Ningbo Tianyi Medical Devices Co., Ltd. (hereinafter referred to as 'Tianyi Medical') was successfully listed on April 7, 2022. The number of shares issued in this public offering was 14.736842 million shares, with an issue price of 52.37 yuan per share.

The company is a high-tech enterprise mainly engaged in the research, development, production and sales of medical polymer consumables and other medical devices in the fields of blood purification and ward nursing. It is one of the earliest enterprises in China to focus on this area. Its main products include extracorporeal circulation blood lines for blood purification devices, disposable arteriovenous puncture sets, disposable integrated oxygen inhalation tubes, feeders and feeding tubes, etc. Frost & Sullivan has long been paying attention to the global and Chinese biopharmaceutical industries, publishing a large number of research reports, which are widely cited in the prospectuses of leading ChiNext-listed companies in the industry, helping customers accelerate their growth.

Overview of Blood Purification Consumables

Blood purification refers to the process of removing certain pathogenic substances from a patient's blood by drawing it out of the body and passing it through a purification device using methods such as diffusion, convection, and adsorption. The basic treatment methods for blood purification include hemodialysis (HD), peritoneal dialysis (PD), hemofiltration (HF), hemodiafiltration (HDF), continuous renal replacement therapy (CRRT), single ultrafiltration, plasma exchange (PE), plasma adsorption, and hemoperfusion (HP), as well as the combined application of these various techniques. Among them, hemodialysis is currently the most commonly used and important method of blood purification and an effective treatment for acute and chronic renal failure, including end-stage renal disease (ESRD), and certain acute drug and toxin intoxications.

The process of hemodialysis involves the exchange of substances between blood and dialysate through contact with a semi-permeable membrane and concentration gradients. Metabolic waste and excess electrolytes in the blood move towards the dialysate, while calcium ions, bases, and other substances in the dialysate move into the blood. This process removes metabolic waste and toxins from the patient's blood, adjusts water and electrolyte balance, and regulates acid-base balance. The medical devices primarily used in hemodialysis treatment include hemodialysis machines, dialyzers, extracorporeal circulation circuits, puncture needles, dialysate, and hemodialysis powder. Among these, the extracorporeal circulation circuit, also known as the hemodialysis tubing, is an important part that connects the human body to the dialysis device. It serves as a safe channel for hemodialysis, ensuring the continuity and effectiveness of blood purification, and directly affecting the life and health of dialysis patients.

