Frost & Sullivan

Yaojie Ankang (Nanjing) Technology Co., Ltd. (Stock Code: 2617.HK) successfully listed on the main board of the Hong Kong capital market on June 23, 2025. The company is a clinical-stage biopharmaceutical company oriented towards clinical needs, focusing on the discovery and development of innovative small molecule therapies for tumors, inflammation, and cardiac metabolism diseases. Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan') provides exclusive industry advisory services for the listing of Yaojie Ankang (Nanjing) Technology Co., Ltd., and hereby warmly congratulates them on their successful listing.

Yaojie Ankang (Nanjing) Technology Co., Ltd. (hereinafter referred to as 'Yaojie Ankang') successfully listed on June 23, 2025. The company plans to issue 1,528.1 million H shares, 90% of which will be international offerings and 10% will be public offerings. The maximum offering price per share is HK$13.15, and the net proceeds from fundraising are expected to be approximately HK$161.3 million.

During the process of listing in Hong Kong this time, Frost & Sullivan mainly undertook the following tasks: helping the issuer accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the issuer's competitive advantages, assisting the issuer, investment banks, and other intermediaries in completing the relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important chapters), helping the issuer complete communication with the Hong Kong Stock Exchange and investors, assisting investors in quickly understanding the market ecosystem and competitive landscape, and assisting the issuer in completing feedback on various industry-related issues from the Hong Kong Stock Exchange.

According to LiveReport's big data (statistical data as of June 1, 2025), from January to May 2025, as well as during the past 12 and 36 months, Frost & Sullivan provided listing industry advisory services for 17 (63%), 48 (63%) and 152 (68%) Hong Kong-listed IPOs respectively, boasting rich industry experience and communication skills with exchanges and investors.

PART/1

Investment Highlights

-

The company is a biopharmaceutical firm oriented towards clinical needs, currently in the registration clinical stage. It focuses on discovering and developing small molecule innovative therapies for tumors, inflammation, and cardiovascular metabolic diseases. With its comprehensive internal R&D system, the company has established a pipeline of six clinical-stage candidate products and one preclinical candidate product.

-

The company's core product, Tinengotinib, is the world's first and only investigational drug that has entered the registration clinical stage for the treatment of patients with recurrent or refractory cholangiocarcinoma who are FGFR inhibitors resistant to conventional treatment. It is also the world's first and only investigational drug that may simultaneously inhibit the FGFR/JAK pathway and has clinical efficacy evidence for metastatic castration-resistant prostate cancer.

-

Other indications for tinogotinib include hepatocellular carcinoma, breast cancer, cholangiocarcinoma, and pan-FLT3/FGFR solid tumors.

-

For tinogotinib, the company is currently conducting multi-regional Phase III clinical trials in the United States, South Korea, the United Kingdom, eight EU countries, and Taiwan, China. It is also conducting pivotal Phase II trials in Mainland China under accelerated approval regulations.

-

The company's pipeline product TT-00920 is currently the only PDE9 inhibitor in clinical development for the treatment of chronic heart failure. It acts directly on myocardial cells and represents a novel and promising treatment option for HFrEF and HFpEF.

-

The company's pipeline product TT-01025 is currently the only VAP-1 inhibitor in clinical trials in China, intended for oral treatment of NASH. The results of the completed Phase I clinical study in China show that the drug has good safety and tolerability at single doses of up to 300mg and multiple doses of up to 100mg.

-

The company has established strategic partnerships and collaborations with international cooperation and value creation. The company's experience and capabilities in drug discovery, research and development, and business development enable it to establish partnerships and collaborate with multinational corporations and leading domestic biopharmaceutical companies, including LG Chem, Roche, Eisai, and EA Pharma.

