Frost & Sullivan

Rongda Hefei Zhonghe (Xiamen) Technology Group Co., Ltd. (Stock Code: 9881.HK) successfully listed on the main board of the Hong Kong capital market on June 10, 2025. The group is a supplier of automatic identification and data collection (AIDC) devices and solutions, engaged in the design, research and development, manufacturing, and marketing of printing equipment, scales, POS terminals, and PDAs. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provides exclusive industry advisory services for the listing of Rongda Hefei Zhonghe (Xiamen) Technology Group Co., Ltd., and hereby warmly congratulates them on their successful listing.

Rongda Technology Group Co., Ltd. (Xiamen) (hereinafter referred to as 'Rongda Tech') successfully went public on June 10, 2025, with a tender offer price ranging from 10 yuan to 12 yuan, raising up to 220 million yuan in funds.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing the relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business, and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

According to LiveReport's big data (statistical data as of May 1, 2025), from January to April 2025, and during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 13 (76%), 47 (65%) and 149 (69%) Hong Kong IPOs respectively, boasting rich industry experience and communication skills with exchanges and investors.

PART/1

AIDC Devices and Solutions Market Overview

Definition and Classification

AIDC (Automated Identification Data Collection) refers to various technologies applied for automatically identifying objects, collecting relevant data, and directly inputting it into computer systems without human intervention. AIIDC systems can be used to manage data related to inventory, delivery, assets, security, and logistics, significantly improving efficiency and accuracy by reducing time and manpower required for processes.

Core AIDC technologies include barcode scanning, smart cards and magnetic stripe cards, optical character recognition, radio frequency identification scanning, and biometric systems. These technologies are directly involved in the process of reading or collecting data from items, individuals, or environments, and then capturing the relevant data for further processing.

AIDC devices can be categorized into (i) dedicated printers; (ii) scales; (iii) point-of-sale terminals ("POS terminals"); (iv) personal digital assistants ("PDAs"); and (v) others, such as barcode scanners, in-vehicle terminals, access control systems, electronic item surveillance systems, and smart cabinets.

●Special printers include receipt printers, barcode and label printers, as well as portable learning printers. Receipt printers are convenient tools for handling customer transactions, capable of printing customer receipts, credit card statements, and other related documents during sales operations at retail, manufacturing, shipping, and logistics sites. These printers are widely used in the retail, manufacturing, shipping, and logistics industries for label products, packaging, and freight tracking and management by using roll labels. Barcode and label printers come in different sizes and processing capabilities. Special printers mainly include thermal printers, dot matrix printers, and inkjet printers. Portable learning printers utilize OCR technology and include automatic recognition of student assignments. Special printers generate identifiers and ensure that the collected data is standardized, making it generally readable and recognizable by AIDC devices.

●Weighing instruments can be used in enterprise or commercial environments to accurately measure the weight of sold or purchased goods or products. Weighing instruments are typically used for automatic identification of objects and collection of object data, which are then directly input into computer systems without manual intervention.

●The POS terminal is a system used to process corporate sales transactions. A POS terminal generally includes hardware such as cash registers or computers, as well as software that assists companies in handling sales, managing inventory, and generating reports. Modern POS terminals typically come with features such as barcode scanning, credit card processing, and customer relationship management tools, and are widely used in retail, hospitality, healthcare, and other industries. POS terminals mainly include terminal machines, mobile and tablet computers, and online printers. POS terminals are usually integrated with various AIDC technologies such as barcode scanners, radio frequency identification readers, and sometimes even biometric systems for employee identity verification.

●Personal digital assistants are handheld electronic devices that can serve as customer data terminals, effectively collecting data and enabling digital business management. Similar to POS terminals, most of our personal digital assistants also support Wi-Fi, Bluetooth, and Global Positioning System (GPS), along with built-in printing functions, barcode scanning lenses, and NFC card readers. Our personal digital assistants are commonly used in logistics distribution, warehouse inventory tracking, manufacturing, retail e-commerce, and store management. Personal digital assistants used for AIDC applications generally include barcode scanning or wireless radio frequency identification reading capabilities, which are multifunctional devices capable of processing data and communicating.

●Other examples include: (i) Barcode reader: A device that automatically reads barcodes on items as they pass through a scanning area, mainly used in retail stores and logistics; (ii) Vehicle-mounted terminal: A durable device connected to forklifts, trucks, warehouse vehicles, etc., allowing operators to collect and access data while moving; (iii) Access control system: Utilizes wireless radio frequency identification, biometrics, and smart card technology to manage entrances and exits for area security; (iv) Electronic item surveillance system: Mainly suitable for retail areas, detects and prevents theft by identifying inactive or unremoved tags; (v) Smart cabinet: Used in healthcare and other industries, manages inventory of high-value items in real-time through RFID technology.

