KuaiDou Dajia has successfully gone public on June 24, 2022, with an issue volume of 31,200,000 shares and a starting price of HK$21.5 per share.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the company accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the company's competitive advantages, assisting the company, investment banks, and other intermediaries in completing the writing of relevant parts of the prospectus (such as the summary, industry overview, business, and other important chapters), facilitating communication with the Hong Kong Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the company in completing feedback on various industry-related issues from the Hong Kong Stock Exchange.

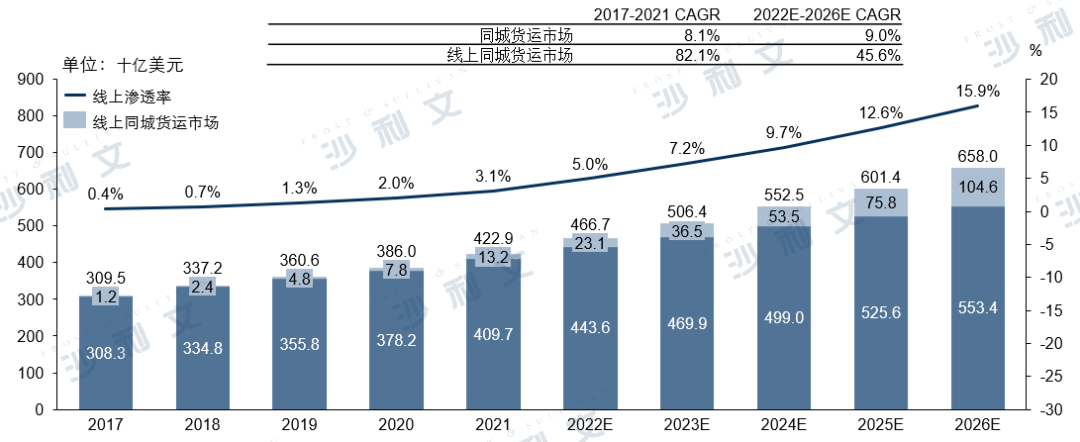

The online penetration rate of the Asian intra-city freight market is growing at a high speed

Intra-city freight refers to the transportation business of goods within a city. In the supply chain logistics structure, intra-city freight is subordinate to the transportation and distribution link. From a geographical perspective, intra-city freight occurs within the city boundaries. In terms of cargo types, the freight industry usually refers to goods weighing less than 30 kg per piece as express delivery, and those weighing 30 kg or more as freight. Intra-city freight is a specialized logistics and distribution service. It affects the delivery quality of the entire supply chain, directly participating in industrial production and distribution within the supply chain, and is an important aspect for shippers to evaluate the quality of logistics services.

The market size of intra-city freight in Asia was $309.5 billion in 2017. With urbanization and the popularization of mobile internet, the intra-city freight market will further develop. Due to the impact of COVID-19 in 2020, demand for intra-city freight will increase further. The market size of intra-city freight flows in Asia will reach $422.9 billion in 2021, with a compound annual growth rate of 8.1%.

The demand for intra-city freight in Asia will grow rapidly in 2021, with supporting services gradually maturing and their penetration rate into cities increasing accordingly. According to a Frost & Sullivan report, intra-city freight in Asia is expected to grow from $466.7 billion in 2022 to $658 billion by 2026, with a compound annual growth rate of 9.0% between 2022 and 2026. At the same time, due to the large number of Asian countries and significant differences in development status among different regions, the overall online intra-city freight market in Asia is still in its early stages of development, with the market rapidly expanding. In 2021, the online penetration rate for intra-city freight in Asia was 3.1%, and it is expected to reach 15.9% by 2026.

