Excellence Group Limited (Stock Code: 0933.HK) successfully listed on the Main Board of the Hong Kong Capital Market on June 27, 2023. The company is a multi-brand operator, mainly focusing on the design, development, brand promotion, and sales of casual clothing and footwear, while also providing a rich sports experience. With the aim of developing sports, the company manages and operates sports parks, sports centers, and ice rinks, as well as manages and operates esports clubs, coordinates sports events, and provides sports-related marketing services to further enhance the sports experience. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provided exclusive industry advisory services for the listing of Excellence Group Limited, and hereby warmly congratulate them on their successful listing transfer.

During the process of this listing transfer, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, sponsor, and other professional intermediary institutions in completing the writing of relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and providing feedback on industry-related issues to the Hong Kong Stock Exchange for the issuer.

Investment highlights

The company's compound annual revenue growth rate from 2020 to 2022 was 190.3%;

The company has a diversified product portfolio, with differentiated fashion brands and products;

The company has a comprehensive omnichannel retail network, providing a full range of consumer experiences;

The company manages and operates nine sports parks and centers under the Li Ning Sports Park brand, hosting a variety of sports events to promote consumer sports experiences;

The company enjoys a high reputation in the sports industry, especially as its senior management team has a long history in the sector.

According to the Frost & Sullivan report, in terms of retail sales of the company's brands under the Clarks brand portfolio for 2022:

Ranked first among British fashion and casual footwear brands;

Ranked eighth among US fashion and casual footwear brands.

Fashion Industry Market Overview

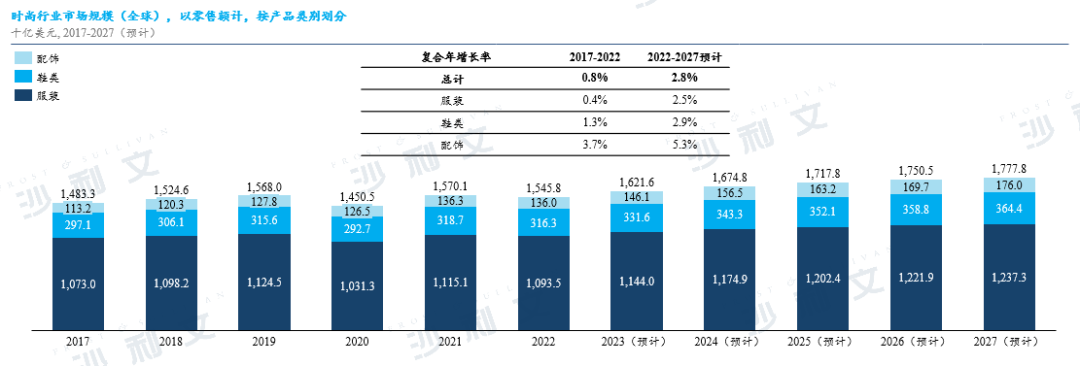

In terms of retail sales, the global fashion industry's market size grew steadily from $1483.3 billion in 2017 to $1545.8 billion in 2022, with a compound annual growth rate of 0.8%. The main reason is the decline in consumers' willingness to purchase non-essential consumer goods (including fashion clothing and footwear), which led to a slight decrease in 2020. It is expected that with the gradual recovery of the economy over the next few years, the global fashion industry's market size will increase to $1777.8 billion in 2027, with a compound annual growth rate of 2.8%. In terms of product types, clothing is the largest contributor, accounting for 70.7% of the total market size in 2022, followed by footwear, which ranked second, accounting for 20.5% of the total market size in 2022.