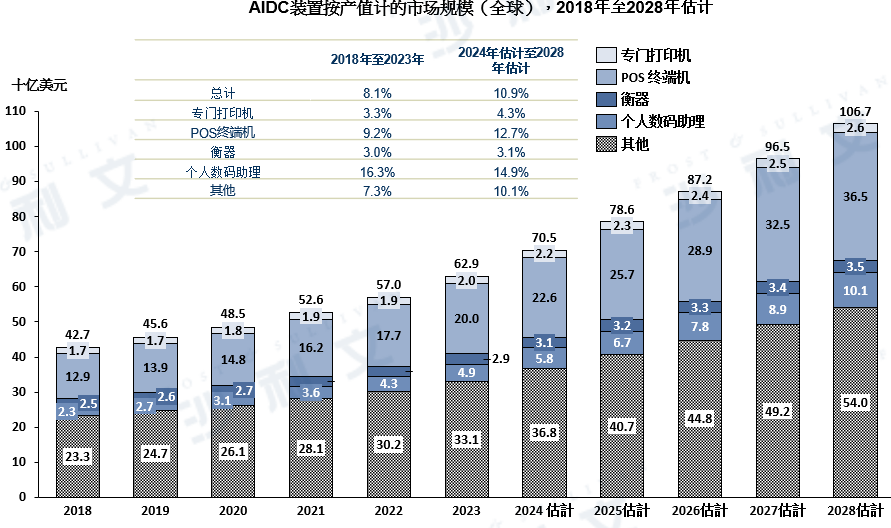

market scale

The global smart device market by value was driven by growing demand for personalized shopping experiences, increased demand for real-time inventory management, and the continuous development of online and offline retail trends. The market size increased from $42.7 billion in 2018 to $62.9 billion in 2029, with a compound annual growth rate of 8.1%. The increasing popularity of cashless payment systems and advancements in artificial intelligence and machine learning are expected to drive market development. The global smart device market by value is expected to grow at a compound annual growth rate of 10.9% from 2024 to 2028, reaching $106.7 billion by 2028. Retailers are seeking to streamline operations and improve customer experiences, which has led to the increasing application of point-of-sale (POS) systems and mobile POS solutions, thereby increasing demand for specialized printers (including receipt printers). The market size of specialized printers by value increased from $1.7 billion in 2018 to $2 billion in 2023, with a compound annual growth rate of 3.3%. Advances in printing technology (such as thermal and inkjet printing) and the popularization of online ordering and delivery will continue to be drivers of market growth. The market size of specialized printers by value is expected to reach $26 billion by 2028, with a compound annual growth rate of 4.3% from 2024 to 2028.

Source: Frost & Sullivan report

Market Drivers and Opportunities

●Increased demand for efficient automated retail solutions

In recent years, online shopping has become increasingly popular, coupled with retailers' need to streamline operations and reduce costs, leading to a significant increase in demand for efficient automated retail solutions. Automated vending machines, self-service kiosks, and self-checkout systems, among other AI-driven devices and solutions, are becoming more common in various retail stores. These solutions offer many advantages, including improving efficiency, reducing labor costs, and facilitating customers. In addition to traditional automated retail solutions, new technologies such as artificial intelligence and machine learning are also being integrated into AI-driven devices and solutions to create more advanced solutions, tailoring shopping experiences for each customer, including personalized recommendations, targeted advertising, and consumption pattern prediction. In summary, the demand for efficient automated retail solutions is likely to continue increasing, thereby driving the development of AI-driven devices and solutions.

● Reduce operating costs

AIDC devices and solutions can significantly reduce retailers' operating costs. By automating operational processes, retailers can save labor costs and improve efficiency, thereby enhancing profitability. For instance, self-service checkout systems equipped with intelligent POS terminals can reduce the need for cashiers, saving retailers a substantial amount of labor costs. In addition, retailers can also obtain data from specialized printers and POS terminals, among other automated retail devices, to optimize inventory levels and reduce waste. In summary, reducing operating costs is one of the main advantages that AIDC devices and solutions bring to retailers. By implementing such solutions, retailers can enhance profitability and maintain competitiveness in the ever-changing retail environment.

● More intelligent manufacturing plants and warehouses have been established

Intelligent warehouses are becoming increasingly popular in the retail industry. These warehouses utilize advanced technologies such as automation, robots, and IoT sensors to improve operational efficiency, reduce costs, and strengthen inventory management. These technologies can automate tasks such as sorting and packaging, inventory management, and shipping, which can significantly reduce labor costs and improve efficiency. Sensors can track product locations and monitor their condition, helping retailers detect potential issues such as product expiration or damage. The collected data can also assist retailers in optimizing shipping routes, reducing the need for multiple trips, thereby lowering transportation costs. In 2022, the Chinese government issued the "14th Five-Year Plan for Intelligent Manufacturing Development," proposing that by 2025, most manufacturing enterprises should achieve digitization, and major manufacturers should gradually integrate artificial intelligence into production. This plan requires the joint efforts of the government, research and development companies, academia, and industry. As part of the strategic development of smart factories, AIDC device manufacturers adopt key technologies such as robots and computer numerical control machine tools, using the core advantages of these technologies to improve production efficiency, ensure product quality, and reduce costs. In addition, by adopting predictive maintenance technology combined with enterprise resource planning, AIDC device manufacturers can automatically closely monitor inventory levels and utilization rates.

