Frost & Sullivan

Anjing Food Group Co., Ltd. (Stock Code: 2648.HK) successfully listed on the Main Board of the Hong Kong capital market on July 4, 2025. The company is a leading enterprise in China's frozen food industry, dedicated to providing food in various consumption scenarios such as home, restaurants, and dining out. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') has provided exclusive industry advisory services for the listing of Anjing Food Group Co., Ltd., and hereby warmly congratulates them on their successful listing.

Anji Group Co., Ltd. (hereinafter referred to as 'Anji') successfully listed on July 4, 2025. The company plans to issue 3,999.47 million H shares, of which 90% will be international offerings and 10% will be public offerings. The maximum offering price per share is HK$66.00, raising a net amount of approximately HK$2.64 billion.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support and highlight the issuer's competitive advantages, assisting the issuer, investment banks and other intermediaries in completing the writing of relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and providing assistance to the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

According to LiveReport's big data (statistical data as of June 30, 2025), from January to June 2025, as well as during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 29 (71%), 52 (market share 64%), and 161 (market share 69%) Hong Kong-listed IPOs respectively, boasting rich industry experience and communication skills with exchanges and investors.

PART/1

Investment Highlights

-

China's largest frozen food company;

-

A nationwide sales network that covers the entire region, across all channels, and penetrates deeply;

-

A cross-category diversified product portfolio centered on big products;

-

The combination of real estate sales and centralized production, along with the economies of scale, brings cost advantages;

-

Advanced digital capabilities enhance scientific decision-making and operational efficiency across the entire process;

-

A visionary and experienced management team, as well as a proactive corporate culture.

According to the Frost & Sullivan report, in terms of revenue for 2024:

-

Ranked first in China's frozen food industry;

-

Ranked first in China's frozen prepared food industry;

-

Ranked first in the Chinese frozen dish products industry;

-

It ranks fourth in the Chinese frozen noodle and rice product industry; however, in terms of revenue from emerging frozen noodle and rice products (excluding traditional ones such as dumplings, tangyuan, and zongzi), it ranks first.

PART/2

Overview of the Global Frozen Food Industry

Frozen foods refer to pre-packaged foods designed specifically for dining scenarios, which are made primarily from aquatic ingredients, meat, grains, powdered seasonings, beans, etc., with auxiliary materials such as water, oil, and condiments. The freezing process can rapidly reduce the thermal center temperature of the food to below -18°C. Frozen foods should be stored, transported, and sold at this temperature.

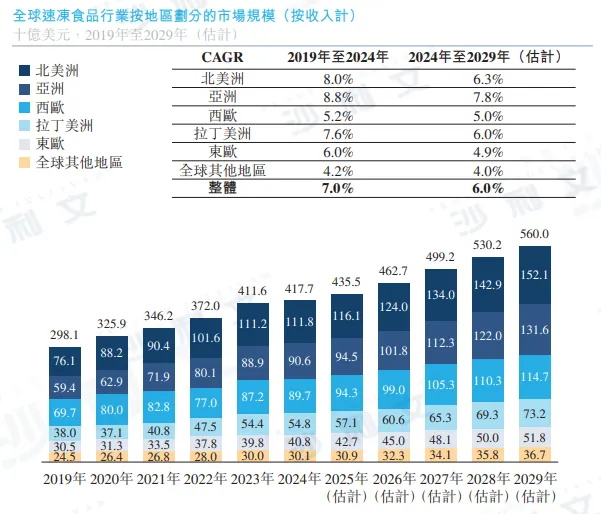

In recent years, the global frozen food industry has achieved significant growth on a solid foundation. From 2019 to 2024, the market size of the global frozen food industry grew at a compound annual growth rate (CAGR) of 7.0%, reaching $417.7 billion in 2024. Looking ahead, driven by factors such as increased customer penetration, product category expansion, technological progress, and improved infrastructure, the global frozen food industry is expected to continue growing steadily. From 2024 to 2029, the CAGR of the global frozen food industry is expected to reach 6.0%. In terms of regional scale, North America, Asia, and Western Europe are the regions with the largest market size for the global frozen food industry. In 2024, the market size of frozen food in Asia reached $90.6 billion and is expected to lead all regional markets with a CAGR of 7.8% over the next five years.

Source: World Bank, Frost & Sullivan analysis

PART/3

Overview of China's Frozen Food Industry

China's frozen foods mainly include frozen prepared foods, frozen dishes, frozen pasta and rice products, as well as other categories such as frozen soups and pastries.