PART/2

Overview of the Market for Small Molecule Tumor Targeted Therapies

Small molecule drugs refer to any organic compound drug with a low molecular weight. As therapeutic drugs, small molecule drugs have certain advantages: most drugs can be administered orally and can penetrate cell membranes to reach intracellular targets. Small molecule drugs can also be designed to contact biological targets through various modes of action, allowing for further customization of their distribution, such as allowing for systemic exposure with or without the blood-brain barrier. In addition, small molecule drugs are structurally less complex, simplifying CMC (Chemical Manufacturing Control), manufacturing, transportation, and storage, resulting in relatively lower costs. Therefore, small molecule drugs remain the main drug mode for treating cancer.

In the past few decades, the field of cancer treatment has made rapid progress, evolving from surgery and radiotherapy to chemotherapy. More advanced treatment regimens, represented by targeted therapy and immunotherapy, have recently developed in order to improve patient outcomes while reducing systemic adverse reactions. The global market size for oncology drugs is expected to increase from $251.4 billion in 2024 to $436.8 billion in 2030. In China, driven by favorable policies, continuously improving patient affordability, and the introduction of innovative targeted drugs, the market size for oncology drugs is expected to grow from RMB 274.5 billion in 2024 to RMB 574.8 billion in 2030.

Compared with traditional treatment regimens, targeted therapy provides patients with better efficacy, alleviates symptoms, and/or improves quality of life by targeting specific oncogenic pathways. In addition to being used as a single therapy, small molecule targeted therapies have been approved or are currently undergoing clinical trials in combination with several other therapies, including chemotherapy, other targeted therapies, and immunotherapy. Combined targeted therapies and immunotherapy can produce synergistic effects, reverse the immunosuppressive tumor microenvironment, improve target exposure, thereby enhancing anti-tumor efficacy. Combinations have been proven to yield better results in clinical practice. For example, in a preclinical study, an MTK inhibitor combined with an anti-PD-1 antibody caused significant tumor shrinkage and improved survival rates in mice with lung tumors. Neither single-agent MTK inhibitor treatment nor anti-PD-1 antibody treatment alone achieved this effect.

Therefore, small molecule drugs are an important approach in cancer treatment. Globally, according to sales revenue in 2022, small molecule drugs occupy five positions among the top ten oncology drugs. Similarly, in China, based on sales revenue in 2022, small molecule drugs also occupy five positions among the top ten oncology drugs. To date, the FDA has approved 102 new small molecule targeted oncology drugs, while the National Medical Products Administration has approved 95 such drugs. From 2018 to 2023, one-third of the oncology drugs approved by the FDA and National Medical Products Administration were small molecule targeted drugs.

Main indication markets for MTK inhibitors

● Cholangiocarcinoma

Biliary tract cancer is a common type of liver and gallbladder cancer worldwide, usually including cholangiocarcinoma and gallbladder cancer. The bile duct is a branch that connects the liver and gallbladder with the small intestine, and cholangiocarcinoma is a disease where malignant cells form in the bile ducts. Common symptoms of cholangiocarcinoma include jaundice, fatigue, and abdominal pain, and its risk factors often involve the common role of chronic biliary inflammation in the development of cholangiocarcinoma. Approximately 25.2% of cholangiocarcinoma patients have FGFR mutations. Depending on the origin, cholangiocarcinoma can be divided into intrahepatic cholangiocarcinoma (iCCA) and extrahepatic cholangiocarcinoma (eCCA), with extrahepatic cholangiocarcinoma further divided into hilar cholangiocarcinoma and distal cholangiocarcinoma (pCCA and dCCA, respectively). iCCA can sometimes be misdiagnosed as hepatocellular carcinoma, especially when using contrast-enhanced ultrasound for diagnosis, with a high misdiagnosis rate. According to a research paper published in Cancer Treat Reviews in 2023, about 95% of cholangiocarcinoma patients may eventually develop acquired resistance after receiving FGFR inhibitor treatment.

