Healthy Therapeutics Group Co., Ltd. (hereinafter referred to as 'Healthy Therapeutics') was officially listed on the Swiss Stock Exchange at Zurich time on September 26, 2022, with the final issue price of GDRs being $14.42 per share. The company issued a total of 6,382,500 GDRs, representing 63,825,000 underlying A-share stocks, raising approximately $92 million in total funds.

During the listing process on the Hong Kong Stock Exchange, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, global coordinators, and other professional intermediary institutions in completing the writing of relevant parts of the prospectus (such as an overview, key competitive advantages, industry and market overview, business, and other important sections), helping the issuer communicate with the Hong Kong Stock Exchange and investors, and assisting investors in quickly understanding the market ecosystem and competitive landscape.

Healthcare Yuan is a comprehensive pharmaceutical company with strong commercial capabilities, extensive R&D layout, and sustainable development. In terms of R&D investment, in 2021, Healthcare Yuan's R&D investment accounted for more than 10%, ranking fifth among listed comprehensive pharmaceutical companies in China. Healthcare Yuan has made strategic investments in multiple fields such as respiratory, digestive, and assisted reproductive medicine, targeting large patient populations and unmet clinical needs in these areas.

Healthcare Yuan has achieved revenue growth for 15 consecutive years. In 2021, it ranked sixth among listed comprehensive pharmaceutical companies in China in terms of revenue. In 2021, in terms of terminal sales, the company ranked among the top five in the Chinese respiratory system disease inhalation preparations market, the Chinese proton pump inhibitor drug market, and the Chinese gonadotropin drug market, and among the top three among domestic manufacturers. In the first half of 2022, Healthcare Yuan invested RMB 805 million in research and development, a year-on-year increase of 15.39%. As of the end of June, Healthcare Yuan had a total of 249 ongoing projects, including a recombinant novel coronavirus fusion protein vaccine that has been included in the emergency use of sequential booster immunization, and as many as 43 high-barrier complex preparations.

Analysis of the Chinese Respiratory System Disease Drug Market

Respiratory diseases are common and frequently occurring illnesses that can be caused by various factors such as smoking, air pollution, and climate. Asthma and chronic obstructive pulmonary disease (COPD), as representative respiratory diseases, are characterized by high incidence rates, high mortality rates, and long disease courses. Affected by factors such as population aging and changes in lifestyle habits, it is estimated that the number of patients with respiratory diseases will continue to grow in the future, leading to a huge demand for clinical medications. In 2017, the market size of drugs for respiratory diseases in China was RMB 764 billion. Affected by centralized procurement, the market size of drugs for respiratory diseases in China decreased to RMB 751 billion in 2021. With the improvement of the diagnostic rate and standardized treatment rate of respiratory diseases in our country, as well as the continuous growth in clinical medication demand, it is expected that the market size of drugs for respiratory diseases in China will gradually climb in the future.

Analysis of the Inhalation Preparation Market for Respiratory Diseases in China

Inhalation preparations are the preferred dosage form for chronic respiratory diseases such as asthma and COPD, characterized by rapid onset, high bioavailability, and fewer side effects. They can avoid the first-pass effect through the liver and reach the target organs directly, thereby increasing local lung drug concentration while reducing systemic toxicity and the risk of resistance, providing a high-quality solution for long-term maintenance treatment of chronic respiratory diseases. In 2017, the market size of inhalation preparations for respiratory diseases in China was 125 billion yuan, and by 2021, it had reached 195 billion yuan, with a compound annual growth rate of 11.7% during this period. As the use of medications for respiratory diseases in China becomes more standardized, the market for inhalation preparations for respiratory diseases in China will further grow.

At present, most of the market share for inhalation preparations for respiratory diseases in China is still dominated by foreign-funded pharmaceutical companies. Inhalation preparations are complex formulations with high barriers to entry, and the research and development threshold is particularly high for small-sized inhalation preparations. After the first imported budesonide suspension for inhalation was approved in China in 2001, there was nearly 20 years of market monopoly. In 2020, Health Yuan's two specifications of budesonide suspension for inhalation were successively approved, with the small-sized budesonide suspension being the first domestic generic.