-

Frozen prepared foods. Frozen prepared foods refer to pre-packaged foods that are produced using aquatic ingredients and/or meat as the main raw materials, combined with other raw materials such as grains, beans, and eggs, along with seasonings. They are processed into shapes through mixing, cooking, and then frozen using certain techniques.

-

Frozen dish products. Frozen dish products refer to pre-packaged dish products made primarily from aquatic ingredients and/or meat, with other ingredients and seasonings added, through pre-processing (such as cutting, stirring, marinating, rolling, shaping, and seasoning) and/or pre-cooking (such as frying, deep-frying, roasting, boiling, or steaming), followed by freezing. Frozen dish products mainly include semi-finished and finished dishes that still require heating and cooking before consumption.

-

Frozen noodle and rice products. Frozen noodle and rice products refer to pre-packaged foods made primarily from grains such as wheat, rice, corn, and other cereal products, along with other raw materials and seasonings. They are processed through pre-cooking and freezing techniques.

PART/4

The market scale of China's frozen food industry

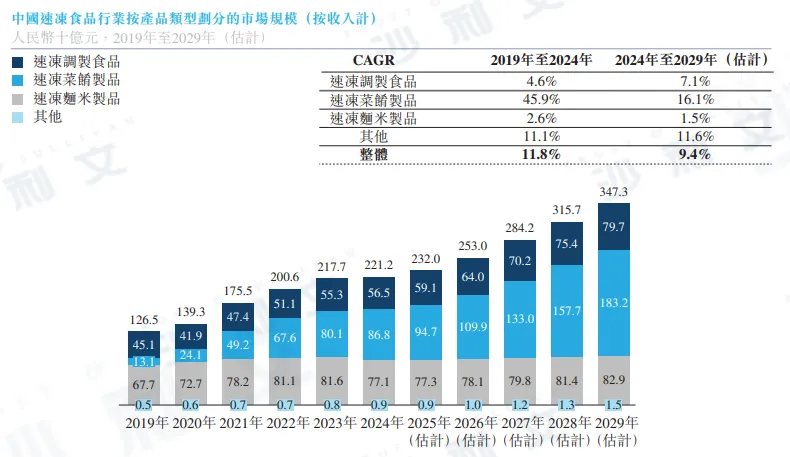

Compared to mature markets such as Japan and the United States where the frozen food industry has developed, China's frozen food industry is still in its growth phase. From 2019 to 2024, the industry experienced rapid growth with a CAGR of 11.8%, reaching 2212 billion yuan in 2024. Driven by multiple factors such as increased demand for catering services, higher penetration rates among individual customers leading to increased household consumption, improved product quality and nutrition, and enhanced cold chain infrastructure, China's frozen food industry will continue to expand. The CAGR of the industry from 2024 to 2029 is expected to reach 9.4%, with growth expected to exceed other catering-related industries (such as staple foods, snacks, oils, condiments, and liquid milk), indicating strong growth potential. In terms of revenue in 2024, frozen food accounts for more than 20% of the packaged food market. Packaged foods refer to products pre-packaged in specific quantities and made in specific materials and containers, mainly including ready-to-eat foods, ready-to-heat foods, ready-to-cook foods, and ready-to-serve foods.

Data source: National Bureau of Statistics, Frost & Sullivan analysis

PART/5

Driving Forces of China's Frozen Food Industry

●The share of chain restaurants in the Chinese catering market is continuously increasing.

The proportion of chain restaurants in China's catering industry rose from 13.3% in 2019 to 22.0% in 2024. This proportion is still lower than that of mature markets (about 55% in the United States and about 50% in Japan), and it is expected to continue rising. These chain restaurants include a variety of Chinese dining forms such as hot pot, spicy hot pot, and barbecue, all of which generate a large demand for standardized and pre-prepared ingredients. Frozen food companies can provide high-quality products to ensure consistency in flavors across multiple locations, thus well meeting the needs of these chain restaurants. In addition, with the recovery and improvement of offline consumption scenarios, China's catering industry achieved stable growth in 2024. In 2024, the market scale reached RMB 5,571.8 billion in terms of revenue, with a CAGR of 3.6% from 2019 to 2024. It is expected that China's catering industry will continue to expand in the future, thereby driving growth in China's demand for frozen food.

●Group meal services strive for standardization, quality, and efficiency.

