MINISO Group Holding Limited successfully went public on July 13, 2022, issuing 41.1 million shares at an issue price of HK$13.80 per share.

During the Hong Kong listing process, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, sponsor, and other professional intermediary institutions in completing the writing of relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important sections), facilitating communication between the issuer and the Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on industry-related issues from the Stock Exchange.

Overview of China's Home Furnishing Products Market

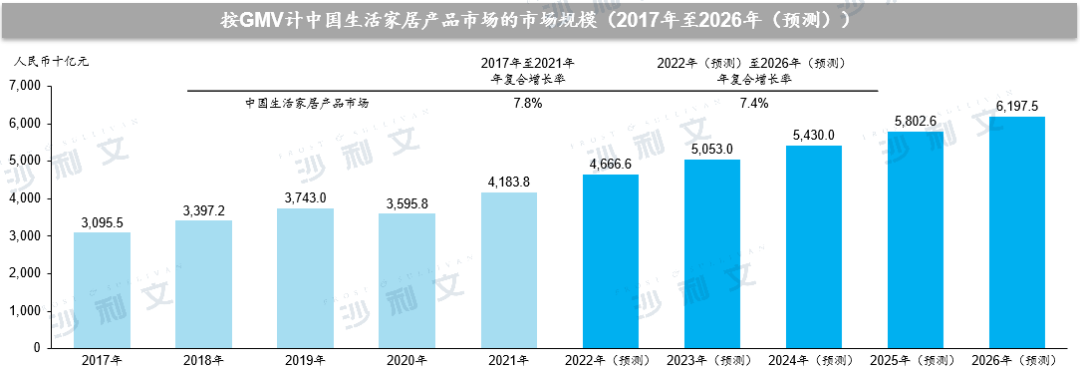

Living home products generally refer to various consumer household items, such as personal care products, bags and accessories, small electronic devices, digital accessories, stationery, snacks, daily necessities, textiles, and toys. In terms of GMV, the scale of China's living home product market increased from RMB 3.1 trillion in 2017 to RMB 4.2 trillion in 2021, with an annual compound growth rate of 7.8%, exceeding the annual compound growth rate of 4.8% for China's retail market during the same period and being one of the fastest-growing markets among all retail segments. The following chart shows the scale of China's living home product market by GMV over the listed years:

Source: Frost & Sullivan report

The home furnishings market can be divided into three sub-markets based on retailer type: (i) Own-brand comprehensive retail, generally referring to retailers distributing various home furnishings products, with over 50% of their total GMV coming from own-brand home furnishings; (ii) Exclusive retail, where retailers mainly focus on distributing a specific type of home furnishings product, with over 50% of their total GMV coming from that particular category; and (iii) Supermarket department store retail, generally referring to retailers who widely distribute a variety of home furnishings products available under various brands, with the total GMV from their own-brand home furnishings being less than 50%.

Overview of China's Own-brand Comprehensive Retail Market

Self-owned brand comprehensive retailers typically possess a rich assortment of lifestyle home products that are exquisitely designed, high-quality, and cost-effective. These retailers generally sell their products through various channels such as direct operation, franchising, and agency, or flexibly combine them. As an important part of China's lifestyle home product market, the self-owned brand comprehensive retail market in China has been developing rapidly. With Chinese consumers becoming more rational in their consumption behavior, affordable and high-quality lifestyle home products are becoming increasingly popular. In addition, Chinese consumers (especially younger generations) are increasingly favoring products that reflect their personal preferences. These trends have brought tremendous market opportunities and potential to self-owned brand comprehensive retailers.

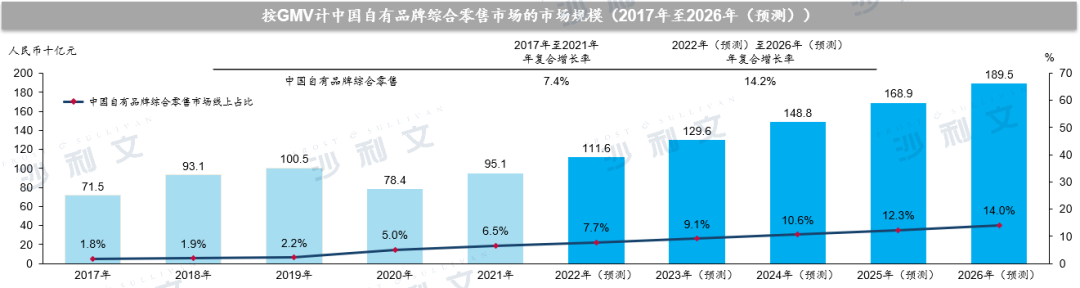

In terms of GMV, the scale of China's own-brand comprehensive retail market increased from RMB 715 billion in 2017 to RMB 951 billion in 2021, with an annual compound growth rate of 7.4%. It is expected to further increase at a compound annual growth rate of 14.2% from 2022 to 2026. The following chart shows the scale of China's own-brand comprehensive retail market by GMV for the listed years:

Source: Frost & Sullivan report

China's own brand comprehensive retail marketDriving factors and development trends

The Chinese owned brand comprehensive retail market has the following market drivers and development trends:

1) There is an increasing emphasis on differentiated experiences, product quality, design, cost-effectiveness, and personalization.With the continuous increase in disposable income and living standards, Chinese consumers have become more diverse in their demands and hold higher expectations for differentiated shopping experiences, as well as the quality, design, and cost-effectiveness of home products. Therefore, Chinese owned brand comprehensive retailers are keeping up with market trends and changing consumer preferences, and rapidly improving the shopping experiences and products they offer in all these aspects. Specifically, Chinese owned brand comprehensive retailers have adjusted and expanded their product portfolio to cater to the increasingly important personal tastes and preferences of Chinese consumers (especially the younger generation).

2) Penetration into lower-tier cities.Chinese owned brand comprehensive retailers have been accelerating their penetration into lower-tier cities to meet the growing consumer demand and reach markets with significant growth potential. To support market penetration and to enhance brand awareness in a cost-effective manner, these owned brand comprehensive retailers adopt various business models such as direct operation, franchising, and agency. Due to their generally accumulated brand awareness from existing operations, sufficient financial strength, supply chain and product procurement capabilities, as well as rich experience and technical knowledge, owned brand comprehensive retailers generally have an advantage over small stores and other local retailers and can compete successfully.

3) Empowering intelligent product development and efficient supply chains with technology.With continuous technological upgrades and widespread application, the owned brand comprehensive retail industry has accelerated its digital transformation process to develop products that can better meet consumer needs, achieve higher operational and supply chain efficiency, and reduce costs. Data analysis technology has helped owned brand comprehensive retailers accurately explore and grasp the ever-changing consumer tastes and needs, enabling retailers to offer consumers more customized products and shopping experiences.

In addition, the technical optimization of the supply chain can often integrate and simplify various links in the comprehensive retail value chain of own brands, such as demand analysis, product design, production, warehousing and logistics, sales management, and customer service. This greatly improves the efficiency of product development, the supply chain, and other business operations involved in this process.

4) Development and integration of online and offline channels.Despite the rapid growth of online channels and their increasing importance, consumers in China's own-brand comprehensive retail market still prefer offline stores. The reason is that offline stores can provide consumers with a personal shopping experience brought about by a comfortable shopping environment and considerate services. To further cater to these consumer preferences and make profits through online channels, in addition to using third-party e-commerce platforms, Chinese own-brand comprehensive retailers have continuously developed O2O business models and reached consumer groups through digital platforms. Under the O2O model, consumers can switch from online channels to offline channels without sacrificing the personalized experience and close interaction of offline stores while enjoying the convenience of online channels.

With the continuous development of technology, it is expected that online and offline channels will become more closely integrated in the future, providing consumers with a seamless and convenient shopping experience and driving consumer demand.