●AIIDC technology plays a key role in digitalization and data management across various industries

The healthcare industry and several other sectors are accelerating the digitization and effective data management, which has become a major catalyst for deploying AIoT devices. In healthcare, key requirements such as accurate patient record storage, secure medication dispensing, and compliance with strict privacy regulations are driving the integration of specialized printers and PDAs. Similarly, in the hospitality industry, AIoT technologies such as mobile POS systems enable service providers to offer personalized and efficient services directly to guests, thereby improving overall customer satisfaction. In addition, growing industry sectors such as event management also utilize these devices to simplify registration, attendee tracking, and access control, demonstrating the multifunctionality and expanding practicality of AIoT devices in various service-oriented industries.

● The sustainable development of the education industry is conducive to portable learning printers

Private education in China is experiencing significant growth, especially in tutoring classes, online tutoring, and training institutions. To support this booming development, education companies are investing in high-quality teaching resources and integrating advanced technology into their operations. Portable learning printers are a notable innovation in this field, and their relationship with the education industry is becoming increasingly close. Portable learning printers are designed to be compact and easy to carry, tailored for educational environments, allowing students to print out learning materials and question sets directly and in real-time in their study space or classroom. They facilitate real-time feedback on students' homework, enabling them to spot and correct mistakes on the spot, thereby enhancing their learning experience. The convenience of pocket-sized printers helps students efficiently review wrong questions and consolidate their understanding of subject knowledge. Therefore, portable learning printers are expected to emerge as a practical tool that integrates physical and digital learning fields, and this niche market is expected to continue growing.

competitive landscape

● Rankings and market share

The global market for AIDC devices is relatively fragmented, with mature leaders in each sub-market (including POS terminals, PDAs, specialty printers, and scales) in terms of business and product model development. In recent years, the rapid development of retailing, coupled with continuous advancements in digital technology, has driven demand for AIDC devices in the Asia-Pacific region. At the same time, many device manufacturers and shipments from countries such as China and Japan are also expanding continuously, allowing the region to occupy a significant market share in the global AIDC device market.

China is a major market in the Asia-Pacific region, accounting for about 16.6% of the global market share in 2023. The Chinese market is fragmented, with over 2,500 operators. Chinese market operators can be roughly divided into (i) international companies; or (ii) domestic companies, and can be further subdivided according to the scope of services they provide within the value chain of AIDC device solutions.

The competition in the Chinese specialized printer market is quite fierce, with more than 300 industrial enterprises above designated size participating. The earnings of the top ten companies account for 28.0% of the entire market. In 2023, the group ranked ninth with earnings of RMB 1.538 billion, accounting for 1.8% of the overall Chinese specialized printer market. At the same time, in terms of market share, the group was the second-largest specialized printer supplier in Fujian Province, China, in 2023.

Source: Frost & Sullivan report

Entry barriers

● Brand and project track record

Existing AIDC device and solution suppliers typically have a record of successfully delivering projects and have established a good reputation. New market entrants do not have a precedent of successful marketing, and the requirement for performance records and reputation can become an entry barrier for them. Having a good record of performance indicates that AIDC device and solution suppliers have extensive technical capabilities and experience, which is also clear evidence of their competitive advantage in participating in complex large-scale projects. However, establishing a good image takes a long time, making it a major obstacle to entering the market.

● Qualification threshold

Due to the importance of payment security and technological patents, the AIDC device industry has established specialized quality certifications and standards for manufacturers' procurement and production, with some certification processes taking considerable time. In addition, the complexity of qualification certifications varies among customers from different industries, such as credit card organizations, acquiring institutions, or retail chains. Customers generally focus on examining the manufacturer's financial condition, operational status, quality system, and technical level, among other standards. Specifically, large enterprises usually select product solutions through bidding, while new entrants may not be able to obtain certification quickly, posing a significant obstacle to them.

● Market tips

AIDC device and solution providers need to deeply understand local market nuances in order to design services for specific regions, thereby improving retailers' operational efficiency and reducing costs. As consumer trends and digital technology continue to change, AIDC device and solution providers must have strong management teams, possess professional knowledge, and understand the market to meet the ever-changing market demands in inventory management, mobile payments, and even data analysis. Electronic payment terminals and specialized printers are carriers for collecting and generating data and play an important role in retailers' daily operations. Therefore, manufacturers must continuously update technology and optimize functions to meet market needs. New market entrants lack relevant market expertise and cannot easily win the favor of major retailers.