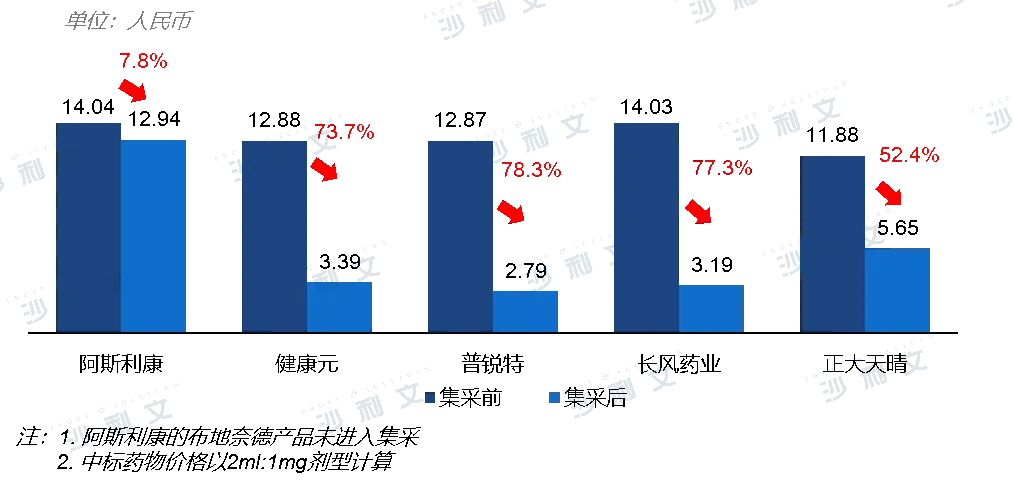

The clinical demand for chronic respiratory diseases is high and there is a long-term need for medication. In 2021, inhaled budesonide suspension was included in the fifth national centralized drug procurement, which provided favorable opportunities for domestic products that had just been launched on the market, increasing their penetration at the hospital level. In the first half of 2022, Health Yuan achieved revenue of 561 million yuan in the field of respiratory diseases, a year-on-year increase of 259%. Driven by import substitution encouragement policies and the improvement of domestic innovative R&D technologies, domestic innovative inhalation preparations are expected to break the import monopoly pattern in the domestic market for respiratory disease inhalation preparations in the future.

Comparison of winning bid prices before and after the centralized procurement of budesonide inhalation suspension

Source: CDE, Frost & Sullivan analysis

Analysis of the Chinese Digestive Tract Disease Drug Market

Digestive tract medications mainly include antacids, anti-flatulence drugs, anti-ulcer drugs, cholagogues, liver-protecting drugs, and antiemetics, among which antacids, anti-flatulence drugs, and anti-ulcer drugs are widely used in the treatment of digestive tract ulcers, gastroesophageal reflux, and other diseases related to gastric acid and gastrointestinal flatulence. Affected by factors such as irregular diet and sleep patterns, accelerated pace of life, and increased life pressure, the clinical demand for digestive tract medications is continuously climbing. In 2017, the market scale of digestive tract medications in China was RMB 131.2 billion, and in 2021, it reached RMB 142.8 billion. During this period, the compound annual growth rate was 2.2%, and it is expected that the market for digestive tract medications in China will continue to grow steadily in the future.

