All Things Cloud Technology Services Co., Ltd. (hereinafter referred to as 'All Things Cloud') successfully went public on September 29, 2022, with a global issuance of 116.7 million shares at an issue price of HK$49.35 per share.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support and highlight the issuer's competitive advantages, assisting the issuer, investment banks and other intermediaries in completing the writing of relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

China property management service industry

Property management originally referred to the operation, control, and supervision of real estate. With the evolution of China's property management service industry over the past few decades, the scope of the industry and related services has gone through several development stages:

-

early stage

In the early 1980s, China's first property management service company was established, marking the beginning of the history of the property management service industry in China. In the early stages, the property management service market was highly fragmented, with low profits for property management service companies and limited standardization of services. During this period, market participants focused on providing one or more basic property management services, such as order maintenance services, cleaning services, repair and maintenance services, gardening services, etc.

-

Normalization phase

In 2003, the 'Property Management Regulations' were introduced, establishing a regulatory framework for China's property management service industry and promoting it into a standardized phase.

-

diversification phase

In 2012, the '12th Five-Year Plan for the Development of the Service Industry' was introduced, encouraging Chinese property management service companies to carry out diversified services, marking the industry's entry into a diversified phase. Subsequently, with the implementation of other related regulations, an open and fair market system was established within the industry. During this stage, major service providers provided services for various properties, including residential properties, retail properties, office buildings, public utilities, industrial parks, schools, and hospitals. At the same time, in addition to providing high-quality basic property management services, well-known property management service providers have also expanded their service scope to include various value-added services (including real estate sales and leasing brokerage, house decoration and renovation services, etc.).

In addition, in order to expand their service scope and improve profitability, leading participants not only choose to compete with existing giants in some highly potential value-added areas such as housing sales and rental brokerage, home decoration services, etc., but also begin to enter new markets that intersect or are related to property management services.

-

technology phase

Driven by the development of advanced technology, leading market participants have begun to explore the application of technology in property management services, leading the industry into a technological phase. At this stage, some industry leaders are combining basic property management services and value-added services with technology-enabled solutions (such as smart property consulting services, comprehensive smart space solutions, remote enterprise operation services, and remote space operation services), starting to explore new profit models.

With the development of the property management service industry, some leading market participants are no longer positioning themselves as mere 'property management service providers', but rather as 'property management and commercial operation service providers', 'comprehensive urban operation service providers', or 'comprehensive property management and lifestyle service operators'. The term 'space management services' has begun to become an industry-recognized terminology, reflecting the changes in the industry's development.

Currently, apart from leading market participants such as Wanyun Cloud, which are developing ahead of their peers and starting to compete in various markets, most property management service companies mainly provide services for residential properties as well as non-residential properties such as office buildings, shopping centers, public utilities (government buildings, hospitals, schools, etc.), industrial parks, etc.

Property management service companies typically provide the following services: (i) Basic property management services, including order maintenance, cleaning, repair and maintenance, garden landscaping, etc.; and (ii) Value-added services, including value-added services for property developers and community value-added services. The value-added services provided for property developers mainly include on-site services, pre-property management services, pre-delivery services, repair and maintenance services, and other event-based services. Community value-added services mainly include house decoration and renovation services, house sales and rental brokerage services, public area operation services, parking space sales services, mechanical and electrical equipment maintenance services, etc.

