Frost & Sullivan

Peking Union Medical College Pharmaceutical Co., Ltd. (Stock Code: 2592.HK) successfully listed on the main board of the Hong Kong capital market on July 3, 2025. The company is an innovative clinical-stage ophthalmic biotech company dedicated to developing novel and differentiated therapies. For many years, Peking Union Medical College Pharmaceutical Co., Ltd. has been focusing on internal discovery, development, and commercialization of first-in-class and best-in-class ophthalmic therapies. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provides exclusive industry advisory services for the listing of Peking Union Medical College Pharmaceutical Co., Ltd., and hereby warmly congratulates them on their successful listing.

PDC Vision Cloud Pharmaceutical Co., Ltd. (hereinafter referred to as 'PDC Vision Cloud') was successfully listed on July 3, 2025. The company plans to issue 60.582 million H shares, of which 90% will be for international sale and 10% for public sale. The maximum offering price per share is HK$10.10, raising a net amount of approximately HK$5.222 million.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing the relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business, and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

According to LiveReport's big data (statistical data as of June 30, 2025), from January to June 2025, and during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services to 29 (71%), 60 (67%), and 164 (69%) Hong Kong-listed IPOs respectively, boasting rich industry experience and experience in communicating with exchanges and investors.

PART/1

Investment Highlights

The company is a clinical-stage ophthalmic biotech company dedicated to developing various therapies. With its comprehensive internal R&D system, the company has established an innovative pipeline consisting of candidate drugs covering major diseases in the anterior and posterior parts of the eye. Among them, there are four candidate drugs in clinical stage and four candidate drugs in preclinical stage.

● Core product CBT-001

CBT-001 is a potential first-in-class drug for the treatment of pterygium (a benign proliferative ocular surface disease), and is expected to become the world's first drug for the treatment of pterygium. Through early non-invasive treatment, CBT-001 can control the development of pterygium, reducing or delaying the need for surgical removal. In addition, CBT-001 can also be used for the prevention of pterygium growth and reduction of conjunctival congestion. Currently, the company is conducting Phase 3 multi-region clinical trials in the United States and China, and plans to further advance clinical research in New Zealand, Australia, and India. In the future, it will submit new drug applications to the FDA and the National Medical Products Administration.

●Core product CBT-009

CBT-009 is an atropine ophthalmic preparation used to treat myopia in adolescents aged 5 to 19 years. It is the only candidate drug in clinical phase that uses an aqueous formulation. Based on preclinical and clinical studies conducted by the company, CBT-009 is comparable in efficacy to aqueous formulations but has significant advantages in terms of patient tolerance, safety, and product stability. Currently, CBT-009 has completed Phase 1/2 clinical trials and plans to conduct Phase 3 clinical trials simultaneously in the United States and China after toxicity studies are completed in China. Its other indications also include the prevention and control of myopia in adolescents.

● Pipeline Product CBT-006

CBT-006 is a potential first-in-class candidate drug for the treatment of meibomian gland dysfunction-related dry eye syndrome. It uses a unique active ingredient and is expected to fill an existing therapeutic gap, becoming a first-in-class product.

● Pipeline Product CBT-004

CBT-004 is currently the only candidate drug in clinical trials globally for the treatment of vascularized blepharoptosis. Existing treatment options are mostly eye drops containing humectants, non-steroidal anti-inflammatory drugs, or steroids, which due to insufficient safety and efficacy, fail to meet clinical needs. In contrast, CBT-004 is expected to demonstrate significant advantages.

● Other preclinical candidate drugs

-

CBT-007: Used to improve the success rate of glaucoma filtering surgery

-

CBT-199 and CBT-145: New formulations and chemical entities for the treatment of presbyopia

-

CBT-011: ADS conjugate for the treatment of diabetic macular edema

The company has established strategic partnerships for international cooperation and value co-creation to promote the global commercialization of its core products. The company has signed a commercialization license agreement with FarDC Biologics, granting it exclusive and sublicensable licenses to produce and commercialize CBT-001 in the Greater China region; and has reached an exclusive license agreement with CanSino Biologics, authorizing it to develop, produce, and commercialize CBT-001 and related drugs in Japan, South Korea, and Southeast Asian countries.

In the future, the company will continue to expand in-depth cooperation with global pharmaceutical companies by leveraging its strong technology platform and international layout, thereby enhancing the global accessibility and commercial value of core products.

PART/2

Overview of the Ophthalmic Drug Market

Global Ophthalmic Drug Market

Ophthalmic diseases refer to conditions that affect any part of the eye, including the cornea, optic nerve, lens, retina, choroid, and ocular surface. There are over a hundred known ophthalmic diseases. Based on the type of disease, ophthalmic diseases can be classified into:

-

Ophthalmic diseases that do not threaten vision, including dry eye syndrome, blepharochromia, and conjunctivitis (inflammation of the conjunctiva). Although these conditions usually do not directly lead to vision loss, if not treated promptly, they can also cause serious complications and affect the patient's quality of life.

-

Ophthalmic diseases that threaten vision include pterygium, retinal diseases (one of the main causes of vision impairment and blindness), glaucoma, as well as myopia and presbyopia in adolescents.

