Huizhou Technology Co., Ltd. (Stock Code: 2481.HK) successfully listed on the main board of the Hong Kong capital market on July 10, 2023. The company is a cross-provincial heating service provider mainly operating in the 'Three Norths' region, providing heating services to residents and non-residents primarily through franchise rights. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') has provided exclusive industry advisory services for the listing of Huizhou Technology Co., Ltd., and we hereby extend our warmest congratulations on its successful listing.

Huizhu Technology Co., Ltd. (hereinafter referred to as 'Huizhu Tech') successfully went public on July 10, 2023. The company plans to issue 7,560 million H shares, of which 90% will be international offerings, 10% will be public offerings, and an additional 15% will be in the form of over-allotment rights. The issue price per share is HK$3.60, with 1,000 shares per lot, raising a net amount of approximately HK$18.75 billion.

During the Hong Kong listing process, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, sponsor, and other professional intermediary institutions in completing the writing of relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important sections), assisting the issuer in communicating with the Hong Kong Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on industry-related issues from the Hong Kong Stock Exchange.

Investment highlights

The company is a leading provider of heating services;

The company can utilize diverse heat sources to provide clean and high-quality heating services;

The company has the capability to manage multiple heating projects distributed across different provinces in China and lead the industry development;

The company has an integrated digital heating service management platform that can control its cross-provincial operations and improve operational efficiency;

The company has strategic synergies with highly trusted industrial partners that drive industry development;

The company has an experienced and dedicated management team.

According to the Frost & Sullivan report, based on the actual heating service area in 2022, the company:

Ranked fourth among non-state-owned heating enterprises in China, accounting for about 1.8% of the total market share;

Ranked second among non-state-owned cross-provincial heating enterprises in China.

Overview of China's Heating Service Industry

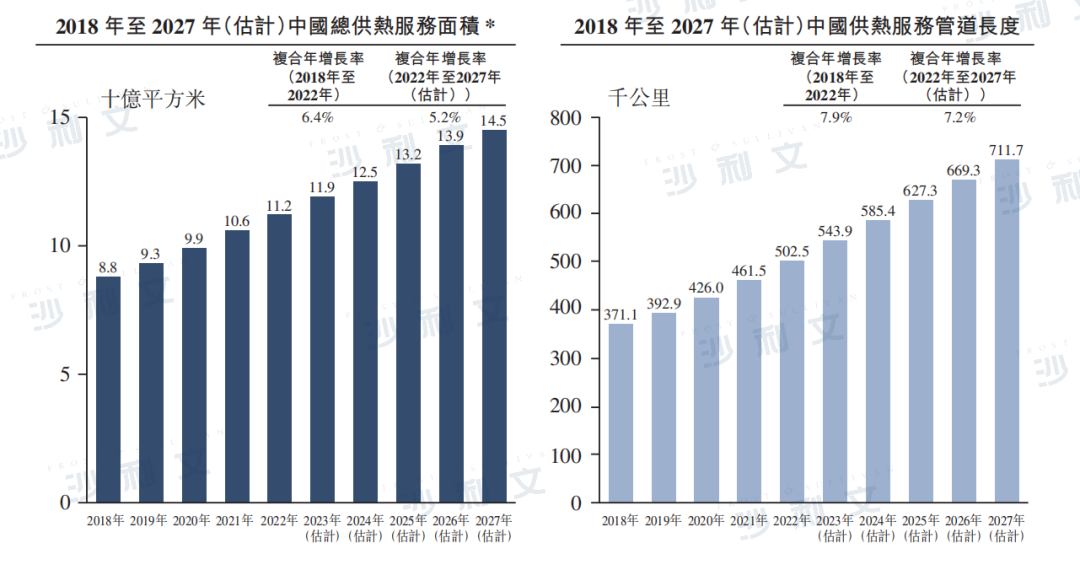

Heating is one of the basic public services in China, involving national economy and people's livelihood. In recent years, China's urban heating industry has developed rapidly. National statistical data show that China's total heating service area increased from 8.8 billion square meters in 2018 to 11.2 billion square meters in 2022, with a compound annual growth rate of 6.4%. It is expected that China's total heating service area will increase to 14.5 billion square meters by 2027, with a compound annual growth rate of 5.2% from 2022 to 2027.

