Intelligent Cloud Health Technology Group (hereinafter referred to as 'Intelligent Cloud Health') successfully went public on July 6, 2022, issuing 19 million shares at an issue price of HK$30.50 per share, raising up to HK$580 million at most.

During the Hong Kong listing process, Frost & Sullivan mainly undertook the following tasks: helping the company accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the company's competitive advantages, assisting the company, investment banks, and other intermediaries in completing relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important sections), facilitating communication with the Hong Kong Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the company in completing feedback on various industry-related issues from the Hong Kong Stock Exchange.

China's Digital Health and Wellness Market

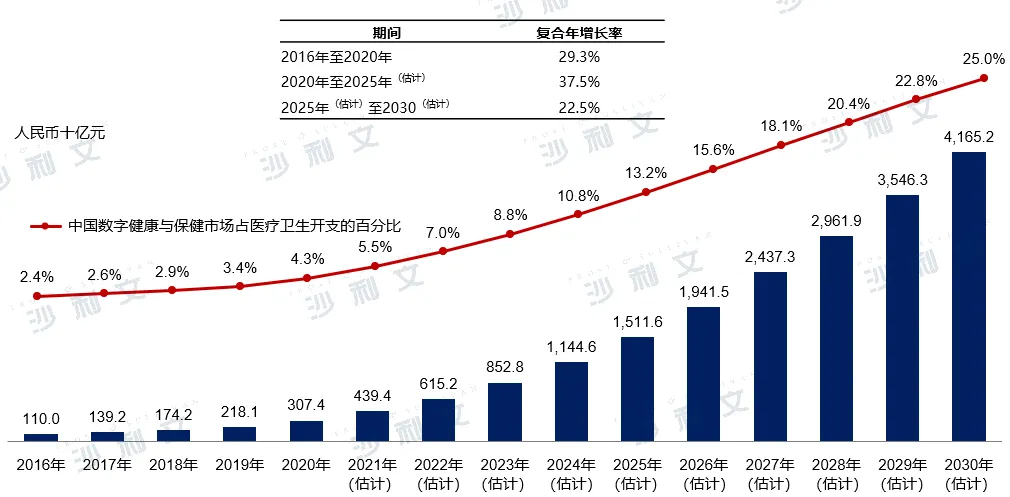

Driven by favorable policies and continuous technological progress, different sectors of the healthcare industry have shown an obvious acceleration in digitization, leading to rapid growth in China's digital health and wellness market. It is estimated that by 2025, the scale of China's entire digital health and wellness market will reach 1.5116 trillion yuan, with a compound annual growth rate of 37.5% from 2020 to 2025, and further reaching 4.1652 trillion yuan by 2030, with a compound annual growth rate of 22.5% from 2025 to 2030.

China's digital health and wellness market size, 2016-2030E

Data source: Analysis by Frost & Sullivan

China chronic disease management market

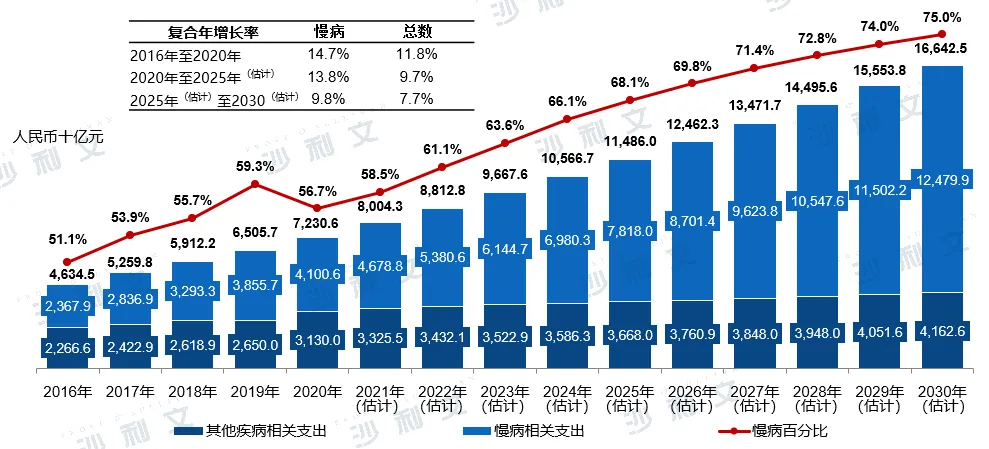

China's chronic disease management market has a huge patient base and high growth potential, making it one of the most important sub-markets in China's healthcare market. China's chronic disease healthcare expenditure is expected to grow from RMB 410 billion (accounting for 56.7% of total healthcare expenditure) in 2020 to RMB 1247.99 billion (accounting for 75.0% of total healthcare expenditure) by 2030.