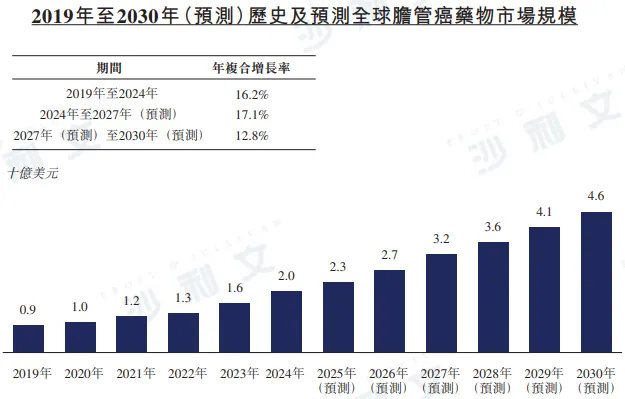

The global market size for cholangiocarcinoma drugs will reach $2 billion in 2024, with an annual compound growth rate of 16.2% from 2019 to 2024. It is expected to grow to $32 billion by 2027, with an annual compound growth rate of 17.1% from 2024 to 2027, and further increase to $46 billion by 2030, with an annual compound growth rate of 12.8% from 2027 to 2030. In 2024, the market size for cholangiocarcinoma drugs in China reached RMB 32 billion, with an annual compound growth rate of 16.4% from 2019 to 2024, and is expected to further grow to RMB 55 billion and RMB 76 billion by 2027 and 2030 respectively.

Source: Frost & Sullivan report

Overview of FGFR Inhibitor Market

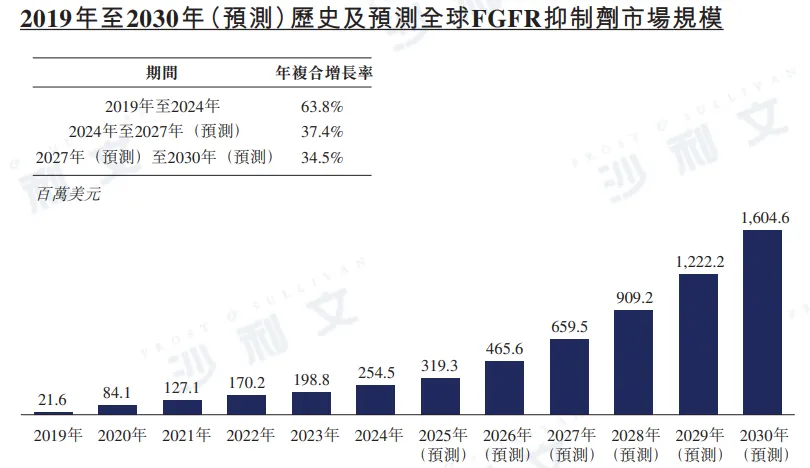

In 2024, the global FGFR inhibitor market value was $254.5 million, with an annual compound growth rate of 63.8% from 2019 to 2024. It is expected that this market size will grow to $659.5 million by 2027, with an annual compound growth rate of 37.4% from 2024 to 2027, and further to $16.046 billion by 2030, with an annual compound growth rate of 34.5% from 2027 to 2030. In China, the FGFR inhibitor market size reached RMB 815 million in 2024 and is expected to grow to RMB 455.6 million by 2027, with a compound annual growth rate as high as 77.5% from 2024 to 2027. Moreover, the market size is expected to soar further to RMB 20.024 billion by 2030, with an annual compound growth rate of 63.8%.

Source: Frost & Sullivan report

Overview of the AXL/FLT3 inhibitor market

In 2024, the global market size for AXL/FLT3 inhibitors reached $483.9 million, with a compound annual growth rate of 29.8% from 2019 to 2024. It is estimated that the market size will reach $823.7 million in 2027, $1396.5 million in 2030, with a compound annual growth rate of 19.4% from 2024 to 2027 and 19.2% from 2027 to 2030.

