Frost & Sullivan

Shuangdeng Group Co., Ltd. (Stock Code: 6960.HK) successfully listed on the main board of the Hong Kong capital market on August 26, 2025. The company is a leading provider of energy storage services in the fields of big data and communications, focusing on the design, research and development, manufacturing, and sales of energy storage batteries and systems. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provides exclusive industry advisory services for the listing of Shuangdeng Group Co., Ltd., and hereby warmly congratulates them on their successful listing.

Shuangdeng Group Co., Ltd. (hereinafter referred to as 'Shuangdeng Group') successfully listed on August 26, 2025. The company issued a total of 5,855.70 million shares, of which 90% were international offerings and 10% were public offerings. The issue price per share was HK$14.51, and the net proceeds raised were approximately HK$850 million.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support and highlight the issuer's competitive advantages, assisting the issuer, investment banks and other intermediaries in completing the writing of relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

Frost & Sullivan has always been a leader in helping companies go public in Hong Kong. According to LiveReport's big data (statistical data as of June 30, 2025), from January to June 2025, as well as during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services to 29 (accounting for 71% of the market share), 60 (accounting for 67% of the market share), and 164 (accounting for 69% of the market share) Hong Kong-listed IPOs respectively, ranking first in terms of number. It has rich industry experience and communication skills with regulatory authorities, exchanges, investment and financing institutions, and various related agencies.

PART/1

Investment Highlights

-

According to a Frost & Sullivan report, ranked first in global shipments among communication and data center energy storage battery suppliers by new installed capacity in 2024, with a market share of 11.1%;

-

The company is a global leader in data center and communication base station energy storage battery solutions. As of December 31, 2024, the company has served five of the world's top ten telecom operators and equipment manufacturers, nearly 30% of the world's top hundred telecom operators and equipment manufacturers, as well as five major telecom operators and equipment manufacturers in China. The company serves 80% of China's top ten self-owned data center enterprises and 90% of China's top ten third-party data center enterprises;

-

The company has strong R&D capabilities, creating products with high security, cost-effectiveness, and superior performance;

-

The company has excellent manufacturing and operational capabilities;

-

The company has a loyal and high-quality customer base that trusts the brand, as well as an experienced and forward-looking management team.

PART/2

Overview of Global and China's Energy Storage Markets

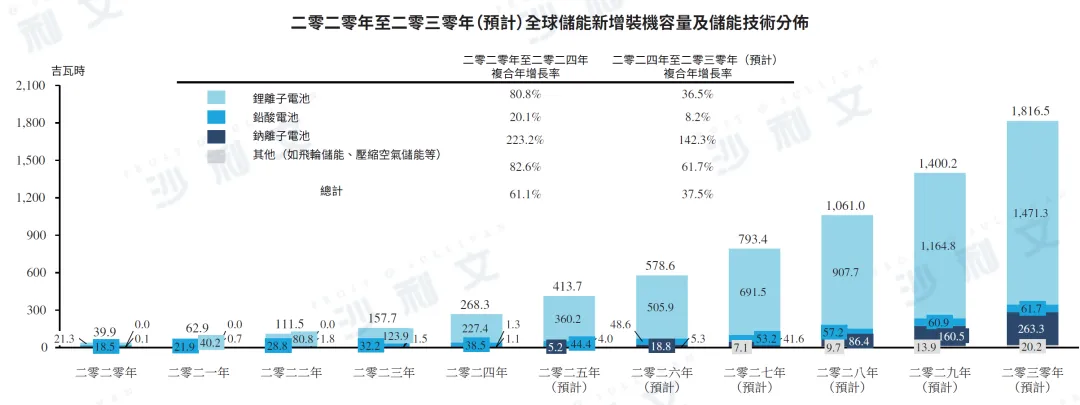

Energy storage refers to the storage of electrical energy, including technologies and measures that use chemical or physical methods to store electrical energy and release it when needed. Energy storage technologies mainly include electrochemical and mechanical energy storage technologies. Electrochemical energy storage technologies can be further divided into types such as lithium-ion batteries, lead-acid batteries, and sodium-ion batteries. Mechanical energy storage technologies can be further divided into flywheel energy storage and compressed air energy storage. Energy storage technologies are widely used in communication and data centers as well as on the power side, which is further divided into the power source side and the user side. In 2024, calculated based on new installed capacity, the global energy storage market size was about 268.3 gigawatt-hours. Electrochemical energy storage technologies such as lithium-ion batteries, lead-acid batteries, and sodium-ion batteries accounted for more than 99% of the energy storage market share based on new installed capacity, dominating market development.

