Frost & Sullivan

Jiaxin International Resource Investment Co., Ltd. (Stock Code: 3858.HK) successfully listed on the main board of the Hong Kong capital market on August 28, 2025. The company is the world's largest open-pit tungsten mine with tungsten trioxide (WO3) resources and its Bakhtala tungsten mine is the world's fourth-largest tungsten mine (including both open-pit and underground mines) in terms of WO3 resources, possessing the world's largest designed tungsten production capacity from a single tungsten mine. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provided exclusive industry advisory services for the listing of Jiaxin International Resource Investment Co., Ltd. and hereby warmly congratulate them on their successful listing.

Jiaxin International Resources Investment Co., Ltd. (hereinafter referred to as 'Jiaxin International') successfully went public on August 28, 2025. The company plans to issue approximately 110 million shares globally, including 10.9812 million shares in Hong Kong, China, 98.8376 million shares internationally, with an additional about 15% in the form of over-allotment rights.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support and highlight the issuer's competitive advantages, assisting the issuer, investment banks and other intermediaries in completing the writing of relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

Frost & Sullivan has always been a leader in helping companies go public in Hong Kong. According to LiveReport's big data (statistical data as of June 30, 2025), from January to June 2025, and during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 29 (market share 71%), 60 (market share 67%), and 164 (market share 69%) Hong Kong IPOs, ranking first in terms of number. It has a wealth of industry experience and communication skills with regulatory authorities, exchanges, investment and financing institutions, and various related agencies.

PART/1

Investment Highlights

-

The company holds the exclusive mining rights (the right to explore and mine tungsten ore) to the Bakutai tungsten mine (an open-pit mine located in the Almaty region of Kazakhstan);

-

The company has favorable conditions and is seizing the global demand for tungsten and tungsten products;

-

The company's Bakhtyut tungsten mine is located in a commercially advantageous geographical location and benefits from the support of Kazakhstan's initiative to join the Belt and Road Initiative with China;

-

The company has an experienced management team with valuable industry and management expertise;

-

The company fulfills its social responsibilities and endeavors to achieve sustainable development through continuous ESG efforts;

-

The company's shareholders possess rich industry experience, laying a solid foundation for business growth and expansion.

According to the Frost & Sullivan report, in terms of mineral resources for 2024, the company:

-

The world's largest open-pit tungsten mine with tungsten trioxide (WO3) resources;

-

The company's Bakutai tungsten mine is also the world's fourth-largest tungsten mineral resource producer (including open-pit and underground mines), with the largest designed tungsten production capacity in a single tungsten mine.