Source: Frost & Sullivan report

Overview of BTK Inhibitor Market

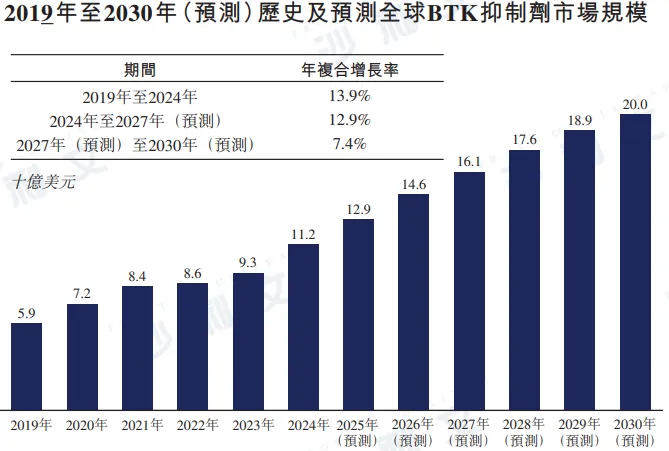

From 2019 to 2024, the global BTK inhibitor market size grew from $5.9 billion to $11.2 billion, with an annual compound growth rate of 13.9%. It is expected that this market size will reach $16.1 billion in 2027 and $20 billion in 2030, with a compound annual growth rate of 12.9% from 2024 to 2027 and 7.4% from 2027 to 2030.

Source: Frost & Sullivan report

PART/3

Competitive landscape of small molecule tumor targeted therapies in China

Competitive landscape of cholangiocarcinoma indications

As of now, three small molecule targeted therapies have been approved by the FDA for the treatment of cholangiocarcinoma: fulvestrant, pembrolizumab, and avastinib. Additionally, one small molecule targeted therapy has been approved by the National Medical Products Administration for the treatment of cholangiocarcinoma: pembrolizumab. Globally, there are 33 small molecule targeted therapies for cholangiocarcinoma in phase II or late clinical development, and in China, there are 12 such therapies in phase II or late clinical development.

Competitive landscape of MTK inhibitors

Data source: Center for Drug Evaluation, ClinicalTrials.gov, Frost & Sullivan analysis

Competitive landscape of FGFR inhibitors

As of now, the FDA has conditionally approved two FGFR inhibitors for the treatment of cholangiocarcinoma, namely fulvestrant and perifolitinib, as well as an FGFR-targeted MTK inhibitor for the treatment of urothelial carcinoma, namely erdafitinib. The National Medical Products Administration has conditionally approved perifolitinib for the treatment of cholangiocarcinoma. However, these approved drugs are unable to overcome FGFR resistance. In addition, an FGFR inhibitor under Helsinn Healthcare SA, enfolitinib, has also been approved by the FDA for the treatment of cholangiocarcinoma. However, Helsinn Healthcare SA voluntarily requested to revoke its NDA approval, not out of concern about safety or efficacy. Nevertheless, enfolitinib is also unable to overcome FGFR resistance.

As of now, there are 14 FGFR inhibitors in global clinical development stages II or later, including two for the treatment of cholangiocarcinoma that has progressed after previous FGFR inhibitor therapy. In China, there are 11 FGFR inhibitors in phase II or later clinical development, among which only one is used for the treatment of cholangiocarcinoma that has progressed after previous FGFR inhibitor therapy. Globally, to date, tinogotinib stands out as the only candidate drug in registration clinical trials, used in China for the treatment of cholangiocarcinoma that has progressed after previous FGFR inhibitor therapy.

Data source: Center for Drug Evaluation, ClinicalTrials.gov, Frost & Sullivan analysis

Competitive landscape of AXL/FLT3 inhibitors

As of now, there is only one AXL/FLT3 inhibitor (Gemcitabine from Astellas Pharma) that has been approved by the FDA and the National Medical Products Administration for AML in 2018 and 2021, respectively. No AXL inhibitors have been approved for the treatment of solid tumors. As of now, four AXL inhibitors for solid tumors are in clinical trials in the United States, while three are in clinical trials in China.