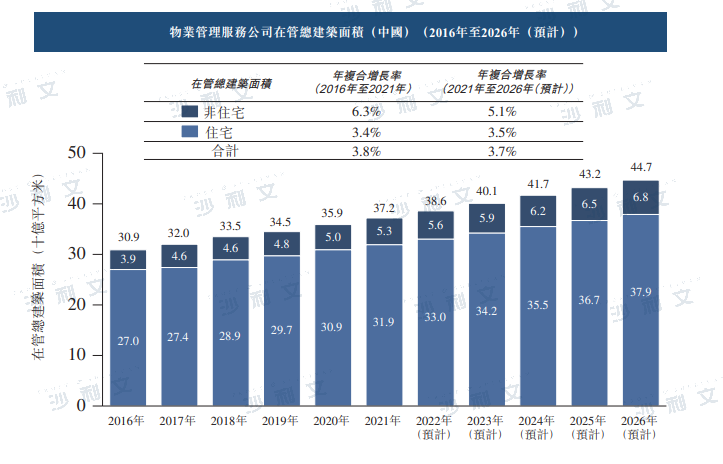

The total managed construction area of property management service companies in China increased from 30.9 billion square meters in 2016 to 37.2 billion square meters in 2021, with an overall annual compound growth rate of 3.8%. In 2021, the total managed construction area of residential properties in China reached 31.9 billion square meters, with an overall annual compound growth rate of 3.4% from 2016 to 2021. In 2021, the total managed construction area of non-residential properties reached 5.3 billion square meters, with an overall annual compound growth rate of 6.3% from 2016 to 2021. By 2026, it is expected that the total managed construction area will reach 44.7 billion square meters, with an overall annual compound growth rate of 3.7% from 2021 to 2026. The following chart lists the total managed construction area of property management service companies in China from 2016 to 2026:

Source: Frost & Sullivan report

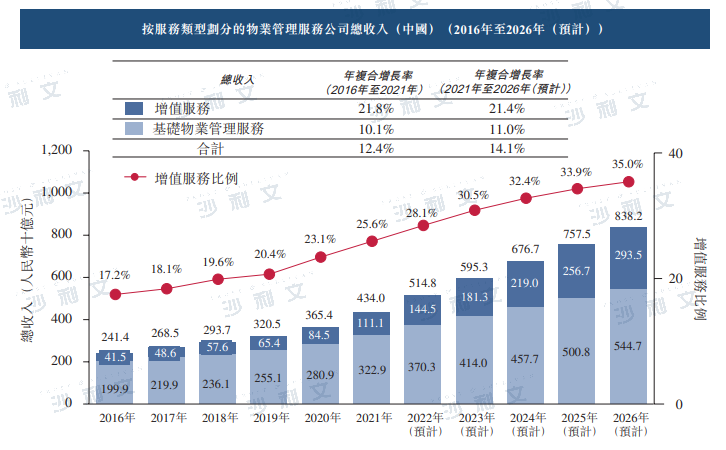

The competition in the property management service market in China is fierce and highly fragmented. In 2021, the revenue of property management service companies mainly came from basic property management services, accounting for about 74.4%. In recent years, property management service companies have been striving to diversify their services and revenue sources. As services become increasingly diversified, the total revenue from value-added services provided by these companies has increased from RMB 415 billion in 2016 to RMB 1111 billion in 2021, with an overall annual compound growth rate of 21.8%. It is expected to reach RMB 2935 billion by 2026, with an overall annual compound growth rate of 21.4% from 2021 to 2026. From 2016 to 2021, the proportion of value-added services in the total revenue of property management service companies increased from 17.2% to 25.6%, and is expected to reach 35.0% by 2026. The following chart lists the total revenue of property management service companies in China classified by service type from 2016 to 2026:

Source: Frost & Sullivan report

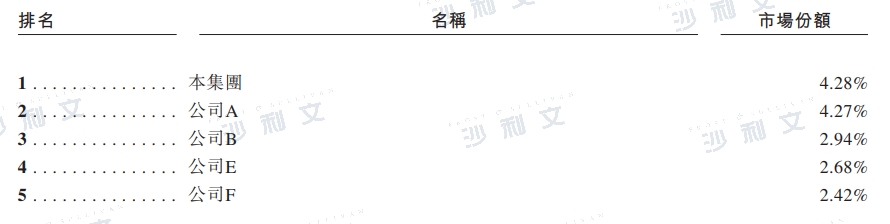

In 2021, based on basic property management service revenue, Wumart Cloud ranked first in the Chinese property management service market, with a market share of 4.28%. The following table lists the details of the top five service providers in the Chinese property management service market by basic property management service revenue in 2021:

Note:

a) Basic property management services mainly include order maintenance, cleaning, repair and maintenance, as well as garden landscape services. The revenue is based on basic property management income, as the service coverage of value-added services provided by the top five property management service providers varies and they are not fully comparable.

b) The revenue of Company A does not include the 'Three Supplies and One Page' business.