Data source: Analysis by Frost & Sullivan

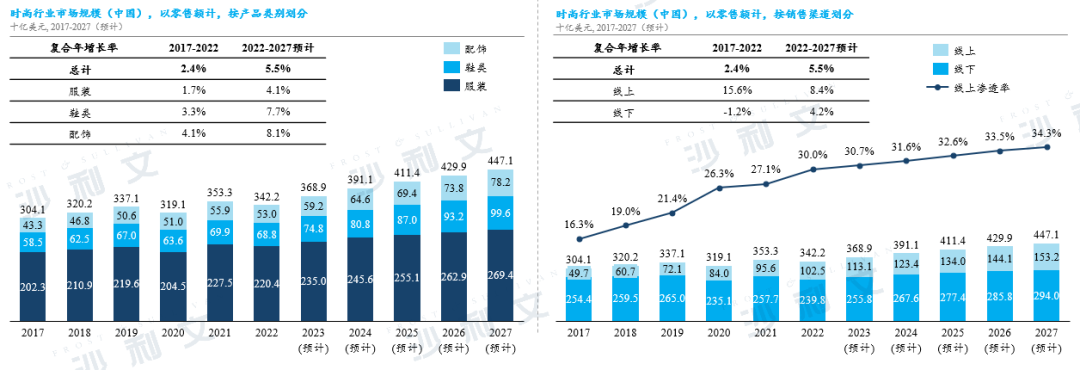

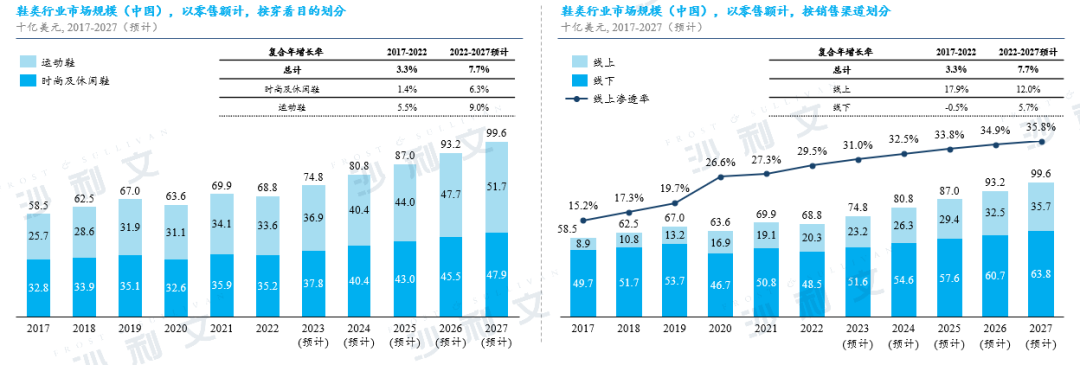

According to a Frost & Sullivan report, China is the largest fashion market in the world by retail sales in 2022. Despite the slight reduction in market size due to the impact of COVID-19 in 2020, the fashion industry market in China has experienced rapid expansion since 2017. This is mainly attributed to strong economic growth and the improvement in the consumption capacity of Chinese citizens. By retail sales, the market size of China's fashion industry increased from $304.1 billion in 2017 to $342.2 billion in 2022, with a compound annual growth rate of 2.4%. It is expected that by 2027, the market size will further increase to $447.1 billion, with a compound annual growth rate of 5.5%.

From 2017 to 2027, although offline channels remain the main contributor to retail sales, online channels' retail sales have gradually increased, with a growth rate expected to accelerate, thereby gradually increasing market share. Online channel retail sales grew rapidly from $497 billion in 2017 to $1025 billion in 2022, with a compound annual growth rate of 15.6%. It is estimated that by 2027, online channel retail sales will reach $1532 billion, with a compound annual growth rate of 8.4%.

Data source: Analysis by Frost & Sullivan

Trend of raw material prices in the Chinese fashion industry

Raw materials in the fashion industry can be divided into two types: natural fibers (such as cotton, silk, and cocoons) and chemical fibers (such as spandex, polyester, and nylon). According to a Frost & Sullivan report, the prices of these main raw materials in China fluctuated between 2017 and 2022, mostly due to the outbreak of COVID-19. The pandemic led to a reduction in production demand in the fashion industry, causing prices to reach their lowest point in 2020. As the economy gradually recovered, prices rose again in 2021. Historical price trends are shown in the following chart:

Data source: Analysis by Frost & Sullivan

Market Overview of Footwear Industry

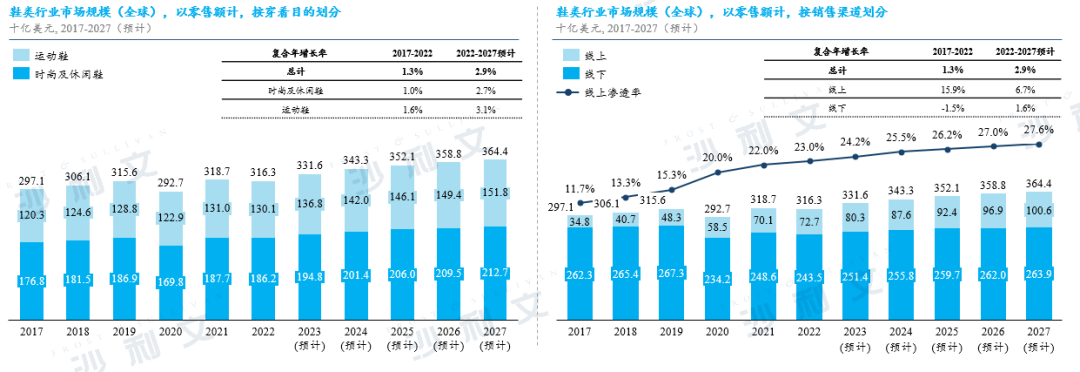

The global footwear industry can be divided into two main types based on the purpose of wear: (a) Fashion and casual footwear industry, which includes the 'Clarks' brand under the Group; (b) Sports footwear industry. Fashion and casual footwear are designed for daily wear, while sports footwear is designed for athletic activities and complements clothing and equipment as part of sport gear. Affected by COVID-19, the retail sales market size of the global fashion and casual footwear industry increased from $176.8 billion in 2017 to $186.2 billion in 2022, with a compound annual growth rate of 1.0%. With the gradual economic recovery, it is expected to reach $212.7 billion by 2027, with a compound annual growth rate of 2.7%.

In terms of sales channels, offline channels are expected to continue as the main contributor to retail sales from 2022 to 2027. With the increasing maturity of e-commerce business models and further prompting changes in consumer habits due to COVID-19, online sales channels have grown rapidly. Online retail sales of footwear (including fashion and casual shoes, and sports shoes) increased from $348 billion in 2017 to $727 billion in 2022, with a compound annual growth rate of 15.9%. It is estimated that by 2027, online sales of footwear will reach $1006 billion, with a compound annual growth rate of 6.7%.

