China Conch Environmental Protection Holdings Limited (abbreviated as "Conch Environmental Protection") successfully listed on the main board of the Hong Kong capital market on March 30, 2022, by way of an introduction. Frost & Sullivan provided exclusive industry advisory services for Conch Environmental Protection's listing in Hong Kong and hereby warmly congratulate it on its successful listing.

During this listing process in Hong Kong, Frost & Sullivan mainly undertook the following tasks: helping the company accurately and objectively understand its positioning in the target market, using objective market data to discover, support and highlight the company's competitive advantages, assisting the company, investment banks and other intermediaries in completing the writing of relevant parts of the prospectus (such as the summary, industry overview, business and other important chapters), helping the company complete communication with the Hong Kong Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the company in completing various feedbacks from the Hong Kong Stock Exchange on industry-related issues.

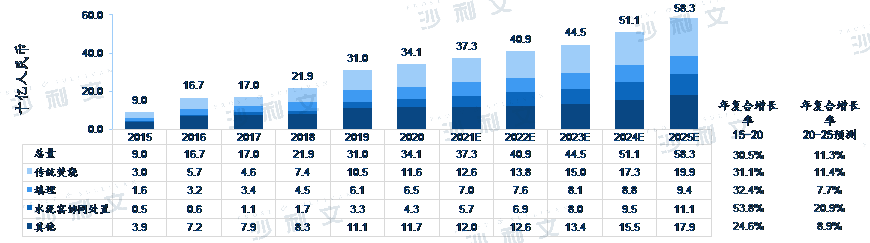

China's demand for solid waste disposal continues to grow

Solid waste refers to solid, semi-solid substances and gaseous substances loaded into containers originating from production and living activities. China's solid waste disposal industry can be divided into three major parts: (i) industrial solid waste disposal; (ii) hazardous waste disposal; and (iii) urban solid waste disposal. Specifically, industrial solid waste disposal refers to the disposal of solid waste generated by industrial production that is not classified as hazardous waste (including industrial polluted soil and contaminated soil). Hazardous waste disposal refers to the disposal of waste that causes significant harm to the environment and human health (for definitions see relevant national standards on identifying hazardous waste). Urban solid waste disposal refers to the disposal of solid waste generated by daily life activities and classified as urban solid waste according to relevant laws and regulations.

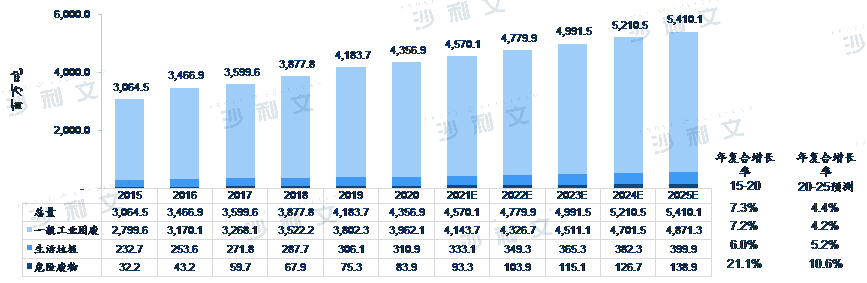

According to Frost & Sullivan, China's solid waste disposal volume increased from 306.45 million tons in 2015 to 435.69 million tons in 2020, with a compound annual growth rate of 7.3% from 2015 to 2020, and is expected to maintain stable growth from 2020 to 2025, with a compound annual growth rate of 4.4%. Calculated by disposal volume, the hazardous waste disposal segment accounts for about 1.9% of China's solid waste disposal market, and is expected to increase at a compound annual growth rate of 21.1% compared to other sectors from 2015 to 2020, and is expected to increase at a compound annual growth rate of 10.6% by 2025.

