China International Travel Service Group Co., Ltd. (hereinafter referred to as 'CITIC Travel') successfully listed on August 25, 2022, with a global issuance of 10.3 million shares at a price of HK$158.00 per share, raising approximately HK$158.92 billion in net proceeds.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in writing relevant parts of the prospectus (such as overview, competitive advantages and strategy, industry overview, business, and other important sections), facilitating communication between the issuer, investment banks, and other intermediaries with the Hong Kong Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange, etc.

Overview of the global tourism retail market

Major categories of tourism retail by commodity type

The tourism retail market can be divided into two categories based on the types of goods sold: duty-free items and taxable items:

Exempted items: The sale of exempted items refers to imported goods that are exempt from customs duties and import taxes, as well as domestic products that are refunded (exempted) from taxes and sold in duty-free stores. Such goods are generally sold to cross-border travelers or those heading to island destinations.

Taxable goods: The sale of taxable goods refers to the sale by travel retailers of taxable goods in a tourism environment where taxes are levied on goods.

Main categories of tourism retail by distribution channel

Tax-free and taxable goods are sold in the tourism retail market through various sales channels, mainly including port stores, island resorts stores, city stores, and others:

Port Store: A port store refers to a retail tourism shop for 'entry-exit' travel, located at major hubs such as airports, land borders, train stations, cross-border bus stations, and ports. The common customers at port stores are transportation passengers heading to their destinations.

Island Stores: Island stores refer to tourism retail shops that are eligible to operate duty-free and travel retail businesses within designated areas (usually islands), with the duty-free items limited to customers who are leaving the designated area. Island stores attract (i) tourists holding valid identification documents and (ii) local residents who are leaving the designated area. Such stores are generally located in downtown locations or at airports within designated areas.

In-city stores: In-city stores generally refer to tourism retail shops located in the city center that are frequented by (i) foreign nationals who have obtained valid identification documents and exit travel vouchers, and (ii) domestic residents who have returned from abroad within a certain period of time.

Others: Other stores refer to travel retail shops on cruise ships, ferries, or airplanes. Customers who frequently visit such stores are generally passengers traveling by transportation to their destinations.

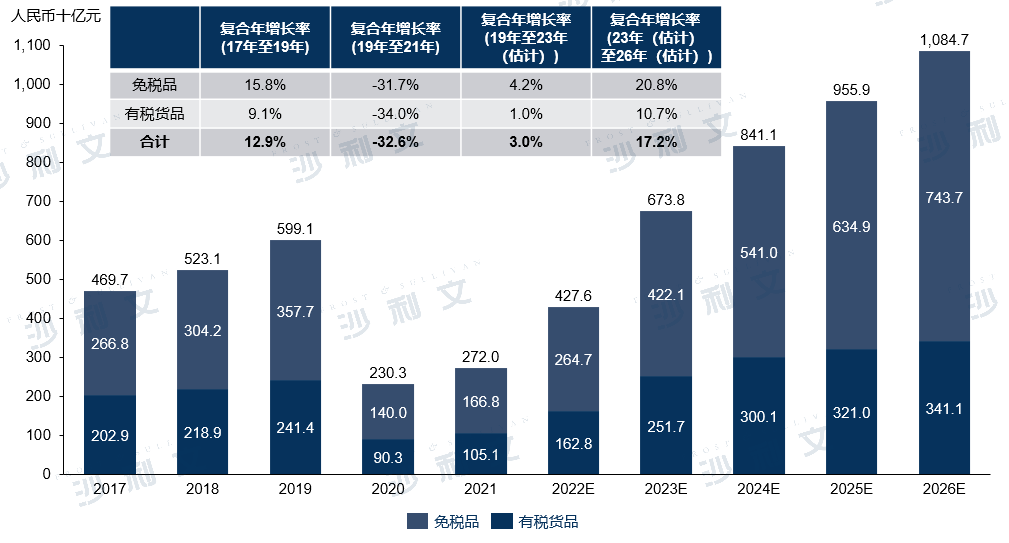

Global tourism retail market size

According to a report by Frost & Sullivan, before the COVID-19 pandemic, the global travel retail market grew steadily, increasing from RMB 469.7 billion in 2017 to RMB 599.1 billion in 2019, with a compound annual growth rate of 12.9%. In 2020 and 2021, the COVID-19 pandemic and related travel restrictions had a significant impact on the global travel retail market, causing its market size to drop sharply to RMB 272 billion in 2021 compared to 2019.