Correspondingly, the length of China's heating service pipelines, including primary and secondary pipelines, increased from 371,100 kilometers in 2018 to 502,500 kilometers in 2022, with a compound annual growth rate of 7.9%. It is expected to increase to 711,700 kilometers by 2027, with a compound annual growth rate of 7.2% from 2022 to 2027.

Data source: National Bureau of Statistics, Frost & Sullivan analysis

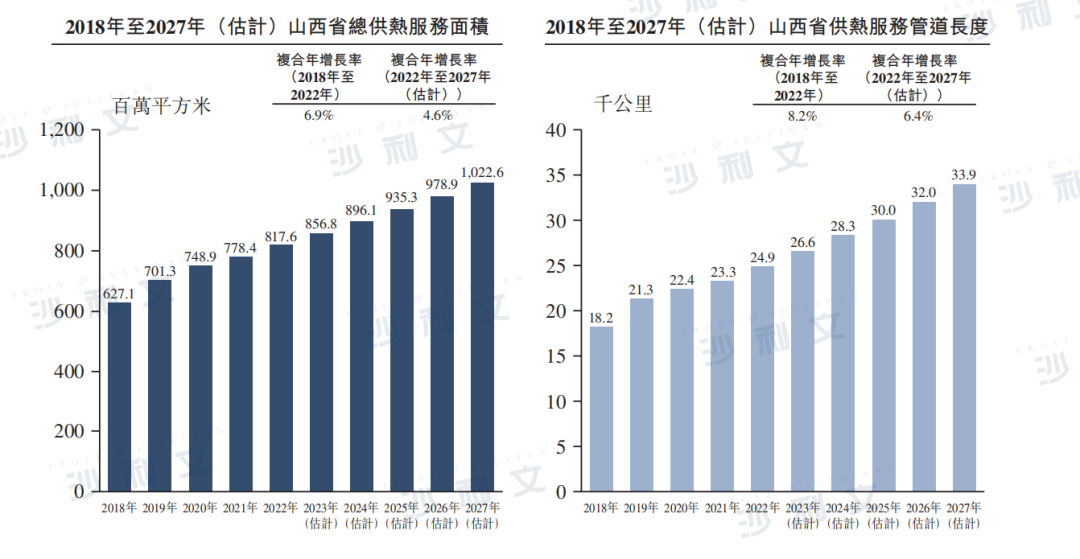

Shanxi Province Heating Service Industry

The total heating service area in Shanxi Province increased from 6.271 million square meters in 2018 to 8.176 million square meters in 2022, with a compound annual growth rate of 6.9%. In 2022, the total heating service area in Shanxi Province accounted for 7.3% of China's total heating service area. Correspondingly, the length of heating service pipelines in Shanxi Province increased from 18,200 kilometers in 2018 to 24,900 kilometers in 2022, with a compound annual growth rate of 8.2%.

The Shanxi Provincial Government encourages the use of various heat sources such as cogeneration, natural gas, electricity, and solar energy to support the development of clean heating. It is expected that the total heating service area in Shanxi Province will increase to 10.226 million square meters by 2027, with a compound annual growth rate of 4.6% from 2022 to 2027. It is also projected that the length of heating service pipelines in Shanxi Province will increase to 33,900 kilometers by 2027, with a compound annual growth rate of 6.4% from 2022 to 2027.

Data source: National Bureau of Statistics, Frost & Sullivan analysis

Gansu Province Heating Service Industry

The total heating service area in Gansu Province increased from 2.346 million square meters in 2018 to 3.024 million square meters in 2022, with a compound annual growth rate of 6.6%. In 2022, the total heating service area in Gansu Province accounted for 2.7% of China's total heating service area. Correspondingly, the length of pipelines for heating services in Gansu Province increased from 5,900 kilometers in 2018 to 13,400 kilometers in 2022, with a compound annual growth rate of 22.6%.