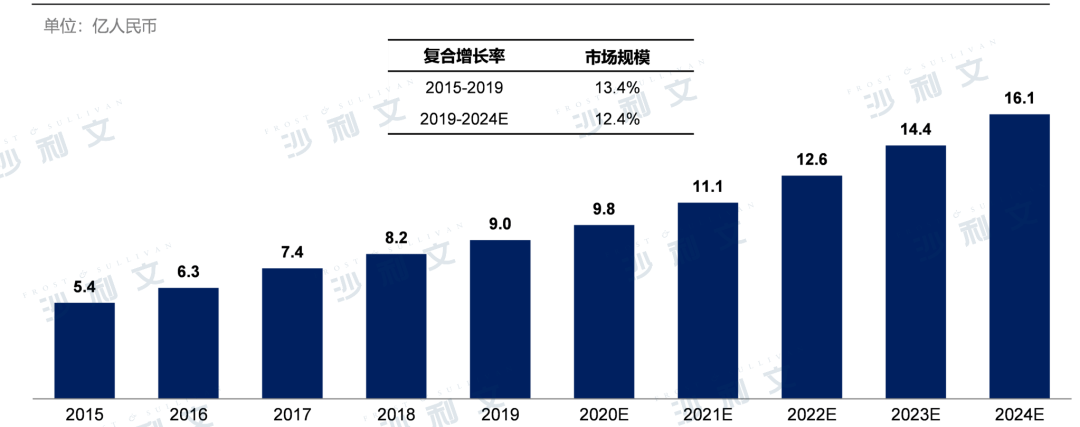

Market scale of extracorporeal circulation blood circuit

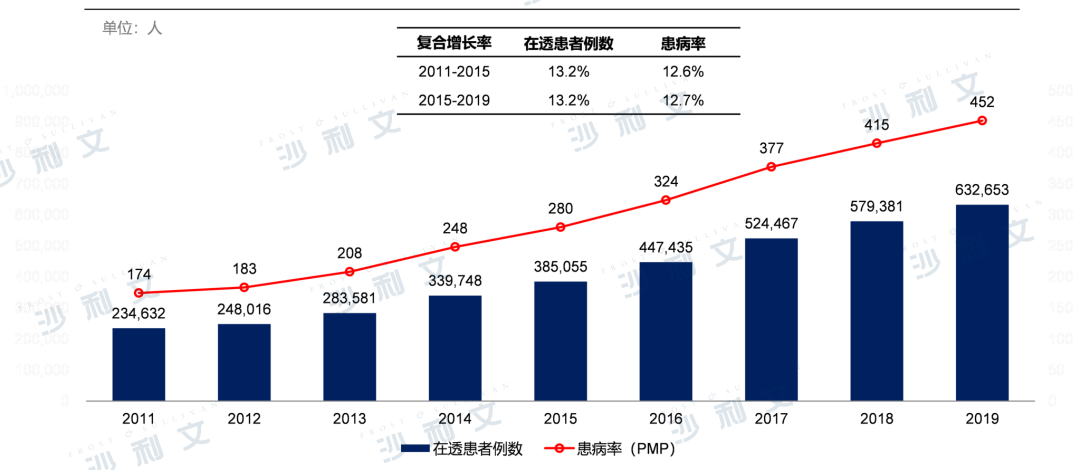

In China, factors such as population aging and changes in the disease spectrum have led to a continuous increase in the number of hemodialysis patients. According to data from the National Hemodialysis Case Information Registration System (CNRDS), the number of hemodialysis patients in China has rapidly increased from 385,000 in 2015 to 633,000 in 2019, with an average annual compound growth rate of 13.2%. The growing number of patients and the improvement in dialysis treatment rates provide broad space for industry growth. The market size of extracorporeal circulation blood circuits in China increased from 540 million yuan in 2015 to 900 million yuan in 2019, with an average annual compound growth rate of 13.4% during this period. It is estimated that by 2024, the Chinese extracorporeal circulation blood circuit market will reach 1.61 billion yuan, with an average annual compound growth rate of 12.4% during this period.

Market scale of extracorporeal circulation blood circuit in China2015-2024E

Source: Frost & Sullivan report

Currently, the construction of ICU wards in China is still at a relatively low level. The COVID-19 pandemic has highlighted issues such as insufficient ICU construction and weak treatment capabilities. With increased government financial subsidies in the future, the expansion of ICU wards is expected to lead to an increase in the use of CRRT consumables. The market size for CRRT dedicated extracorporeal circulation blood circuits is expected to grow rapidly.

Overview of Ward Nursing Consumables

There are a wide variety of consumables for ward care, mainly divided into infusion and nursing supplies, anesthesia and respiratory supplies, medical diagnostic and monitoring supplies, etc., according to their uses. Common products for infusion and nursing supplies include sterile syringes, puncture needles, feeding tubes, nasogastric tubes, etc.; common products for anesthesia and respiratory supplies include nebulizers, breathing tubes, oxygen inhalation tubes, breathing masks, etc.; common products for medical diagnostic and monitoring supplies include disposable tongue depressors, disposable electrocardiogram electrodes, etc. With the continuous growth of medical demand in China, the number of hospital admissions has been increasing year by year. According to data from the Chinese Health Statistics Yearbook, from 2015 to 2019, the number of hospitalizations in China increased from 210 million to 270 million, with an average annual compound growth rate of 6.0% during this period, correspondingly leading to rapid development in ward care consumables.

In anesthesia and respiratory consumables, oxygen tubes are mainly used for clinical oxygen therapy. Oxygen therapy refers to a treatment method that improves arterial blood oxygen partial pressure and saturation by supplying oxygen, increases arterial oxygen content, corrects hypoxia caused by various reasons, promotes tissue metabolism, and maintains the body's vital activities. It is also a commonly used treatment method in clinical practice. Oxygen administration methods are divided into invasive ventilation and non-invasive ventilation. Invasive ventilation is suitable for more severe dyspnea that requires tracheal intubation or tracheotomy; non-invasive ventilation has no wound surface and delivers oxygen to the patient's nasal cavity through an oxygen tube, oxygen mask, etc. An oxygen tube usually consists of an oxygen inlet interface, an oxygen hose, an adjustment ring, a nasal plug (or mask), etc. To avoid respiratory tract dryness caused by oxygen inhalation, an oxygen tube can be equipped with a humidifier bottle. A disposable oxygen tube with a humidifier bottle is called a sterile humidified oxygen device.