PART/2

Overview of the Tungsten Industry Globally, China and Kazakhstan

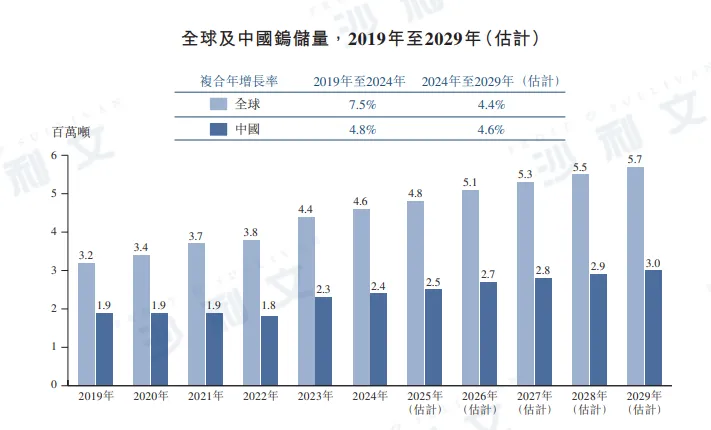

The global tungsten ore resources are unevenly distributed, with most reserves located in China, Russia, Kazakhstan, and other regions. Most super-large deposits are situated in important metallogenic belts. The world's top five tungsten mines for 2024 are the Dahutang Tungsten Mine and Shizhuyuan Tungsten Mine in China, the Hemerdon Tungsten Mine in the UK, the Bakhuta Tungsten Mine in Kazakhstan, and the Sisson Tungsten Mine in Canada. Global tungsten reserves increased from 320 million tons in 2019 to 460 million tons in 2024, with a compound annual growth rate of 7.5%. As countries around the world steadily explore various types of tungsten ore, it is expected that global tungsten reserves will reach 570 million tons by 2029, with a compound annual growth rate of 4.4% from 2024 to 2029. In 2024, China is the largest tungsten reserve country, accounting for more than 50% of global reserves. China's reserves fluctuated from 2019 to 2024, reaching 240 million tons in 2024. In the future, it is expected that China's tungsten reserves will show a slight increase, reaching 300 million tons by 2029, with a compound annual growth rate of 4.6% from 2024 to 2029.

Data source: Analysis by Frost & Sullivan

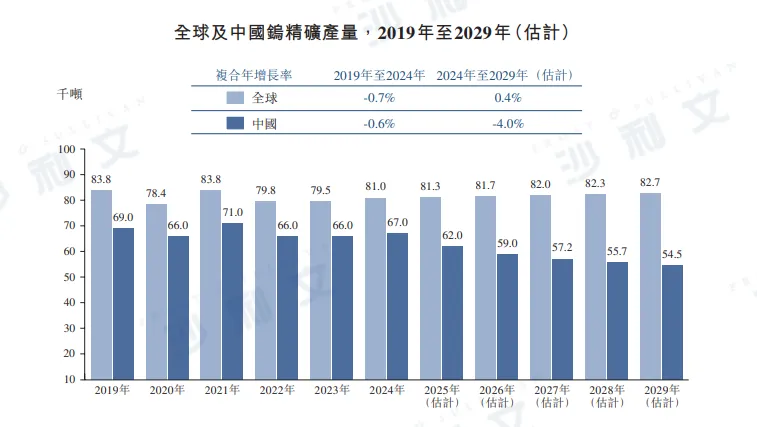

China is the country with the largest tungsten concentrate production in 2024. To protect national reserves, the Ministry of Natural Resources of China issues annual tungsten concentrate mining quotas each year. These quotas have been in effect since 2002. China's tungsten concentrate mining quota for 2024 is set at 114,000 tons of tungsten concentrate. Due to the Chinese government's implementation of limited mining quotas for tungsten concentrate and the relatively low operating rate in previous years, China's tungsten concentrate production decreased from 69,000 tons in 2019 to 67,000 tons in 2024, with a compound annual growth rate of -0.6%. The market expects domestic tungsten concentrate production to reach 54,500 tons in 2029, with a compound annual growth rate of -4.0% from 2024 to 2029.