The market scale of the group meal market in 2024 is RMB 2,067.1 billion, characterized by suppliers mainly providing meals and services in group settings. The market has developed rapidly in recent years, with an expected CAGR of 9.1% from 2024 to 2029. The group meal industry requires high levels of standardization and quality assurance, especially in terms of food safety, quality stability, and operational efficiency, which align with the characteristics of frozen foods. Therefore, it is expected that the frozen food industry will significantly benefit from the expansion of the group meal market.

●Western cuisine growth

In 2024, the scale of China's Western-style catering market reached RMB 917.5 billion, accounting for 16.5% of the overall catering market. From 2024 to 2029, the CAGR of this market is expected to reach 9.8%, exceeding that of the overall Chinese catering market. The growth drivers include the localization of Western dishes, diversified menu choices, and expansion into lower-tier cities. In addition, compared to Chinese catering, the simpler cooking methods of Western cuisine make the production of frozen foods easier to standardize, achieving consistent quality and taste. Therefore, the widespread use of frozen foods in Western cuisine has driven the growth of the frozen food industry.

●The penetration rate of individual customers in household consumption scenarios continues to rise.

Frozen foods provide great convenience and variety, effectively solving the time constraints faced by family customers in an increasingly fast-paced lifestyle. The increase in disposable income further supports the growing demand. China's per capita disposable income increased from RMB 30,733 in 2019 to RMB 41,314 in 2024, with a CAGR of 6.1%. With the improvement in purchasing power, customers are pursuing more diverse, higher-quality, convenient, and delicious options. Due to the simplicity and convenience of cooking, frozen foods are increasingly penetrating households and becoming an indispensable part of daily life.

●Upgrade cold chain infrastructure to lay a solid foundation

Driven by improvements in the supply side (including raw material supply), technological advancements, and the development of cold chain infrastructure, China's frozen food industry has experienced stable growth. China is the largest pork producer and also a major producer of livestock and poultry meat, aquatic products, ensuring a stable and sufficient supply of raw materials for frozen food production. With the development of automation and intelligent technologies, improved processing efficiency enables frozen food companies to quickly respond to changing market demands. The expansion of cold chain infrastructure, especially refrigerated trucks, has laid a solid foundation for the development of the frozen food industry. From 2019 to 2024, the number of refrigerated trucks increased from 215,000 to 495,000, supporting industry growth. This infrastructure upgrade has promoted the expansion of the cold chain logistics market, increasing from RMB 339 billion in 2019 to RMB 536 billion in 2024, with a CAGR of 9.6%. The strengthening of cold chain infrastructure has improved transportation efficiency, reduced product losses, and established a more reliable distribution network. Therefore, improvements in the supply side have led to increased efficiency and operational costs for frozen food companies, thereby providing end customers with more affordable products. At the same time, improved efficiency and the expansion of distribution networks have also expanded product variety and accessibility, providing customers with more choices and further promoting the development of the frozen food industry.

PART/6

Future industry opportunities

●Industry integration is expected to accelerate.

With the diversification of customer needs and intensified market competition, coupled with the encouragement of mergers and acquisitions policies and the emergence of acquisition opportunities, the integration of the frozen food industry is expected to accelerate. In the past five years, the market share of the top five companies in the frozen prepared food industry has increased from about 17% in 2019 to 22% in 2024. Companies that rely on a single sales channel or product category may face growth constraints and struggle to meet the increasingly diverse needs of customers. In contrast, companies with a diversified product portfolio and omnichannel strategies will be able to further expand. Such companies possess strong supply chain integration capabilities, innovation capabilities, and extensive market coverage, enabling them to better respond to market changes and leverage synergies between products and channels to enhance overall competitiveness.

●Expanded to global markets

The global frozen food industry is at different stages of development in different countries. With the continuous growth of global demand for frozen food, the internationalization of Chinese frozen food provides an important opportunity for future expansion. This transformation reflects the growing global demand for convenient and high-quality frozen food, enabling Chinese enterprises to enter international markets and further promoting the development of the global industry.

●Diversified consumption scenarios

The frozen food industry is undergoing transformation and expanding continuously in different consumer scenarios. In addition to traditional households and restaurants, venues such as tourist attractions, community convenience stores, canteens, and discount stores have also rapidly expanded. At the same time, consumers' awareness of food safety is increasing day by day, driving an increase in demand for healthy and nutritious choices, making frozen food more popular.