Data source: Annual reports of listed companies, Frost & Sullivan reports

China's Community Space Residential Consumption Service Market

The Chinese community space residential consumption service market provides three main categories of services: (i) basic residential property management services; (ii) residential-related asset services; and (iii) community value-added services. Basic residential property management services include maintenance and repair, gardening, cleaning, and order maintenance services. Residential-related asset services include housing sales and rental brokerage services, as well as housing renovation and home improvement services. Housing sales and rental brokerage services refer to housing sales services (including new and existing house sales) and housing rental services, while housing renovation and home improvement services include providing decoration design services, renovation, and construction. Community value-added services mainly include public area operation services, parking space sales services, mechanical and electrical equipment maintenance services, etc.

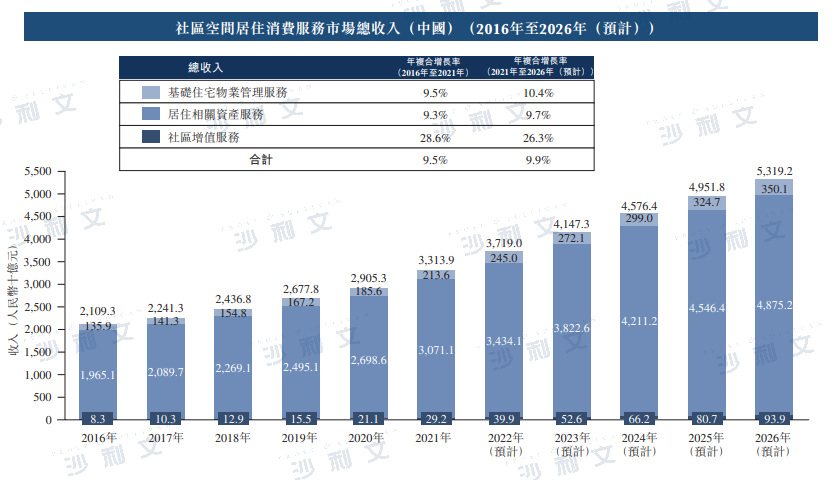

The total revenue of China's community space residential consumption service market has increased from RMB 2,109.3 billion in 2016 to RMB 3,313.9 billion in 2021, with an overall annual compound growth rate of 9.5%. It is expected that by 2026, the revenue will reach RMB 5,319.2 billion, with an overall annual compound growth rate of 9.9% between 2021 and 2026.

In the residential consumption service market within community spaces, the total revenue from basic residential property management services has increased from RMB 135.9 billion in 2016 to RMB 213.6 billion in 2021, with an annual compound growth rate of 9.5%. It is expected that by 2026, it will reach RMB 350.1 billion, with an annual compound growth rate of 10.4% from 2021 to 2026.

The total revenue from community value-added services has increased from RMB 8.3 billion in 2016 to RMB 29.2 billion in 2021, with an overall annual compound growth rate of 28.6%. It is expected that by 2026, the revenue will reach RMB 939 billion, with a compound annual growth rate of 26.3% between 2021 and 2026.

The total revenue of the residential-related asset service market has increased from RMB 1,965.1 billion in 2016 to RMB 3,071.1 billion in 2021, with an annual compound growth rate of 9.3%. It is expected to reach RMB 4,875.2 billion by 2026, with an annual compound growth rate of 9.7% from 2021 to 2026. The following chart lists the total revenue of China's community space residential consumption service market from 2016 to 2026:

Source: Frost & Sullivan report

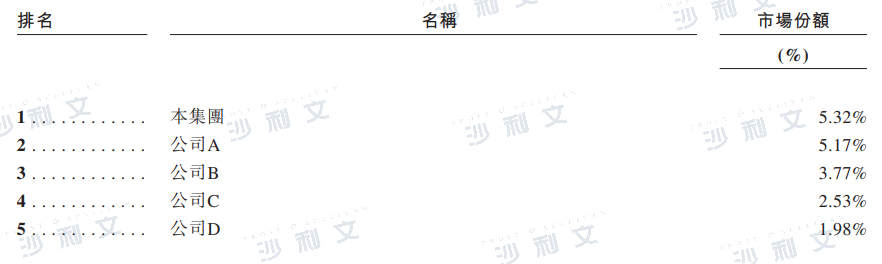

Among the three major sectors of the residential consumption service market in China's community space, the basic residential property management service market is a key focus for Everything Cloud. In 2021, the total revenue of the basic residential property management service market in China reached RMB 213.6 billion. Based on the revenue in 2021, the top five service providers accounted for about 18.77% of the market share. In 2021, ranked by revenue, Everything Cloud was the first in the basic residential property management service market in China, capturing a market share of 5.32%. The following table lists the details of the top five service providers in the basic residential property management service market in China, categorized by revenue in 2021:

Total revenue of Suzhou Property Management Service Company

Note:

a) The revenue of Company A does not include the 'three supplies and one page' business.