Global Comprehensive Retail Market for Own Brands

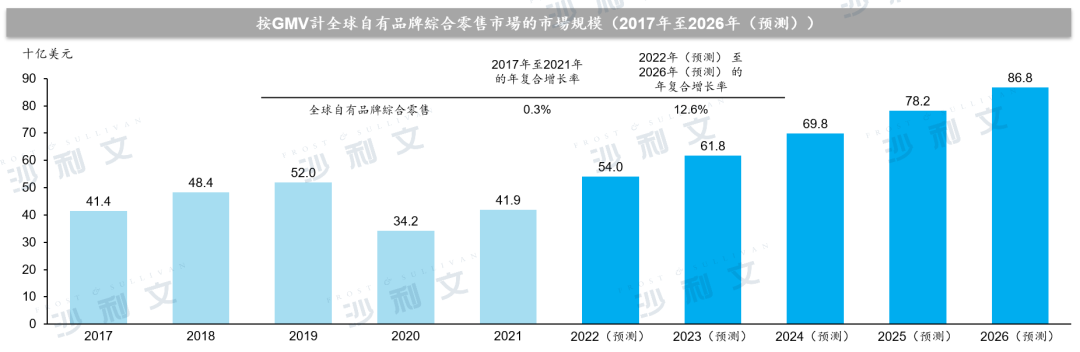

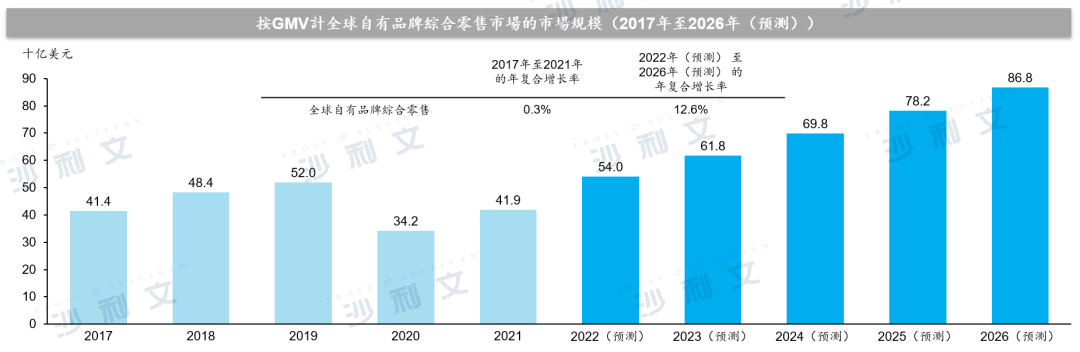

Over the past 20 years, the global owned brand omnichannel retail market has grown steadily. In terms of GMV, the scale of the global owned brand omnichannel retail market increased from $41.4 billion in 2017 to $41.9 billion in 2021, with an annual compound growth rate of 0.3%. It is expected to continue growing at an accelerated annual compound growth rate of 12.6% between 2022 and 2026. The following chart shows the scale of the global owned brand omnichannel retail market by GMV over the listed years:

Source: Frost & Sullivan report

Key macroeconomic factors such as GDP growth, population, and urbanization levels are driving the development of home furnishings markets in various regions. Consumers in developed countries generally have stable household incomes, a complete social welfare system, and relatively strong purchasing power, enabling them to pursue higher living standards. Therefore, consumers in developed countries have a stable demand for high-quality home furnishings products, and brands have become a key factor in consumer product selection. Consumer demand for customized product design, excellent shopping experiences, and reasonable prices has continuously driven the growth of the comprehensive retail market for own-brand products in developed countries. The comprehensive retail market for own-brand home furnishings products in developed countries is relatively mature and is expected to maintain stable growth.

On the other hand, the sustained growth of emerging economies has driven consumers' consumption of lifestyle products with fashionable designs, high cost performance, and high quality. Retail markets in emerging countries are gradually evolving from traditional retail models to modern retail models empowered by e-commerce. The upgrading of consumption structure, the integration of online and offline channels, and the improvement of shopping experiences will drive future growth in the comprehensive retail market of emerging country-owned brands.

China's trend toy market

Trend toys refer to toys that incorporate unique design and aesthetic elements of trendy culture, or licensed content featuring movie, animation, cartoon, or game characters. There are a wide variety of them, including blind boxes, art toys, collectibles, dolls, building blocks, and puzzle sets.

The trend toy market in China has developed rapidly over the past five years. In terms of GMV, the scale of the Chinese trend toy market increased from RMB 10.8 billion in 2017 to RMB 34.5 billion in 2021, with an annual compound growth rate of 33.7%. It is expected to grow at a compound annual growth rate of 24.0% from 2022 to 2026. The following chart shows the scale of the Chinese trend toy market by GMV and its product categories for the listed years:

Source: Frost & Sullivan report

Driving factors of the Chinese trend toy market

The Chinese trend toy market is driven by the following factors:

1) An active, diverse, and growing fan base.The main driving force behind the rapid growth of China's trend toy industry is its enthusiastic, active, and diverse fan base, mostly from the Generation Z (born in the mid-to-late 1990s to the early 2010s) and the Millennial generation (born in the early 1980s to the mid-1990s and into the early 2000s). This fan base continuously seeks ways to express their love for and interact with the trendy cultural content they are passionate about.