Asian intra-city freight market scale

2017 to 2026 (forecast)

Source: Frost & Sullivan report

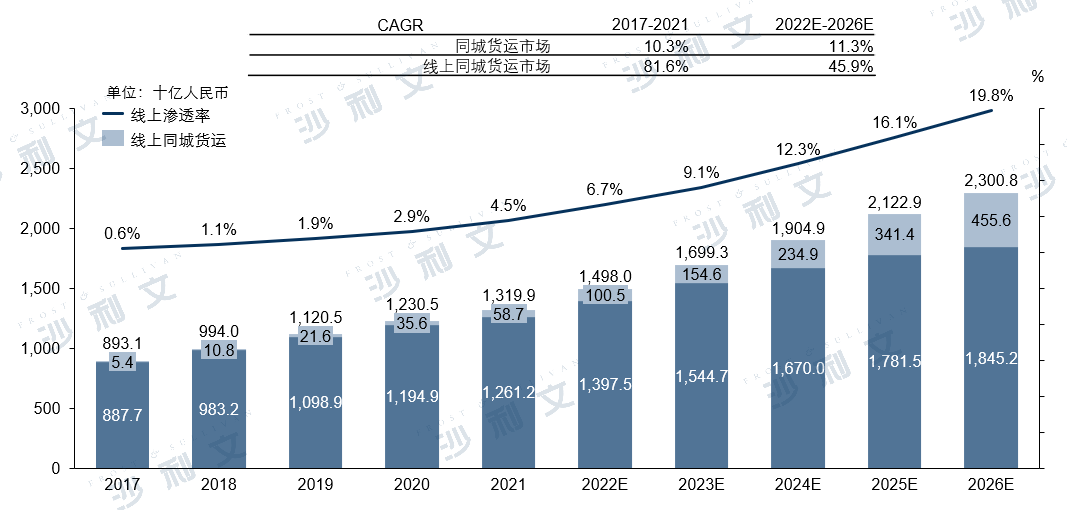

The development of intra-city freight in China is rapid

The scale of the intra-city freight market is closely related to GDP, and it is also affected by factors such as population density, mobile internet penetration rate, and e-commerce penetration rate. The higher the GDP, population density, mobile internet, and e-commerce penetration rates, the greater the demand for the intra-city freight market.

According to a Frost & Sullivan report, the Chinese intra-city freight market has developed rapidly in the past five years. The market size reached 1,319 billion RMB in 2021, with a compound annual growth rate of 10.3% from 2017 to 2021. In 2021, third- and fourth-tier cities accounted for about 64% of the Chinese mainland intra-city freight market. With the continuous growth of GDP and trade activities, as well as the development of e-commerce and new retail, there is still broad room for development in the Chinese intra-city freight market.

With the further development of the social economy and the increase in urbanization rates in China, commodity trading activities will become more active and frequent. Therefore, the demand for intra-city freight in China will continue to expand in the future. The market size is expected to maintain a steady growth trend. According to a Frost & Sullivan report, the intra-city freight market size in China is expected to reach 2,300.8 billion yuan by 2026, with a compound annual growth rate of 11.3% compared to 2022.

In 2017, online platforms for intra-city freight in China were in the early stages of development, with a penetration rate as low as 0.6%. With the development of online platforms and the popularization of mobile internet, the penetration rate of online platforms for intra-city freight in China reached 4.5% in 2021. Due to lifestyle changes caused by COVID-19 and further improvement in penetration rates, as mobile internet develops, online platform penetration will rise rapidly and is expected to reach 19.8% by 2026.

Market scale of intra-city freight transportation in Mainland China

2017 to 2026 (forecast)