Data source: Analysis by Frost & Sullivan

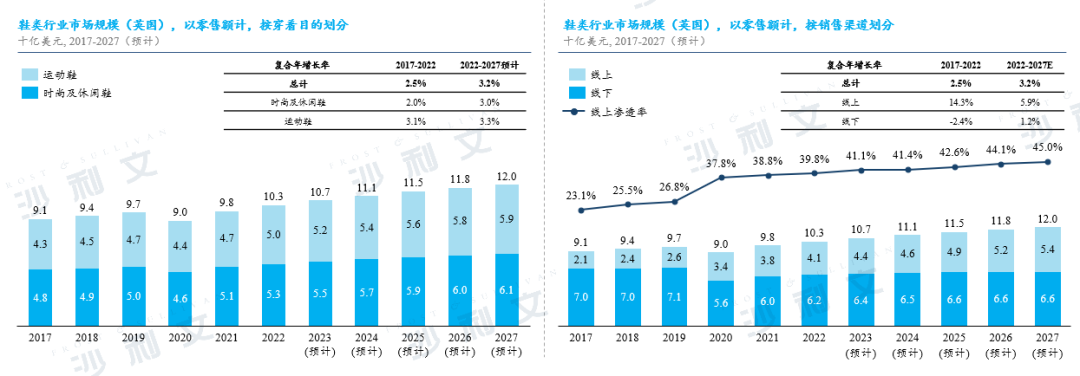

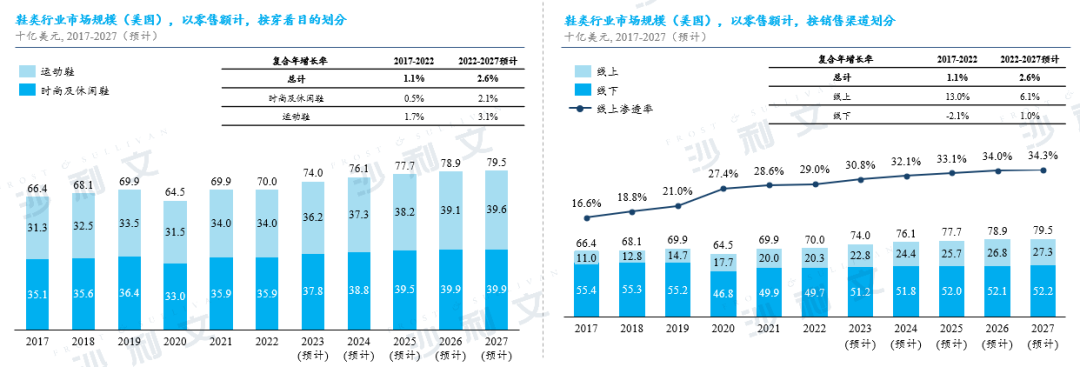

In 2022, China, the United States, and the United Kingdom together accounted for nearly half of the global footwear industry's market share, with China, the United States, and the United Kingdom holding 21.8%, 22.1%, and 3.3% of the market share, respectively. The development of the footwear industries in China, the United States, and the United Kingdom is roughly similar to that of the global footwear industry. From 2017 to 2022, retail sales in these regions all experienced moderate growth and are expected to continue between 2023 and 2027. In terms of distribution channels, online channels experienced rapid growth from 2017 to 2022 and are expected to maintain this growth trend from 2023 to 2027. Among these regions, the retail sales history and forecast growth rate of the Chinese footwear market are the highest, mainly due to the rapid development of the Chinese economy and the increase in per capita disposable income.

Data source: Analysis by Frost & Sullivan

Data source: Analysis by Frost & Sullivan

Data source: Analysis by Frost & Sullivan

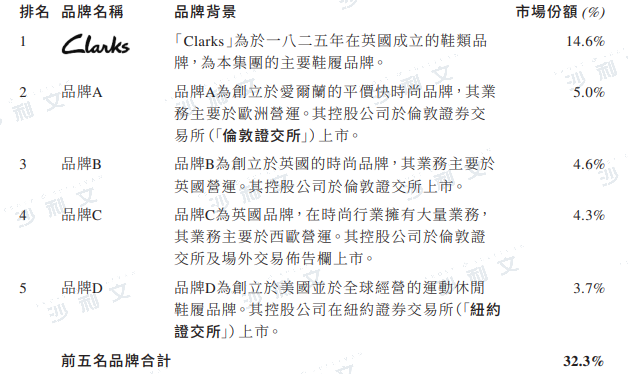

Competitive landscape of the UK fashion and casual footwear market

The UK's fashion and casual footwear industry is relatively concentrated. According to a Frost & Sullivan report, the top five brands account for 32.3% of the market share in terms of retail sales. 'Clarks' ranks first in the UK fashion and casual footwear industry with a market share of 14.6%, far exceeding the second-ranked brand which has only a 5.0% market share.

Data source: Analysis by Frost & Sullivan

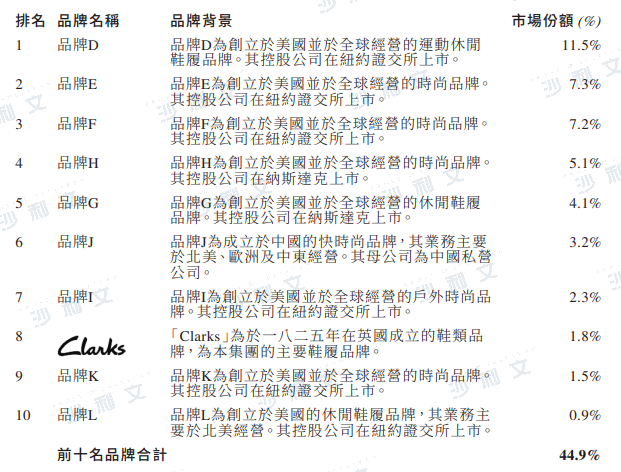

Competitive landscape of the US fashion and casual footwear market

The fashion and casual footwear industry in the United States is relatively concentrated. In terms of retail sales, the top ten brands account for 44.9% of the market. 'Clarks' ranked eighth in 2022, with a market share of 1.8%.

Data source: Analysis by Frost & Sullivan

Key market drivers in the fashion and footwear industry

-

The Rise of the New Generation

The new generation of consumers (i.e., millennials and Generation Z) are becoming the main consumer group in the fashion and footwear industry. They value self-expression, individuality, quality, and brand reputation. The increasing awareness of fashion and the diversification of styles are driving the growth and development of the fashion and footwear industry.