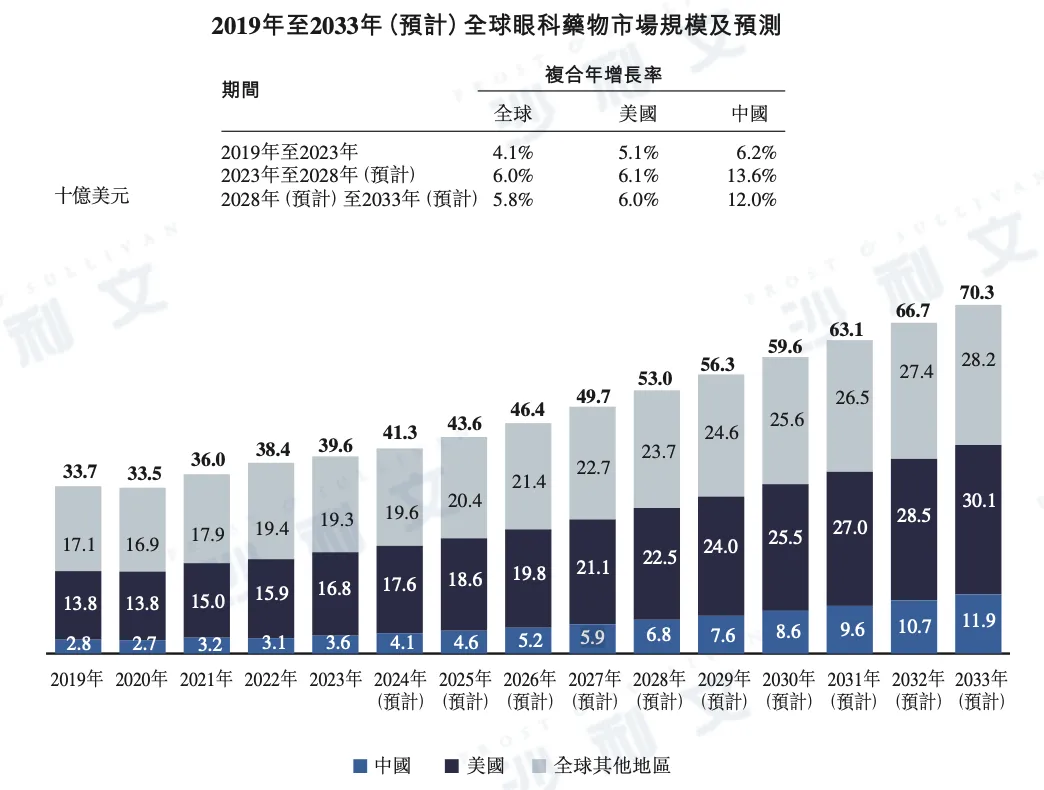

With the intensification of global population aging and changes in lifestyle, the number of patients with major ophthalmic diseases continues to rise, driving rapid growth in the global ophthalmic drug market.

The following is a detailed data on the market size of ophthalmic drugs in the United States, China, and other regions around the world from 2019 to 2033:

Data sources: literature review, expert interviews, annual reports published by market participants, Frost & Sullivan analysis

PART/3

Pterygium

Overview

Pterygium is a common benign proliferative ocular surface disease characterized by wing-like fibrovascular conjunctival tissue growing on the corneal edge. Although originating from the sclera, the apex of pterygium can invade the cornea, leading to visual impairment, ocular discomfort, and changes in appearance.

Ultraviolet exposure (such as prolonged activity in sunlight) is widely considered an important risk factor for pterygium, making outdoor workers a high-risk group. The pathogenesis of pterygium is closely related to changes in local ocular surface homeostasis. Its main histological features include proliferation of limbal stem cells, active fibrovascular tissue, epithelialization, extracellular matrix changes with accumulation of collagen and elastic fibers, as well as inflammatory infiltration.

The growth types of pterygium can be divided into slow-growing and progressive types. Regardless of the growth rate, it can cause foreign body sensation, stinging pain, congestion, and visual impairment. If not treated in time, a very small number of cases may lead to blindness due to corneal scarring. In addition, when pterygium grows to the surface of the cornea, it can destroy the normal tear film, causing dry eyes and stinging pain. The body's immune response can also lead to congestion, inflammation, and redness and swelling of the eyes, with patients often experiencing symptoms such as red eyes, tearing, and foreign body sensation.

According to the progression of the lesion, pterygium can be divided into three stages. In the first stage, the lesion's head does not reach the midline between the corneal limbus and the pupil margin; in the second stage, the lesion's head crosses the midline but has not reached the pupil; in the third stage, the lesion's head invades the pupil margin.

In the first two stages, patients typically present with symptoms of dry eyes (such as a burning sensation, itching, tearing) and conjunctival hyperemia (such as redness, stinging, tearing, and a foreign body sensation); when progressing to the third stage, pterygium may cause astigmatism or directly invade the visual axis, leading to significant visual impairment.

Global competitive landscape of drugs for the treatment of pterygium

Currently, there are no drugs approved globally for the treatment of pterygium.

According to the analysis of Frost & Sullivan, both CBT-001 and AG-86893 are nintedanib, with the same mechanism of action; the active compound of RMP-A03 has not been disclosed. At present, all candidate drugs developed for the treatment of pterygium are administered topically.

Nintedanib (trade name Ofev®Produced by Boehringer Ingelheim and marketed as a reference product for CBT-001. Ofev®The active ingredient is nintedanib monethanesulfonate (the patent also belongs to Boehringer Ingelheim with a validity period until 2034). It was approved by the US Food and Drug Administration (FDA) in 2014 for the treatment of idiopathic pulmonary fibrosis in the form of oral capsules. In China, Ofev®It has been included in the national medical insurance catalog, with a terminal price of about 4,500 yuan for 30 capsules; in the United States, the market price for 60 capsules is about $13,695. Due to differences in medical insurance plans and treatment regimens, the actual payment price for American patients can range from full reimbursement to as high as $243 per capsule.

Nintedanib is a small molecule multi-target tyrosine kinase inhibitor that acts on a variety of receptor tyrosine kinases (PDGFR & alpha;/β, FGFR 1-3, VEGFR 1-3, CSF1R, and FLT3), as well as non-receptor tyrosine kinases (except for FLT3, which are associated with the pathogenesis of interstitial lung disease). It blocks intracellular signal cascades by competitively binding to the ATP-binding sites of these kinases, inhibiting the pathological processes related to the remodeling of fibrotic tissue in interstitial lung disease.