Source: Frost & Sullivan report

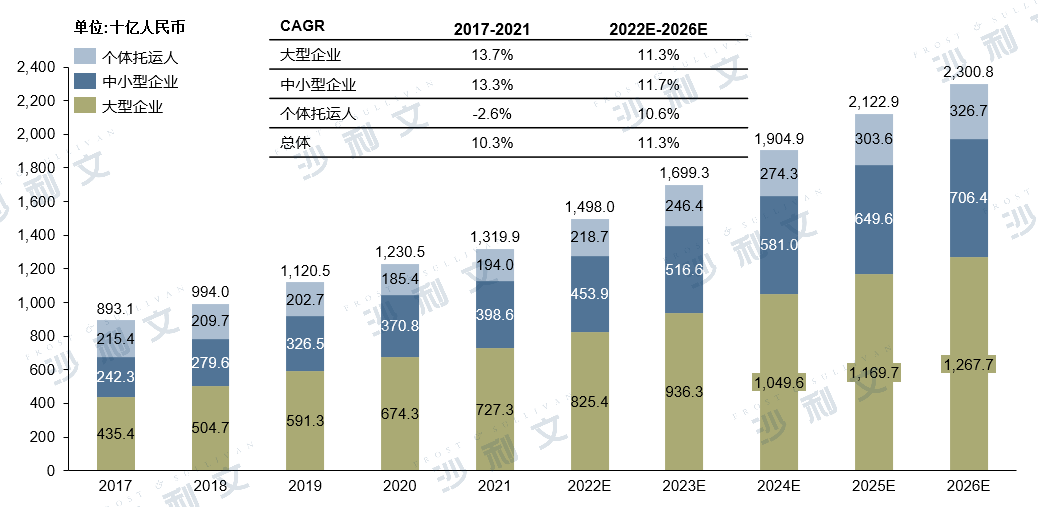

The demand for intra-city freight is mainly concentrated in large enterprises

The Chinese intra-city freight market can be divided into three categories based on the type of shippers: individual shippers, small and medium-sized enterprises, and large enterprises. Currently, most shippers in the industry come from the categories of enterprises, public services, or logistics service providers, accounting for a total market share of 85%. In 2021, the proportion of individual shippers accounted for about 15% of the Chinese intra-city freight market.

With the rapid development of the logistics industry and the increasing demand for service responsiveness from shippers, more and more enterprises are choosing to outsource services to large local freight platforms. According to a Frost & Sullivan report, from 2017 to 2021, the market size of local freight for large enterprises grew from 435.4 billion yuan to 727.3 billion yuan, with a compound annual growth rate of 13.7%. The market size for local freight is expected to continue expanding, especially in the segmented markets of large enterprises and logistics service providers. It is estimated that the market size of local freight for large enterprises will reach 1267.7 billion yuan by 2026, with a compound annual growth rate of 11.3% from 2022 to 2026.

Market scale of intra-city freight transportation in Mainland China (by customer type)

2017 to 2026 (forecast)

Source: Frost & Sullivan report

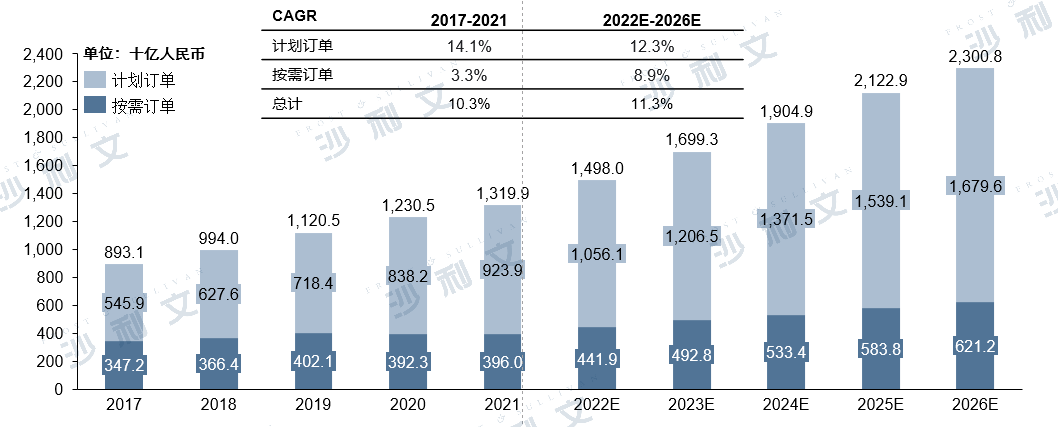

The demand for intra-city freight is mainly based on planned orders.

As a fundamental module of logistics, the majority of consignors for intra-city freight come from the segmented markets of retail enterprises. The digitization of the intra-city freight industry has also evolved with the development of e-commerce, enabling it to cooperate with e-commerce platforms and provide services on demand. These entities often have regular needs and use pre-orders more frequently. From 2017 to 2021, the market size of the planned order segment grew from 545.9 million yuan to 923.9 billion yuan, with a compound annual growth rate of 14.1%. As analyzed earlier, the proportion of large enterprises will increase. Therefore, it is expected that the market size of planned orders will reach 1.6796 trillion yuan by 2026.

