Hongxin Construction Development Co., Ltd. (Stock Code: 9930.HK) successfully listed on the main board of the Hong Kong capital market on May 25, 2023. The company is a leading equipment operation service provider in China, mainly engaged in the operation leasing of equipment and materials, engineering technical services, platforms, and other services in the field of construction projects. It has become a one-stop solution provider for aerial work platforms, new support systems, new formwork systems, and other diversified engineering machinery and equipment. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provided exclusive industry advisory services for Hongxin Construction Development Co., Ltd.'s listing, and we hereby extend our warm congratulations on its successful listing.

Hongxin Construction Development Co., Ltd. (hereinafter referred to as 'Hongxin Construction') successfully went public on May 25, 2023. The company issued approximately 365 million H shares globally, of which 90% were international offerings and 10% were Hong Kong offerings. The issue price per share was HK$4.52, raising a net amount of approximately HK$1.518 billion.

During the Hong Kong listing process, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important sections), facilitating communication between the issuer and the Hong Kong Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

Investment highlights

The company's largest equipment operation service provider nationwide;

The company is one of the leaders in the equipment operation service market for aerial work platforms, new support systems, and new formwork systems;

The comprehensive synergies among various product lines of the company are remarkable, providing a full range of multi-functional services covering the entire project lifecycle centered around customers;

The company possesses outstanding digital capabilities, continuously improving operational efficiency and customer service;

The company has established a diversified, blue-chip customer base that is loyal and high-quality;

The company has profound experience in equipment operation, engineering technology accumulation, and industry-leading large-scale operational capabilities;

The company has strategic synergies with highly trusted industrial partners that drive industry development;

The company has a management team that shares a common mission and is highly visionary.

According to a report by Frost & Sullivan:

Based on its operating revenue in 2022, the company is China's largest equipment operation service provider;

Based on the equipment inventory in 2022, the company ranks first nationwide in all three sub-markets: aerial work platforms, new support systems, and new formwork systems.

Overview of China's Equipment Operation and Maintenance Service Market

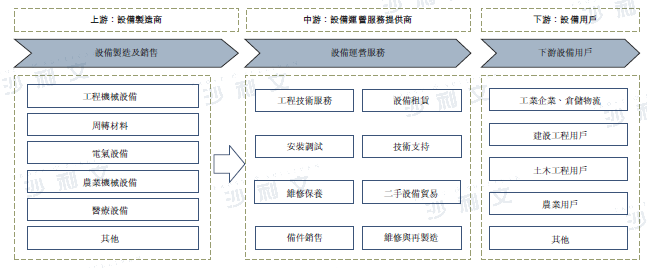

The equipment operation service market can be divided into three parts according to the value chain: 1) upstream equipment suppliers; 2) midstream equipment operation service providers; 3) downstream equipment users. Upstream equipment suppliers are mainly engaged in equipment manufacturing and sales, including but not limited to engineering machinery and equipment, support systems and formwork systems, electrical equipment, agricultural machinery and equipment, medical equipment, etc. Midstream equipment operation service providers mainly provide services such as equipment leasing, construction installation, maintenance, etc. Downstream equipment users come from diverse industries, including but not limited to industry, warehousing and logistics, construction projects, civil engineering, agriculture, and other fields.

Source: Frost & Sullivan report

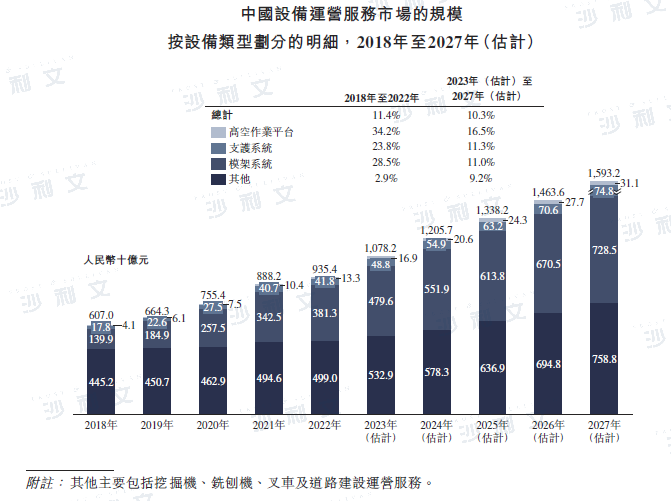

According to a Frost & Sullivan report, the market size of equipment operation services in China (in terms of revenue) increased from RMB 607 billion in 2018 to RMB 935 billion in 2022, with a compound annual growth rate of 11.4%. With further optimization and integration of market participants, improvement in service quality and specialization levels, as well as an increase in the number of equipment, it is expected that the market size of equipment operation services in China (in terms of revenue) will increase to RMB 1.593 trillion by 2027, with a compound annual growth rate of 10.3% from 2023 to 2027.