●National product expansion and full-year supply of seasonal products

The frozen food industry is gradually expanding its geographical coverage, and now regional specialty foods can be purchased nationwide. In addition, due to consumers' growing demand for diverse and convenient dining options that cater to different tastes and occasions, seasonal festival foods are now available throughout the year. This transformation highlights the industry's adaptability to changing customer preferences, providing a wider range of products to meet the needs of different regions and seasons.

PART/7

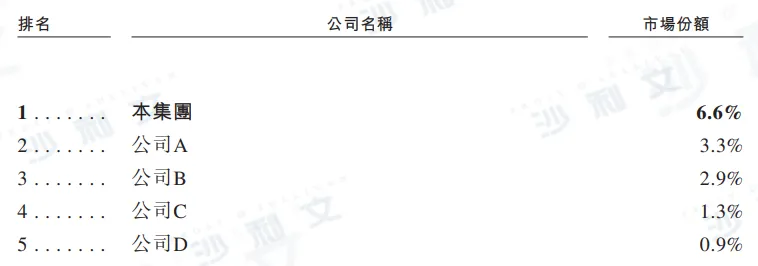

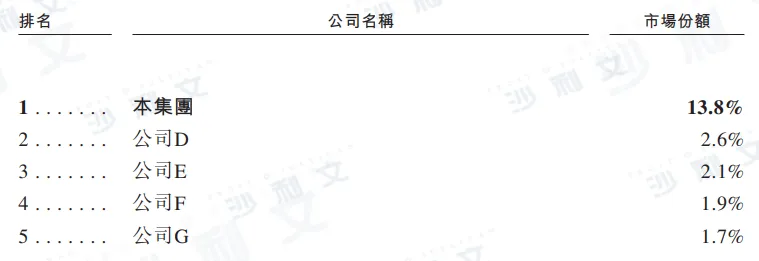

Competitive landscape of China's frozen food industry

The company ranks first in the Chinese frozen food industry, maintaining a dominant position, with a market share of about 6.6% in 2024.

Data source: Public information or documents of each company, Frost & Sullivan analysis

PART/8

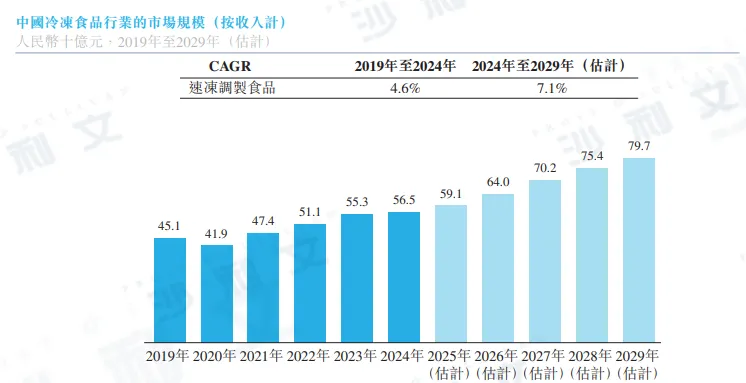

China's Frozen Prepared Foods Industry

China's frozen prepared food industry has shown strong growth in recent years. In 2020, the catering industry was restricted from operating hours due to public health events, coupled with supply-side disruptions, which limited industrial growth that year. From 2019 to 2024, the CAGR of the industry market scale was 4.6%, reaching RMB 565 billion in 2024. Driven by multiple factors such as the increasing diversification of dining methods like hot pot, spicy hot pot, and barbecue, as well as the growing demand for high-quality products, China's frozen prepared food industry is expected to achieve rapid growth, with a CAGR forecasted to be 7.1% from 2024 to 2029.

Data source: National Bureau of Statistics, Frost & Sullivan analysis

PART/9

Competitive landscape of China's frozen prepared food industry

Ranked first in China's frozen prepared food industry by revenue in 2024.