Analysis of the Market for Proton Pump Inhibitors in China

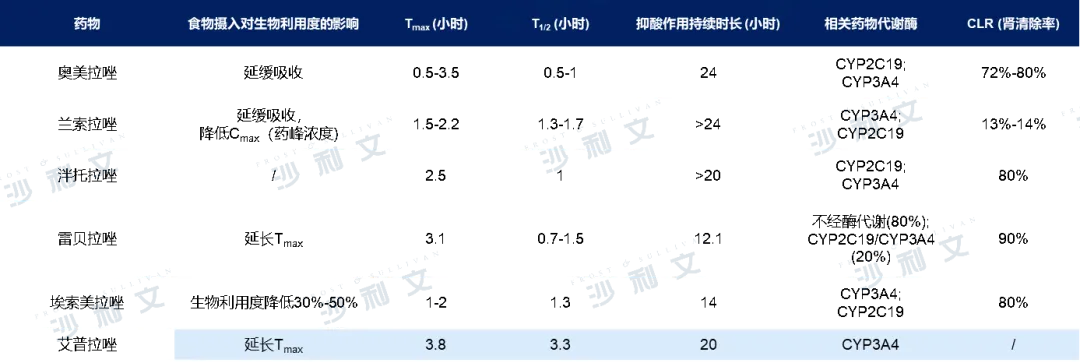

Proton pump inhibitors are currently one of the most potent drugs for inhibiting gastric acid secretion and are commonly used in clinical practice to treat digestive tract diseases such as gastroesophageal reflux and duodenal ulcers. In 2017, the market size of proton pump inhibitor drugs in China was 251 billion yuan. Affected by centralized procurement, the market size of proton pump inhibitor drugs in China declined to 227 billion yuan in 2021. Commonly used proton pump inhibitors include omeprazole, lansoprazole, pantoprazole, rabeprazole, esomeprazole, and ilaprazole, which can block gastric acid secretion by inhibiting H+/K+-ATPase compounds.

The core product of Health Yuan in the field of digestive tract diseases, esomeprazole sodium for injection, as the only product under this generic name, has several advantages such as less impact from food intake, stable and sustained onset, and higher safety without being affected by CYP2C19 (drug metabolism enzyme) gene polymorphisms. At the end of 2021, the product was renewed in the national medical insurance negotiation with a price reduction from 156 yuan to 71 yuan, a decrease of 54.5%. Although the product price was affected by the national negotiation renewal, considering the outstanding clinical application value of esomeprazole sodium, Health Yuan's revenue in this disease area in the first half of 2022 was still quite substantial, reaching as high as 1.781 billion yuan. In the future, the renewal of the national medical insurance negotiation will further increase the product coverage at the hospital level, with a promising prospect.

Comparative analysis of proton pump inhibitors

Data source: Literature review, drug instructions, Frost & Sullivan analysis

Analysis of the Market for Sex Hormones and Reproductive System Regulators in China

Sex hormone and reproductive system regulation drugs include estrogens, androgens, progesterone, anti-androgens, systemic hormonal contraceptives, gonadotropins, and other ovulation-stimulating drugs. In 2017, the market size of sex hormone and reproductive system regulation drugs in China was 21.4 billion yuan, and by 2021, it had grown to 26.3 billion yuan. The compound annual growth rate during this period was 5.3%, and it is expected that the market will continue to grow in the future.

Leuprorelin, as a representative gonadotropin drug, can be used to treat various endocrine diseases such as endometriosis and uterine fibroids. There is a high clinical demand for it, but it is ineffective when taken orally and must be administered by injection. Currently, only three products of leuprorelin for injection have been approved in China, all of which are microsphere preparations, resulting in a relatively balanced market pattern that can show steady and continuous growth. Leuprorelin for injection microspheres are classified as Class B medical insurance drugs and have been included in multiple clinical guidelines and expert consensuses, with widespread clinical application. Microsphere preparations can effectively improve the bioavailability of drugs and achieve long-acting, targeted dosing, thereby reducing the dosage and frequency of administration and improving patient compliance. The development of microsphere preparations is challenging, and Health Yuan is one of the three domestic manufacturers that have successfully commercialized sustained-release microspheres to date.