Source: Frost & Sullivan report

Market competition pattern of equipment operation services in China

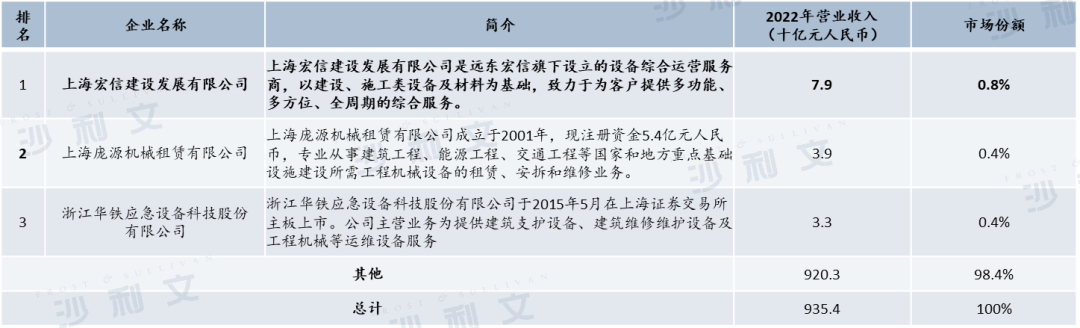

The overall equipment operation service market in China is extremely fragmented. In terms of revenue, the top three participants in 2022 accounted for only 1.6% of the total market size, with over 15,000 small and medium-sized participants occupying the remaining 98.4% of the market share. In terms of revenue, Hongxin Jianfa ranked first in 2022, accounting for 0.8% of the market share.

Source: Frost & Sullivan report

Overview of the Working At Height Platform Market

A high-altitude working platform refers to a movable mechanical device used for operations at certain heights. According to the 'National Classification Standard for High-Altitude Work', any equipment used for work at heights above two meters where there is a possibility of falling is classified as a high-altitude working platform. Compared to traditional high-altitude working tools such as baskets, today's high-altitude working platforms are more flexible in operation and scheduling, capable of significantly accelerating construction progress, simplifying construction processes in harsh environments, reducing labor intensity and labor costs, and ensuring the safety of construction workers. In addition, the application scenarios of high-altitude working platforms are expanding from traditional fields such as manufacturing and construction to more diversified areas, including but not limited to agriculture, consumer goods, cultural tourism, entertainment, and other industries.

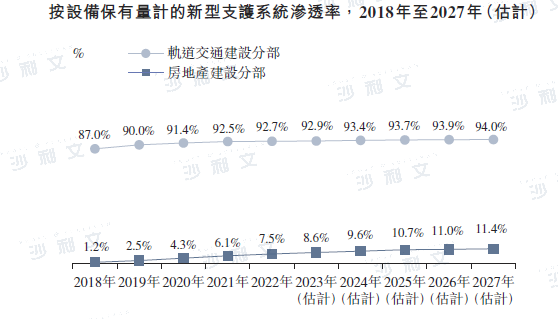

Given the advantages of aerial work platforms and increasing market demand, the equipment inventory of aerial work platforms has increased significantly from 113,200 units in 2018 to 487,400 units in 2022, with a compound annual growth rate of 44.1%. It is expected that this will further increase to 1.1946 million units by 2027, with a compound annual growth rate of 17.7% from 2023 to 2027. In 2022, the equipment inventory of aerial work platforms in China was 487,400 units, of which about 428,900 units came from equipment operation service providers, accounting for approximately 88% of the total inventory.