-

Continuous digital transformation

The emergence of online channels and data intelligence, along with the increasing popularity of social media platforms, is driving digital transformation. In addition, due to lockdowns and social distancing measures during the COVID-19 outbreak, online shopping has become more prevalent. The empowerment of electronic technology and social distancing during the pandemic have gradually shifted consumers' shopping habits from traditional offline channels to online ones. Despite fluctuations in online sales during China's lockdown due to supply chain and property disruptions, integrating e-platforms and technology into sales and marketing has become an urgent task for fashion brands, driving expansion in the fashion and footwear industries.

-

Consumers have diverse needs

The uneven wealth distribution between cities and less developed areas leads to diverse consumer demands. When consumers in developed regions tend to seek more high-end and personalized products, those in less developed areas are often more price-sensitive. In an increasingly differentiated market, fashion suppliers can benefit from developing a multi-brand strategy to meet the needs of different consumer groups with a diversified product portfolio and seize market potential.

-

Optimize the brand portfolio

Leading companies in China's fashion industry are developing their brand portfolio by strategically creating and expanding multiple brands targeting different age groups or consumption preferences within their target customer base to achieve synergies. A diverse, comprehensive, and distinctively branded portfolio can help companies establish connections with different target consumer groups, organize cross-brand promotional activities, meet consumers' diverse needs, thereby gaining more loyal customers in a relatively fragmented market and expanding market share.

Click at the end of the articleRead the original textViewing Listing Documents

Frost & Sullivan has extensive research experience in the consumer retail industry and has assisted many well-known enterprises in successfully listing on the capital market. Successful listings include Shanghai Shangmei (2145.HK), Giant Biosciences (2367.HK), China COSCO (1880.HK), MingChuang Youpin (9896.HK), Jiulongwang Food (1927.HK), Vesync (2148.HK), Blue Moon (6993.HK), Poplar Mart (9992.HK), MingChuang Youpin (NYSE: MNSO), Nongfu Spring (9633.HK), Fengxiang Food (9977.HK), China Feihai (6186.HK), Taobao Sports (6110.HK), China National Tobacco International (6055.HK), Youpin 360 (2360.HK), Wugu Flour Mill (1837.HK), Baby Tree (1761.HK), Deying Holdings (2250.HK), Bingshi International (1705.HK), Golden Cat and Silver Cat (1815.HK), Miming Lifestyle Department Store (8473.HK), Sainsbury's (1475.HK), Debao Group (8436.HK), Seiko China (NASDAQ: SECO), Barbie Bebe (8297.HK), Asia Grocery (8413.HK), Chowking Duck (1458.HK), COFCO Foods (1610.HK), Dali Foods (3799.HK), Vientiane International (0288.HK), Chow Tai Fook (1929.HK), Jumei Youpin (NYSE: JMEI), and others.

Recommended Reading

Frost & Sullivan helps Joyouwang Food successfully go public in Hong Kong (1927.HK)

Frost & Sullivan assists Vesync in successfully listing on the Hong Kong Stock Exchange (2148.HK)

Frost & Sullivan assists Blue Moon in successfully listing on the Hong Kong Stock Exchange (6993.HK)

Frost & Sullivan helps famous innovative products successfully go public in the US (NYSE:MNSO)

Frost & Sullivan helps China's Feihai succeed in listing on the Hong Kong Stock Exchange (6186.HK)

Frost & Sullivan helps Top Glove Sports S.A. successfully go public in Hong Kong (6110.HK)

Frost & Sullivan helps Youpin 360 successfully go public in Hong Kong (2360.HK)

Frost & Sullivan helps Baby Tree successfully go public in Hong Kong (1761.HK)

Frost & Sullivan helps Golden Cat and Silver Cat successfully go public in Hong Kong (1815.HK)

Frost & Sullivan helps Nippon Sake & Foods Co., Ltd. successfully go public in Hong Kong (1475.HK)

Frost & Sullivan helps COFCO Meat successfully list on the Hong Kong Stock Exchange (1610.HK)

*The above order is not sequential and is arranged in reverse chronological order based on listing time.