Among different types of shippers, small and medium-sized enterprise merchants and individual shippers tend to choose on-demand orders more often than large enterprises. From 2017 to 2021, the market size of on-demand orders grew from 347.2 billion yuan to 396 billion yuan, with a compound annual growth rate of 3.3%. It is expected that the market size will reach 621.2 billion yuan by 2026.

Market scale of intra-city freight transportation in Mainland China (by order type)

2017 to 2026 (forecast)

Source: Frost & Sullivan report

Pain points of the intra-city freight market

-

Driver's end

The diverse needs of enterprises and company shippers are difficult to meet. The diverse transportation demands of enterprise shippers pose challenges to local freight service providers. In China's local freight market, most cargo owners are small and medium-sized enterprises and large companies, which have significant differences among their shippers. This diversity in the demand for freight services increases the difficulty of local freight delivery. Such services require transportation and distribution according to customized needs, such as: i) Direct delivery, where construction materials, food and dairy products, chemicals, engineering products, etc., are delivered directly along customized routes and specific types of transport vehicles; ii) Remote drop-off delivery, such as e-commerce local delivery and grocery delivery. In addition, there are also on-demand local deliveries in the market, such as seasonal promotions and large events for e-commerce. To meet the significant differences in service needs and requirements among shippers, local freight service providers need to possess strong comprehensive service capabilities, be able to adopt effective plans and strategies, and promptly address the current pain points of shippers' diverse and customized demands for drivers.

Lack of effective capacity allocation capabilities. Service providers in the intra-city freight market find it difficult to utilize a complete logistics network and online platforms to provide scaled services. Currently, orders in China's intra-city freight market are relatively concentrated, while capacity resources mainly come from logistics companies, individual drivers, and driver teams, leading to poor resource integration. There is currently a lack of clear standards for intra-city freight services, which need to be distinguished from cross-city logistics services. At this stage, service providers find it difficult to utilize a complete logistics network and optimized digital platforms to achieve the scale advantages of intra-city freight. This not only restricts the individual development of service providers in establishing a complete intra-city freight network but also hinders other enterprises from collaborating and utilizing their existing logistics resources and capabilities. It also poses problems for drivers, as their capacity is difficult to reach optimal levels.

-

Shipper

Orders are difficult to respond to in a timely manner. Currently, the number of service providers offering various types of intra-city freight services on the market is limited, resulting in a low proportion that meets market demand, making it challenging to improve service provider satisfaction. The freight transportation needs from small and medium-sized enterprises as well as large enterprises account for a relatively high proportion in the intra-city freight market, with typically larger volumes and certain customization requirements. However, the current market's capacity resources are usually fragmented, and large orders often struggle to receive a response in a short time, making it difficult to improve customer satisfaction. To address the pain points faced by shippers, platform service providers need to fully utilize drivers' capabilities, reasonably allocate driver resources, and provide order response speeds.

Local freight lacks standardized transaction processes. Due to significant differences among consignors, the services required for different types of cargo transportation vary, leading to numerous customized needs such as vehicle requirements, transport capacity, ordering, pricing, etc. However, there are currently no clear industry standards regarding how transactions should be conducted, pricing terms, and ordering processes. The industry needs to specify standardized service processes to provide consignors with stable and high-quality services.

The quality of freight service varies greatly. Currently, there are limited drivers in the same-city freight market who can ensure a complete service delivery process and high-level service quality assurance, leading to uneven service quality among market participants. Some drivers and vehicles find it difficult to fully meet the needs of shippers due to various factors. The current same-city freight market requires standardized service processes, and there is still room for improvement in terms of service.