Source: USGS, Ministry of Natural Resources of China, Frost & Sullivan analysis

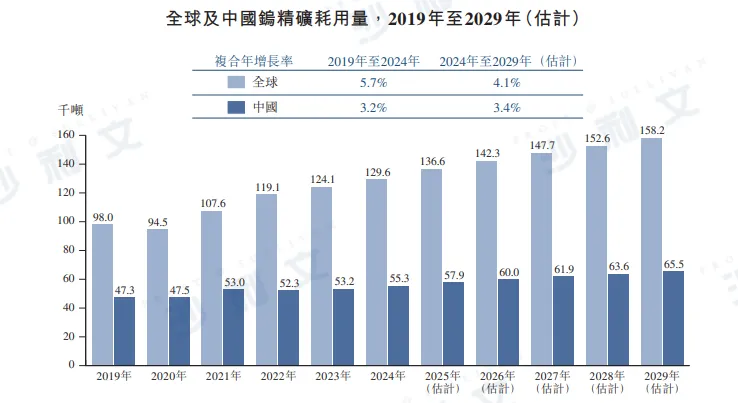

Due to the natural characteristics of tungsten and its widespread use in different regions, the consumption of tungsten concentrate increased from 98,000 tons in 2019 to 129,600 tons in 2024, with a compound annual growth rate of 5.7%. Looking ahead, with the rapid growth of downstream markets and the continuous increase in tungsten consumption, such as in the photovoltaic (PV) industry which also consumes a large amount of tungsten, it is expected that the consumption of tungsten concentrate will reach 158,200 tons in 2029, with a compound annual growth rate of 4.1%. China's consumption of tungsten concentrate increased from 47,300 tons in 2019 to 55,300 tons in 2024, with a compound annual growth rate of 3.2%. Looking ahead, with the continuous development of technology and demand for tungsten (especially in the field of cemented carbide products), it is expected that China's consumption of tungsten concentrate will reach 65,500 tons in 2029, with a compound annual growth rate of 3.4%. As the Chinese economy steadily grows, the consumption of tungsten concentrate in different industries continues to increase. Compared with other materials, tungsten has an overwhelming competitive advantage, leading to rapid development of the tungsten market. For example, tungsten is often made into cemented carbide products and is widely used in many industries such as aerospace, military, and PV (photovoltaic). Tungsten and tungsten wires can be used to produce materials with high hardness, wear resistance, and corrosion resistance. With the foreseeable capacity expansion and large-scale application, the cost-effectiveness of tungsten wires will be higher than carbon steel wires, making them a reliable alternative product in the PV industry. Before 2022, the consumption of tungsten concentrate will grow steadily, with a compound annual growth rate of 3.5% from 2018 to 2021. In the foreseeable future, with the continuous demand from downstream industries, the compound annual growth rate of China's tungsten concentrate consumption from 2024 to 2028 is expected to be about 3.4%.