Data source: Center for Drug Evaluation, ClinicalTrials.gov, Frost & Sullivan analysis

Competitive landscape of BTK inhibitors

As of now, the FDA has approved four BTK inhibitors, and the National Medical Products Administration has approved five BTK inhibitors. Among them, pirtobrutinib is the only non-covalent reversible BTK inhibitor. To date, there are two non-covalent reversible BTK inhibitors in development in the United States for the treatment of hematological malignancies; in China, eight non-covalent reversible BTK inhibitors are in clinical development for the treatment of hematological malignancies.

PART/4

Driving factors of targeted therapy for small molecule tumors in China

drug resistance

Despite the improved efficacy of small molecule tumor targeted therapies, one of the key issues with these treatments is the frequent emergence of resistance during disease progression. Most cancer patients receiving small molecule targeted drugs gradually develop resistance, such as to small molecule targeted drugs targeting FGFR, BTK, EGFR, ALK, and NTRK. Almost all patients with cholangiocarcinoma treated with FGFR inhibitors eventually develop resistance. Metastatic prostate cancer was initially sensitive to AR antagonists but eventually develops resistance due to lineage plasticity and other mechanisms. For HR+/HER2- breast cancer, most patients eventually develop acquired resistance to first-line treatments including CDK4/6 inhibitors. Therefore, there is a huge need for second-line treatment for these cancer patients.

Low five-year survival rate

Currently, there is no direct method for early detection of cholangiocarcinoma. Therefore, patients with cholangiocarcinoma are usually diagnosed at an advanced stage, resulting in a low survival rate. Cholangiocarcinoma is characterized by its high malignancy, invasiveness, and rapid progression, with a five-year survival rate of about 10%, which is far lower than the five-year survival rate of 69% for all cancer types combined in the United States.

Major cancer types with high incidence and mortality

In 2023, breast cancer and prostate cancer were the two cancers with the highest incidence rates in the United States, accounting for the largest number of new cancer cases. Similarly, in China, breast cancer and prostate cancer are also among the top ten cancers with the highest incidence rates, ranking sixth and ninth respectively. In addition, breast cancer and prostate cancer were one of the five leading causes of cancer-related deaths in the United States in 2023, with breast cancer ranking fourth and prostate cancer ranking fifth. In China, the mortality rate from breast cancer ranks seventh.

Demand keeps increasing

As the cancer patient population continues to expand, the demand for innovative drugs with better efficacy is also increasing day by day. This is especially true for cancers with limited treatment options. In recent years, new targets such as FGFR, KRAS, and c-MET have become a focus of development.

PART/5

Barriers to entry into the Chinese small molecule tumor targeted therapy market

Gain a deep understanding of disease mechanisms and key pathogenic factors

A comprehensive understanding of disease mechanisms and the identification of key pathogenic factors are crucial for precise molecular targeting at various key targets. Effective entry into cells and precise targeting are at the core of the development of small molecule targeted drugs.

Target discovery, compound screening, and optimization

The success of small molecule targeted drug development depends on target discovery, compound screening, and optimization. The main challenges include fierce competition around popular targets, as well as the scarcity of new targets and innovative technical methods. Breakthroughs in target discovery and compound design are crucial for overcoming these entry barriers.

Drug design for the general patient population

Small molecule targeted drugs are usually only effective for patients with specific gene mutations, limiting their broad-spectrum applicability.

For example, when selecting targeted anti-tumor drugs, identifying specific gene mutations in patients is usually a prerequisite, highlighting the critical role of genetic testing in configuring targeted therapies. Designing therapies that can potentially treat a broader patient population remains a significant challenge.

Solving the problem of drug resistance

Overcoming drug resistance is another major obstacle for small molecule targeted drugs. Almost all small molecule targeted drugs face the problem of resistance after a period of clinical use. Resistance mechanisms include increased drug efflux, reduced cell uptake, target cell gene mutations, altered signaling pathways, phenotypic remodeling, and reactivation of the DNA repair system. Addressing these resistance challenges is crucial for expanding the clinical utility of targeted therapies.