Main drivers of growth in the intra-city freight market

-

Sustainable development of the national economy

Over the past five years, the Chinese economy has experienced a period of sustained and stable development. Multiple sectors, including national infrastructure, trade, and manufacturing, have developed rapidly, while also promoting the establishment and improvement of transportation infrastructure in urban areas. In recent years, China has strengthened the construction of urban roads and public transportation facilities, improving the quality of transportation infrastructure, cargo transport levels, and the volume of goods transported within cities. In addition, the production level of vehicles used for intra-city freight has also been improved, with further upgrades in vehicle quality and functionality. Therefore, with the increase in the number of freight vehicles, service demand, and transportation convenience, the intra-city freight market has grown rapidly.

-

New business models trigger demand for intra-city freight

In the past five years, with the emergence of new business models, the supply chain pattern in China's intra-city freight market has been reshaped, continuously bringing new growth vitality to the market. Retail giants such as Taobao and Meituan have been dedicated to developing new business models, aiming to change the way they provide intra-city freight services to customers. For example, community group buying, as a new business model, enables residents within a community to purchase groceries and other daily necessities at higher costs and with greater time efficiency. Since most groceries contain fresh food, related logistics services need to have higher delivery efficiency and responsiveness, which has raised the requirements for freight services to a higher level. Intra-city freight is one of the infrastructure components of these new business models. The outbreak of new business models has increased the customization level on the demand side, while end-to-end distribution seeks greater transportation functions and capacity within urban boundaries. The transactions brought about by these new platforms have promoted the continuous growth of intra-city freight demand.

-

The improvement of urbanization level in China has led to an increase in market demand

The acceleration of urbanization and the comprehensive improvement of residents' consumption levels have not only increased market demand for intra-city freight transportation. The development of urban infrastructure is a prerequisite and foundation for the continuous growth of cargo transportation and distribution needs. With the advancement of urbanization, urban infrastructure will become more complete, laying a solid foundation for the development of intra-city freight transportation. At the same time, from 2016 to 2020, China's urban population gradually increased, and urbanization experienced steady growth. The increase in the urbanization rate has promoted the expansion of the coverage of urban logistics networks, the growth of the number of carriers in urban areas, and the potential increase in the number of drivers and service delivery capabilities. In addition, the improvement of residents' consumption levels is providing a solid economic foundation for urban families' commodity consumption, and the growth of per capita disposable income will directly drive an increase in intra-city freight transportation demand.

Frost & Sullivan has extensive research experience in the automotive and transportation industry, assisting well-known enterprises in successfully accessing capital markets. Successful listings include NIO Automotive (NIO.SGX), NIO Automotive (9866.HK), Canggang Railway (2169.HK), YGMZ.NASDAQ, Asia Express (8620.HK), InfinityL&T (1442.HK), TOMOHOLDINGS (6928.HK), EH.NASDAQ, Aodima (8418.HK), Xiangxing International (8157.HK), CIMC Vehicles (1839.HK), Xunlong (1930.HK), CSSC Leasing (3877.HK), Chengdu Expressway (1785.HK), Tianrui Auto Interior (6162.HK), Baren Holdings (2885.HK), Huazi International (2258.HK), Pulin Chengshan (1809.HK), NIO Automotive (NIO.NYSE), Wanlida (8482.HK), Qilu Expressway (1576.HK), Yingheng Technology (1760.HK), Asia Industry (1737.HK), Ruifeng Power (2025.HK), Gaomeng Technology (8065.HK), Hebei Yichen (1596.HK), Zhengli Holdings (8283.HK), Junao Holdings (8035.HK), Yadi Group (1585.HK), Yihai Car Rental (EHIC.NYSE), Xinchen Power (1148.HK), Zhengxing Wheels (ZX.NYSE), Shuanghua Holdings (1241.HK), Changfeng Axles (1039.HK).

Recommended Reading

01. Frost & Sullivan assisted NIO in successfully going public in Singapore (SGX:NIO)

04. Frost & Sullivan Assists YGMZ.NASDAQ's Successful Listing in the US

08. Frost & Sullivan assists iFlytek in successfully going public in the US (EH.NASDAQ)

19. Frost & Sullivan assisted NIO Automotive in successfully going public in the US (NIO.NYSE)