In terms of the pharmacological mechanism of pterygium, nintedanib is expected to delay or replace the need for surgical treatment by inhibiting angiogenesis and fibrosis.

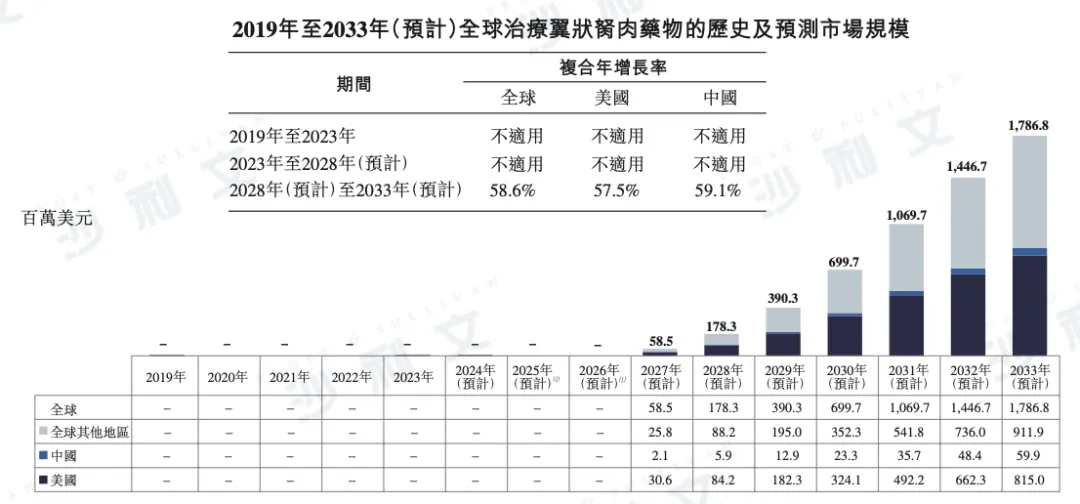

Market scale of pterygium medications

The global drug market for the treatment of pterygium is expected to experience rapid growth, with a scale that is projected to reach $178 million by 2028 and increase to $178.7 billion by 2033. During this period, the compound annual growth rate (CAGR) will reach 58.6%.

Regionally, the US market size is expected to reach $84.2 million in 2028, increasing to $815 million in 2033 with a CAGR of 57.5%. The Chinese market is expected to reach $5.9 million in 2028 and increase to $59.9 million in 2033 with a CAGR of 59.1%.

The following is a detailed distribution of the global pterygium treatment drug market size from 2019 to 2033, including data details for the United States, China, and other regions:

Note:

(1) Currently, there are no drugs approved globally for the treatment of pterygium, and the first one is expected to be launched in 2027.

(2) The key assumptions for the growth of the market for drugs for pterygium in the United States, China, and globally include: (i) Number of patients: Based on authoritative statistics and literature analysis, considering risk factors such as population aging and proximity to the equator, it is expected that the prevalence will increase slightly. (ii) Diagnosis and treatment rate: Currently, the diagnosis and treatment rates in the United States and China are about 3.0% and 0.6%, respectively; it is expected to rise to 3.5% and 0.9% by 2027, further increasing to 6.1% and 2.8% by 2033, benefiting from improved patient health awareness and expanded treatment options such as targeted drugs. (iii) Drug accessibility: With the launch of more drugs and improved affordability, it is expected that the accessibility rates in the United States and China will reach 0.5% and 0.2% by 2027, rising to 7.6% and 1.5% respectively by 2033. (iv) Annual treatment cost: Based on the expected pricing of CBT-001, it is competitive compared to Restasis (≥$638) and Xiidra (≥$693). (v) Drug launch timing: Three candidate drugs for pterygium are expected to be approved for market launch in 2027, 2029, and 2036, respectively, improving accessibility and driving market growth.

Data sources: literature review, expert interviews, market surveys, Frost & Sullivan analysis

The main drivers of market growth and entry barriers for drugs treating pterygium

The growth of the pterygium drug market is mainly driven by the following key factors:

1. The patient population is constantly expanding

Pterygium is a common eye disease affecting millions of people worldwide. As the number of patients continues to rise, the market demand for effective drug treatment regimens is growing steadily, driving pharmaceutical companies to accelerate the development and commercialization of new therapeutic products.

2. Unmet medical needs

Public awareness of eye health and the accessibility of treatment options is continuously increasing, injecting growth momentum into the pterygium drug market. Due to the potential impact of pterygium on vision and quality of life, patients' demand for more effective drug interventions is becoming increasingly urgent, driving an expansion of the treatable patient population. According to a survey in the Brazilian Amazon region, the prevalence rates of visual impairment and blindness caused by pterygium are 14.3% and 3.9%, respectively.

3. The Urgency of Early Medication

Currently, there are no approved drug therapies for the treatment of pterygium globally, and surgical removal remains the main treatment method. However, surgery has a recurrence rate of about 10%, and off-label medications can only alleviate symptoms, posing safety and efficacy concerns with long-term use. If pterygium can be treated with drug intervention at an early stage, it will significantly improve patient prognosis and reduce the need for invasive treatments.

Although the number of patients with winged pterygium globally is relatively stable, due to the current lack of approved drugs and the limitations of existing treatment methods, the market size is expected to experience explosive growth once new drugs are approved in the future. Such innovative drugs are expected to improve patient clinical outcomes and reduce dependence on invasive treatments.

In addition, developing drugs for the treatment of pterygium faces multiple research and development challenges, including establishing effective models based on the disease's pathogenesis, determining the optimal route of administration and delivery formulations. Considering the fibrovascular pathological characteristics of pterygium, inhibiting related growth factors to block their development has become a patented technology for some companies, and it also sets entry barriers for other potential market participants using eye drops such as nanoemulsions.