Frost & Sullivan, integrating 61 years of global consulting experience, has dedicated 24 years to serving the booming Chinese market. With a global perspective, we help clients accelerate their business growth, achieving benchmark positions in industry growth, innovation, and leadership. The healthcare industry is one of the core areas of focus for Frost & Sullivan. Over the past 20-plus years, the Frost & Sullivan team has provided financing and financial advisory services, IPO industry advice, strategic consulting, management consulting, and other services to hundreds of outstanding domestic and international biopharmaceuticals, medical devices, healthcare services, and internet healthcare companies. Successful listings include: Dingdang Health (9886.HK), Bioriginal (2315.HK), Zhiyun Health (9955.HK), MeinGene (6667.HK), Prenetics (PRE.NASDAQ), Yunkang Group (2325.HK), Rike Biotech (2179.HK), Lepu Biotech (2157.HK), Clear Medical (1406.HK), Baxin An (2185.HK), Yonghe Medical (2279.HK), Kailaiying (6821.HK), Beihai Kangcheng (1228.HK), Gusheng Tang (2273.HK), Yingpeng Technology (2251.HK), Clover Biotech (2197.HK), Minimally Invasive Robotics (2252.HK), Harmony Cayman (2256.HK), Kunbo Medical (2216.HK), Xianruida (6669.HK), Kangsheng Global (9960.HK), Yimaitong (2192.HK), Tengsheng Boyao (2137.HK), CanSino (2162.HK), Chaopu Ophthalmology (2219.HK), Guichuang Tongqiao (2190.HK), Hua Huang Medicine (0013.HK), Codel Therapeutics (2171.HK), Zhaoke Ophthalmology (6622.HK), Nature Pharmaceuticals (UPC.NASDAQ), Saisun Pharmaceutical (6600.HK), Zhaoyan New Drugs (6127.HK), Novogene Health (6606.HK), Tianyan Pharmaceuticals (ADAG.NASDAQ), Beikang Medical (2170.HK), Jianbimiao Miao (2161.HK), Minimally Invasive Heart Center (2160.HK), Ruili Medical Beauty (2135.HK), Jiaosisi Pharmaceutical (1167.HK), Hepcon Pharma (2142.HK), JD Health (6618.HK), Deqi Pharma (6996.HK), Rongchang Biotech (9995.HK), WuXi AppTec (2126.HK), Simcere Pharmaceutical (2096.HK), Yunding New Energy (1952.HK), Jiahe Biotech (6998.HK), Zai Ding Pharma (9688.HK), Ekonvitis (1477.HK), Yongtai Biotech (6978.HK), Haipure Pharma (9989.HK), Kechuang Pharmaceutical (9939.HK), Peijia Medical (9996.HK), Kangfang Biotech (9926.HK), Nuo Cheng Jianhua (9969.HK), IMAB.NASDAQ, Kanglong Chemical (3759.HK), China Antibody (3681.HK), Dongyao Pharmaceutical (1875.HK), Yasheng Pharmaceutical (6855.HK), Fuhong Hanlin (2696.HK), Hansoh Pharmaceutical (3692.HK), Mabtech Pharma (2181.HK), Fangda Holdings (1521.HK), Via Bio (1873.HK), Cornerstone Pharmaceuticals (2616.HK), Junshi Biosciences (1877.HK), WuXi AppTec (2359.HK), Innovent Biologics (1801.HK), Hualing Medicine (2552.HK), BeiGene (6160.HK), Gilead Sciences (1672.HK), WuXi AppTec (2269.HK), China Resources Medicine (3320.HK), Jacobson Scientific Research Pharmaceutical (2633.HK), Hua Huang China Medicine (HCM.NASDAQ), Kingsbridge Biotechnology (1548.HK), BBI Life Sciences (1035.HK), etc. In terms of the number of filings, the Frost & Sullivan healthcare team maintains an absolute leading position in Hong Kong's healthcare IPO market, consistently ranking first in market share from 2018 to 2021.

Since the listing of the first batch of companies on the Sci-tech Innovation Board in July 2019, Frost & Sullivan reports have been widely cited in the prospectuses of leading Sci-tech Innovation Board listed companies in the industry. These include: Nuo Cheng Jian Hua (688428.SH), Aopu Mai Biotech (688293.SH), MicroPort Electrodiagnostics (688351.SH), Mengke Pharmaceutical (688373.SH), Yifang Biotech (688382.SH), Jicui Yaokang (688046.SH), Haichuang Pharmaceutical (688302.SH), Rongchang Biotech (688331.SH), Rendu Biotech (688193.SH), Shouyao Holdings (688197.SH), Heyuan Biotech (688238.SH), Yaxin Security (688225.SH), Xidi Micro (688173.SH), Mawei Biotech (688062.SH), Yahong Medicine (688176.SH), BeiGene (688235.SH), Jiahe Meikang (688246.SH), Dizhe Medicine (688192.SH), Novogene (688105.SH), Chengda Biotech (688739.SH), Geke Micro (688728.SH), Huaxi Biotech (688363.SH), Junshi Biotech (688180.SH), Zhejiang Oncology (688266.SH), BeiGene (688177.SH), and Shenzhou Cells (688520.SH). They are considered one of the most powerful, professional, and influential industry research institutions in the sector. We hope to work with enterprises to understand industry trends, seize development opportunities, jointly promote innovation and upgrading of China's healthcare industry, and build a healthy future.

Recommended Reading

05. Frost & Sullivan Assists Prenetics in Successful Listing on the US Stock Market (NASDAQ:PRE)

29. Frost & Sullivan assists Nature Pharma in successfully going public on the NASDAQ:UPC)