Data source: Public information or documents of each company, Frost & Sullivan analysis

PART/10

China's Frozen Dishes Industry

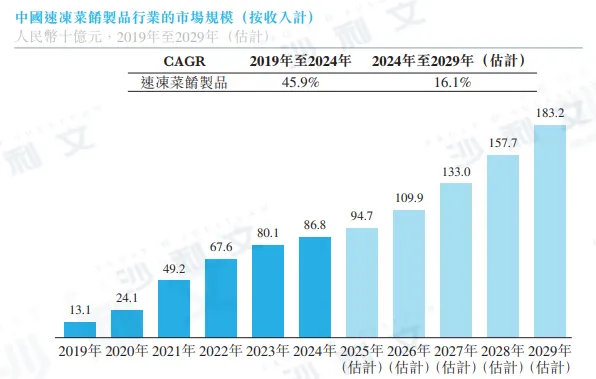

The frozen dish products industry in China is still in its infancy but has shown significant growth. The CAGR from 2019 to 2024 is 45.9%, reaching 868 billion yuan in 2024. The rapidly growing frozen dish products industry is mainly driven by the growth in catering and personal customer demand. The catering industry is characterized by chain operations that emphasize standardization and efficiency. As the penetration rate of chain operations continues to rise, the demand for frozen dish products has also increased. For individual customers, in an increasingly fast-paced lifestyle, the demand for convenience cooking is gradually increasing, leading to a preference for frozen dish products in household consumption. The Chinese market has a high acceptance of new products, especially pre-packaged dishes such as flavored crayfish and flavored chicken. The industry is expected to maintain strong growth, with a CAGR from 2024 to 2029 reaching 16.1%.

Data source: National Bureau of Statistics, Frost & Sullivan analysis

PART/11

Competitive landscape of China's frozen dish products industry

Based on 2024 revenue, the company ranks first in the frozen dish products industry in China.

Data source: Public information or documents of each company, Frost & Sullivan analysis

PART/12

China's Frozen Noodles and Rice Products Industry

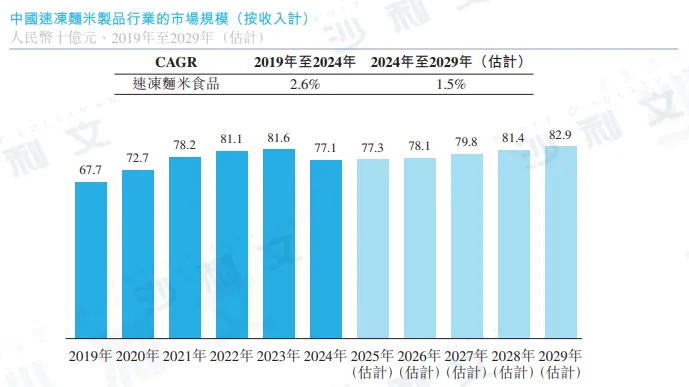

The Chinese frozen noodle and rice product industry has entered a mature phase in recent years, with traditional products and new-style products showing a differentiated trend. From 2019 to 2024, the industry's market scale has a compound annual growth rate (CAGR) of 2.6%, reaching 771 billion yuan by 2024. Multiple factors such as the diversification of new products, customer preferences, and the expansion of consumption scenarios are expected to drive sustained and stable growth. The industry is expected to have a CAGR of 1.5% from 2024 to 2029. Traditional products such as dumplings, tangyuan (rice balls), and zongzi (rice dumplings) have developed into a stable phase due to their deep integration with Chinese dietary culture, with a long development cycle. In contrast, emerging products such as baked wheat and hand-held pancakes are growing faster. These innovative products cater to changing customer preferences, promote continuous demand, and reflect the industry's trend towards more diversified products.

Data source: National Bureau of Statistics, Frost & Sullivan analysis

PART/13

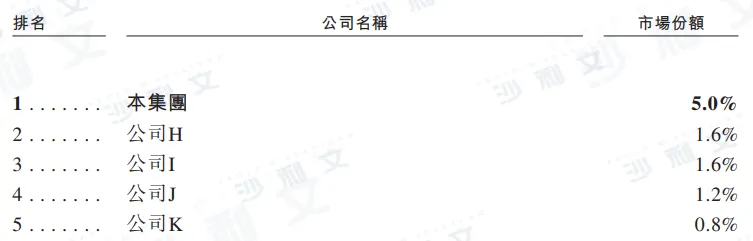

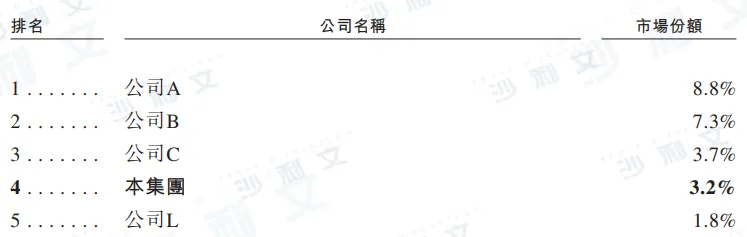

Competitive landscape of China's frozen noodle and rice products industry

Based on 2024 revenue, the company ranks fourth in the Chinese frozen noodle and rice product industry; however, when calculating by revenue of emerging frozen noodle and rice products (excluding traditional ones such as dumplings, tangyuan, and zongzi), it ranks first.