PART/4

Myopia among teenagers

Overview

Myopia in adolescents, also known as progressive myopia or nearsightedness, is a common visual problem that gradually develops and occurs in children and adolescents. Research shows that the occurrence of myopia is due to the combined action of genetic and environmental factors, including prolonged close-range eye use (such as reading and using electronic devices), insufficient outdoor activities, and long-term exposure to strong light environments.

The main mechanism of myopia is an increase in eye length or a change in corneal curvature, which causes light from distant objects to focus in front of the retina, thereby leading to blurred vision at distances. According to refractive power, 0.50 to -6.00 diopters are considered mild to moderate myopia, while those exceeding -6.00 diopters are considered high myopia.

Unlike refractive myopia caused by ciliary muscle fatigue and contraction, the characteristic of juvenile myopia is a rapid increase in axial length of the eye, leading to gradual elongation of the eyeball. Even if the ciliary muscle function is normal, accurate focusing cannot be achieved. This pathological change can further develop into high myopia, increasing the risk of complications such as retinal choroidal atrophy, choroidal neovascularization, macular hole, and retinal detachment, causing severe and permanent visual impairment. In fact, myopia has become one of the leading causes of blindness globally.

Children and adolescents aged 5 to 19 are in a critical period of visual development, during which myopia develops particularly rapidly. If not intervened in time, it will not only affect the educational level and quality of life of children but may also have long-term negative impacts on their mental health and cause productivity losses worldwide.

It is worth noting that children living in developed urban areas are at high risk of myopia, suggesting an urgent need to promote effective prevention, control, and treatment measures among urban children and adolescents to slow down axial elongation of the eye and prevent myopia complications.

The global competitive landscape of drugs for treating myopia in adolescents

Eikance 0.01% Eye Drops are the first prescription medication approved by the Therapeutic Goods Administration (TGA) of Australia for use in children aged 4 to 14 years old to slow down the progression of myopia. Currently, the product is only approved and commercially available in Australia and New Zealand. In Australia, the market price of Eikance is about A$40, with each patient's annual treatment cost being approximately A$480. Eikance 0.01% Eye Drops have also been approved by the New Zealand Medicines and Medical Devices Safety Authority and can be purchased from pharmacies in New Zealand with a prescription starting from the end of June 2024.

In addition to Eikance, China's Xingqi Meiope 0.01% Eye Drops were approved by the National Medical Products Administration in March 2024 for use in children aged 6 to 12 as a treatment option to slow down myopia progression. Ryjusea 0.025% Eye Drops were also approved in Japan in December 2024 and in the European Union in June 2025 for use in children aged 5 to 15 to slow down myopia progression.

Currently, there are no atropine-based drugs approved for the treatment of myopia in adolescents in the United States or Hong Kong. Clinically, they are mainly used off-label through low-dose atropine eye drops.

The reference drug for CBT-009 is atropine, which has been approved by the US Food and Drug Administration (FDA) for ophthalmic treatment. The FDA-approved brand names for 1% atropine sulfate solution include Atropine Sulfate and Isopto Atropine.®Applicable for mydriasis, ciliary muscle paralysis in amblyopia treatment, and correction of healthy eyes. Many ophthalmic drugs contain atropine sulfate as the active ingredient. Among them, Isopto Atropine®Approved by the FDA in 2016, its manufacturer and patent holder is Alcon, with the patent valid until 2030.

Market scale of drugs for treating myopia in adolescents

The global market for myopia treatment drugs for adolescents is experiencing rapid growth. The market size increased from $72.8 million in 2019 to $90.2 million in 2023, with a CAGR of 5.5% during this period. It is expected that the market size will leap to $858 million by 2028 and reach $3.697 billion by 2033. The CAGRs from 2023 to 2028 and from 2028 to 2033 are as high as 56.5% and 33.9%, respectively.

Although there are currently no approved drugs in the United States for the treatment of myopia in adolescents, the market potential is enormous. It is estimated that the US market size will reach $308 million by 2028, further increasing to $1.37 billion by 2033, with a CAGR of 34.7% from 2028 to 2033.

The Chinese market has also shown a strong growth momentum. From 2019 to 2023, the market size of myopia treatment drugs for teenagers in China increased from $3 million to $5.2 million, with a CAGR of 14.5%. It is expected that it will reach $348 million in 2028, increase to $1.299 billion in 2033, and have CAGRs as high as 113.8% and 30.1% respectively from 2023 to 2028 and from 2028 to 2033.

The following is a detailed data on the global market size of myopia treatment drugs for adolescents from 2019 to 2033, including market details for the United States, China, and other regions:

Global historical and forecasted market size of drugs for treating myopia in adolescents from 2019 to 2033 (estimated)

Note:

The growth in the market size of drugs for treating myopia in adolescents in the United States, China, and globally is based on the following key assumptions: (i) Number of patients: According to authoritative statistics and literature analysis, the prevalence of myopia among adolescents is high, but several previously approved drugs (such as NVK-002, SYD-101, OT-101, HR19034) have not yet been approved. (ii) Diagnosis and treatment rate and drug penetration: Currently, about 90% of adolescent myopia patients are corrected by wearing glasses, and there are no approved drugs in the United States and China, resulting in a smaller historical market size. With the approval of Xingqimiao Euphorbia in China and the future launch of more drugs, it is expected that the penetration rate of myopia drugs among adolescents will reach about 10.2% and 8.9% in the United States and China, respectively, by 2033. The growth drivers include (a) new drug approvals, (b) policy promotion and public education to raise awareness of early intervention, (c) increased willingness of parents to invest in vision care. (iii) Annual treatment cost: Estimated at about $600 in the United States and about 3,600 yuan in China based on Eikance and Xingqimiao Euphorbia prices. The price of Ryjusea approved in Japan and the European Union has not been disclosed.