With the support of government policies, Gansu Province encourages more private capital to enter the heating service industry. Driven by resources, technology, private capital, and provincial policies, the heating service industry will continue to develop in a sustainable manner. It is expected that the total heating service area in Gansu Province will increase to 4.109 billion square meters by 2027, with a compound annual growth rate of 6.3% from 2022 to 2027. It is also anticipated that the length of heating service pipelines in Gansu Province will increase to 16,100 kilometers by 2027, with a compound annual growth rate of 3.8% from 2022 to 2027.

Data source: National Bureau of Statistics, Frost & Sullivan analysis

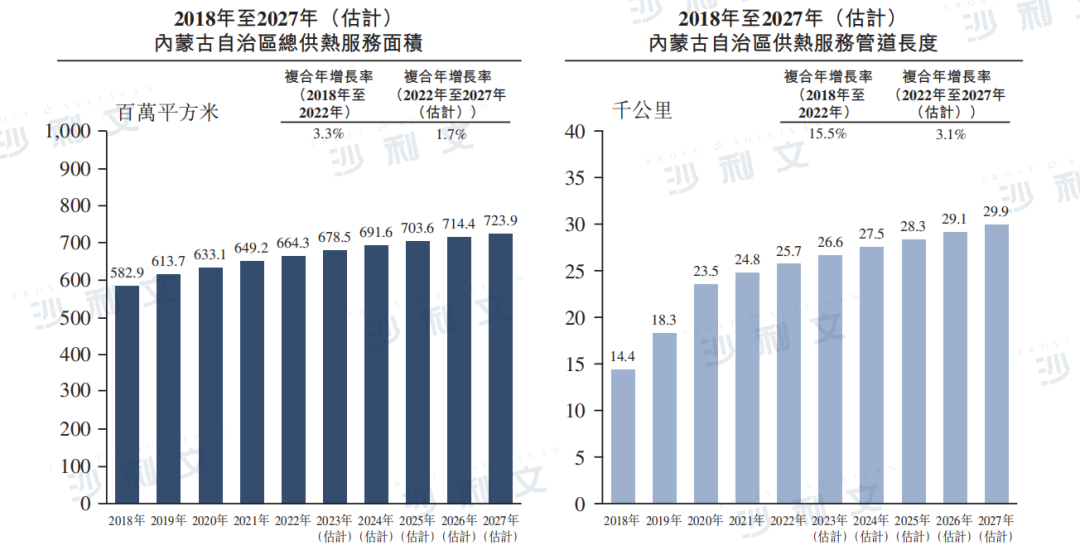

Inner Mongolia Autonomous Region Heating Service Industry

The total heating service area in Inner Mongolia Autonomous Region increased from 5.829 billion square meters in 2018 to 6.643 billion square meters in 2022, with a compound annual growth rate of 3.3%. In 2022, the total heating service area in Inner Mongolia Autonomous Region accounted for 5.9% of China's total heating service area. Correspondingly, the length of heating service pipelines in Inner Mongolia Autonomous Region increased from 14,400 kilometers in 2018 to 25,700 kilometers in 2022, with a compound annual growth rate of 15.5%.

Under the guidance of policies in Inner Mongolia Autonomous Region, local governments have increased financial investment in heating service facilities in small and medium-sized cities and county towns, and encouraged the promotion of new heating service technologies such as new cogeneration and energy-saving technologies. This move will support the stable growth of the heating service industry in Inner Mongolia Autonomous Region. It is expected that the total heating service area in Inner Mongolia Autonomous Region will increase to 7.239 billion square meters by 2027, with a compound annual growth rate of 1.7% from 2022 to 2027. It is also estimated that the length of heating service pipelines in Inner Mongolia Autonomous Region will increase to 29,900 kilometers by 2027, with a compound annual growth rate of 3.1% from 2022 to 2027.