Assuming that overall global international travel restrictions outside China will gradually be relaxed starting from the end of 2022, tourism retail market expectations are expected to recover gradually in 2023 and reach RMB 673.8 billion by 2023. From 2023 to 2026, tourism retail market expectations continue to grow steadily and reach RMB 1.0847 trillion by 2026, with a compound annual growth rate of 17.2% from 2023 to 2026.

Global tourism retail market size (by sales revenue)

2017 to 2026 (estimated)

Source: Frost & Sullivan report

Global tourism retail market competition landscape

According to a Frost & Sullivan report, the global tourism retail market has a relatively high concentration and high entry barriers. In 2021, the top five global travel retailers accounted for 72.5% of the market share based on sales revenue, with CEC ranking first with a market share of 24.6%. The following chart illustrates the market concentration in 2021 and the market shares of the top five global travel retailers based on sales revenue.

Top 5 Global Travel Retailers by Revenue (2021)

Source: Frost & Sullivan report

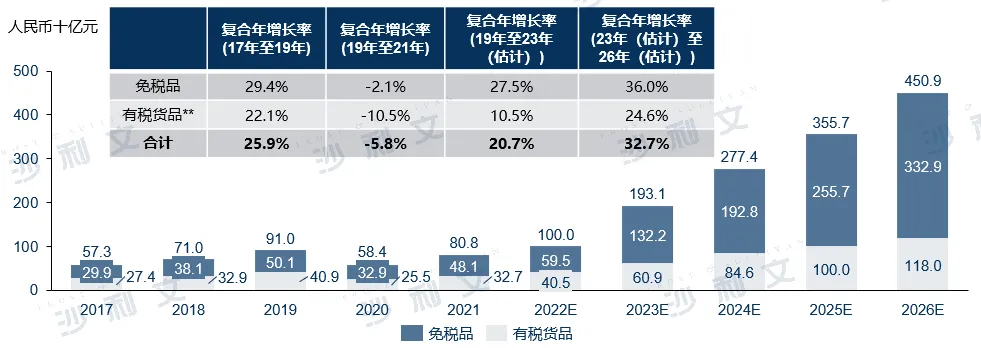

Overview of China's tourism retail market

According to a Frost & Sullivan report, the sales revenue of travel retail goods in China increased from RMB 573 billion in 2017 to RMB 910 billion in 2019, with a compound annual growth rate of 25.9%. In 2020 and 2021, like other regions of the world, local and international tourism in China were affected by the COVID-19 pandemic. However, due to successful control of the epidemic and favorable policies aimed at developing the duty-free market and expanding domestic consumption by the Chinese government, the Chinese travel retail market only declined by a compound annual rate of 5.8% between 2019 and 2021 (compared with a global and Asian decline of 32.6% and 15.4% respectively during the same period), and still reached RMB 808 billion in 2021.

With a market share of 77.8% based on sales revenue in the 2021 China tourism retail market, CEC is the largest participant in this market. In terms of the retail channels for Chinese island tourism, CEC also held the highest market share at 90.1% in 2021, making it the largest player in the island tourism retail market.

In the first half of 2022, due to the emergence of COVID-19 Omicron variant cases in some regions of China, the recovery speed of cross-border and domestic tourism slowed down, further affecting the performance of the tourism retail market. However, considering that the spread of the COVID-19 Omicron variant cases is effectively controlled, cities such as Shanghai have lifted previous lockdowns. Coupled with the government's efforts to accelerate economic recovery and resume business activities by introducing stimulus policies, the market expectations for China's tourism retail will recover. It is estimated that the scale of China's tourism retail market in 2022 will reach RMB100 billion.

Considering recent cases of the COVID-19 Omicron variant, assuming that the spread of the COVID-19 pandemic in China has been gradually controlled since the first half of 2023, and with the gradual recovery of cross-border tourism, driven by the revival of tourism industry, international tourism, and favorable government policies for the development of duty-free markets, the market size of China's travel retail is expected to climb to RMB 450.9 billion before 2026, with a compound annual growth rate of 32.7% from 2023 to 2026. The following chart shows the market size of China's travel retail from 2017 to 2026.

Market scale of China's tourism retail market* (calculated based on sales revenue)

2017 to 2026 (estimated)

* The scale of China's tourism retail and duty-free market does not include duty-free goods that non-island Hainan residents can purchase.