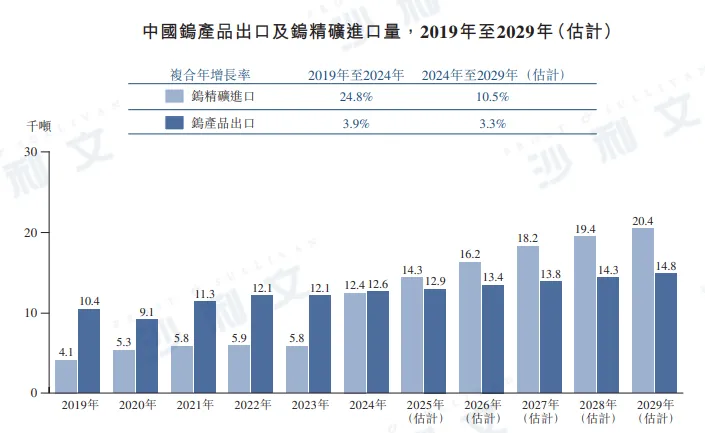

China has implemented a policy to restrict the export of tungsten concentrate in order to protect domestic tungsten resources and ensure their sustainable supply. In recent years, with the gradual depletion of tungsten resources in China and the increasing awareness of environmental protection, the Chinese government has taken a series of measures to limit the export of tungsten concentrate. According to the regulations of the Ministry of Commerce of the People's Republic of China, enterprises must possess the qualification to export tungsten ore, and the Ministry of Commerce discloses which enterprises are eligible to export each year. After review, there are 15 qualified and compliant enterprises for the year 2024. China has a vast capacity for tungsten product smelting and processing, yet to protect tungsten resources, China implements an annual quota system for domestic tungsten concentrate production. As a result, China has become a major importer of tungsten concentrate and exports a large amount of smelted and processed tungsten products. Due to the continuous development of China's tungsten processing industry and tungsten smelting technology, China's tungsten exports have gradually shifted from primary tungsten products such as tungsten trioxide and tungsten carbide to downstream products with high production added value such as cemented carbide. China is the country with the largest tungsten concentrate production in 2024. At the same time, by volume of tungsten product exports, China is also a major supplier of tungsten products in 2024. In 2024, China's tungsten product exports accounted for about 40% of global consumption outside China. The export volume of downstream tungsten products increased from about 10,400 tons in 2019 to 12,600 tons in 2024 and is expected to increase to about 14,800 tons by 2029. Tungsten is considered an important strategic mineral, and China has reserved a portion of its tungsten concentrate production each year over the historical period. Therefore, although China's tungsten concentrate production has been higher than its consumption over the historical period, it has not used all of its produced tungsten concentrate to produce tungsten products and has been importing more and more tungsten concentrate to meet its consumption needs. In addition, due to the overall continuous reduction of domestic tungsten concentrate production and the overall continuous increase in domestic tungsten concentrate consumption, the surplus between domestic tungsten concentrate production and consumption is continuously narrowing, expected to turn into a shortage around 2026, leading to further increased import demand for tungsten concentrate. Furthermore, due to the huge domestic consumption demand for tungsten concentrate and the export demand for tungsten products made from tungsten concentrate, it is expected that the import volume of tungsten concentrate will increase from 12,400 tons in 2024 to 20,300 tons in 2029. Therefore, there will be strong demand for tungsten concentrate imported from Kazakhstan in the future.

Source: China Tungsten Industry Association, Frost & Sullivan analysis

Note: The export volume of tungsten products refers to tungsten products made from tungsten concentrate as raw material.

Source: Ministry of Natural Resources of China, Frost & Sullivan analysis

Note: The consumption of tungsten concentrate refers to the consumption of metallic tungsten.

China is the world's largest producer and consumer of tungsten. The price of tungsten concentrate in China usually reflects domestic policies and downstream consumer demand. The environmental regulations and mining policies of the Chinese government have a direct impact on tungsten supply, leading to price fluctuations. In addition, changes in demand from major industries such as aviation, automotive, and electronics in China can also drive price changes. Globally, tungsten prices are affected by a wide range of factors. Price fluctuations in tungsten concentrate in China and globally have an impact on multiple industries and economies around the world. Tungsten is an important metal known for its exceptional hardness and high melting point, making it indispensable in a variety of applications, especially in manufacturing, aviation, defense, and electronics. Tungsten reserves are not as abundant as other metals, and production is concentrated in a few countries. Any interruption in the supply chain, such as mining problems or geopolitical tensions, can lead to soaring prices. Global tungsten concentrate supply is concentrated in a few major producing countries such as China, Russia, and Canada. Production disruptions caused by geopolitical tensions, natural disasters, or labor strikes can lead to price spikes. In addition, demand for tungsten is closely related to the global economic situation. During economic growth, industries that rely on tungsten (such as manufacturing and construction) drive up demand, thereby driving up prices. The price of ammonium metatungstate (AMT) in China and globally has fluctuated in the past, but has generally shown an upward trend from 2017 to 2024. AMT is an important material in the tungsten smelting industry, mainly used to produce tungsten trioxide or blue tungstate to make metallic tungsten powder, which is then used to manufacture tungsten materials, tungsten alloys, and other products. Due to restrictions on the production of raw material tungsten concentrate for manufacturing AMT, domestic production pressure has increased, leading to continuous price increases in AMT, which has also led to rising prices of downstream products such as tungsten carbide. From early 2017 to mid-2018, due to stricter environmental supervision by the Chinese government, the price of AMT in China rose. At the same time, prices of tungsten carbide and tungsten concentrate also increased. In 2020, due to global supply shortages and energy resource limitations, the price of AMT also rose during this period. Looking ahead, as the world economy gradually recovers from COVID-19, downstream market demand for tungsten is expected to gradually recover, and demand for AMT, tungsten carbide, and tungsten concentrate is expected to continue growing. In this context, it is expected that prices in China and globally will increase again in the short term and show an upward trend in the long term.