Data sources: literature review, expert interviews, market surveys, Frost & Sullivan analysis

The main drivers of market growth and entry barriers for drugs treating myopia in adolescents

The growth of the market for myopia treatment drugs among teenagers is mainly driven by the following key factors:

1. The number of myopic people continues to expand

Myopia has become an important public health issue globally. Affected by factors such as accelerated urbanization, lifestyle changes, and extended study hours, the prevalence of myopia among adolescents has risen significantly over the past half century, especially in East Asia. As the number of myopic children and adolescents continues to increase, the demand for drugs to slow down myopia progression is growing day by day, thereby driving the continuous expansion of the market size.

In China, the problem of myopia among teenagers is particularly prominent. The 'Comprehensive Implementation Plan for the Prevention and Control of Myopia in Children and Adolescents' proposes that by 2030, the myopia rates among primary school students, junior high school students, and senior high school students should be controlled below 38%, 60%, and 70% respectively. Such national strategies not only raise public awareness of myopia prevention and control but also lay a solid foundation for the development of the myopia medication market. Research indicates that without intervention, myopia may become one of the most common irreversible causes of vision loss in East Asia.

2. Clinical validation of the therapeutic efficacy of atropine eye drops

Currently, the number of non-atropine drugs approved globally for delaying myopia progression is limited, and their efficacy is generally not satisfactory. Numerous studies have confirmed that atropine eye drops have good tolerance while slowing myopia development and are safe and reliable even when used for long periods. Low-dose atropine eye drops have been used off-label globally for decades and are gradually being incorporated into routine myopia management. The 'Guidelines for the Prevention and Control of Myopia in Children and Adolescents' recommend 0.01% atropine eye drops as an adjunct to routine optical correction, with minimal side effects, suitable for children and adolescents.

Since 2019, 0.01% atropine eye drops have been used in China as an in-hospital preparation for medical institutions to slow down myopia progression. With the approval of related products for marketing, clinical use is expected to become increasingly widespread, further driving market growth.

Although the number of myopic teenagers in the United States and other key markets has remained relatively stable, while the number of patients in China has decreased, the market for myopia medications for teenagers still has strong growth potential due to the importance of myopia prevention and control in public health, as well as the significant advantages of atropine in terms of efficacy and safety.

In addition, the development of atropine eye drops still faces technical challenges. Due to the presence of ester bonds in the atropine molecular structure that are prone to hydrolysis, traditional aqueous eye drop formulations have poor stability, affecting their shelf life. They can also cause eye irritation and affect the medication compliance of children and adolescents. To overcome these issues, some companies have developed non-aqueous eye drop formulations and used approved artificial tears as the main excipient to improve comfort, forming entry barriers through patent protection. These innovative technologies are expected to further promote the development of the market for myopia treatment drugs for adolescents.

PART/5

Dry eye syndrome related to meibomian gland dysfunction

Overview

Meibomian glands are large sebaceous glands located within the eyelids, secreting lipids to form the outermost layer of the tear film, helping to prevent water evaporation and maintain tear film stability. Meibomian gland dysfunction (MGD) is a chronic, diffuse glandular disease characterized by glandular obstruction or dysfunction, leading to reduced lipid secretion and causing evaporative dry eye syndrome.

The main symptoms of MGD patients include abnormal tear secretion, dry and itchy eyes, stinging pain, inflammation, and blepharitis, which manifests as inflammation of the eyelids and crusty secretions at the base of the eyelashes. Women and the elderly are high-risk groups for MGD.

According to a Frost & Sullivan report, MGD is an important cause of dry eye disease cases accounting for 70% to 86% globally. As a common public health issue, the global total prevalence rate of dry eye disease is about 10%. If the condition progresses further, dry eye disease can lead to visual impairment and functional decline, seriously affecting the quality of life of patients.

Dry eye syndrome is a multifactorial tear film disease characterized by increased tear film osmolarity, ocular inflammation, degenerative changes of the ocular surface, and abnormal nerve sensation, manifesting as symptoms such as ocular discomfort, itching, and blurred vision. Patients with moderate to severe conditions often experience depressive emotions due to limited daily activities.

Groups with poor tear film stability are often accompanied by meibomian gland blockage or mite infections. Prevention and treatment of meibomian gland blockage and mite infections are particularly important for the prevention and control of dry eye syndrome.

Currently, mild dry eye syndrome is mainly treated with artificial tears, education, and environmental adjustments; as the condition progresses, local anti-inflammatory drugs (such as cyclosporine, steroids, rifampicin), eyelid cleansing, lacrimal duct plugging, thermodynamic therapy, amniotic tape, autologous serum may be required, and in severe cases, surgical intervention may even be necessary. However, existing treatment options still have limitations, and there is an increasing demand globally for innovative therapies for dry eye patients.

Global competitive landscape of drugs for treating dry eye syndrome related to meibomian gland dysfunction

The treatment methods for dry eye syndrome are diverse, including artificial tears, anti-inflammatory drugs, and other intervention measures. However, the approval of Miebo® (perfluorohexyl octane eye drops) marks an important breakthrough in the treatment field. On May 18, 2023, Miebo® was approved by the US Food and Drug Administration (FDA) for the treatment of signs and symptoms of dry eye syndrome, becoming the first and only prescription drug for dry eye syndrome that directly targets tear evaporation approved by the FDA.

Excessive tear evaporation is often closely related to abnormal meibomian gland function. Previously, topical ophthalmic prescription drugs could only act on indirect factors of dry eye syndrome, such as inflammation, bacterial growth, or insufficient tear secretion, but not on the key driver of the disease—excessive tear evaporation. The launch of Miebo is expected to bring new treatment options to a large number of dry eye syndrome patients, improving symptoms and enhancing quality of life.