Based on new installed capacity, the global energy storage market size increased from 39.9 gigawatt-hours in 2020 to 268.3 gigawatt-hours in 2024, with a compound annual growth rate of 61.1%. Energy storage can meet market demands for stability, cost-effectiveness, and environmental sustainability, playing a key role in the energy strategies of many countries. In addition to enhancing energy self-sufficiency, flexibility, and security, it also helps reduce electricity costs. Therefore, driven by government support policies, falling costs of energy storage batteries, increased application of renewable energy, and improved awareness of energy storage, it is expected that the global energy storage market size based on new installed capacity will increase from 268.3 gigawatt-hours in 2024 to 1,816.5 gigawatt-hours in 2030, with a compound annual growth rate of 37.5%.

Data sources: IEA, China Energy Storage Alliance (CNESA), Frost & Sullivan analysis

PART/3

Overview of Global and China's Communication Energy Storage Markets

The communication and data center industries are highly interconnected in terms of technical foundation, application scenarios, market demand, etc., supporting each other and jointly driving the development of the modern information society. The communication industry is responsible for data transmission and exchange, ensuring the rapid and reliable transmission of information, while data centers process and analyze large amounts of data. Both communication and data centers require extensive infrastructure, high bandwidth, and low-latency network support, and rely on technological innovation and security protection. With the increase in the number of smart devices and network users, market demand drives the development of these two industries, jointly supporting intelligent decision-making, optimizing network efficiency, and improving service quality. The development of the energy storage industry for communication and data centers is crucial for achieving multiple goals, including (i) ensuring the stable operation of data centers and communication networks, preventing data loss and communication interruptions; (ii) improving energy efficiency and reducing energy waste; (iii) reducing operating costs by storing electricity during off-peak hours and using it during peak hours; supporting renewable energy applications, providing stable power supply, and assisting in green development; responding to emergencies and unexpected situations, ensuring business continuity and reliability; and (iv) promoting the development of smart grids, achieving flexible power dispatching and management, and providing more reliable power guarantees for the communication and data center industries.

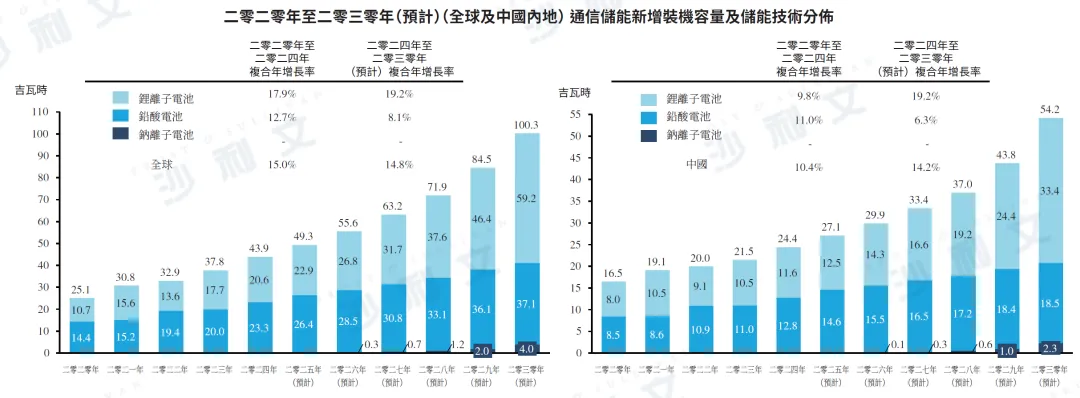

Communication energy storage refers to the use of energy storage systems to provide backup power or supplementary energy to ensure the continuous operation of communication base stations. Energy storage solutions (especially energy storage systems) are crucial for maintaining communication networks during power outages or voltage fluctuations, ensuring uninterrupted connections, and reliable communication services. As of 2024, the cumulative number of 5G communication base stations globally has reached 6.5 million, with a compound annual growth rate of 56.5% compared to 2020. In 2024, China alone accounted for 65.1% of the global cumulative number of 5G communication base stations. According to data from the Ministry of Industry and Information Technology, from 2022 to 2024, the construction volume of new 5G base stations in China decreased from 887,000 to 874,000, resulting in a decrease in the newly installed energy storage capacity for new 5G communication base stations in China and a slowdown in the growth of the 5G communication base station energy storage market in China. In recent years, some countries and regions have experienced power outages, voltage fluctuations, and other unstable power supply issues, affecting the normal operation of communication base stations. To ensure the reliability, stability, and continuity of communication networks, the demand for stable and reliable power supply to base stations has also increased accordingly.

