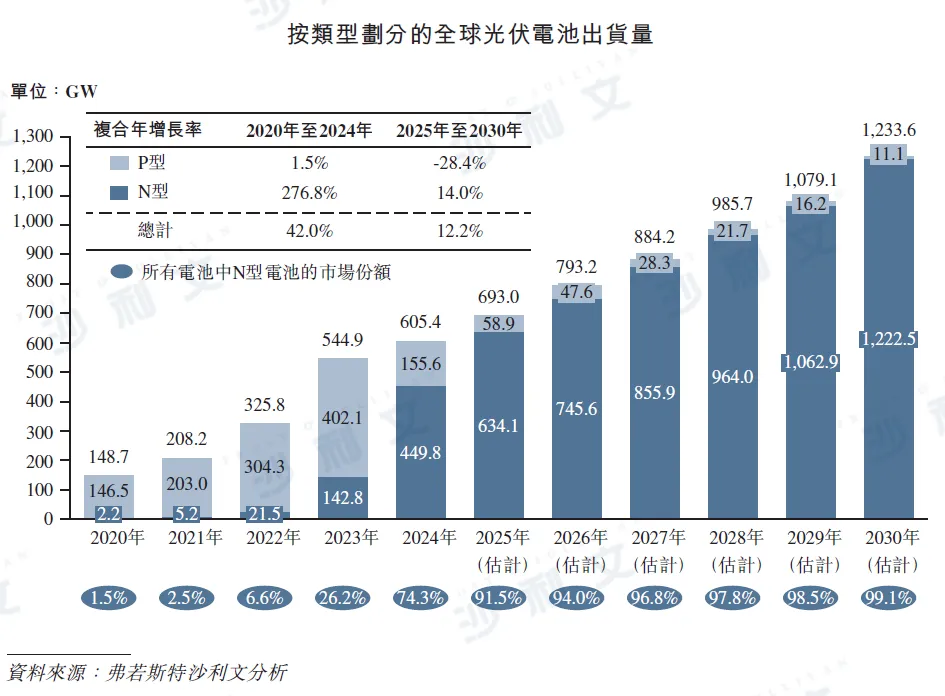

Due to mature technology and lower manufacturing costs compared to other types of photovoltaic cells, P-type PERC cells have been the mainstream technology in the photovoltaic industry for several years. However, with the continuous growth of the photovoltaic market and the efficiency of P-type PERC cells approaching theoretical limits, there are challenges in meeting the demand for cost reduction and efficiency improvement in solar power generation. Therefore, in order to seek new breakthroughs in the industry, leading market participants are focusing on N-type cells, and both the production volume and market penetration rate of N-type cells have risen rapidly. In 2024, the market share of N-type cells reached 74.3%.

PART/4

Photovoltaic Cell Market Drivers

● Carbon Neutrality and Energy Security Issues

Given the good adaptability, resource availability, commercial maturity, and stability of solar energy, it is becoming increasingly important in achieving global carbon neutrality and national energy security. Driven by these advantages, the global cumulative installed capacity of solar power generation exceeded hydropower in 2023, is expected to exceed natural gas in 2026, exceed coal-fired power generation in 2027, and by 2050, solar power generation will account for about 50% of the global cumulative installed capacity. The Chinese government has promised to increase the proportion of non-fossil fuels in primary energy consumption to about 25% by 2030, and the cumulative installed capacity of solar and wind power generation will exceed 1,200 GW. These goals reflect China's determination to promote renewable energy in its energy transformation focusing on solar energy.

● Economic Feasibility, Technological Progress, and Large-scale Mass Production

Technological progress has greatly improved the conversion efficiency of photovoltaic cells, reduced the cost of photovoltaic power generation, achieved grid parity, and made solar power generation economically attractive. Photovoltaic cell manufacturers have made significant progress in developing high-efficiency N-type photovoltaic cells (such as N-type TOPCon cells and HJT cells). Even a 1% increase in power conversion efficiency can reduce the power generation cost by 5% to 7%. The above progress of high-efficiency photovoltaic cells, combined with large-scale mass production and experience accumulation, has continuously reduced the cost of solar photovoltaic power generation by more than 85% from 2010 to 2020. Therefore, the share of global cumulative installed capacity of solar power generation is growing rapidly.