The continuous expansion of innovative products, categories, and trend cultural features helps to expand the fan base across different age groups and genders. Over time, due to continuous exposure and discussion about trend cultural content, many consumers who occasionally purchase trend toys have become frequent repeat buyers. To better meet fans' need to access more trend cultural content through trend toy products, industry participants in the trend toy sector have organized offline activities such as trend toy trade shows and exhibitions in recent years. With the increasing popularity, it is expected that more trend toy events and exhibitions will emerge in the future.

2) Diversified sales and customer interaction channels.Although face-to-face and interactive shopping experiences at offline stores are still indispensable, online channels, especially social networks-based platforms, have become a supplement to offline stores, creating convenient and unique shopping experiences for consumers, especially after the COVID-19 pandemic. Online channels such as O2O and e-commerce platforms help trend toy store operators showcase and promote their products to a wider consumer base, while also becoming additional sources of customer acquisition and revenue.

In addition, consumers are constantly seeking ways to express their enthusiasm for their favorite trendy cultural content and establish connections with it. Driven by technology, trend toy buyers can share the latest product information and industry news through the internet, more and more industry participants use social networking platforms to retain loyal customers and attract new ones, and obtain first-hand information about consumer preferences and needs from their own social platforms.

3) Diversified products.Although the blind box segment of China's trend toy market has occupied the largest market share since 2017 and has grown at the fastest rate compared to other segments, the market has also introduced various other trend toy categories to meet changing customer needs and is expected to grow rapidly in the future. Continuously creating more diverse trend toy product lines to satisfy any unmet or underserved consumer needs will continue to drive the development of China's trend toy market.

4) The importance of brand collaborations and IP incubation is increasing day by day.Driven by the booming market demand, trend toys are becoming increasingly popular in China. Leading brands have also started launching trend toys based on trend IPs to capture the growing market demand. As the importance of IPs continues to rise and procurement costs related to IP development or licensing increase, trend toy retailers with their own IP incubation capabilities are more likely to stand out in the fierce competition for trend toys based on their own IPs and maintain higher customer loyalty.

Competitive landscape analysis

According to a Frost & Sullivan report, the global owned brand comprehensive retail market is highly competitive and fragmented. In 2021, Myntra's global owned brand comprehensive retail business had a GMV of approximately RMB 18 billion (US$2.8 billion), accounting for 6.7% of the global owned brand comprehensive retail market share and ranking first in the market by GMV. Myntra's China-owned brand comprehensive retail business had a GMV of RMB 10.8 billion, accounting for 11.4% of the market share and ranking first in China by GMV.

According to a Frost & Sullivan report, the Chinese trend toy market is in a period of rapid industry development with a low concentration of market share. In 2021, Midea Group's GMV from its trend toy business in China was RMB 3.744 billion, ranking seventh in the Chinese trend toy market.

Frost & Sullivan has extensive research experience in the consumer goods industry and has assisted many well-known enterprises in successfully listing on capital markets. Successful listings include: Joyouwang Foods (1927.HK), Vesync (2148.HK), Blue Moon (6993.HK), Popcorn Mart (9992.HK), Mingchuang Youpin (NYSE:MNSO), Nongfu Spring (9633.HK), Fengxiang Foods (9977.HK), Simore (6969.HK), China Feihai (6186.HK), Taobop Sports (6110.HK), China National Tobacco International (6055.HK), Youpin 360 (2360.HK), Wugu Mofang (1837.HK), Baby Tree (1761.HK), Yongsheng Agriculture (8609.HK), Longhui Holdings (1007.HK), Xinrong International (1587.HK), Yiyuan Liquor (8146.HK), Jierong International (2119.HK), Bins International (1705.HK), Golden Cat and Silver Cat (1815.HK), HuaMi Technology (NYSE:HMI), Nippon Confectionery (1475.HK), Debao Group (8436.HK), Barbie Bebe (8297.HK), Asia Grocery (8413.HK), Chowking Duck (1458.HK), COFCO Meat (1610.HK), COFCO Dairy (1492.HK), Dali Foods (3799.HK), Manor Ranch (1533.HK), Vientiane International (0288.HK), CLEATIL (3709.HK), Urban Beauty (2298.HK), Cabine Clothing (2030.HK).

Recommended Reading

08. Frost & Sullivan assists SIMOR to successfully go public in Hong Kong (6969.HK)

14. Frost & Sullivan assists BaoBabu to successfully go public in Hong Kong (1761.HK)

Frost & Sullivan helps Golden Cat and Silver Cat successfully go public in Hong Kong (1815.HK)

22. Frost & Sullivan assists HuaMi Technology in successfully going public in the US (NYSE:HMI)