In populous Asia-Pacific countries such as India and Indonesia, due to the rapid deployment of communication base stations and the inadequacy of existing power grids, communication energy storage has become an indispensable infrastructure. Therefore, the new installed capacity of communication energy storage in the Asia-Pacific region (excluding the Chinese mainland) is expected to grow from 10.9 gigawatt-hours in 2024 to 27.9 gigawatt-hours in 2030, with a compound annual growth rate of 16.9%.

In markets in Europe, the Middle East, and Africa, the development of 5G and overall communication industries has been relatively mature and continues to advance. However, the Middle East and Africa regions are still in the early stages of 5G commercialization and have significant development potential. Therefore, the new installed capacity for communication energy storage in Europe, the Middle East, and Africa is expected to increase from 5.4 gigawatt-hours in 2024 to 11.6 gigawatt-hours in 2030, with a compound annual growth rate of 13.7%.

Data sources: CNESA, industry expert interviews, Frost & Sullivan analysis

PART/4

Overview of Global and China's Data Center Energy Storage Market

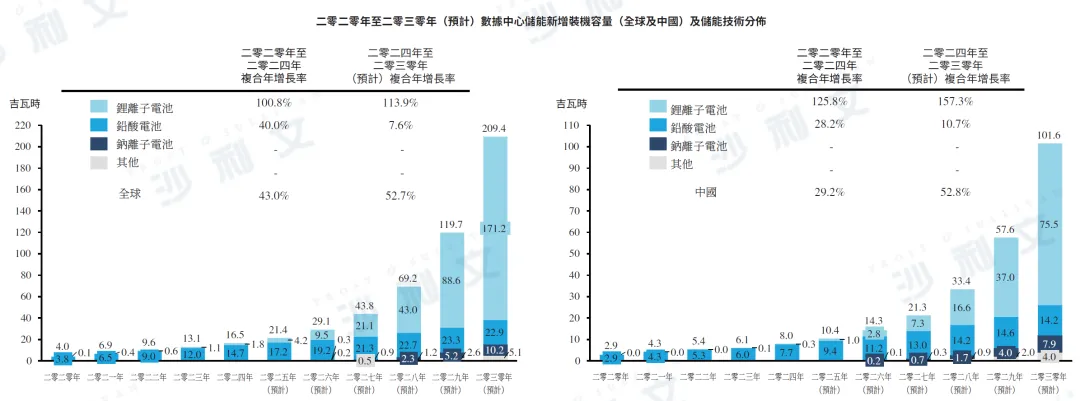

Driven by the rise of artificial intelligence and big data analysis, the energy demand for data centers is increasing day by day, greatly promoting the development of data center energy storage. The complexity and scale of artificial intelligence algorithms are constantly growing, requiring vast computing resources, which has led to a significant increase in energy consumption on traditional and modern computing platforms such as cloud computing and edge computing. The number of global data center racks increased sharply from 12.5 million in 2020 to 33.9 million in 2024, with a compound annual growth rate of 28.3%. With the rapid development of artificial intelligence technology and its continuous expansion in various industries, it is expected that the number of global data center racks will reach 181.3 million in 2030, with a compound annual growth rate of 32.3% starting from 2024. As the main driving force behind global data center expansion, China accounted for 32.2% of the total global data center racks in 2024. With strong government support, it is expected that the number of data center racks in China will reach 61.3 million in 2030, with a compound annual growth rate of 33.3%.

The improvement in computing power of data center racks places a huge pressure on energy demand. The proportion of data center electricity demand in global electricity demand is expected to increase from 4.0% in 2024 to 10.1% in 2030. The surge in energy demand poses challenges to existing energy supply systems, hence the necessity of adopting energy storage technologies to ensure the stability of power supply and improve the energy efficiency of data centers. As the focus in the data center sector shifts towards meeting computing needs while addressing energy challenges, energy storage technologies not only support the stable operation of data centers but also contribute to the broader goal of sustainable power supply by improving energy efficiency and promoting integration with renewable energy. Therefore, the development of the data center energy storage industry is crucial for the sustainable development of data center infrastructure.