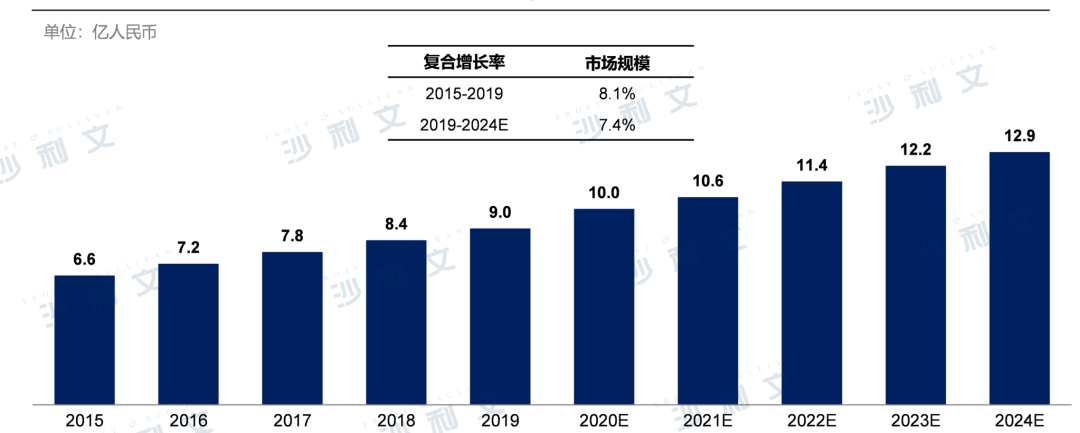

Market development of sterile humidified oxygen inhalation devices

Oxygen therapy is a commonly used clinical treatment method, and sterile humidified oxygen devices are routine medical consumables that are essential for healthcare institutions, with a large basic demand. In recent years, with the aging population and an increase in hospital admissions, the market size of sterile humidified oxygen devices in China has been steadily increasing. According to Frost & Sullivan data, the market size of sterile humidified oxygen devices in China increased from 660 million yuan in 2015 to 900 million yuan in 2019, with an average annual compound growth rate of 8.1% during this period. It is estimated that by 2024, the market for sterile humidified oxygen devices in China will reach 1.29 billion yuan, with an average annual compound growth rate of 7.4% during this period.

Market size of sterile humidified oxygen inhalation devices in China, 2015-2024E

Source: Frost & Sullivan report

China's blood purification and ward nursing industry

Development drivers

The aging population is intensifying, increasing medical demand

The national average life expectancy continues to rise, from 67.8 years in 1982 to 77.3 years in 2019. According to the National Bureau of Statistics, in 2019, the number of people aged 65 and above in China was 176 million, accounting for 12.6%, indicating an accelerated aging process. Looking at the trend of population structure changes in China from 2011 to 2019, the proportion of people aged 65 and above in China's total population has been increasing year by year, with the aging of China's population intensifying continuously. The incidence of hypertension and diabetes among elderly people in China is relatively high and continues to rise with the deepening of aging. With the intensification of China's population aging, the number of cases of kidney diseases and other diseases caused by these geriatric diseases, as well as the number of hospitalized patients, will show a continuous growth trend. This will continuously expand the demand for blood purification and ward care, thereby driving sustained market growth.