Data source: Annual reports of listed companies, Frost & Sullivan reports

Driving factors of the community space residential consumption service market

Urban population and per capita disposable income growth:The steady growth of China's urban population and per capita disposable income has led to an increasing demand for high-quality community space living consumption services. China's urbanization rate increased from 57.4% in 2016 to 64.7% in 2021. China's urban population has been steadily growing, rising from 7.93 million people in 2016 to 9.143 billion people in 2021, with an annual compound growth rate of 3.3%. The per capita disposable income of urban residents in China also increased steadily from 33,616 yuan in 2016 to 47,412 yuan in 2021, with an annual compound growth rate of 7.1%. As a result, residential sales area has significantly increased, thereby stimulating the demand for community space living consumption services. On the other hand, with the increase in per capita disposable income, people pursue better living environments and are more willing to pay for high-quality community space living consumption services, such as butler services, which are personalized services provided by community space living consumption service providers before and after owners move into their new homes.

Rapid development in first-tier, new first-tier, and second-tier cities:The urban population in first-tier cities, new first-tier cities, and second-tier cities has been growing steadily, with annual compound growth rates of 3.2%, 5.7%, and 4.0% between 2016 and 2021, respectively. In addition, from 2021 to 2026, the annual compound growth rates of per capita disposable income for urban families in first-tier cities, new first-tier cities, and second-tier cities are expected to reach 7.1%, 7.0%, and 7.1%, respectively. Residents in first-tier, new first-tier, and second-tier cities have strong consumer power and have higher expectations for living environments and residential service quality. Correspondingly, the continuous development of first-tier, new first-tier, and second-tier cities will further drive the development of the community space residential consumption service market in China.

House leasing, renovation, and home improvement services are becoming increasingly common:With limited new housing supply and continuous rising housing prices, the volume of second-hand housing transactions and rental transactions has been on the rise over the past five years. The volume of existing home transactions increased from 2.13 million units in 2016 to 5.92 million units in 2021, with an annual compound growth rate of 22.7%. In addition, benefiting from the government's support for fully furnished houses, the demand for house redecoration and luxury living services has further increased, allowing community space residential consumption service providers to enter this market and compete with existing home improvement companies.

Opportunities for the Future Development of the Community Space Residential Consumption Service Market

Great market potential:The community space residential consumption service market has tremendous market potential, and industry revenue is steadily increasing. The increase in urban population leads to an expansion of the consumer base for community space residential consumption services. Moreover, the per capita disposable income of families in first-tier, new first-tier, and second-tier cities has risen, making the demand for high-quality community space residential consumption services more urgent. In addition, the service scope of the community space residential consumption service market has been continuously expanding, bringing new growth points to the market and making residential-related asset services an important part.

Accelerate industrial concentration:In recent years, the concentration of the community space residential consumption service market has been continuously increasing due to major providers acquiring other participants. They are also actively seeking alliances and mergers to achieve economies of scale. It is expected that leading community space residential consumption service providers will continue to enhance their competitiveness, consolidate their market share, expand service offerings, and further increase the concentration of the Chinese community space residential consumption service market.

Improve service quality:With the enhancement of consumer awareness and the increase in per capita disposable income, property owners now pay more attention to service quality when choosing community space residential consumption service providers and pursue better living conditions and community environments. The growth in consumers' purchasing power has also raised the quality standards for operations and services. In the future, it is expected that community space residential consumption service providers will continuously improve service quality and operational capabilities by applying information technology for optimization and upgrading services.

Apply new technologies:With the rapid development of information technology, big data, cloud computing, and other new technologies in China, the digitalization and intelligent transformation of the community space residential consumption service market has become one of the mainstream trends for the future. Specifically, the development of information technology and digitization enables community space residential consumption service providers to improve service quality and reduce operating costs. Providers can use smart access control and parking systems to provide better convenience for citizens, as well as reduce labor costs and energy consumption for operating enterprises. They can also utilize social media, mobile applications, and other technical tools to effectively integrate and allocate community resources.