In the data center industry, there is an increasing emphasis on configuring energy storage solutions to ensure reliable power supply and improve energy efficiency through sustainable energy sources. The global new installed capacity of data center energy storage increased from 4.0 gigawatt-hours in 2020 to 16.5 gigawatt-hours in 2024, with a compound annual growth rate of 43.0%. It is expected to further increase to 209.4 gigawatt-hours by 2030, with a compound annual growth rate of 52.7% from 2024 to 2030. The new installed capacity of data center energy storage in China increased from 2.9 gigawatt-hours in 2020 to 8.0 gigawatt-hours in 2024, with a compound annual growth rate of 29.2%. It is expected to further increase to 101.6 gigawatt-hours by 2030, with a compound annual growth rate of 52.8% from 2024 to 2030. The accelerated deployment of data centers and the increasing demand for sustainable energy supply will further drive strong growth in the data center energy storage market outside mainland China, as well as in Europe, the Middle East, and Africa. The new installed capacity of data center energy storage in the Asia-Pacific region (excluding mainland China) and Europe, the Middle East, and Africa is expected to increase from 1.7 gigawatt-hours and 1.3 gigawatt-hours in 2024 to 22.1 gigawatt-hours and 10.9 gigawatt-hours in 2030, with compound annual growth rates of 52.7% and 42.8%, respectively.

Data source: Interviews with industry experts, analysis by Frost & Sullivan

PART/5

Overview of the Competitive Landscape in the Global Communication and Data Center Energy Storage Industries

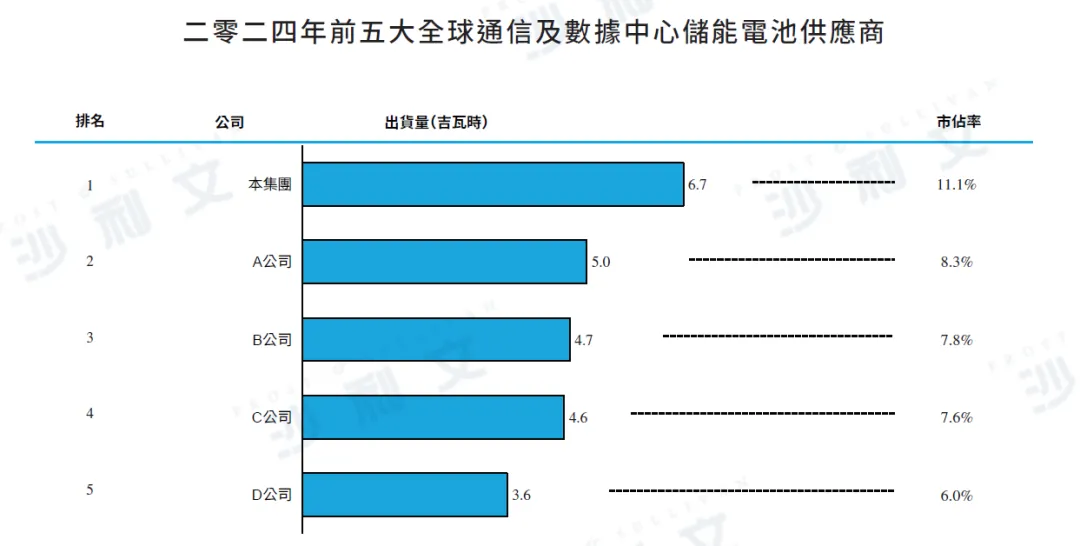

In 2024, the total new installed capacity of energy storage batteries for global communication and data center applications reached 60.4 gigawatt-hours, with the top five manufacturers accounting for approximately 40.7% of the market share. The Group's shipment volume reached 6.7 gigawatt-hours, ranking first among global suppliers of energy storage batteries for communication and data centers, with a market share of 11.1%.