** Taxable goods sales revenue includes online orders placed after departing Hainan by island travelers.

Source: Frost & Sullivan report

China's duty-free market

According to a Frost & Sullivan report, due to the rapid development of tourism and the improvement in residents' income levels, China's duty-free market experienced rapid growth from 2017 to 2019, with a compound annual growth rate of 29.4%. In 2020 and 2021, under the COVID-19 pandemic, China's duty-free market demonstrated resilience due to successful epidemic control, along with favorable policies aimed at developing the duty-free market and expanding domestic consumption by the Chinese government. The market only declined by a compound annual growth rate of 2.1% between 2019 and 2021 (compared to a global and Asian decline of 31.7% and 14.9% respectively during the same period), and still reached 481 billion yuan in 2021.

In the first half of 2022, due to the emergence of COVID-19 Omicron variant cases in some regions of China, the recovery speed of cross-border and domestic tourism slowed down, further affecting the performance of the duty-free goods sales market. However, considering that the spread of the COVID-19 Omicron variant cases is effectively controlled, coupled with the government's efforts to accelerate economic recovery and restart business activities through stimulus policies, the market outlook for duty-free goods sales in China is expected to recover. It is estimated that the scale of duty-free goods sales in China will reach RMB 595 billion in 2022. Favorable government policies will continue to drive future growth of China's duty-free goods market, with the market expected to reach RMB 1322 billion in 2023, with a compound annual growth rate of 27.5% from 2019 to 2023.

Assuming that the spread of the COVID-19 pandemic in China is gradually brought under control starting from the first half of 2023, and cross-border tourism gradually resumes, the market forecast for Chinese duty-free goods is expected to further climb to RMB 332.9 billion by 2026, with a compound annual growth rate of 36.0% from 2023 to 2026.

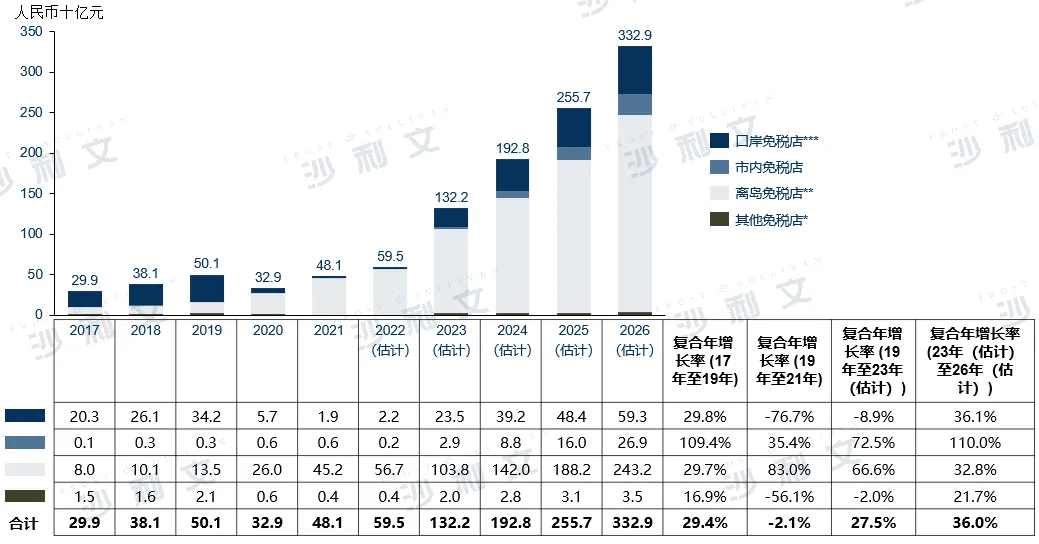

China's duty-free market by channel

According to a Frost & Sullivan report, China's tax-free channels include ports, offshore islands, urban areas, and other tax-free sales channels. The port duty-free store channel and the offshore island store channel are the largest tax-free channels in China, accounting for 94.6% and 97.9% respectively in 2017 and 2021. By 2026, these channels are expected to continue as the main tax-free product sales channels, accounting for 90.9% of tax-free product sales that year.

China's duty-free shops at ports grew rapidly before 2020. The market for duty-free shops at ports increased from RMB 20.3 billion in 2017 to RMB 342 billion in 2019, with a compound annual growth rate of 29.8%. In 2020 and 2021, like duty-free shops at other ports around the world, China's duty-free shops were severely hit by the COVID-19 pandemic. Sales revenue of duty-free shops at ports in China decreased by a compound annual growth rate of 76.7% between 2019 and 2021. In the first half of 2022, due to the emergence of COVID-19 Omicron variant cases in some regions of China, the recovery speed of cross-border tourism slowed down, further affecting the performance of the duty-free commodity sales market at ports. It is estimated that the scale of duty-free commodity sales at ports in China will reach RMB 22 billion in 2022.