The market size of drugs for treating dry eye syndrome related to meibomian gland dysfunction

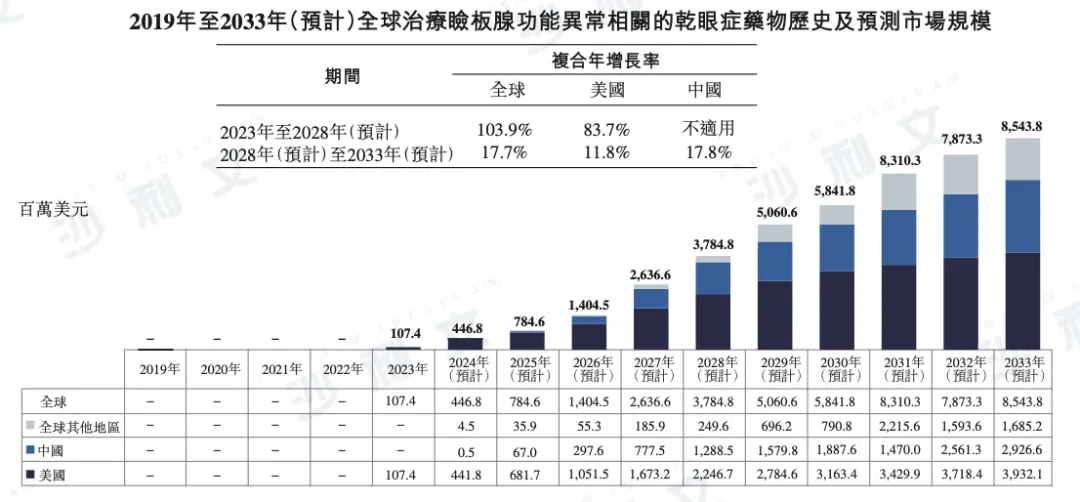

According to a Frost & Sullivan report, the global drug market for treating meibomian gland dysfunction (MGD)-related dry eye syndrome is expected to maintain strong growth. By 2028, the market size is expected to reach $3.785 billion and further grow to $8.544 billion by 2033, with a CAGR of 17.7% from 2028 to 2033.

Regionally, the US market is expected to reach $2.247 billion in 2028 and grow to $3.932 billion by 2033, with a CAGR of 11.8%.

The growth potential of the Chinese market is particularly significant, with an estimated market size reaching $1.289 billion in 2028 and increasing to $2.927 billion by 2033, with a CAGR of 17.8%.

The following provides detailed data on the global market size of drugs for meibomian gland dysfunction-related dry eye disease from 2019 to 2033, including market details for the United States, China, and other regions:

Data sources: literature review, expert interviews, market surveys, Frost & Sullivan analysis

The main drivers of market growth and entry barriers for drugs treating dry eye syndrome related to meibomian gland dysfunction

The growth of the drug market for treating meibomian gland dysfunction (MGD)-related dry eye syndrome is mainly driven by the following key factors:

1. The patient population continues to expand

The prevalence of meibomian gland dysfunction remains high, driving patients and healthcare professionals to deepen their understanding of the disease, thereby stimulating the demand for effective drug treatments. Studies have shown that MGD is an important causative factor in 70% to 86% of dry eye syndrome cases worldwide. Drugs targeting MGD can not only effectively alleviate symptoms but also provide more targeted treatment options for patients affected by the disease.

2. In-depth understanding of the causes of diseases

In the past, the diagnosis and treatment of dry eye syndrome mainly focused on tear film instability. However, in recent years, dry eye syndrome has been defined as a multifactorial disease and is clearly divided into two subtypes: aqueous-deficient dry eye syndrome and evaporative dry eye syndrome. The enhanced understanding of the etiological mechanisms has promoted the development of targeted drugs. In the future market, more innovative therapies focusing on the pathological mechanisms of MGD will emerge to meet the growing treatment needs of patients.

3. Major shift in treatment strategies

In recent years, the treatment approach for MGD has undergone a significant transformation from symptom management to etiological treatment. Traditional therapies mainly focused on alleviating symptoms, whereas current treatment concepts place more emphasis on addressing the underlying mechanisms of the disease, providing comprehensive and sustainable treatment plans.

In 2023, the US Food and Drug Administration (FDA) approved Miebo™, becoming the first and only drug for dry eye syndrome that directly targets tear evaporation (usually associated with meibomian gland dysfunction, MGD). This marks an important milestone in the treatment field. According to Bausch & Lomb Inc.'s third-quarter financial report for 2023, Miebo™ reached a total of 9,600 prescriptions in its first month of market launch (including new and repeat orders), reflecting the strong demand and positive acceptance of this innovative therapy by healthcare professionals and patients.

However, in addition to the general barriers to entry in the global ophthalmic drug market, the development of MGD-related dry eye disease drugs still faces multiple challenges, including a lack of in-depth understanding of the disease's pathogenesis and effective treatment methods for addressing the causes. For example, the discovery of the dissolution mechanism of cholesterol, a major component causing lipid deposition at the meibomian gland opening, and its patent layout may constitute obstacles for other market participants entering this field.

PART/6

blepharochromic stoma

Overview

Lipid keratopathy is a common conjunctival degenerative lesion, characterized by round, pale yellow raised tissue located on the bulbar conjunctiva near the cornea, usually not involving the cornea itself. Its pathological feature is the degeneration of subepithelial collagenous elastic tissue, accompanied by proliferation of transparent connective tissue, forming a yellowish-white fibrovascular elevation.

Most patients with blepharochromic striae have no obvious symptoms and therefore do not require treatment. However, their pale yellow protrusions can cause mechanical irritation or cause ocular surface stinging due to uneven tear film distribution. When the lesion becomes vascularized or inflamed, patients may experience changes in appearance, eye congestion, stinging, pain, foreign body sensation, tearing, and itching, which severely affect eye comfort and quality of life.