Per capita healthcare expenditure continues to grow, and the demand for medical devices is increasing

With the rapid development of China's economy and the improvement of residents' income levels, residents' emphasis on health has been continuously increasing. In 2019, China's total health expenditure reached 6.5 trillion yuan, a 10.3% increase from the previous year, far higher than the GDP growth rate during the same period. In 2019, the proportion of China's total health expenditure to GDP was 6.6%, and it has been steadily increasing in recent years. Against the backdrop of continuously rising national economic levels, per capita disposable income and people's awareness of health have been growing, thereby increasing per capita spending on healthcare across the country. From 2011 to 2019, China's per capita disposable income increased from 14,551 yuan to 30,733 yuan, with a compound growth rate of 9.8%; China's per capita health expenditure increased from 1,806.9 yuan to 4,656.7 yuan, with a compound growth rate of 12.6%. According to data from the National Bureau of Statistics, in 2019, China's per capita healthcare consumption expenditure was 1,902 yuan, an increase of 12.9%, accounting for 8.8% of per capita consumption expenditure. Per capita healthcare consumption expenditure has been continuously growing, with an average annual compound growth rate of 13.0% since 2015. The rapid increase in total health expenditure and per capita health expenditure has provided broad development space for China's medical consumables and other medical device industries.

The number of hemodialysis patients continues to increase, medical insurance policies are gradually implemented, and market capacity is expanding.

According to the data from the National Blood Purification Case Information Registration System (CNRDS), the number of hemodialysis patients in China has rapidly increased from 235,000 in 2011 to 633,000 in 2019, with an average annual compound growth rate of 13.2%. The number of hemodialysis patients in China is growing rapidly. According to the data from the China Kidney Data System, the most common cause of kidney disease in China is glomerular disease, accounting for 57.4%, followed by diabetic nephropathy (16.4%), hypertensive renal damage (10.5%), and cystic kidney disease (3.5%). The epidemiology of kidney disease in China is undergoing a transformation, and with the continuous rise in the prevalence of diabetes and hypertension, the prevalence of end-stage renal disease (ESRD) in China will continue to grow.

Number of dialysis patients nationwide, 2011-2019

Data source: National Blood Purification Case Information Registration System

Thanks to relevant national policies, the development of basic medical insurance for urban residents in China has entered a fast track in recent years. It has been continuously improved in terms of overall planning level, system construction, and benefit security, enhancing the ability of urban residents and employees to withstand disease risks and effectively reducing the medical burden. By the end of 2019, the number of insured persons under basic medical insurance in China exceeded 1.3 billion, with an insured coverage rate stable at over 95%. Among them, the number of employees participating in basic medical insurance was 329,260,000, an increase of 12.45 million or 3.9% compared with the end of last year; the number of urban and rural residents participating in basic medical insurance was 1.0251 billion, an increase of 127,740,000 or 14.2% compared with the end of last year.

The COVID-19 pandemic is expected to accelerate the construction of ICU wards, leading to a rapid increase in the market for related medical consumables.

China's intensive care unit (ICU) construction was very weak before the SARS outbreak. The SARS epidemic spurred rapid development in ICU care, and the state required that tertiary hospitals must be equipped with ICU departments. In 2006, the 'Guidelines for ICU Construction and Management in China' proposed that the number of ICU beds should generally be 2%-8% of the total number of beds serving that ICU or the hospital, with an additional increase as appropriate. After years of development, China's ICU department bed capacity reached 57,000 in 2019, but the bed ratio was only 0.65%, still some distance from the target of 2%-8% set in the guidelines. This COVID-19 prevention and control response has once again reflected insufficient ICU construction and weak treatment capabilities. Referring to the promotion of intensive care medicine by SARS, this COVID-19 pandemic is expected to lead to another increase in ICU bed numbers, thereby rapidly expanding the markets for CRRT and ward nursing medical consumables.