Market Competition Pattern of China's High-altitude Work Platform Operation Services

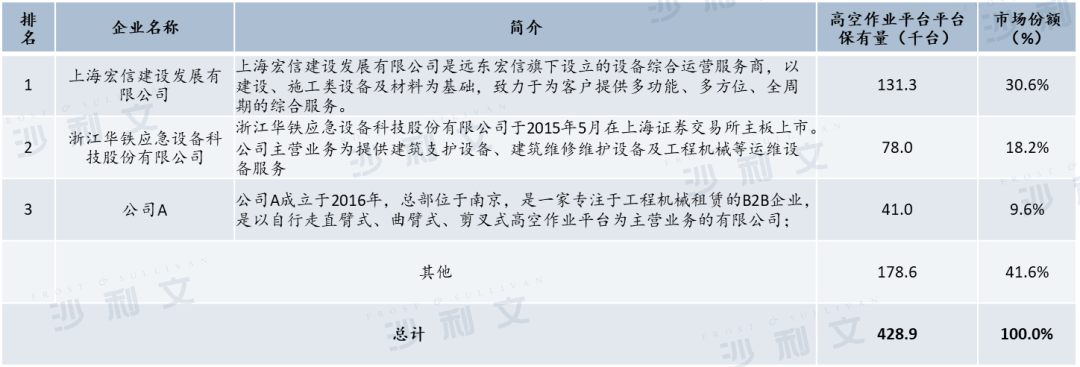

The operation service market for aerial work platforms in China is highly concentrated. Based on the equipment holdings of aerial work platforms, as of December 31, 2022, the three major market participants together accounted for 58.4% of the total market size, with approximately 1,600 small and medium-sized market participants occupying the remaining 41.6% of the market share. In terms of equipment holdings of aerial work platforms, as of December 31, 2022, Hongxin Jianfa held a market share of 30.6% with 13,100 aerial work platform units in stock, ranking first in the Chinese market.

Source: Frost & Sullivan report

Market Overview of Support Systems

The support system refers to the temporary retaining structures built during underground or underwater construction processes, such as foundation pits or cofferdams, used to protect the safety of workers and equipment. Traditionally, support systems were mainly made of concrete or cement and could not be reused. In 2022, the equipment inventory of concrete support systems reached several hundred million tons. The Ministry of Housing and Urban-Rural Development issued the 'Guiding Opinions on Promoting the Reduction of Construction Waste' in 2020, stipulating that local government agencies must establish and gradually improve the working mechanism for reducing construction waste, strengthen source control of construction waste, promote the transformation of engineering construction production organization models, effectively reduce the generation and emission of construction waste during the engineering construction process, and continuously advance the sustainable development of the construction industry and the improvement of urban and rural living environments.

To meet the growing demand for more efficient, safer, more economical, and environmentally friendly support systems, the market share of new support systems (mainly referring to steel support systems, which are environmentally friendly, safe, intelligent, and recyclable) is rapidly increasing. New support systems can reduce material consumption during construction and can compensate for the shortcomings of manual labor or traditional support systems (such as better waterproof performance), thereby accelerating construction progress, improving construction methods, ensuring the safety of construction workers, and ensuring that projects proceed as planned. The many competitive advantages of new support systems help them quickly replace traditional support systems on the market. New support systems are widely used in fields such as bridge construction, subways, stadiums, tunnels, transportation systems, station construction, and excavation support in building construction.

The inventory of new support systems in China increased from 15.549 million tons in 2018 to 39.679 million tons in 2022, with a compound annual growth rate of 26.4%. It is expected that by 2027, this will further increase to 73.902 million tons, with a compound annual growth rate of 11.9% from 2023 to 2027. The market size (in terms of revenue) of new support systems in China increased from RMB 17.8 billion in 2018 to RMB 41.8 billion in 2022, with a compound annual growth rate of 23.7%. It is expected that by 2027, this will further increase to RMB 74.8 billion, with a compound annual growth rate of 11.3% from 2023 to 2027. In 2022, the total inventory of new support systems in China was about 39.679 million tons, of which approximately 31.743 million tons (or about 80.0%) came from equipment operation service providers.

In addition, the underground construction, where support systems are widely used, has maintained rapid growth in recent years. According to a Frost & Sullivan report, since the implementation of the 13th Five-Year Plan, the total area of underground construction increased by a cumulative 1.4 billion square meters from 2016 to 2020. The growth in the total area of underground construction accounted for 22.0% of the total construction area of completed urban areas from 15.0% in 2016 to 2020. According to the same source, the total area of underground construction is expected to increase to about 310 million square meters by 2026, with the percentage of the total construction area of completed urban areas further increasing to 23.0% by 2026.