Data source: Interviews with industry experts, analysis by Frost & Sullivan

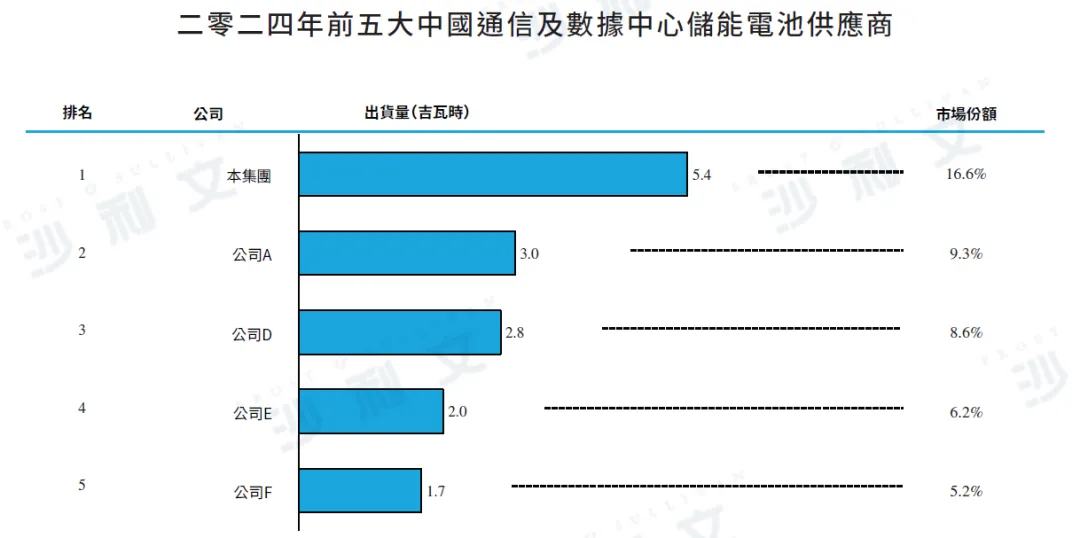

In 2024, the total new installed capacity of energy storage batteries for communication and data center applications in China reached 32.4 gigawatt-hours, with the top five market participants collectively accounting for about 45.9% of the market share. The Group achieved a shipment volume of 5.4 gigawatt-hours, ranking first among Chinese communication and data center energy storage battery suppliers, with a market share of 16.6%. In 2024, the Group ranked first in global communication base station energy storage market shipments, occupying a market share of 9.2% in the global communication market. At the same time, the Group ranked first among Chinese enterprises in global data center energy storage market shipments in 2024, occupying a market share of 16.1% in the global data center market.

Data source: Interviews with industry experts, analysis by Frost & Sullivan

PART/6

Global and China's Energy Storage Market Drivers

Industry demand for communication networks and data centers

In the era of 5G communication, artificial intelligence, and big data, the power demand for communication networks and data centers for the transmission, storage, and processing of large volumes of data has increased significantly, driving the industry's demand for energy storage.

On one hand, the rapid expansion and development of communication networks have driven an increase in demand for communication networks. With the evolution of modern communication infrastructure, the market's demand for energy continues to grow, requiring strong energy solutions to ensure continuous and reliable service delivery. In addition, in the communication energy storage industry, the commercialization and expansion of 5G networks have greatly increased the power demand for communication base stations. 5G technology is known for its ultra-fast response times and extremely low latency (less than one millisecond), making it the mainstream type of base station in markets such as China. By 2030, it is estimated that China will additionally configure 8 million 5G base stations, bringing the total number of communication base stations to about 12.2 million.

On the other hand, due to related workloads such as artificial intelligence (AI) and high-performance computing (HPC), the demand for data centers will increase. Implementing these workloads usually requires replacing racks and backup power infrastructure to ensure efficient, secure, and continuous power supply. In the future, the widespread deployment, accelerated adoption, and application of AI will further accelerate the construction process of data centers. It is expected that the number of data center racks globally will grow from 181 million in 2024 to 2030 at a compound annual growth rate of 32.3%.

Energy transformation aims to shift towards a low-carbon energy system by improving energy efficiency, decarbonizing power generation, and electrifying the economy, in order to achieve net-zero carbon dioxide emissions. Key approaches include transitioning from traditional high-polluting energy sources to renewable energy such as solar, wind, and hydropower. Energy storage technology plays a crucial role in minimizing energy waste caused by fluctuations in renewable energy supply. Energy transformation is a global growth trend. As of the end of 2024, more than 150 countries around the world have committed to achieving carbon neutrality by mid-21st century, covering over 80% of global carbon dioxide emissions. Specifically, China has put forward the 'dual carbon' goal, aiming to peak carbon dioxide emissions by 2030 and achieve carbon neutrality by 2060. The implementation of such initiatives by multiple countries helps accelerate the development of new energy and energy storage markets. Especially in the field of communication and data center energy storage, power costs account for a large portion of data center and communication operating expenses, accounting for about 60% and 30% of their total operating costs respectively. The integration of renewable energy infrastructure such as photovoltaics is reducing power expenditures, while energy storage systems ensure the uninterrupted operation of base stations and data centers.