● Integrated Energy Storage Systems Provide Complementary Solutions

In the past, solar power generation and other renewable energy sources encountered difficulties in effectively utilizing the generated electricity, resulting in energy waste. Therefore, countries around the world have been actively promoting the integration of solar energy and energy storage systems to store excess electricity generated by photovoltaic systems and release it when demand exceeds system capacity. This integration helps improve the reliability and stability of photovoltaic systems by making up for the power gap between generation and consumption. In addition, energy storage systems can also achieve peak shaving, load transfer, and backup power sources, thereby improving the power consumption efficiency of photovoltaic power generation and enhancing the competitiveness of solar power generation.

Click at the end of the article

Read the original article

View the complete prospectus

Frost & Sullivan has rich research experience in the energy and power industry, assisting well-known enterprises to successfully list on the capital market. Recent successful listing cases include: Reliance Industries (NASDAQ:LSE), Reshape Energy (2570.HK), Guofu Hydrogen Energy (2582.HK), Huizhu Technology (2481.HK), Guohong Hydrogen Energy (9663.HK), Huzhou Gas (6661.HK), MingYang Smart Energy (MYSE:LI), PowerChina International (SDIC:LI), NAC Energy Technology (1597.HK), Jiaxing Gas (9908.HK), Chuncheng Thermal Power (1853.HK), CNPC Clean Energy (1759.HK), Jiutai Bangda (2798.HK), TNL Natural Gas (8536.HK), Tianbao Energy (1671.HK), Yuguang International (1621.HK), Jintai Feng (8479.HK), Zhongcheng Energy (2337.HK), Inner Mongolia Energy Engineering (1649.HK), Rescognex (1679.HK), Persta Resources (3395.HK), New Energy (1799.HK), China Energy Engineering (3996.HK), North China Energy (NASDAQ:CNEY), etc.

Recommended Reading

Frost & Sullivan helps Reliance Industries successfully list in the US (NASDAQ:LSE)

Frost & Sullivan helps Shanghai Reshape Energy successfully list in Hong Kong (2570.HK)

Frost & Sullivan helps Guofu Hydrogen Energy successfully list in Hong Kong (2582.HK)

Frost & Sullivan helps Guohong Hydrogen Energy successfully list in Hong Kong (9663.HK)

Frost & Sullivan helps Huizhu Technology successfully list in Hong Kong (2481.HK)

Frost & Sullivan helps Huzhou Gas successfully list in Hong Kong (6661.HK)

Frost & Sullivan helps North China Energy successfully list in the US (NASDAQ:CNEY)

Frost & Sullivan helps NAC Energy Technology successfully list in Hong Kong (1597.HK)

Frost & Sullivan helps Jiaxing Gas successfully list in Hong Kong (9908.HK)

Frost & Sullivan helps Chuncheng Thermal Power successfully list in Hong Kong (1853.HK)

Frost & Sullivan helps TBK & Sons successfully list in Hong Kong (1960.HK)

Frost & Sullivan helps CNPC Clean Energy successfully list in Hong Kong (1759.HK)

Frost & Sullivan helps Jiutai Bangda successfully list in Hong Kong (2798.HK)

Frost & Sullivan helps TNL Natural Gas successfully list in Hong Kong (8536.HK)

Frost & Sullivan helps Tianbao Energy successfully list in Hong Kong (1671.HK)

Frost & Sullivan helps Yuguang International successfully list in Hong Kong (1621.HK)

Frost & Sullivan helps Jintai Feng successfully list in Hong Kong (8479.HK)

Frost & Sullivan helps Zhongcheng Energy successfully list in Hong Kong (2337.HK)

Frost & Sullivan helps Inner Mongolia Energy Engineering successfully list in Hong Kong (1649.HK)

Frost & Sullivan helps Rescognex successfully list in Hong Kong (1679.HK)

Frost & Sullivan helps Persta Resources successfully list in Hong Kong (3395.HK)

Frost & Sullivan helps New Energy successfully list in Hong Kong (1799.HK)

Frost & Sullivan helps China Energy Engineering successfully list in Hong Kong (3996.HK)

*The above order is not in any particular sequence and is arranged in reverse order of listing time