China Commercial Enterprise and Urban Space Integrated Service Market

The Commercial Enterprise Space Comprehensive Service provides two types of services, including: (i) Property and Facilities Management Services, mainly comprising order maintenance services, cleaning services, greening services, facilities operation and maintenance, environmental, health and safety management, comprehensive administrative support, event support, and protocol services; and (ii) Value-added services for developers, including pre-delivery services, building renovation and repair services, as well as site visits and model apartment services.

Urban space mainly includes government buildings, schools, hospitals, roads, streets, and other urban spaces. Urban spatial integration services include three types of services: (i) Spatial governance, which mainly includes urban cleaning and sanitation services, maintenance of municipal infrastructure, as well as management services for the safety and order of urban public spaces (including indoor and outdoor areas open to the public); (ii) Urban special facility operations, including water quality control driven by technology, maintenance and protection of river systems, and comprehensive management of urban parks; and (iii) Operation and management of old residential areas, mainly including management and renovation services for old residential areas.

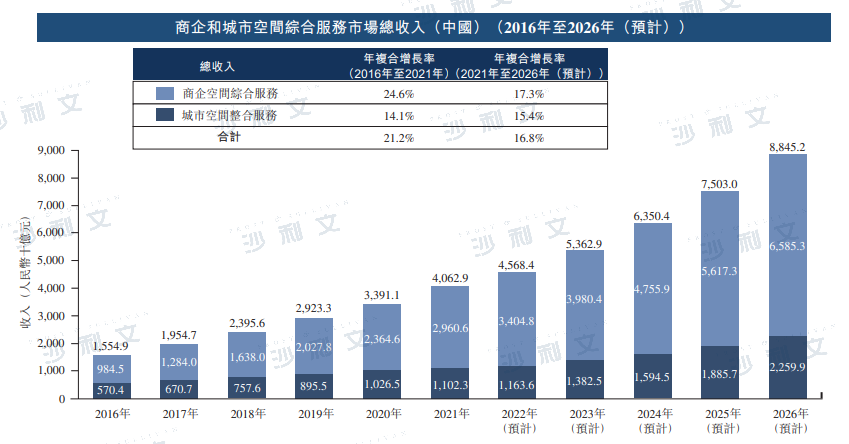

The total revenue of the China business enterprise and urban space integrated service market has increased from RMB 1,554.9 billion in 2016 to RMB 4,062.9 billion in 2021, with an overall annual compound growth rate of 21.2% from 2016 to 2021. It is estimated that the revenue of the China business enterprise and urban space integrated service market will reach RMB 8,845.2 billion by 2026, with an overall annual compound growth rate of 16.8% from 2021 to 2026. The following chart shows the total revenue of the China business enterprise and urban space integrated service market from 2016 to 2026:

Source: Frost & Sullivan report

With the continuous expansion of commercial space and service scope, as well as the increasing awareness of related service outsourcing (especially administrative outsourcing), China's property and facilities management services market is expected to maintain rapid growth over the next five years. It is estimated that by 2026, the property and facilities management market will reach RMB 6,385.7 billion, with a compound annual growth rate of 17.3% from 2021 to 2026. At the same time, it is projected that the developer value-added services market will reach RMB 199.6 billion by 2026, with a compound annual growth rate of 19.5% from 2021 to 2026. The following chart shows the total revenue of China's commercial space comprehensive service market from 2016 to 2026:

Source: Frost & Sullivan report

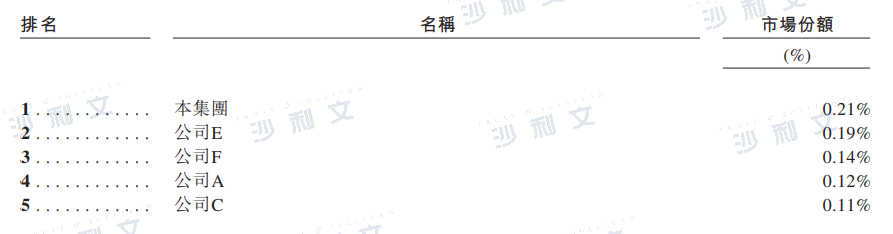

The revenue of China's commercial enterprise and urban space integrated service market reached 4,062.9 billion yuan in 2021. The competition in the commercial enterprise and urban space integrated service market is fierce and fragmented. In this market, based on revenue in 2021, the top five commercial enterprise and urban space integrated service providers accounted for 0.77% of the market share, among which our group ranked first with a market share of 0.21%. The following table lists the details of the top five commercial enterprise and urban space integrated service providers in China's market based on revenue in 2021:

Note:

a) The revenue of Company A does not include the 'Three Supplies and One Page' business.

Data source: Annual reports of listed companies, Frost & Sullivan reports

Driving factors of the business enterprise and urban space integrated service market

Urbanization process and economic regional development:The development of China's macroeconomy has driven the urbanization process and the increase in per capita disposable income, thereby boosting the development of comprehensive business and urban space services markets. The proportion of urban population in China increased from 57.4% in 2016 to 64.7% in 2021. At the same time, per capita disposable income of urban residents rose from RMB 33,616 in 2016 to RMB 47,412 in 2021, with an annual compound growth rate of 7.1%. This has led to an increasingly concentrated population that requires more carefully designed business and urban spaces, as well as better working and urban environments, thereby driving an increase in the demand for comprehensive business and urban space services and improving the quality of these services. On the other hand, the Chinese government has implemented a new urbanization strategy, including promoting sustainable urban development that is eco-friendly and low-carbon footprint, providing better services for urban residents, and increasing the use of electronic devices to collect specific operational data. These plans have put forward stricter requirements for governance methods, thereby stimulating the demand for professional services in urban public spaces. In addition, the Chinese government has been cultivating more developed economic regions over the past decade, such as promoting the development of the Chengdu-Chongqing Twin-City Economic Circle. This move has further stimulated China's demand for comprehensive business space services.

The stable development of business space and comprehensive business space services:Business space expansion has been rapid. In 2021, the total construction area of business properties in China reached 900 million square meters. In addition, due to favorable economic development, government policies, and a good business environment, more and more domestic and international companies are establishing headquarters in first-tier and new first-tier cities. These factors together bring tremendous market potential to the comprehensive service market for business space in China. Moreover, in recent years, more and more companies have begun to hire professional comprehensive service providers for business space to achieve higher investment returns and management efficiency. Comprehensive comprehensive services for business space can also help companies concentrate their management resources on their core business departments, which in the long run will increase the demand for comprehensive services for business space and improve its penetration rate.

Beneficial policies:Since the Third Plenary Session of the 18th Central Committee in 2013, which resolved to allow social capital to participate in urban infrastructure investment and operation through franchise operations, the government has issued a series of policies to encourage private capital investment and management of urban services. For example, the 'Implementation Opinions on Further Strengthening Urban Refined Management' issued by local governments in 2020 proposed that the government will guide and encourage social capital to actively participate in investment and operation of urban services, and promote the use of a cooperation model between government and social capital. The 'Guiding Opinions on Comprehensively Promoting the Transformation of Old Urban Residential Areas' issued by the government in 2020 also proposed that the government will improve urban functions by optimizing the urban road system, improving municipal public infrastructure, and accelerating the renovation of old residential areas.

Opportunities for the future development of business enterprise and urban space integrated service markets

Technology Empowerment:The development of information technology, especially related technologies such as 5G, artificial intelligence, and the Internet of Things (IoT), enables businesses and urban space comprehensive service providers to improve service quality and effectively reduce costs. For example, intelligent building integrated management, smart security patrols, and intelligent parking lot management systems have been embedded into business space comprehensive services. In the future, it is expected that business space comprehensive service providers will use technological applications to expand their service scope and improve service quality. At the same time, urban space integration service providers have already utilized advanced technologies such as IoT, cloud platforms, and big data to achieve intelligent and digital urban space integration services by improving urban operational efficiency.

Shift towards a more integrated service model:Driven by customers' more comprehensive needs and the expansion of business space, comprehensive service providers for business spaces will expand their service scope. In addition to traditional property services, they will offer high-quality integrated services (such as energy consumption management services, human resource management services, and pre-delivery services) to meet customer needs. This will prompt the comprehensive service market for business spaces towards a more integrated model.