Source: Frost & Sullivan report

Competitive landscape of new support systems

According to a Frost & Sullivan report, there are approximately 1,000 support system operation service providers in China, with most of them having equipment holdings of less than 10,000 tons. The new support system operation service market in China is highly fragmented, and as of December 31, 2022, the top three market participants accounted for only 7.9% of the total market size, with the remaining 92.1% being held by smaller and medium-sized market players. In terms of equipment holdings of new support systems, as of December 31, 2022, Hongxin Jianfa ranked first in the Chinese market with a market share of 5.0%, holding approximately 1.5766 million tons of new support system equipment.

Market Overview of Formwork System

The formwork system mainly includes two major categories: formwork and scaffolding, which are used for temporary support and enclosure protection during the construction of the main structure of engineering projects. From a material perspective, traditional formwork systems often refer to wooden or bamboo products or steel pipe fastener or bowl buckle types; whereas new formwork systems mostly refer to steel plate fastener types. Compared with traditional formwork, plate fastener products have significant advantages in terms of assembly flexibility, safety, and economic benefits. In 2022, the equipment inventory of traditional scaffolding was about 571 million tons.

Currently, provinces and cities such as Jiangsu, Shanghai, and Hubei have introduced relevant incentive policies to promote the application of bolted scaffolding. For example, the Jiangsu Provincial Department of Housing and Urban-Rural Development issued a 'Notice on Strengthening Construction Safety Management' in May 2020, encouraging the promotion of socket-type bolted steel pipe scaffolding for urban rail transit projects and high-risk projects. With increasing demand from customers for efficient, safe, cost-saving, and environmentally friendly formwork systems, the market share of new formwork systems has surged. Especially, with the rapid development of urban infrastructure and stricter requirements for energy conservation, environmental protection, and construction safety, bolted scaffolding has gained market recognition, quickly replacing traditional scaffolding and being widely used in construction scenarios such as subways, railways, bridges, factories, and housing construction.

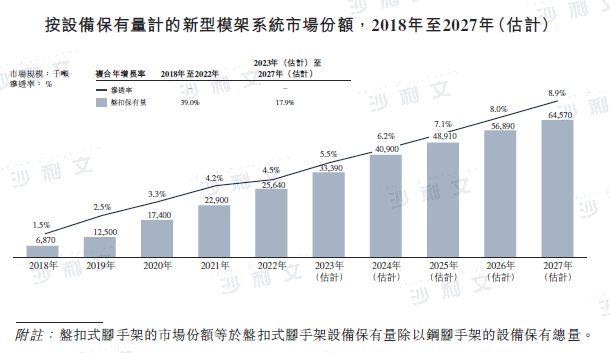

The equipment inventory of China's prefabricated scaffolding increased from 6.87 million tons in 2018 to 25.64 million tons in 2022, with a compound annual growth rate of 39.0%. It is expected that the inventory will further increase to 64.57 million tons by 2027, with a compound annual growth rate of 17.9% from 2023 to 2027. In 2022, the equipment inventory of prefabricated scaffolding in China was 25.64 million tons, of which about 19.23 million tons (or approximately 75%) came from equipment operation service providers.

Source: Frost & Sullivan report

Competitive landscape of new mold base system

The operation service market for new modular frame systems in China is highly fragmented. Based on the equipment holdings of new modular frame systems, as of December 31, 2022, the three major market participants together accounted for only 6.0% of the total market size, with about 800 small and medium-sized market participants occupying the remaining 94.0% of the market share. In terms of equipment holdings of new modular frame systems, as of December 31, 2022, Hongxin Jianfa held approximately 623,000 tons of new modular frame system equipment, accounting for 3.2% of the market share and ranking first in the Chinese market.

China Equipment Operation and Maintenance Service Market

Key market drivers

The market demand for equipment operation services is closely related to the development of infrastructure construction. In the future, China's urbanization process will continue, which corresponds to significant growth potential in the construction industry and infrastructure sectors such as highways, airports, and rail transit. The demand for equipment is expected to continue increasing. Coupled with the trend of industrial structure transformation and upgrading in China and the growing need for full utilization of social resources, the equipment service industry, including leasing, will receive stronger external driving forces. In addition, the emergence and expansion of urban agglomerations and metropolitan areas in China have also generated a large demand for infrastructure construction. With the development of infrastructure construction in these fields, the demand for equipment operation services, especially in the construction sector, is expected to continue growing.

In the field of construction machinery and other equipment, new industrial forms driven by artificial intelligence, the Internet of Things (IoT), and big data are gradually emerging. The IoT and digital services involve a wider range of data collection, storage, computation, and cloud-based services based on data, enabling communication between devices and people, as well as between devices and other devices and the cloud. The gradual rise of the IoT will further promote the specialization of the equipment service industry, refine and specialize social division of labor, and make integrated services such as equipment leasing, corresponding engineering construction services, and after-sales maintenance more recognized and accepted by customers.