Data source: National Bureau of Statistics, Frost & Sullivan analysis

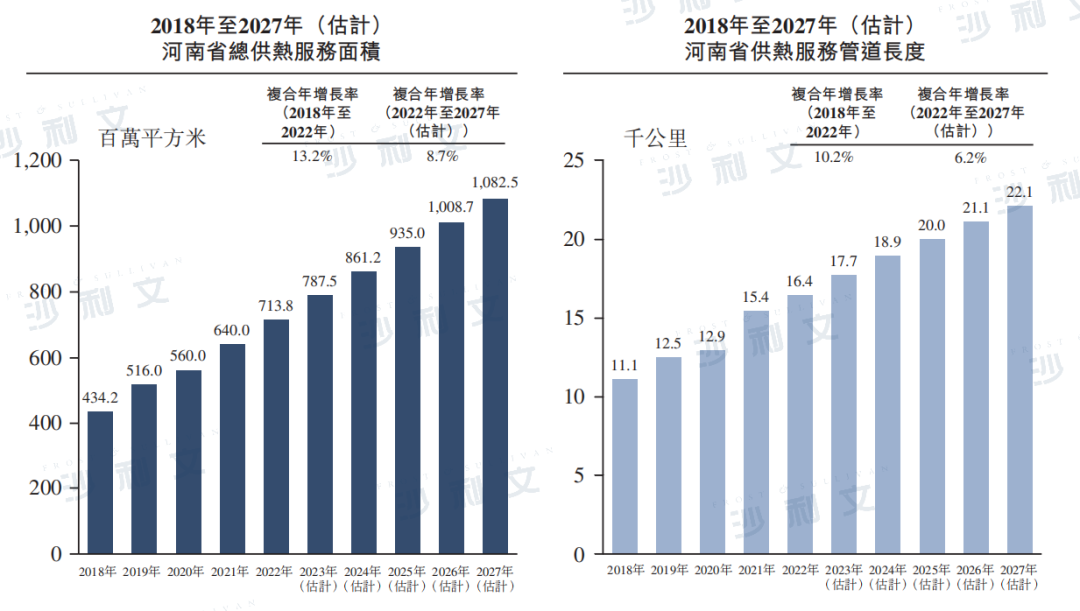

Henan Province Heating Service Industry

The total heating service area in Henan Province increased from 4.342 billion square meters in 2018 to 7.138 billion square meters in 2022, with a compound annual growth rate of 13.2%. In 2022, the total heating service area in Henan Province accounted for 6.4% of China's total heating service area. Correspondingly, the length of heating service pipelines in Henan Province increased from 11,100 kilometers in 2018 to 16,400 kilometers in 2022, with a compound annual growth rate of 10.2%.

Driven by multiple policy stimuli, the total heating service area in Henan Province has grown rapidly over the past five years, with an expected stable growth rate. It is estimated that the total heating service area in Henan Province will increase to 10.825 million square meters by 2027, with a compound annual growth rate of 8.7% from 2022 to 2027. It is also expected that the length of heating service pipelines in Henan Province will increase to 22,100 kilometers by 2027, with a compound annual growth rate of 6.2% from 2022 to 2027.

Data source: National Bureau of Statistics, Frost & Sullivan analysis

Competitive landscape of China's heating service market

China's heating service industry is fragmented, with numerous market participants. Currently, most market participants in China's heating service industry are divided into three categories: professional heating service providers, subsidiaries of power generation groups, and real estate developers. Professional heating service providers can be further divided into state-owned enterprises and non-state-owned enterprises, among which non-state-owned professional heating service companies continue to develop due to flexible operations, cost control advantages, and favorable government policies. In 2021, the total actual heating service area in China was 10.4 billion square meters, with the top five participants providing a total heating service area of 360 million square meters, accounting for only 11.4% of the total market. In 2022, the total actual heating service area in China was 112 billion square meters. Most of the top ten participants are state-owned enterprises. The total heating service area of the top ten companies in 2022 accounted for more than 16.0% of China's total actual heating service area, with the tenth-largest heating service provider providing an actual heating service area exceeding 1 million square meters.

Cross-provincial market participants are not common in this industry due to the need for high technical advantages and extensive cross-provincial operational experience. In 2022, non-state-owned enterprises operated a total actual heating service area of 23.712 million square meters in China, accounting for 21.0% of the total actual heating service area in 2022. In 2022, the company ranked fourth in market share at 1.8% of the market segment. At the same time, based on the actual heating service area in 2022, the company is the second-largest non-state-owned cross-provincial heating service provider in China.