Data source: Public information or documents of each company, Frost & Sullivan analysis

Click at the end of the articleRead the original textView the full prospectus

Frost & Sullivan has extensive research experience in the consumer industry and has assisted many well-known enterprises in successfully listing on capital markets. Successful listings include: Saturday Fort (6168.HK), Haitian Flavor Industry (3288.HK), Titanium (Nasdaq: PTNM), Niu Daren (Nasdaq: MB), Newman's (2530.HK), Caoji Group (2593.HK), Mao Geping (1318.HK), Mengjinyuan (2585.HK), Laopu Gold (6181.HK), FJCGC (2497.HK), Yan Zhi Wu (1497.HK), Daily Cooking (NYSE: DDC), Youbao Online (2429.HK), Feifanlingyue (0933.HK), Shanghai Shangmei (2145.HK), Ju Zi Biotech (2367.HK), China COSCO (1880.HK), Midea Group (9896.HK), Jiulongwang Food (1927.HK), Vesync (2148.HK), Blue Moon (6993.HK), Pop Mart (9992.HK), Midea Group (NYSE: MNSO), Nongfu Spring (9633.HK), Fengxiang Food (9977.HK), China Feihai (6186.HK), Taobo Sports (6110.HK), China National Tobacco International (6055.HK), Youpin 360 (2360.HK), Wugu Flour Mill (1837.HK), Baby Tree (1761.HK), Deying Holdings (2250.HK), Bingshi International (1705.HK), Golden Cat Silver Cat (1815.HK), Miming Lifestyle Department Store (8473.HK), Nissin Foods (1475.HK), Debao Group (8436.HK), Seiko China (NASDAQ: SECO), Barbie Bebe (8297.HK), Asia Grocery (8413.HK), Chowking Duck (1458.HK), COFCO Meat (1610.HK), Dali Foods (3799.HK), Vientiane International (0288.HK), Chow Tai Fook (1929.HK), Jumei Youpin (NYSE: JMEI), and others.

Recommended Reads (Swipe up and down to view more)

Frost & Sullivan helps Saturday Stratford successfully go public in Hong Kong (6168.HK)

Frost & Sullivan assists Pitanium in successfully going public in the US (Nasdaq: PTNM)

Frost & Sullivan helped Mr. Niu successfully go public in the US (Nasdaq: MB).

Frost & Sullivan helps Newman's S.A. successfully go public in Hong Kong (2530.HK)

Frost & Sullivan helps Maogoping successfully go public in Hong Kong (1318.HK)

Frost & Sullivan helps Mengjin Garden successfully go public in Hong Kong (2585.HK)

Frost & Sullivan helps the established brand Gold successfully go public in Hong Kong (6181.HK)

Frost & Sullivan assists Yanzhiwu in successfully listing on the Hong Kong Stock Exchange (1497.HK)

Frost & Sullivan helps Rizhao Dadi Cook successfully go public in the US (NYSE:DDC)

Frost & Sullivan assists Vesync in successfully listing on the Hong Kong Stock Exchange (2148.HK)

Frost & Sullivan assists Blue Moon in successfully listing on the Hong Kong Stock Exchange (6993.HK)

Frost & Sullivan helps Pop Mart successfully go public in Hong Kong (9992.HK)

Frost & Sullivan helps famous innovative products successfully go public in the US (NYSE:MNSO)

Frost & Sullivan helps China's Feihai succeed in listing on the Hong Kong Stock Exchange (6186.HK)

Frost & Sullivan helps Top Glove Sports S.A. successfully go public in Hong Kong (6110.HK)

Frost & Sullivan helps Youpin 360 successfully go public in Hong Kong (2360.HK)

Frost & Sullivan helps Baby Tree successfully go public in Hong Kong (1761.HK)

Frost & Sullivan helps Golden Cat and Silver Cat successfully go public in Hong Kong (1815.HK)

Frost & Sullivan helps Nippon Sake & Foods Co., Ltd. successfully go public in Hong Kong (1475.HK)

*The above order is not sequential and is arranged in reverse chronological order based on listing time.