PART/3

Competitive landscape of tungsten industry globally, in China, and in Kazakhstan

According to a Frost & Sullivan report, Bacta tungsten mine is the world's fourth-largest single tungsten mine, with mineral resources amounting to 0.23 million tons and ranking first in terms of designed production capacity. Bacta tungsten mine is a world-class large-scale open-pit tungsten mine and also the largest developing tungsten concentrate outside China as of December 31, 2024.

Data source: Analysis by Frost & Sullivan

PART/4

Global, Chinese and Kazakhstanian Tungsten Industry Drivers

● The rarity of non-ferrous tungsten resources and continuous innovation in mining technology

Tungsten is a scarce material with excellent characteristics such as high melting point, high density, high hardness, high wear resistance, and stable chemical behavior. Tungsten products are commonly used in various fields including machinery manufacturing, power resources, and defense industry. Tungsten reserves increased from about 320,000 tons in 2019 to 460,000 tons in 2024, with a compound annual growth rate of 7.5%. In 2024, global tungsten production was about 81,000 tons, while global tungsten consumption was about 129,600 tons, resulting in a gap of as high as 48,600 tons, reflecting the scarcity and strong demand for tungsten resources. Although global tungsten resources are widely distributed in different regions, China currently holds the lead in tungsten resources and reserves, accounting for more than 50% of global tungsten resources and reserves. China implements a total mining quota for tungsten to control its exploitation, which is uniformly planned and allocated by national departments for the mining of tungsten resources in various regions. In addition, Canada, Kazakhstan, and Russia also possess relatively rich tungsten resources. With technological progress and continuous reserve growth, continuous innovation in mining technology will become the main factor for the growth and development of the tungsten industry to match the relatively scarce tungsten resources, production, and steadily rising tungsten consumption.

● The demand for tungsten from downstream industries is constantly increasing

With the steady growth of the global economy, tungsten consumption in different industries continues to increase, and global tungsten consumption is expected to reach 158,200 tons by 2029. Tungsten is commonly made into cemented carbide products and is widely used in many industries such as aerospace, military, and PV (photovoltaic) industry. Tungsten and tungsten wires can be used to produce materials with high hardness, wear resistance, and corrosion resistance. With foreseeable capacity expansion and large-scale application, the cost-effectiveness of tungsten wire will be higher than that of carbon diamond wire, making it a reliable alternative product for the photovoltaic industry. In addition, tungsten carbide tools are widely used in computer numerical control (CNC) lathe tools. CNC lathe tools require high-hardness, wear-resistant, and high-temperature resistant tools to meet the needs of high-speed cutting and heavy-duty processing. As one of the main components of cemented carbide, tungsten can provide excellent hardness and wear resistance, making tools more durable and having a longer lifespan. In addition, cemented carbide drills are a common industrial cutting tool used for drilling holes in metals, wood, plastics, and other materials. Tungsten carbide particles make tungsten carbide drills hard and wear-resistant, enabling them to effectively cut under high rotational speed and heavy load. In addition, cemented carbide drills have good cutting stability and a long service life, suitable for various drilling applications. Compared with other materials, tungsten has an overwhelming competitive advantage, leading the rapid development of the tungsten market.

● Technological progress in mining processing and smelting

In the development process of tungsten smelting technology, before 1980, soda sintering, hydrochloric acid decomposition (used for high-quality scheelite concentrate), soda pressure leaching, and sodium hydroxide decomposition were the main common methods of tungsten ore decomposition globally. From the early 1980s to the late 1990s, sodium hydroxide decomposition methods represented by hot ball milling (mechanical activation) and alkaline pressure leaching achieved transformative breakthroughs. Since then, the vast majority of tungsten materials have been processed using sodium hydroxide decomposition methods. In recent years, the synergistic leaching technology of sulfur-phosphorus mixed acid for scheelite has achieved atmospheric-pressure decomposition of tungsten ore. With the development of mining processing and smelting technology, enterprises have continuously increased technological research to improve resource utilization rates, upgrade automated processes, and reduce energy costs. In addition, the progress of mining and processing technology has improved the efficiency and cost-effectiveness of tungsten extraction, making it an attractive market for investors.