Data source: Company reports, Frost & Sullivan analysis

Main growth drivers of China's heating service industry

The urbanization rate continues to rise:In the past few years, the urbanization rates in Shanxi Province, Gansu Province, Inner Mongolia Autonomous Region, and Henan Province have continued to increase. Due to the cold winter weather, the heating service industry is a public utility in northern China that covers Shanxi Province, Gansu Province, Inner Mongolia Autonomous Region, and Henan Province. According to the '14th Five-Year Plan for National Economic and Social Development and the Outline of Long-Range Objectives Through the Year 2035' issued by the Central Committee and the State Council, it is expected that the urbanization rate will increase by about 5% from 2021 to 2025. Since China's centralized heating market is mainly concentrated in urban areas, it is expected that the continuous increase in the above-mentioned urbanization rate in China will become the main driving factor for heating service demand. As the urbanization rate in urban areas continues to rise, the urban population has also increased, thereby increasing the demand for heating services. This in turn leads to an increase in the total heating service area and the length of heating service pipelines, meaning that China's market scale is continuously expanding.

Growing demand for high-quality life:With the growing demand for high-quality life among Chinese people, residents' demand for stable and reliable heating services is also increasing. More and more heating service enterprises are adopting new technologies to improve their services. Depending on temperature changes, local governments can advance or extend the heating service period to meet residents' needs. In recent years, extreme weather conditions such as extremely low temperatures and frost have occurred in southern China. The demand for heating services in southern China has become increasingly high, aligning with people's pursuit of high-quality life. Currently, Hefei, Nanjing, Hangzhou, Shanghai, and other cities along the Yangtze River have taken the lead in providing heating services in some residential areas.

Advancements in heating technology:Benefiting from advancements in heating technology, the efficiency and environmental protection level of China's heating service industry have improved in recent years. Shanxi Province, Inner Mongolia Autonomous Region, and Gansu Province have been promoting diversification of heat sources (such as biomass, solar energy, and geothermal energy), as well as upgrading heating service networks through intelligent control of heating services. According to the 'National Coal-fired Power Unit Transformation and Upgrading Implementation Plan', heating service enterprises are encouraged to develop long-distance heating transmission technology to expand the area of heating services. In addition, condensing power plants (which generate heat using coal) are encouraged to be upgraded to cogeneration to become cleaner and more efficient power plants. Currently operating cogeneration units are also encouraged to improve their efficiency levels through technological transformation. By the end of 2025, more than 50 million kilowatts of power plant capacity will have been upgraded. Advances in heating technology have created momentum for the development of the heating service industry.

Click at the end of the articleRead the original textView the prospectus

Frost & Sullivan has extensive research experience in the heating and energy industry, assisting well-known enterprises in successfully listing on capital markets. Recent successful listings include: Huzhou Gas (6661.HK), MingYang Smart Energy (MYSE:LI), SDIC Power (SDIC:LI), Naquan Energy Technology (1597.HK), Jiaxing Gas (9908.HK), Chuncheng Thermal Power (1853.HK), CNPC Clean Energy (1759.HK), Jiutai Bangda (2798.HK), TL Natural Gas (8536.HK), Tianbao Energy (1671.HK), Yuguang International (1621.HK), Jintai Feng (8479.HK), Zhongcheng Energy (2337.HK), Inner Mongolia Energy Construction (1649.HK), Resco (1679.HK), Persta Resources (3395.HK), Xintec Energy (1799.HK), China Energy Construction (3996.HK), North China Energy (NASDAQ:CNEY), and others.

Recommended Reading

Frost & Sullivan assists North China Energy Group in successfully going public on the NASDAQ (CNEY)

Frost & Sullivan helps Sinopec Clean Energy successfully go public in Hong Kong (1759.HK)

Frost & Sullivan helps Dihao International successfully go public in Hong Kong (1621.HK)

Frost & Sullivan helps Resun Medical Group successfully go public in Hong Kong (1679.HK)

Frost & Sullivan assists CECN in successfully listing on the Hong Kong Stock Exchange (3996.HK)

*The above order is not sequential and is arranged in reverse chronological order based on listing time.