MingYang Smart Energy Group Co., Ltd. (hereinafter referred to as 'MingYang Smart') is expected to be officially listed on the London Stock Exchange at 13 July 2022, London time, with a final issue price of $21 per GDR. The company is issuing 3,366.05 million GDRs, representing 168,302,500 underlying A-share stocks, raising a total of $707 million.

During the process of listing on the London Stock Exchange, Frost & Sullivan mainly undertook the following tasks: helping the company accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the company's competitive advantages, assisting the company, investment banks, and other intermediaries in completing relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important sections), facilitating communication between the company and the London Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the company in completing feedback on various industry-related issues from the London Stock Exchange.

Overview of the Global Electricity Market

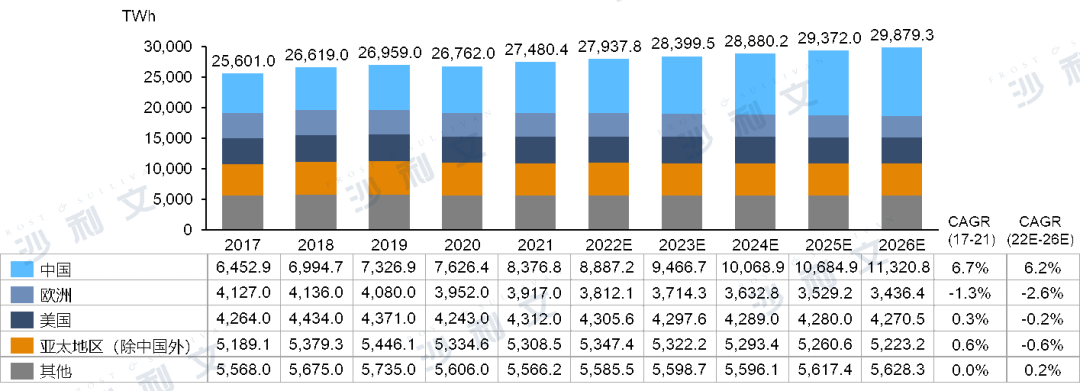

China is the world's largest and fastest-growing electricity market. In 2021, China's total power generation was 8,376.8 TWh, accounting for 30.5% of the global total. China's power generation also increased from 6,452.9 TWh in 2017 to 8,376.8 TWh in 2021, with a compound annual growth rate of 6.7%. It is expected to increase from 8,887.2 TWh in 2022 to 11,320.8 TWh in 2026, with a compound annual growth rate of 6.2%.

Electricity generation (by region), global, 2017 - 2026E

Source: Frost & Sullivan report

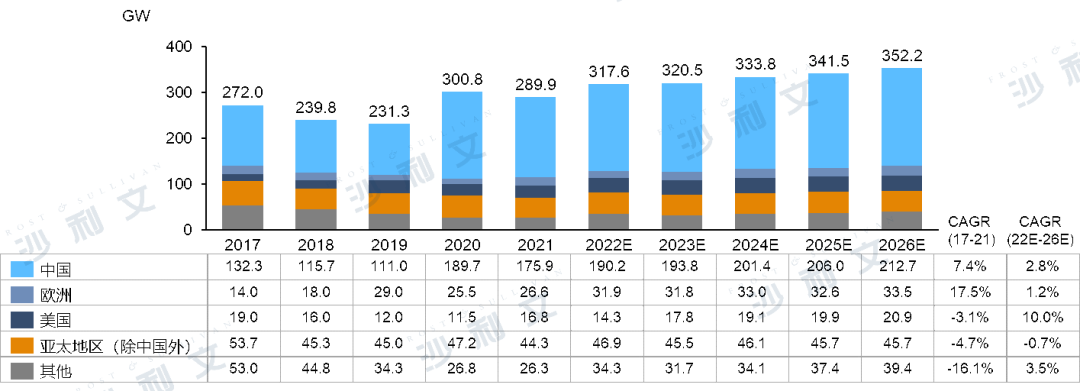

Countries have set goals and commitments to reduce carbon emissions and accelerate the development of renewable energy power. For example, China has promised to achieve carbon neutrality by 2060. The European Union has set development targets, aiming for renewable energy to account for 40% of final energy use by 2030. The British government has set a target that by 2035, electricity generation in the UK will no longer use fossil fuels and will be 100% sourced from renewable energy. Due to favorable policies introduced by governments around the world, the share of renewable energy, mainly including wind, photovoltaic, and hydropower, in the entire energy market, has increased from 63.2% in 2017 to 89.5% in 2021, and is expected to rise from 91.2% in 2022 to 97.4% in 2026, calculated based on new installed capacity.