The occurrence of blepharochalasis is closely related to long-term exposure to environmental stimuli such as wind, dust, ultraviolet rays, and aging. Unlike pterygium, blepharochalasis does not invade the cornea. However, due to its raised characteristics, it can cause uneven tear film diffusion on the ocular surface, leading to tear film rupture, and induce discomfort symptoms such as dry eyes, a burning sensation, blurred vision, and frequent eye rubbing.

Global competitive landscape of drugs for the treatment of blepharochromic striae

Currently, there are no approved drugs globally for the treatment of vascularized blepharochromia. CBT-004 is the only candidate drug in clinical trials globally for the treatment of vascularized blepharochromia.

According to a Frost & Sullivan report, the reference product for CBT-004 is Inlyta produced by Pfizer®(Asimertinib). Inlyta®Approved by the US FDA in 2012 for the treatment of advanced renal cell carcinoma. Axitinib is a small molecule multi-receptor tyrosine kinase inhibitor, with PF PRISM CV as the patent holder, and the patent is valid until 2037.

Axitinib effectively inhibits the growth of new blood vessels and pathological angiogenesis by blocking vascular endothelial growth factor receptor (VEGFR) and platelet-derived growth factor receptor (PDGFR). This mechanism of action provides an important scientific basis for potential drug treatment of vascularized blepharoptosis.

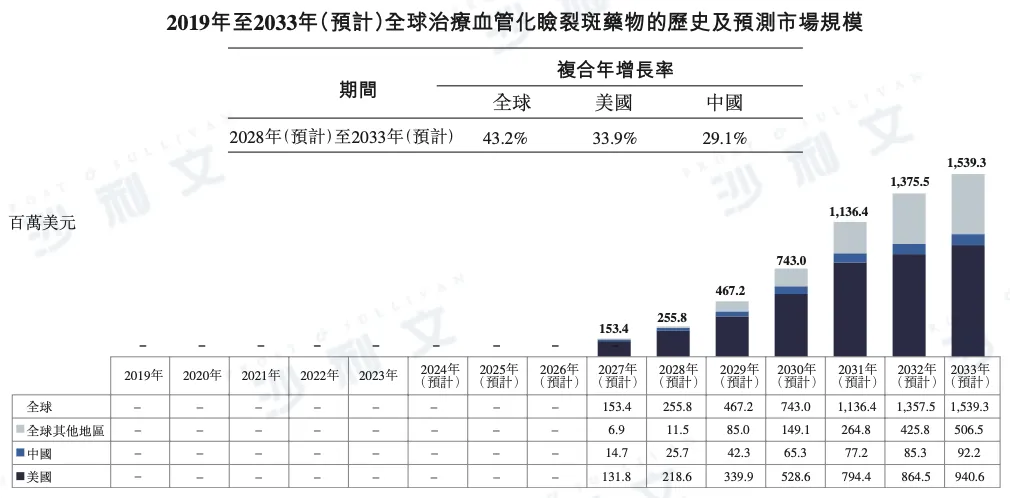

Market scale of drugs for treating vascularized blepharoptosis

According to a Frost & Sullivan report, the global market for vascularized blepharoplasty drugs is expected to experience rapid growth. By 2028, the market size is projected to reach $256 million and further increase to $1.539 billion by 2033, with a CAGR of up to 43.2% from 2028 to 2033.

Regionally, the US market has great growth potential, with the market size expected to reach $219 million in 2028 and increase to $941 million by 2033, with a CAGR of 33.9%.

The Chinese market has also shown steady growth, with an estimated market size of $25.7 million in 2028 and growing to $92.2 million by 2033, with a CAGR of 29.1%.

The following provides detailed data on the global market size of vascularized blepharoplasty drugs from 2019 to 2033, including market details for the United States, China, and other regions:

Data sources: literature review, expert interviews, market surveys, Frost & Sullivan analysis

The main drivers of market growth and entry barriers for drugs treating vascularized blepharochromia

The growth of the drug market for treating vascularized blepharochromia is mainly driven by the following factors:

1. The patient population continues to expand

Vascularized blepharochromic striae is a common ocular surface disease, commonly seen in individuals who are exposed to environmental factors such as ultraviolet rays, dust, and wind for long periods. The number of patients is large, providing a clinical basis and market demand for further research into its pathogenesis and the development of more effective treatment strategies.

2. Unmet medical needs

Currently, there are no approved drug therapies for the treatment of vascularized blepharochalasis globally. Existing treatments mainly focus on alleviating symptoms and cannot fundamentally address the underlying pathological mechanisms of the disease. Therefore, there is an urgent need in the market for innovative therapies that can directly inhibit angiogenesis and inflammation. Breakthroughs in this field are not only expected to significantly improve the quality of life of patients but also provide potential solutions for treating other complex ophthalmic diseases.

In addition to the common barriers to entry in the global ophthalmic drug market, developing drugs for the treatment of vascularized blepharoptosis also faces multiple research and development challenges, including: (i) establishing effective models targeting the pathogenesis of the disease; (ii) determining the optimal administration method; (iii) developing safe and efficient delivery formulations.

Considering the angiogenic pathological characteristics of vascularized blepharochromic stromal dystrophy, developing eye drops that can inhibit related growth factors and forming a technological barrier through patent protection may become an important obstacle for other market participants to enter this field.

PART/7

Glaucoma

Overview

Glaucoma is a group of eye diseases characterized by progressive structural and functional damage to the optic nerve. If not treated in time, it can lead to a blue-green disc change and permanent visual field impairment. Since there are often no obvious symptoms in the early stages, patients are often diagnosed only when the condition has progressed to an advanced stage.