China's healthcare expenditure is broken down by chronic and other disease-related expenditures

2016-2030E

Data source: Analysis by Frost & Sullivan

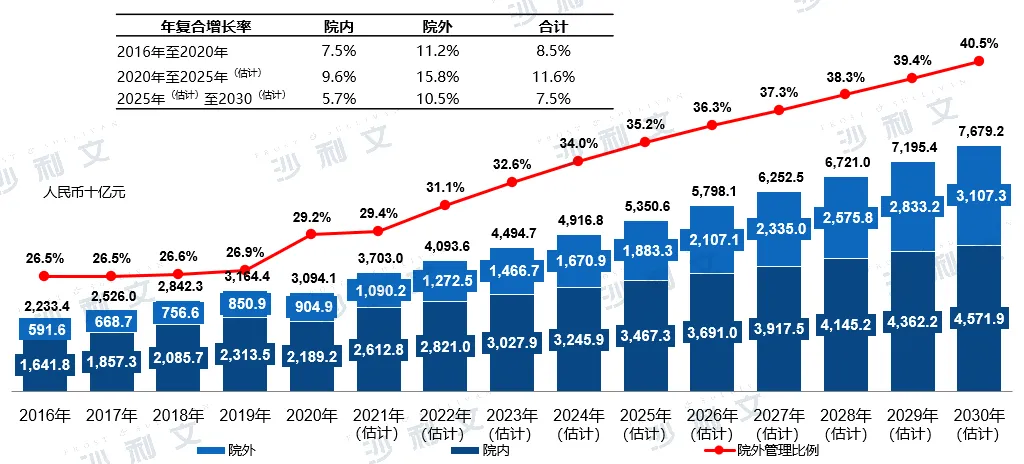

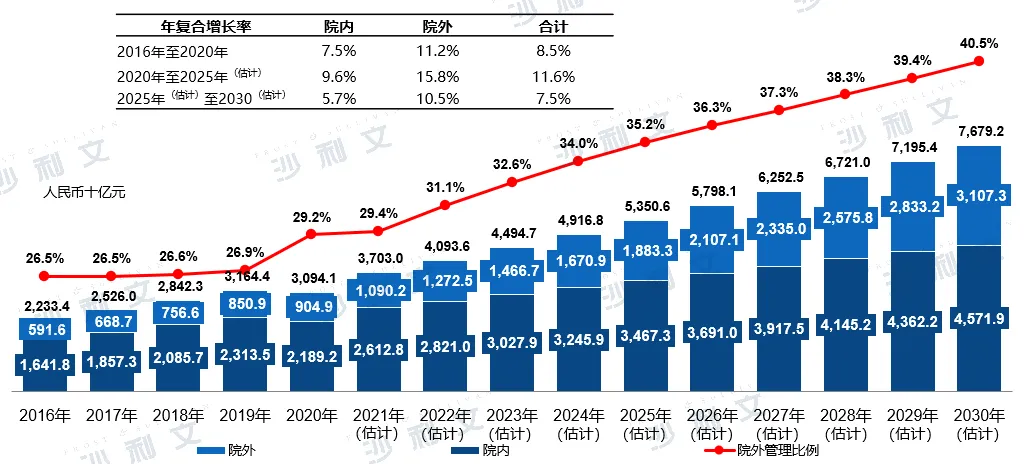

The outflow of prescription drugs is an important emerging trend in chronic disease management. Driven by this long-term trend, supported by the digitization of offline pharmacies and the emergence of internet hospitals, the out-of-hospital market for chronic disease management is expected to continue growing faster than the overall market. The market scale of China's out-of-hospital chronic disease management market (including the sale of medical devices, consumables, drugs, and provision of management services) will increase from RMB 904.9 billion in 2020 to RMB 1883.3 billion in 2025, and is expected to reach RMB 3107.3 billion by 2030. The compound growth rate from 2020 to 2025 is expected to be 15.8%, and from 2025 to 2030 it will be 10.5%.

Segmentation of sales channels in China's chronic disease management market, 2016 - 2030E

Data source: Analysis by Frost & Sullivan

The chronic disease management market can be further subdivided into management services and product sales based on service type. Chronic disease management services refer to the services provided by professional medical staff, including chronic disease consultation, regular check-ups, risk assessment, comprehensive intervention, and management. Chronic disease supplies include medicinal items, medical devices, and other supplies related to chronic disease management. In terms of management services and supplies, this segment is expected to continue growing at a considerable rate from 2020 to 2025, with annual compound growth rates of 13.3% and 10.7%, respectively.