● Intelligent technology promotes improved tungsten utilization efficiency

Tungsten is a scarce, non-renewable strategic resource on a global scale. Therefore, the recycling and utilization of tungsten are also very important. With the widespread adoption of intelligent mining and mineral processing, the overall utilization rate of tungsten has been increasing over the past few years. Today, enterprises can use intelligent technology to mine tungsten ore efficiently and safely. An intelligent system can track tungsten mines or deposits around the clock, ensuring safety and productivity, thereby improving the overall utilization rate of tungsten. Therefore, the industry's deployment of intelligent technology is one of the main driving factors for the tungsten market.

● Favorable policies of the governments of China and Kazakhstan

In 2022, Kazakhstan celebrated the 30th anniversary of its establishment of diplomatic relations with China. Over the past 30 years, the two countries have established a permanent and comprehensive strategic partnership, laying a solid foundation for strengthening friendly relations and further deepening mutually beneficial cooperation. Kazakhstan was one of the first countries to propose the Belt and Road Initiative. The work on jointly building the Belt and Road Initiative between China and Kazakhstan has achieved fruitful results, with about 45 capacity cooperation projects established between the two countries. China and Kazakhstan have signed the "Cooperation Plan on the Integration of the Construction of the Silk Road Economic Belt with the New Economic Policy of the 'Bright Path'." Among the list of China-Kazakhstan cooperation projects, investments in the oil and gas sector account for about half, with the rest distributed in industries such as mining and ore processing, machinery manufacturing, energy, and food production. The joint construction of the Belt and Road Initiative between China and Kazakhstan has injected new vitality into China-Kazakhstan cooperation and promoted the coordinated development of the tungsten mining industry at the policy level. Under the Belt and Road Initiative, the Baku-Tashkent tungsten mine project, as a key project within the capacity cooperation framework between China and Kazakhstan, provides a platform for joint exploration and development cooperation between China and Central Asian countries. In addition, the government of Kazakhstan has also promulgated a number of favorable regulations and plans for the mining industry. For example, the "Kazakhstan 2050 Development Strategy" is a strategic plan issued by the government of Kazakhstan in 2012, aiming to identify new markets where Kazakhstan can form productive partnerships and create favorable investment environments. Since China has established long-term cooperative partnerships with Kazakhstan, such preferential policies have provided a friendly environment for Chinese enterprises operating in Kazakhstan and promoted the development of the tungsten mining industry in both China and Kazakhstan. Moreover, the mining industry is the pillar of the national economy of Kazakhstan. By 2024, the mining industry in Kazakhstan accounted for about 50% of the total industrial output value.

PART/5

Tungsten industry development trends globally, in China and Kazakhstan

●Innovation in tungsten waste recycling and reuse

Currently, most leading enterprises in the tungsten industry can complete the preparation and mining of tungsten. However, in order to make better use of global tungsten resources, leading enterprises not only need to mine tungsten but also recycle and reuse tungsten waste. It is expected that leading enterprises will introduce low-cost, high-efficiency methods for tungsten waste recycling. As the growth of tungsten resources slows down, leading enterprises are no longer simply consuming tungsten resources but are paying more attention to the recycling and reuse of tungsten waste. Currently, about 75% of the global tungsten supply comes from primary tungsten, with only the remaining 25% coming from recycled tungsten. Although the initial investment in advanced technology is relatively high, this technology can significantly improve the efficiency of tungsten resource recycling and reuse, thereby gradually reducing the operating costs of mining enterprises. Due to the strategic importance and scarcity of tungsten, many leading enterprises attach great importance to the recycling of tungsten waste. In recent years, the supply share of recycled tungsten has been increasing and will continue to be a future development trend in the tungsten industry.