Solid waste disposal volume (China), forecast from 2015 to 2025

Source: Frost & Sullivan report

Industrial solid waste in China

accounts for the largest share in the overall solid waste disposal market

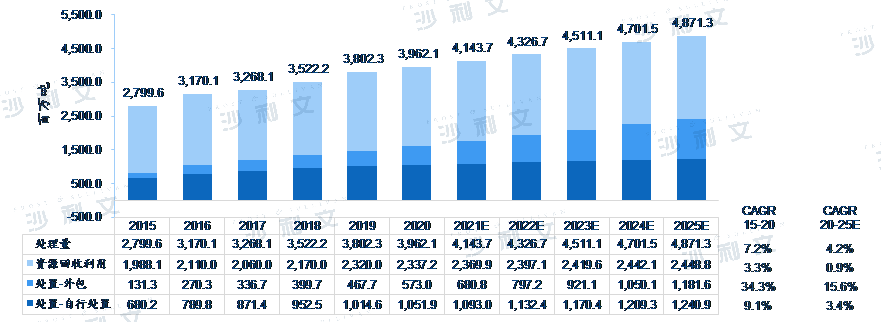

In China's solid waste disposal market calculated by disposal volume, the industrial solid waste segment accounts for the largest share. Industrial solid waste disposal is achieved through resource utilization or disposal. China's industrial solid waste disposal volume using disposal methods increased from 8.115 million tons in 2015 to 16.249 million tons in 2020, with a compound annual growth rate of 14.9%, and is expected to reach 24.225 million tons by 2025, with a compound annual growth rate of 8.3% from 2020 to 2025.

Industrial solid waste disposal volume by treatment method (China)

Forecast from 2015 to 2025

Source: Frost & Sullivan report

China's demand for hazardous waste continues to rise

According to the "National Hazardous Waste List" promulgated by the Ministry of Environmental Protection of China, the National Development and Reform Commission and the Ministry of Public Security in 2020, hazardous waste is defined as: (i) waste with one or more hazardous characteristics such as corrosiveness, toxicity, flammability, reactivity and infectivity; and (ii) waste that may cause harmful effects on the environment or human health. According to the "National Hazardous Waste List" promulgated in 2020, there are a total of 46 types of hazardous waste. Hazardous waste disposal requires relatively advanced technology to prevent the generation of secondary pollutants, resulting in disposal costs higher than those of industrial solid waste or urban solid waste.

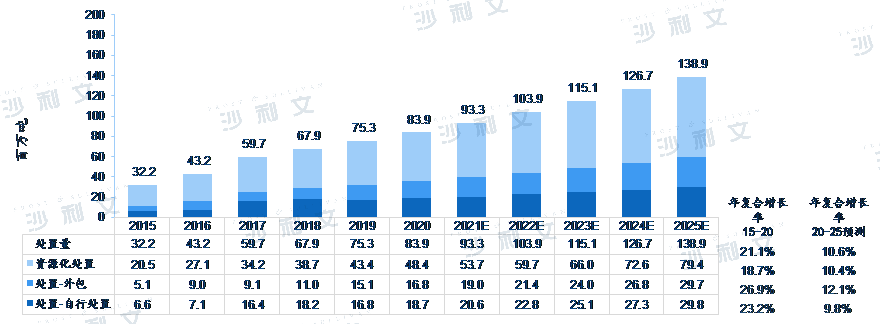

Hazardous waste disposal is achieved through resource utilization or disposal. China's hazardous waste disposal volume increased from 1.17 million tons in 2015 to 3.55 million tons in 2020, with a compound annual growth rate of 24.9%. It is expected to increase from 2020 to 2025 at a compound annual growth rate of 10.9%, reaching 5.95 million tons by 2025. The following figure lists the past and forecasted disposal volumes of China's hazardous waste disposal segment by disposal method from 2015 to 2025.

Details of hazardous waste disposal volume (China), forecast from 2015 to 2025

Source: Frost & Sullivan report

The future growth of hazardous waste co-disposal with cement kilns is relatively fast

According to the Frost & Sullivan report, compared with other disposal methods, the use of cement kilns for hazardous waste disposal increased more rapidly from 2020 to 2025, with a compound annual growth rate of about 21.3%.

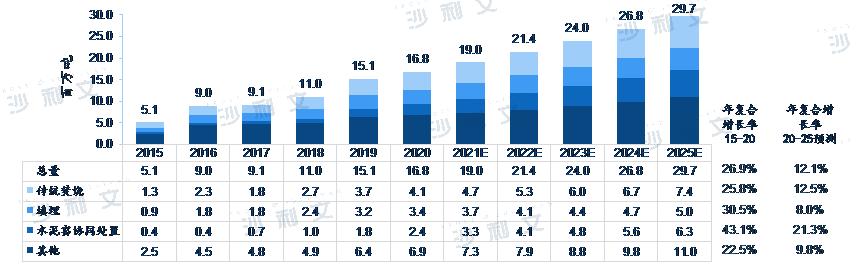

Details of hazardous waste outsourcing disposal volume by treatment method (China)

Forecast from 2015 to 2025

Source: Frost & Sullivan report

Although traditional incineration accounted for 34.0% of China's total hazardous waste outsourcing disposal revenue in 2020, the income generated from cement kiln co-disposal had the fastest growth among different disposal methods, increasing from RMB 500 million per year in 2015 to RMB 43 billion per year in 2020, with a compound annual growth rate of 53.8%. Its share of China's total non-outsourcing disposal revenue increased from 5.6% in 2015 to 12.6% in 2020, and is expected to increase to 19.0% or RMB 111 billion per year by 2025. The utilization rate of cement kilns for waste disposal was about 35% in 2020. The disposal fee for cement kiln hazardous waste was between RMB 1,500 yuan and RMB 2,500 yuan per ton in 2020.