Regulatory Framework and Government Support Mechanism

Subsidies, tax incentives, and investment financial incentives for energy storage projects can reduce upfront costs and promote market acceptance, thereby driving the adoption and deployment of energy storage systems. In the EU, energy storage plays an important role in the European Green Deal and the "Fit for 55" policy plan, which aim to ensure carbon neutrality. These measures have accelerated the installation of renewable power plants and on-site energy storage facilities. In China, regulatory reforms such as simplifying licensing procedures and grid interconnection standards have further promoted the configuration of energy storage systems, thus accelerating project development and implementation. For example, in August 2021, the National Development and Reform Commission of China and the National Energy Administration issued the "Notice on Encouraging Renewable Power Generation Enterprises to Build or Purchase Peak shaving Capacity to Increase Grid-connected Scale," encouraging power generation enterprises to increase the grid-connected scale of renewable power generation installations by building or purchasing peak shaving energy storage capacity. As of December 31, 2024, more than 20 provinces, autonomous regions, and municipalities directly under the Central Government in China have introduced regional policies related to mandatory deployment of energy storage and renewable energy projects. Communication base station and data center operators, which have abundant site resources and rely heavily on energy storage as backup power, will benefit greatly from this policy. Especially in the data center sector, facing increasing pressure, they need to solve their high energy consumption and rapidly growing computing capacity needs by promoting the use of green electricity and reducing carbon emissions. Therefore, the installed capacity of data center energy storage equipped with sustainable power supply functions is expected to reach 80.3 gigawatt-hours by 2030, with a compound annual growth rate of 204.9% starting from 2024. In addition, there have been many significant adjustments to the bidding policies of China's communication base station industry from 2020 to 2024, continuously affecting the mechanisms and costs of energy storage projects. On the other hand, government-funded research and development programs have stimulated innovative development of energy storage technology, effectively reducing costs and improving performance.

Efficiency improvement and cost reduction

The efficiency improvement and cost reduction of power storage technology are the main driving factors for its increasingly widespread integration into modern energy systems. Technological progress (including improvements in battery materials and structures, manufacturing processes, and energy management systems) has led to higher efficiency, longer service life, and stronger safety performance, thereby driving down the cost of storage products. Driven by growing demand and expanded production facilities, economies of scale enable manufacturers to spread fixed costs. For example, the average price of lithium-ion batteries dropped by 64.3% from RMB 1.57 per watt-hour in 2022 to RMB 0.63 per watt-hour in 2024. These cost reductions make storage solutions economically viable in a wider range of applications, accelerating the transformation towards more sustainable, flexible, and resilient energy systems.

PART/7

Global and China's Energy Storage Market Development Trends

Artificial intelligence and big data technology stimulate market demand

The deep integration of artificial intelligence and big data technologies with various industries has led to a surge in market demand for computing power and energy, driving rapid growth in the data center energy storage market. The proportion of data center power demand in global electricity demand is expected to increase from 4.0% in 2024 to 10.1% in 2030. Artificial intelligence and big data applications, known for their intensive data processing needs, require a large amount of computing power and continuous and reliable energy support to operate effectively. The dependence of artificial intelligence and big data on continuous power supply has made energy storage a key component of the infrastructure supporting these technologies.

Diversified technical routes and parallel development

Lithium-ion batteries have a higher energy density and longer lifespan compared to lead-acid batteries, while lead-acid batteries are relatively mature in the industrial value chain. The energy storage industry (especially in data centers and communications fields) will develop in parallel with integrated applications of various battery technologies such as lithium-ion and lead-acid, further enhancing energy storage efficiency by providing diverse battery options. Lithium-ion batteries will contribute the main growth potential, while lead-acid batteries will still remain as one of the mainstream applications. Among other battery technology routes, sodium-ion batteries are expected to continue to gain market share in the energy storage market due to their rich raw material resources, strong environmental adaptability, and high comprehensive efficiency.

Continuously improve battery performance and reduce costs through technological progress

Continuous technological progress and corresponding cost reductions have significantly improved the performance and reliability of energy storage technologies, thereby reducing overall costs. The enhancement in competitiveness has promoted further market development and the widespread application of energy storage solutions. Since data center energy storage systems require excellent high-rate performance to meet the instantaneous backup power needs in short periods, one of the important breakthroughs in this field lies in developing battery discharge rates suitable for different working environments. In addition, leading market participants are also actively investing in the research and development of solid-state battery technology, aiming to provide safer, higher energy density, and longer life cycle product options to meet the diverse needs of customers. These technologies help reduce energy costs and carbon footprints, supporting the wider application of energy storage in markets.