●Technological upgrades bring more tungsten application areas

With technological upgrades, leading enterprises can produce more refined products. Taking China as an example, some leading tungsten companies have introduced advanced technologies and equipment, absorbed, transformed, and independently developed them, achieving localization of key equipment such as spray drying and gas pressure sintering. In the future, with the continuous improvement of the tungsten industry's technical level, it is expected that some leading enterprises' tungsten deep-processing products will include more specifications in terms of thickness, width, length, density, etc. Such advanced tungsten products will gradually develop towards high performance, high precision, and high added value. Therefore, technological upgrading is an opportunity for large enterprises in the future.

●Sustainable mining practices

In the future, the industry will pay more attention to sustainable mining practices, including reducing environmental impact and promoting responsible resource extraction. This may involve using advanced technology for efficient mining, implementing strict environmental regulations, and promoting the reclamation of mines. Compared to underground mining, open-pit mining has better resource utilization rates, higher recovery rates, higher production volumes, higher labor productivity, and lower costs. Therefore, open-pit mining is more sustainable and will become the main trend of the industry in the future.

PART/6

Global, Chinese and Kazakhstanian tungsten industry entry barriers

●Exploration and mining capacity barriers

Exploration and mining capabilities are crucial for the tungsten industry, and industry participants need to accurately identify the specific location, mining methods, and economic value of tungsten ore. For example, some mines show prospecting potential in deeper parts, requiring intensified deep search based on geological research; some mines have large reserves but low exploration depth, far from meeting mining needs; and some mines have been depleted and are on the verge of closure, urgently needing to explore deep ore-forming mechanisms and make clear geological conclusions. Therefore, new entrants in the industry will take a long time to develop their exploration and mining capabilities.

●product quality barrier

As downstream customers increasingly focus on tungsten raw materials, product quality has become one of the main barriers to entering the tungsten industry. Major domestic and international high-end tungsten carbide manufacturers have strict requirements for their main raw materials, ultra-fine and ultra-thick tungsten carbide resources. For example, ultra-fine tungsten carbide requires small particle size, high purity, and a narrow particle size distribution. Companies that do not meet these quality requirements will gradually be phased out. In addition, downstream customers particularly emphasize the stability of product quality. If a company cannot continuously provide products with stable quality, it will find it difficult to survive and develop in the tungsten market.

●technical barriers

With the development of global tungsten technology, tungsten products tend to be characterized by high performance, high precision, and high added value. This trend has put forward higher technical requirements for companies entering the tungsten industry, such as the gradual application in nanomaterials, nanostructured coatings, coating technology, etc. Tungsten carbide cemented carbide tools have high technical standards and requirements for the powder form, chemical purity, and particle size of their main raw material, tungsten carbide. Therefore, new companies entering this industry need to continuously overcome relevant technical barriers.

●capital investment barriers

The tungsten industry requires sufficient capital investment. This is mainly because mining requires a large amount of upfront capital investment, as it takes several years for mines to start production and earn profits. During this process, exploration will be costly, requiring the purchase of geological exploration equipment, mining equipment and infrastructure, as well as hiring a large workforce. In addition, sufficient capital is also crucial for companies engaged in the tungsten industry to establish and maintain their leading market position. Therefore, new entrants lacking sufficient capital may find it difficult to enter the industry.

●talent barrier

The tungsten industry has higher requirements for talents in all aspects. During the production process, production personnel need to accurately control the key parameters of each technological process. Therefore, the company needs to have a variety of talents with many years of experience in the tungsten industry. The industry's demand for talent is not only about professional knowledge but also requires experience. Currently, there are not many professionals in the tungsten industry, and the talent training cycle is long. Finding professional talent may become one of the difficulties faced by new entrants.