Details of hazardous waste outsourcing disposal revenue by treatment method (China)

Forecast from 2015 to 2025

Source: Frost & Sullivan report

The competitive landscape of China's hazardous waste disposal and

co-disposal with cement kilns

According to the Frost & Sullivan report, China's hazardous waste disposal market using disposal methods is relatively fragmented. In 2020, the top five enterprises accounted for 15.9% of the market share by operating disposal capacity. In 2020, Conch Environmental Protection ranked first in this market by operating disposal capacity.

According to the Frost & Sullivan report, the top five enterprises in China's industrial solid waste and hazardous waste co-disposal with cement kilns market by total operating disposal capacity accounted for 56.7% of the market share. In 2020, Conch Environmental Protection ranked first in China's cement kiln co-disposal market by revenue, disposal volume and operating disposal capacity.

Frost & Sullivan has rich research experience in the environmental protection industry and has assisted well-known enterprises successfully list on the capital market. Successful listing cases include Hongcheng Environmental Protection (2265.HK), Dehe Group (0368.HK), Hygieia Group (1650.HK), Yongshun Holdings (6812.HK), Beikong Urban (3718.HK), Taizhou Water Affairs (1542.HK), Beng Soon (1987.HK), Zhuangchen Holdings (1955.HK), Jinmaoyuan Environmental Protection (6805.HK), Everbright Water Affairs (1857.HK), Weigang Environmental Protection (1845.HK), Shanghai Industrial Environment (0807.HK), Boqi Environmental Protection (2377.HK), Ligo Holdings (8472.HK), Everbright Green Environmental Protection (1257.HK), Wancheng Global (8309.HK), Dianchi Water Affairs (3768.HK), Xinglu Water Affairs (2281.HK), Canghai Holdings (2017.HK), Yongshun Group (8421.HK), Datang Environment (1272.HK), Peiran Environmental Protection (8320.HK), Jinjiang Environment (CJE.SP), Kangda International Environmental Protection (6136.HK), Haoze Water Purification (2014.HK).

Recommended reading

02. Frost & Sullivan helps Dehe Group successfully list in Hong Kong (0368.HK)

03. Frost & Sullivan helps Hygieia Group successfully list in Hong Kong (1650.HK)

05. Frost & Sullivan helps Beikong Urban successfully list in Hong Kong (3718.HK)

06. Frost & Sullivan helps Taizhou Water Affairs - H shares successfully list in Hong Kong (1542.HK)

07. Frost & Sullivan helps Beng Soon Machinery successfully list in Hong Kong (1987.HK)

08. Frost & Sullivan helps Hong Kong Zhuangchen successfully list in Hong Kong (1955.HK)

10. Frost & Sullivan helps Everbright Water Affairs successfully list in Hong Kong (1857.HK)

11. Frost & Sullivan helps Weigang Environmental Protection successfully list in Hong Kong (1845.HK)

12. Frost & Sullivan helps Shanghai Industrial Environment successfully list in Hong Kong (0807.HK)

13. Frost & Sullivan helps Boqi Environmental Protection successfully list in Hong Kong (2377.HK)

14. Frost & Sullivan helps Ligo Holdings successfully list in Hong Kong (8472.HK)

16. Frost & Sullivan helps Wancheng Global successfully list in Hong Kong (8309.HK)

17. Frost & Sullivan helps Dianchi Water Affairs successfully list in Hong Kong (3768.HK)

18. Frost & Sullivan helps Xinglu Water Affairs successfully list in Hong Kong (2281.HK)

19. Frost & Sullivan helps Canghai Holdings successfully list in Hong Kong (2017.HK)

20. Frost & Sullivan helps Yongshun Holdings successfully list in Hong Kong(8421.HK)

21. Frost & Sullivan helps Datang Environment successfully list in Hong Kong (1272.HK)

22. Frost & Sullivan helps Peiran Environmental Protection successfully list in Hong Kong (8320.HK)

23. Frost & Sullivan helps Jinjiang Environment successfully list in Singapore (CJE.SP)

25. Frost & Sullivan helps Haoze Water Purification successfully list in Hong Kong (2014.HK)