Globally, glaucoma is the second leading cause of blindness after cataracts, with a blindness rate as high as 38.3%, posing a significant threat to public health. Glaucoma is mainly divided into primary and secondary types. High intraocular pressure, age over 60 years old, specific ethnic backgrounds, previous eye diseases, a history of trauma or surgery, and long-term use of corticosteroids are all major risk factors for glaucoma.

In addition to significant clinical impacts, glaucoma also imposes a huge economic, psychological, and social burden on patients and society, highlighting the importance of strengthening early screening and effective treatment.

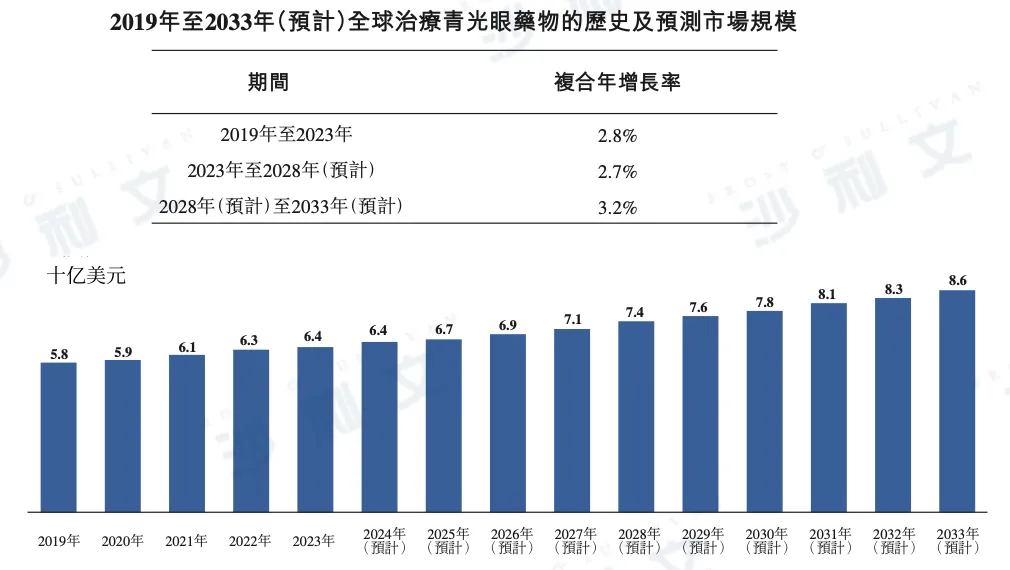

Market scale of drugs for treating glaucoma

According to a Frost & Sullivan report, the global glaucoma treatment drug market reached a market size of $6.4 billion in 2023 and is expected to maintain a steady growth. It is projected to reach $7.4 billion by 2028 and increase to $8.6 billion by 2033. The compound annual growth rates (CAGR) from 2023 to 2028 and from 2028 to 2033 are 2.7% and 3.2%, respectively.

The following is a detailed data on the global glaucoma treatment drug market size from 2019 to 2033:

Data sources: literature review, expert interviews, annual reports published by market participants, market surveys, Frost & Sullivan analysis

PART/8

Presbyopia

Overview

As people age, the lens in the eye gradually thickens and loses its elasticity, making it difficult for the eyes to focus on close objects, resulting in presbyopia (old eyesight). Presbyopia is a refractive disorder that usually occurs after the age of 40, and its essence is due to the gradual loss of accommodation ability, leading to the inability to clearly see objects at different distances.

Against the backdrop of accelerating global population aging, presbyopia has become one of the most pressing visual health issues to be addressed. The mechanisms of drug treatment for presbyopia mainly include: (i) increasing focal depth through the pinhole effect to improve visual clarity; and (ii) softening the lens, restoring some of its elasticity, thereby reducing or improving the impact of presbyopia on vision.

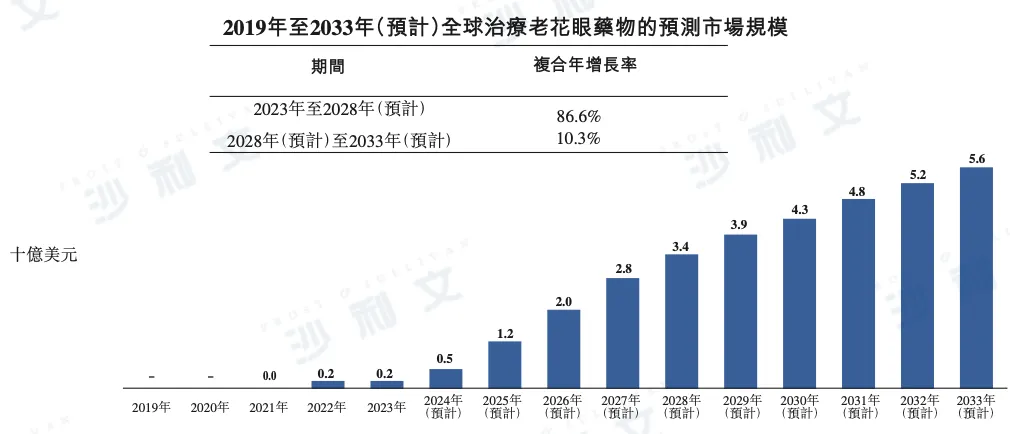

Market scale of drugs for treating presbyopia

According to a Frost & Sullivan report, the global market for presbyopia treatment drugs reached $2 billion in 2023 and is expected to experience explosive growth in the coming years. By 2028, the market size is expected to reach $3.4 billion and further grow to $5.6 billion by 2033. The CAGR from 2023 to 2028 and from 2028 to 2033 is as high as 86.6% and 10.3%, respectively.

The following is a detailed data on the global market size of presbyopia treatment drugs from 2019 to 2033:

Data sources: literature review, expert interviews, annual reports published by market participants, market surveys, and analysis of Frost & Sullivan reports