China's chronic disease management market is segmented by the type of services provided

2016 - 2030E

Data source: Analysis by Frost & Sullivan

China's digital chronic disease management market

Pain points in chronic disease management

Currently, the entire sub-market for chronic disease management is still in its early stages of digitization. Chronic disease management in China is centered around in-hospital medical and health services. Typically, chronic disease management programs include in-hospital diagnosis, treatment, rehabilitation care, and patient follow-up. After patients receive diagnosis, treatment, and prescriptions at the hospital, their health data is recorded in medical records for subsequent evaluation and monitoring of health status. Once patients leave the hospital, they can only manage their own diseases through weekly or biweekly in-hospital follow-ups or medication dispensing. Due to the lack of automated electronic medical record generation and updating, in-hospital and out-of-hospital condition tracking, and systematic patient data analysis, chronic disease management is very inefficient.

In addition, China does not have a national patient database to support digital chronic disease management. In most hospitals, individual patient data is mainly collected and maintained manually, which leaves significant opportunities for digital solutions to improve the efficiency, accuracy, and effectiveness of chronic disease management. At the same time, there is a lack of one-stop solutions in China to monitor patients' conditions and manage their chronic diseases outside the hospital, which is crucial for treatment outcomes.

Value of digital chronic disease management

Given the need for long-term care, regular diagnosis and treatment, the demand for systematic medical data recording, and relatively low medical risks, chronic disease management is most suitable for using digital solutions among all health conditions. Patients with chronic diseases usually require regular follow-ups and continuous prescription renewals and treatments over a long period. As a result, patient-doctor interactions are more frequent, and patients' medical records need to be updated and reviewed regularly. Specifically, patients not only demand efficient diagnosis and in-hospital medical services but also continuous out-of-hospital management. In addition, the risk of misdiagnosis in chronic diseases is relatively controllable, and the potential negative consequences of medical negligence are relatively limited. Therefore, digital chronic disease management solutions possess core value characteristics such as the ability to achieve regular diagnosis and treatment, systematically record and store medical data, solve problems of limited and uneven distribution of medical resources, and make it easier to purchase prescription drugs.

Digital chronic disease management market size

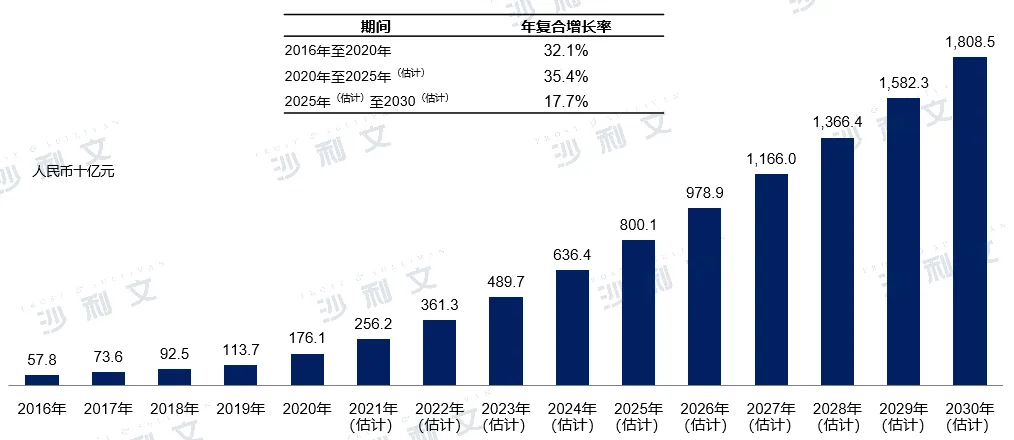

The digital chronic disease management market in China includes sales revenue from chronic disease management services and related products. Digital chronic disease products include medications, consumables, medical devices, nutritional supplements, and other chronic disease supplies. The market scale of China's digital chronic disease management market increased from RMB 578 billion in 2016 to RMB 1761 billion in 2020, with a compound annual growth rate of 32.1% during this period. It is expected that the market scale will further grow from RMB 8001 billion in 2025 to RMB 18085 billion by 2030, with compound annual growth rates of 35.4% and 17.7% for the periods from 2020 to 2025 and from 2025 to 2030 respectively.