Enhanced breadth and depth of services:The state and local governments have issued a series of incentive policies to promote the development of headquarters economy and raise funds for fixed asset investment projects. As a result, there is a new trend where higher-end commercial spaces (including corporate buildings for international corporate regional headquarters) are seeking more comprehensive services for various types of commercial spaces, such as facility management services and IT management services, as well as in-depth services covering the entire service cycle. At the same time, the scope of services provided by urban space integration service providers has been expanding. In addition to traditional operations and maintenance services, they also offer urban management and planning services, such as providing rental services for state-owned properties and organizer services for public institutions.

Strengthening the Urban Butler Function:With the reform of 'delegating power, improving regulation, and optimizing services', the government has shifted from a management-oriented to a service-oriented government. The 'delegating power, improving regulation, and optimizing services' initiative has also given rise to new urban management models. Under this model, the government purchases public services from society, allowing urban space integration service providers to carry out urban space integration services, thereby strengthening their function as 'urban stewards'.

Operating Arrangement:Urban spatial integration service providers have expanded their scale and enhanced their market competitiveness by establishing joint ventures or associates with state-owned enterprises. Since local governments have long been engaged in the urban spatial integration service industry, service providers can gain industry experience and resources through cooperation with local governments. In addition, by establishing joint ventures or associates with state-owned enterprises, service providers can quickly expand the scale of projects they undertake and accumulate industry experience.

Frost & Sullivan has extensive research experience in the property and real estate industry, assisting well-known enterprises in successfully listing on capital markets. Successful listings include: Suxin Good Life (2152.HK), Desheng Property Investment (2270.HK), China Resources Vanguard (1209.HK), Excellence Business Enterprise (6989.HK), Mingyuan Cloud (0909.HK), Bao Long Commercial (9909.HK), China Tianbao (1427.HK), Yincheng Living Services (1922.HK), Fangduo (NASDAQ:DUO), Xinyuan Technology Services (1895.HK), CSI Holdings (NASDAQ:CIH), Lejia Si Holdings (1867.HK), Aoyuan Health (3662.HK), Chuangyi Holdings (3992.HK), Joyou Property (2168.HK), Baoyan Holdings (8601.HK), Hengyu Group (2448.HK), Yajiu Investment Holdings (8426.HK), Red Star Macallan (1528.HK), and others.

Recommended Reading

01. Frost & Sullivan helps Suxin Service successfully list in Hong Kong (2152.HK)

02. Frost & Sullivan helps Desheng Property Investment successfully list in Hong Kong (2270.HK)

03. Frost & Sullivan helps China Resources Vanguard successfully list in Hong Kong (1209.HK)

05. Frost & Sullivan helps Mingyuan Cloud successfully list in Hong Kong (0909.HK)

06. Frost & Sullivan helps Bao Long Commercial successfully list in Hong Kong (9909.HK)

07. Frost & Sullivan helps China Tianbao successfully list in Hong Kong (1427.HK)

08. Frost & Sullivan helps Yincheng Living Services successfully list in Hong Kong (1922.HK)

09. Frost & Sullivan helps Fangduo successfully list in the US (NASDAQ:DUO)

10. Frost & Sullivan helps Xinyuan Service successfully list in Hong Kong (1895.HK)

11. Frost & Sullivan helps CSI Holdings successfully list in the US (NASDAQ:CIH)

12. Frost & Sullivan helps Lejia Si Holdings successfully list in Hong Kong (1867.HK)

13. Frost & Sullivan helps Aoyuan Health successfully list in Hong Kong (3662.HK)

14. Frost & Sullivan helps Chuangyi Holdings successfully list in Hong Kong (3992.HK)

15. Frost & Sullivan helps Joyou Property successfully list in Hong Kong (2168.HK)

16. Frost & Sullivan helps Baoyan Holdings successfully list in Hong Kong (8601.HK)

17. Frost & Sullivan helps Hengyu Group successfully list in Hong Kong (2448.HK)

18. Frost & Sullivan helps Yajiu Investment successfully list in Hong Kong (8426.HK)

19. Frost & Sullivan helps Red Star Macallan successfully list in Hong Kong (1528.HK)

*The above order is not chronological and is arranged in reverse order of listing time