New power installed capacity (by source), global, 2017 - 2026E

Source: Frost & Sullivan report

Overview of the China Fan Market

According to the 'Notice on Improving Wind Power Grid-connected Tariffs' issued by the National Development and Reform Commission (NDRC) in May 2019, starting from 2021, the Chinese government will no longer approve new onshore wind power projects. In 2020, China added a new installed capacity of 50.5 GW for onshore wind power, compared to 24.3 GW in 2019 and 18.5 GW in 2017. Onshore wind power projects in China have achieved parity grid connection. In the future, the new installed capacity for onshore wind power will maintain stable growth, increasing from 44.5 GW in 2022 to 47.2 GW in 2026. Although onshore wind power projects in China have entered parity grid connection, new installations are expected to maintain stable growth during the forecast period driven by the decline in wind power LCOE.

According to the 'Several Opinions of the National Development and Reform Commission on Promoting the Healthy Development of Non-Hydro Renewable Energy Power Generation' released in September 2020, starting from 2022, the government will no longer provide subsidies for grid-connected offshore wind projects. As China enters an era of parity pricing for offshore wind projects after the end of 2021, the newly installed capacity of offshore wind in China in 2021 was 15.5 GW, compared to 3.9 GW in 2020 and 1.2 GW in 2017. 2021 was the peak year for installation, and it is expected that the new installed capacity of offshore wind in China in 2022 will decrease slightly year-on-year. Governments in regions such as Guangdong and Zhejiang, as well as Shandong, have introduced supportive policies to promote offshore wind construction projects. For example, in June 2021, the Guangdong Provincial Government issued the 'Implementation Plan for Promoting the Orderly Development of Offshore Wind and the Sustainable Development of Related Industries', stating that it will continue to provide subsidies for newly installed offshore wind projects within Guangdong Province. Driven by favorable local government policies, the new installed capacity of offshore wind in China is expected to increase from 11.1 GW in 2022 to 14.2 GW in 2026, with a compound annual growth rate of 6.4% during this period.

New wind power installed capacity (onshore and offshore wind power)

China, 2017-2026E

Note: The installed wind power capacity is counted based on the hoisting diameter of the wind turbines.

Source: Frost & Sullivan report

Global and Chinese Offshore Wind Turbine Manufacturing Competition Overview

Based on the newly installed capacity of offshore wind turbines, MingYang Smart has remained in the top ten in the global market over the past five years, with its market share increasing from 0.6% in 2017 to 10.7% in 2021. The group is leading in the field of large-scale offshore wind power, offering advantages such as rapid product updates, low costs, and high power generation efficiency. The group has achieved mass production of several offshore wind turbine models, including MySE3.0MW, MySE4.0MW, and MySE6.0MW. In 2021, based on the newly installed capacity of offshore wind turbines, the group's market share was 10.7%, ranking third globally.

Top 5 global wind turbine manufacturers (new installed capacity of offshore wind turbines),2021

Source: Frost & Sullivan report

Based on the newly installed capacity of offshore wind turbines, MingYang Smart has remained in the top five in the Chinese market over the past five years, with its market share increasing from 2.6% in 2017 to 14.0% in 2021. In 2021, the group dominated the market for offshore wind turbines of 5.0MW and above, owning offshore wind turbine models such as MySE6.0. Calculated based on the newly installed capacity of offshore wind turbines of 5.0MW and above in 2021, the group is the largest turbine manufacturer.

Top 5 Wind Turbine Manufacturers in China (New Installed Capacity of Offshore Wind Turbines), 2021

Source: Frost & Sullivan report

Frost & Sullivan has extensive research experience in the power, renewable energy, and other energy sectors. It assists well-known enterprises in successfully accessing capital markets. Successful listings include: North China Energy (NASDAQ:CNEY), SDIC.LI, Naquan Energy Technology (1597.HK), Jiaxing Gas (9908.HK), TBK&Sons (1960.HK), Chuncheng Thermal Power (1853.HK), CNPC Clean Energy (1759.HK), Jiutai Bangda (2798.HK), TL Natural Gas (8536.HK), Tianbao Energy (1671.HK), Yuguang International (1621.HK), Jintai Feng (8479.HK), Zhongcheng Energy (2337.HK), Inner Mongolia Energy Engineering (1649.HK), Reskang (1679.HK), Persta Resources (3395.HK), Xinteng Energy (1799.HK), China Energy Engineering Corporation (3996.HK), Chao Wei Power Supply (0951.HK), Tianneng Battery (0819.HK), Huadian Fuxin New Energy (0816.HK).

Recommended Reading

18. Frost & Sullivan assists CEC in successfully listing on the Hong Kong Stock Exchange (3996.HK)