China's digital chronic disease management market size, 2016-2030E

Data source: Analysis by Frost & Sullivan

Frost & Sullivan, integrating 61 years of global consulting experience, has dedicated 24 years to serving the booming Chinese market. With a global perspective, they help clients accelerate their corporate growth, achieving benchmark positions in industry growth, innovation, and leadership. The healthcare industry is one of the core areas of focus for Frost & Sullivan. Over the past 20-plus years, the Frost & Sullivan team has provided financing financial advisory, IPO industry advisory, strategic consulting, management consulting, and other services to hundreds of outstanding domestic and international biopharmaceuticals, medical devices, healthcare services, and internet healthcare companies. Successful listings include: MeinGene (6667.HK), Prenetics (NASDAQ: PRE), YunKang Group (2325.HK), Ruike Biotech (2179.HK), LeP Bio (2157.HK), Clear Medical (1406.HK), Bairen (2185.HK), Yonghe Medical (2279.HK), Kailaiying (6821.HK), Beihai Kangcheng (1228.HK), Gusheng Tang (2273.HK), Yingtong Technology (2251.HK), Clover Biotech (2197.HK), Minimally Invasive Robotics (2252.HK), Harmony Cayman (2256.HK), Kunbo Medical (2216.HK), Xianruida (6669.HK), Kangsheng Global (9960.HK), Yimaitong (2192.HK), Tengsheng Bo Yao (2137.HK), CanSino (2162.HK), Chaopu Ophthalmology (2219.HK), Guichuang Tongqiao (2190.HK), Hua Huang Medicine (0013.HK), Koi Pharmaceutical (2171.HK), Zhaoke Ophthalmology (6622.HK), Nature Medicine (UPC.NASDAQ), Sain Life Sciences (6600.HK), Zhaoyan New Drugs (6127.HK), Novogene Health (6606.HK), Tianyan Pharmaceuticals (ADAG.NASDAQ), Beikang Medical (2170.HK), Jianbimiao Miao Miao (2161.HK), Minimally Invasive Heart Center (2160.HK), Rui Li Medical Beauty (2135.HK), Jiake Pharmaceutical (1167.HK), HepPharmaceuticals (2142.HK), JD Health (6618.HK), Deqi Pharmaceuticals (6996.HK), Rongchang Biotech (9995.HK), WuXi AppTec (2126.HK), SonoBIO (2096.HK), Yunding Newray (1952.HK), Jiahe Biotech (6998.HK), Zai Ding Pharmaceuticals (9688.HK), Ocular Oncology (1477.HK), Yongtai Biotech (6978.HK), Haipu Pharmaceutical (9989.HK), Kechuang Pharmaceutical (9939.HK), Peijia Medical (9996.HK), Kangfang Biotech (9926.HK), Nuo Cheng Jian Hua (9969.HK), Tianjing Biotech (IMAB.NASDAQ), Kanglong Chemical (3759.HK), China Antibody (3681.HK), Dongyao Pharmaceutical (1875.HK), Yasheng Medicine (6855.HK), Fuhong Hanlin (2696.HK), Hansoh Pharmaceutical (3692.HK), Mabtech (2181.HK), Fangda Holdings (1521.HK), Via Biotech (1873.HK), CStone Pharmaceuticals (2616.HK), Junshi Biosciences (1877.HK), WuXi AppTec (2359.HK), Xinda Biotech (1801.HK), Hualing Medicine (2552.HK), BeiGene (6160.HK), Gilead Sciences (1672.HK), WuXi AppTec (2269.HK), China Resources Pharmaceutical (3320.HK), Yakuten Scientific Research Pharmaceutical (2633.HK), Hua Huang China Medicine (HCM.NASDAQ), Biotech (1548.HK), BBI Life Sciences (1035.HK), etc. In terms of the number of filings, the Frost & Sullivan healthcare team maintains an absolute leading position in Hong Kong's healthcare IPO market, consistently ranking first in market share from 2018 to 2021.

Since the listing of the first batch of companies on the Sci-tech Innovation Board in July 2019, Frost & Sullivan reports have also been widely cited in the prospectuses of leading Sci-tech Innovation Board-listed companies in the industry. These include: Jicui Pharmaceutical (688046.SH), Haichuang Pharmaceutical (688302.SH), Rongchang Biotech (688331.SH), Rendu Biotech (688193.SH), Shouyao Holdings (688197.SH), Heyuan Biotech (688238.SH), Yaxin Security (688225.SH), Xidi Micro (688173.SH), Mawei Biotech (688062.SH), Yahong Medicine (688176.SH), BeiGene (688235.SH), Jiahe Meikang (688246.SH), Dizhe Medicine (688192.SH), Novogene (688105.SH), Chengda Biology (688739.SH), Geke Micro (688728.SH), Huaxi Biotech (688363.SH), Junshi Biotech (688180.SH), Zijing Pharmaceutical (688266.SH), Biotec (688177.SH), Shenzhou Cells (688520.SH), etc. They are considered one of the most powerful, professional, and influential industry research institutions in the sector. We hope to work with enterprises to understand industry trends, seize development opportunities, jointly promote innovation and upgrading of China's healthcare industry, and build a healthy future.

Recommended Reading

Frost & Sullivan helps Chaogu Eye Hospital successfully go public in Hong Kong (2219.HK)

44. Frost & Sullivan assists Zai Lab to successfully list on the Hong Kong Stock Exchange (9688.HK)

52. Frost & Sullivan assisted Tianjing Biology in successfully going public in the US (IMAB.NASDAQ)