●Barriers to prospecting and mining licenses

Tungsten ore is a specific mineral species that is mined under government supervision in China. To protect and rationally develop and utilize advantageous mineral resources, the Chinese government has continuously postponed the acceptance of new mining exploration and exploitation registration applications. The Ministry of Natural Resources of China mainly determines the total annual mining volume indicators based on the national mineral resource plan, and combines factors such as national industrial policies, ecological environment protection, remaining resource reserves, mining rights, and mining capacity to determine the annual total mining volume indicators for tungsten ore, which are then allocated to provincial natural resources authorities. For new entrants in this industry, the lack of exploration and mining licenses as well as the difficulty in obtaining mining quotas may become serious obstacles.

PART/7

The tungsten markets globally, in China, and in Kazakhstan are facing challenges

●Rising operating costs and heightened environmental awareness

Labor force is an important factor in the tungsten industry. With economic development, labor costs in China and Kazakhstan have been rising in recent years. The average annual salary of employees in the mining industry in China and Kazakhstan has increased from about $12,700 and $9,600 in 2019 to about $20,900 and $19,800 in 2024, with compound annual growth rates of 14.0% and 10.5%, respectively. In recent years, the number of employees in the mining industry has shown a downward trend. In addition, raw material prices used for the production of downstream products also affect the tungsten industry. For example, liquid sodium hydroxide and sulfuric acid are the main raw materials for producing downstream tungsten products, and their price increases in 2021 significantly raised the prices of tungsten products. Moreover, the growing global awareness of ESG policies and environmental protection will also pose obstacles to the mining industry, as mining enterprises often face potential environmental damage issues.

●Uncertainty in the world economic situation

The uncertainty of the world economic situation will also have a certain impact on the tungsten mining industry. In terms of tungsten reserves and production, Russia is a major tungsten-producing country. The Russia-Ukraine war led to short-term fluctuations in the tungsten market. When the war state was in place, Russia was expected to use most of its domestic tungsten reserves to prepare weapons. The shortage of Russian supply led to a reduction in global tungsten supply and increased prices for tungsten products. When the conflict situation is alleviated and can meet short-term reserve and operational needs, the price of tungsten resources may return to normal levels.

Click at the end of the articleRead the original text View the full prospectus

Frost & Sullivan has extensive research experience in the chemical and materials industries, assisting well-known enterprises in successfully listing on the capital market. Successful listings include: Nanshan Aluminum (2610.HK), Chifeng Gold (6693.HK), Biyou Group (9893.HK), Conch Materials Technology (2560.HK), Qiangbang New Materials (001279.SZ), Migao Group (9879.HK), Jihai Resources (2489.HK), Zhongbao New Materials (2439.HK), Shengneng Group (2459.HK), Jinli Yongcime (6680.HK), Avia Avian (IDX: AVIA), Global New Materials (6616.HK), Dafeng Equipment (2153.HK), Yihai International (8659.HK), GHW (9933.HK), Sanhe Fine Chemicals (0301.HK), Xingyu Holdings (2346.HK), Xinghe Holdings (1891.HK), Xuyang Group (1907.HK), Long Resources (1712.HK), Shandong Gold (1787.HK), Henan Jinma (6885.HK), Xingye New Materials (8073.HK), Dongguang Chemicals (1702.HK), Zhongqi Group (1932.HK), Xinbang Holdings (1571.HK), Meigu Technology (8349.HK), Huajin International (2738.HK), Flater Glass (6865.HK), Dynos (1452.HK), Caike Chemicals (1986.HK), Chang'an Renheng (8139.HK), Sansida (1337.TWSE), Born.NYSE, CPC.NYSE, Gu N.YSE, Tianhe Chemicals (1619.HK), Yihua Holdings (2121.HK), Sijia Group (1863.HK), etc.

Recommended Reads (scroll up and down for more)

Frost & Sullivan assists Chifeng Gold in its listing on the Hong Kong Stock Exchange (6693.HK)

Frost & Sullivan assisted Avia Avian in successfully going public in Indonesia (IDX: AVIA)

Frost & Sullivan assists Easergy International in successfully going public in Hong Kong (8659.HK)

Frost & Sullivan assists GHW in successfully listing on the Hong Kong Stock Exchange (9933.HK)