Frost & Sullivan, integrating 61 years of global consulting experience, has dedicated 24 years to serving the booming Chinese market with a global perspective, helping clients accelerate their corporate growth and achieve benchmark positions in industry growth, innovation, and leadership. The healthcare industry is one of the core areas of focus for Frost & Sullivan. Over the past seventeen years, the Frost & Sullivan healthcare team has provided financing financial advisory, IPO industry advisory, strategic consulting, management consulting, and other services to hundreds of outstanding domestic and international biopharmaceuticals, medical devices, healthcare services, and internet healthcare companies. Successful listings include: Ruike Biotech (2179.HK), Leopu Biotech (2157.HK), Clear Medical (1406.HK), Bexin'an (2185.HK), Yonghe Medical (2279.HK), Kailaiying (6821.HK), Beihai Kangcheng (1228.HK), Gushengtang (2273.HK), Yingpeng Technology (2251.HK), Clover Biotech (2197.HK), Minimally Invasive Robotics (2252.HK), Harmony Kamman (2256.HK), Kunbo Medical (2216.HK), Xianruida (6669.HK), Kangsheng Global (9960.HK), Yimaitong (2192.HK), Tengsheng Bopharm (2137.HK), Canopy (2162.HK), Chaoyu Ophthalmology (2219.HK), Guichuang Tongqiao (2190.HK), Hehuang Medicine (0013.HK), Koi Pharmaceutical (2171.HK), Zhaoke Ophthalmology (6622.HK), Nature Pharmaceuticals (UPC.NASDAQ), Sainfo Pharmaceuticals (6600.HK), Zhaoyan New Drugs (6127.HK), Novogene Health (6606.HK), Tianyan Pharmaceuticals (ADAG.NASDAQ), Beikang Medical (2170.HK), Jianbimiao Miao (2161.HK), Minimally Invasive Heart Center (2160.HK), Rui Li Medical Beauty (2135.HK), Jiake Pharmaceutical (1167.HK), HepB Pharma (2142.HK), JD Health (6618.HK), Deqi Pharma (6996.HK), Rongchang Biotech (9995.HK), WuXi AppTec (2126.HK), SinoBIO (2096.HK), Yunding Newray (1952.HK), Jiahe Biotech (6998.HK), Zai Ding Pharma (9688.HK), Ocular Biotechnology (1477.HK), Yongtai Biotech (6978.HK), Haipu Pharmaceutical (9989.HK), Kepang Pharmaceutical (9939.HK), Peijia Medical (9996.HK), Kangfang Biotech (9926.HK), Nuo Cheng Jian Hua (9969.HK), Tianjing Biotech (IMAB.NASDAQ), Kanglong Chemical (3759.HK), China Antibody (3681.HK), Dongyao Pharmaceutical (1875.HK), Yasheng Medicine (6855.HK), Fuhong Hanlin (2696.HK), Hansoh Pharmaceutical (3692.HK), Mabtech Pharma (2181.HK), Fangda Holdings (1521.HK), Via Biotech (1873.HK), CStone Pharma (2616.HK), Junshi Biotech (1877.HK), WuXi AppTec (2359.HK), Innovent Biologics (1801.HK), Hailun Medicine (2552.HK), BeiGene (6160.HK), Gilead Sciences (1672.HK), WuXi AppTec (2269.HK), China Resources Pharmaceutical (3320.HK), Jacobus Pharmaceutica (2633.HK), HCM China Medicine (HCM.NASDAQ), Kingsbridge Biotech (1548.HK), BBI Life Sciences (1035.HK), etc. In terms of the number of filings, the Frost & Sullivan healthcare team maintains an absolute leading position in Hong Kong's healthcare IPO market, consistently ranking first in market share from 2018 to 2021.

Since the listing of the first batch of companies on the Sci-tech Innovation Board in July 2019, Frost & Sullivan reports have been widely cited in the prospectuses of leading Sci-tech Innovation Board listed companies in the industry. These include Rongchang Biotech (688331.SH), Rendu Biotech (688193.SH), Shouyao Holdings (688197.SH), Heyuan Biotech (688238.SH), Yaxin Security (688225.SH), Xidi Micro (688173.SH), Mawei Biotech (688062.SH), Yahong Medicine (688176.SH), BeiGene (688235.SH), Jiahe Meikang (688246.SH), Dizhe Medicine (688192.SH), Novogene (688105.SH), Chengda Biotech (688739.SH), Geke Micro (688728.SH), Huaxi Biotech (688363.SH), Junshi Biosciences (688180.SH), Zhejiang Genomics & Therapeutics (688266.SH), BeiGene (688177.SH), Shenzhou Cells (688520.SH), etc., are considered the most powerful, professional, and influential industry research institutions in the sector. We hope to work with enterprises to understand industry trends, seize development opportunities, jointly promote innovation and upgrading of China's health industry, and build a healthy future.

Recommended Reading

Frost & Sullivan helps Zhaoyan New Drugs successfully list on the Hong Kong Stock Exchange (6127.HK)

41. Frost & Sullivan assists Zai Lab to successfully go public in Hong Kong (9688.HK)

49. Frost & Sullivan assisted Tianjing Biology in successfully going public in the US (IMAB.NASDAQ)