PART/8

Global and Chinese energy storage market entry barriers

Customer recognition barrier

In the energy storage industry, customer recognition constitutes an important barrier for new entrants, especially in the communication and data center energy storage markets. The main downstream customers include large state-owned communication operators, equipment manufacturers, and large technology companies. These organizations possess vast customer resources and significant market shares, placing multi-dimensional service demands on suppliers. They expect suppliers to have high-quality products, cost-effectiveness, reliable delivery capabilities, strong service support, regulatory compliance, and a commitment to sustainable development. To successfully overcome these barriers and gain the trust and cooperation of large-scale customers, suppliers not only need to provide products and services that meet high standards but also demonstrate reasonable pricing and cost structures to satisfy the objective requirements of customers.

capital investment barriers

The capital investment barriers in the energy storage industry mainly stem from equipment procurement, system integration, and the substantial capital expenditures required for continuous operation and maintenance. Establishing an advanced energy storage system production capacity capable of meeting high demand for communication and data center products involves considerable initial costs. These systems not only need to manage large data flows and ensure communication continuity but also possess a high level of complexity to seamlessly integrate with existing digital and energy infrastructure. In addition, operating costs (including the maintenance of complex systems that are crucial for energy efficiency and reliability) further increase the required investment. Therefore, it is usually only enterprises with strong financial support that can enter the market and effectively participate in competition.

technical barriers

The energy storage industry faces significant technical barriers, mainly stemming from precise battery technology, energy management systems, and intelligent control algorithms. Enterprises with core technologies and patents enjoy a significant competitive advantage in the market, capable of providing excellent high-rate performance, higher safety levels, and more cost-effective solutions. In addition, developing or acquiring related technologies requires substantial R&D resources and must deal with the complex global patent layout and regulatory standards. Integrating energy storage technology with existing infrastructure not only requires technical compatibility but also compliance with diverse international energy storage specifications. Therefore, the complexity of technology not only limits market entry for new enterprises but also poses continuous challenges to the scalability and interoperability of solutions within the entire field.

Click at the end of the articleRead the original textView the full prospectus

Frost & Sullivan has rich research experience in the TMT industry and has assisted well-known enterprises in successfully listing on capital markets. Successful listing cases include: Tianyue Advanced (2631.HK), Yimutian (YMT: NASDAQ), Xunzhong Communication (2597.HK), Fenggang Technology (1304.HK), Lens Technology (6613.HK), Julong (NASDAQ: JLHL), Xiangjiang Electric Appliance (2619.HK), Lianzhang Portal (LZMH: NASDAQ), Jiaoyou (GMHS.NASDAQ), EPWK (NASDAQ: EPWK), Sikuang Technology (688583.SH), INLF (INLF.NASDAQ), Innocean (2577.HK), Midea Group (0300.HK), Tianju Dihé (2479.HK), YunGongchang (2512.HK), Youbo Holdings (8529.HK), MFS (2556.HK), ZBAO.US, LGCL (NASDAQ: LGCL), Youbisun (9880.HK), Beike Microelectronics (2149.HK), Willis (SIX: WILL), ICG (ICG.NASDAQ), AIXI Robotics (AIXI.US), Kingsoft Holdings (3896.HK), HaoDong Technology (2440.HK), Xuanwu Cloud Technology (2392.HK), Huitongda (9878.HK), iFlytek (2121.HK), SenseTime (0020.HK), Qinhua Data (CD.NASDAQ), Mingyuan Cloud (0909.HK), Century Group (1849.HK), Weimeng Group (2013.HK), Wankala Group (1762.HK), AsiaInfo Technology (1675.HK), Hongya Holdings (1723.HK), Aurora Mobile (JG.NASDAQ), Chengguan Holdings (8606.HK), Qiyi Technology (1739.HK), Weixin Jinko (2003.HK), Tenpay (1806.HK), Atlinks (8043.HK), Zioncom (8287.HK), ISP Global (8487.HK), Vobile (3738.HK), Aibo Technology (2708.HK), iClick (ICLK.NASDAQ), Shengye Capital (6069.HK), Anlink International (8410.HK), Anke Systems (8353.HK), Junmeng International (8062.HK), Feisida (8342.HK), Future Data (8229.HK) and Asia Backup (8290.HK).