Assuming that the spread of COVID-19 in China is gradually brought under control starting from the first half of 2023, and cross-border tourism gradually resumes, the sales revenue of duty-free shops at Chinese ports is expected to gradually recover and further increase to RMB 593 billion by 2026, with a compound annual growth rate of 36.1% from 2023 to 2026.

China's duty-free islands have also seen rapid growth before 2020. The market size of duty-free islands increased from RMB 8 billion in 2017 to RMB 135 billion in 2019, with a compound annual growth rate of 29.7%. With the COVID-19 pandemic largely under control domestically, coupled with favorable policies aimed at developing the duty-free goods market and expanding consumption by the Chinese government, sales of duty-free islands in China have increased significantly. In 2021, sales revenue reached RMB 452 billion, a compound annual growth rate of 83.0% from 2019 to 2021. In the first half of 2022, due to cases of the COVID-19 Omicron variant in some parts of China, domestic tourism to Hainan Island and other destinations was hit, further affecting the performance of the duty-free goods sales market. It is estimated that the market size of duty-free goods sales in China will reach RMB 567 billion in 2022.

Considering that the transmission of COVID-19 Omicron variant cases is effectively controlled, the scale of China's offshore duty-free market is expected to increase to RMB 1038 billion in 2023, with a compound annual growth rate of 66.6% from 2019 to 2023. The sales revenue of China's offshore duty-free stores is expected to continue growing rapidly and reach RMB 2432 billion by 2026, with a compound annual growth rate of 32.8% from 2023 to 2026.

Market scale of China's duty-free goods market (by channel)*

2017 to 2026 (estimated)

* Other duty-free stores include diplomatic personnel duty-free shops, transportation vehicle duty-free shops, and ship supply duty-free shops.

The sales revenue of the off-island duty-free stores does not include duty-free goods that non-off-island Hainan residents can purchase, nor does it include online orders placed by off-island travelers after leaving Hainan.

*** Duty-free shops at ports include those that allow online reservations and subsequent offline pickup upon leaving the Chinese mainland.

Source: Frost & Sullivan report

Market competition pattern of tax-free shopping in China

According to a Frost & Sullivan report, the Chinese duty-free market is highly concentrated with high entry barriers. In 2021, the top five duty-free travel retailers in China accounted for 98.5% of the retail market by sales revenue. According to the same source, COSCO ranked first among the top five duty-free travel retailers in China in 2021, with a market share of 86.0%. The following chart shows the market concentration and market share details of the top five duty-free travel retailers in China by sales revenue in 2021.

Top 5 Duty-Free Operators in China (by sales revenue), 2021

Source: Frost & Sullivan report

Frost & Sullivan has extensive research experience in the consumer retail industry and has assisted many well-known enterprises in successfully listing on capital markets. Successful listings include: Ming Chuang Youpin (9896.HK), Deying Holdings (2250.HK), Jiulongwang Food (1927.HK), Vesync (2148.HK), Blue Moon (6993.HK), Poplar Mart (9992.HK), Ming Chuang Youpin (NYSE:MNSO), Nongfu Spring (9633.HK), Fengxiang Food (9977.HK), China Feihai (6186.HK), Top Sports (6110.HK), China National Tobacco International (6055.HK), Youpin 360 (2360.HK), Wugu Mofang (1837.HK), Baby Tree (1761.HK), Benshi International (1705.HK), Golden Cat and Silver Cat (1815.HK), Miming Lifestyle Department Store (8473.HK), Nissin Foods (1475.HK), Debao Group (8436.HK), Seiko China (NASDAQ:SECO), Barbie Bebe (8297.HK), Asia Grocery (8413.HK), Chow Tai Fook (1458.HK), COFCO Foods (1610.HK), Dali Foods (3799.HK), Vientiane International (0288.HK), Chow Tai Fook (1929.HK), JMEI (NYSE:JMEI), and others.

Recommended Reading

07. Frost & Sullivan assists Midea Group in successfully going public in the US (NYSE:MNSO)

Frost & Sullivan helps Barbie Beige successfully go public in Hong Kong (8297.HK)