Supply-side structural reform focuses on removing backward production capacity, strengthening professional services, and thereby achieving more efficient resource allocation. More and more enterprises tend to reduce fixed asset investment and leverage ratios, and concentrate resources on the operation of core businesses. At the same time, with the transformation and upgrading of the construction industry, customers face more complex construction scenarios and require advanced construction methods and professional operators. Professional equipment operation service providers can provide high-quality equipment as well as customized construction plans tailored to the characteristics of customer projects. As the specialization within the industry becomes increasingly common, more and more equipment users will prefer to hire professional equipment operation service providers for relevant services rather than purchasing equipment independently, reducing their costs and thus gaining market popularity and great growth potential.

The improvement of construction efficiency is extremely important for application scenarios that emphasize project duration and timeliness, such as building maintenance. Taking the scissor lift platform as an example, compared to traditional scaffolding, it can reduce working hours by about 35% to 60% in applications like wall cleaning, column painting, and lighting maintenance, while saving at least 50% on labor costs. With the deepening aging population in China and the development of the macroeconomy, the annual compound growth rate of construction industry employees' wages has reached as high as 11% in the past decade. Therefore, high labor costs will drive the penetration rate of aerial work platforms on the downstream demand side. At the same time, a series of policies such as the '12th Five-Year Plan' for the construction industry explicitly require the construction industry to significantly reduce the number of deaths in engineering production safety accidents. Since high-altitude falls account for more than half of all accidents in China's housing and municipal engineering production, the introduction of relevant safety policies provides favorable support for the application of aerial work platforms, encouraging downstream enterprises to further improve the utilization rate of related equipment.

Click at the end of the articleRead the original textView the prospectus

Frost & Sullivan has extensive research experience in the engineering machinery and equipment, industrial automation, and mechatronic industries. It has assisted well-known enterprises in successfully listing on the capital market. Successful listings include: Hangzhou Giant Technology (GSI.SW), Quanfeng Holdings (2285.HK), SenSong International (2155.HK), Dafeng Equipment (2153.HK), Wenling Industrial Tools (1379.HK), Haojiang Electromechanical (1408.HK), China Shuta (8623.HK), Haina Intelligence (1645.HK), Aoda Holdings (9929.HK), Meko Pipe Industry (1553.HK), Yonglianfeng (8617.HK), China Pengfei (3348.HK), Hengxin Feng Holdings (1920.HK), Contro (1912.HK), Weiliang Holdings (8612.HK), Kun Group (924.HK), Pipeline Engineering (1865.HK), Cangnan Instrumentation (1743.HK), Kangli International (6890.HK), Hengyi Holdings (1894.HK), Auslion Global (1540.HK), Hengda Technology (1725.HK), China Tower (0788.HK), Junma Technology (8490.HK), Quanda Electric (1750.HK), ZC Tech Gp (8511.HK), Guangli Technology (6036.HK), China Foton (8506.HK), Junqiu Holdings (8485.HK), Jinshang Precision (1651.HK), Jingyang Group (8257.HK), Hongteng Technology (6088.HK), Xingming Holdings (8425.HK), Yisheng (1656.HK), Yurong Group (1536.HK), Yengneng Electromechanical (1608.HK), Yabigang Leasing (1496.HK), China Railway Signal & Communication (3969.HK), Wuxi Shenglida (1289.HK), Jinbangda (3315.HK), Honglin Technology (1087.HK), Saijing Power Electronics (580.HK), Xiangyu Dredging (871.HK), Rongsheng Heavy Industry (1101.HK), China Automation (569.HK), etc.

Recommended Reading

Frost & Sullivan assists Pengfei Group in successfully going public in Hong Kong (3348.HK)

Frost & Sullivan assists Contel in successfully listing on the Hong Kong Stock Exchange (1912.HK)

Frost & Sullivan assists Kun Group in successfully listing on the Hong Kong Stock Exchange (0924.HK)

Frost & Sullivan assists China Tower to successfully go public in Hong Kong (0788.HK)

Frost & Sullivan assisted Yissun to successfully go public in Hong Kong (1656.HK)

Frost & Sullivan assists Eneng Electromechanical in successfully going public in Hong Kong (1608.HK)