Recommended reading (scroll up or down for more)

Frost & Sullivan helped Tianyue Advanced successfully list in Hong Kong (2631.HK)

Frost & Sullivan helped Yimutian successfully list in the US (YMT: NASDAQ)

Frost & Sullivan helped Xunzhong Communication successfully list in Hong Kong (2597.HK)

Frost & Sullivan helped Fenggang Technology successfully list in Hong Kong (1304.HK)

Frost & Sullivan helped Lens Technology successfully list in Hong Kong (6613.HK)

Frost & Sullivan helped Julong successfully list in the US (NASDAQ: JLHL)

Frost & Sullivan helped Xiangjiang Electric Appliance successfully list in Hong Kong (2619.HK)

Frost & Sullivan helped EPWK successfully list in the US (NASDAQ: EPWK)

Frost & Sullivan helped Jiaoyou successfully list in the US (NASDAQ: GMHS)

Frost & Sullivan helped INLF successfully list in the US (INLF.NASDAQ)

Frost & Sullivan helped Innocean successfully list in Hong Kong (2577.HK)

Frost & Sullivan helped Midea Group successfully list in Hong Kong (00300.HK)

Frost & Sullivan helped Tianju Dihé successfully list in Hong Kong (2479.HK)

Frost & Sullivan helped YunGongchang successfully list in Hong Kong (2512.HK)

Frost & Sullivan helped Youbo Holdings successfully list in Hong Kong (8529.HK)

Frost & Sullivan helped MFS successfully list in Hong Kong (2556.HK)

Frost & Sullivan helped ZBAO.US successfully list in the US

Frost & Sullivan helped LGCL successfully list in the US (LGCL.NASDAQ)

Frost & Sullivan helped Youbisun successfully list in Hong Kong (9880.HK)

Frost & Sullivan helped Beike Microelectronics successfully list in Hong Kong (2149.HK)

Frost & Sullivan helped Willis successfully issue GDRs on the Hong Kong Stock Exchange (WILL)

Frost & Sullivan helped ICG successfully list in the US (ICG.NASDAQ)

Frost & Sullivan helped AIXI Robotics successfully list in the US (AIXI.US)

Frost & Sullivan helped Kingsoft Holdings successfully list in Hong Kong (3896.HK)

Frost & Sullivan helped HaoDong Technology successfully list in Hong Kong (2440.HK)

Frost & Sullivan helped Xuanwu Cloud Technology successfully list in Hong Kong (2392.HK)

Frost & Sullivan helped Huitongda successfully list in Hong Kong (9878.HK)

Frost & Sullivan helped iFlytek successfully list in Hong Kong (2121.HK)

Frost & Sullivan helped SenseTime successfully list in Hong Kong (0020.HK)

Frost & Sullivan helped Qinhua Data successfully list in the US (CD.NASDAQ)

Frost & Sullivan helped Mingyuan Cloud successfully list in Hong Kong (0909.HK)

Frost & Sullivan helped Century Group successfully list in Hong Kong (1849.HK)

Frost & Sullivan helped Weimeng Group successfully list in Hong Kong (2013.HK)

Frost & Sullivan helped Wankala Group successfully list in Hong Kong (1762.HK)

Frost & Sullivan helped AsiaInfo Technology successfully list in Hong Kong (1675.HK)

Frost & Sullivan helped Hongya Holdings successfully list in Hong Kong (1723.HK)

Frost & Sullivan helped Aurora Mobile successfully list in the US (JG.NASDAQ)

Frost & Sullivan helped Chengguan Holdings successfully list in Hong Kong (8606.HK)

Frost & Sullivan helped Qiyi Technology successfully list in Hong Kong (1739.HK)

Frost & Sullivan helped Weixin Jinko successfully list in Hong Kong (2003.HK)

Frost & Sullivan helped Tenpay successfully list in Hong Kong (1806.HK)

Frost & Sullivan helped Atlinks successfully list in Hong Kong (8043.HK)

Frost & Sullivan helped Zioncom successfully list in Hong Kong (8287.HK)

Frost & Sullivan helped ISP Global successfully list in Hong Kong (8487.HK)

Frost & Sullivan helped Vobile successfully list in Hong Kong (3738.HK)

Frost & Sullivan helped Aibo Technology successfully list in Hong Kong (2708.HK)

Frost & Sullivan helped iClick successfully list in the US (ICLK.NASDAQ)

Frost & Sullivan helped Shengye Capital successfully list in Hong Kong (6069.HK)

Frost & Sullivan helped Anlink International successfully list in Hong Kong (8410.HK)

Frost & Sullivan helped Anke Systems successfully list in Hong Kong (8353.HK)

Frost & Sullivan helped Junmeng International successfully list in Hong Kong (8062.HK)

Frost & Sullivan helped Feisida successfully list in Hong Kong (8342.HK)

Frost & Sullivan helped Future Data successfully list in Hong Kong (8229.HK)

Frost & Sullivan helped Asia Backup successfully list in Hong Kong (8290.HK)

*The above order is not chronological and is arranged in reverse order of listing time