NIO Group successfully listed on the main board of the Singapore Exchange on May 20, 2022, by way of an introductory presentation. Frost & Sullivan provided exclusive industry advisory services for NIO Group's listing in Singapore and hereby extends its warmest congratulations on its successful listing.

During the listing process in Singapore, Frost & Sullivan mainly undertook the following tasks: helping the company accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the company's competitive advantages, assisting the company, investment banks, and other intermediaries in completing the relevant parts of the prospectus (such as summaries, industry overviews, business sections), facilitating communication between the company and the Singapore Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the company in completing feedback on various industry-related issues from the Singapore Exchange.

Electric vehicles include pure electric cars and plug-in hybrid electric vehicles (PHEVs). Pure electric cars are powered solely by batteries, with all power generated by the motor, thus achieving zero emissions. Plug-in hybrid electric vehicles are equipped with both an internal combustion engine (ICE) and a motor, powered by fuel and batteries (which can be charged through an external power source).

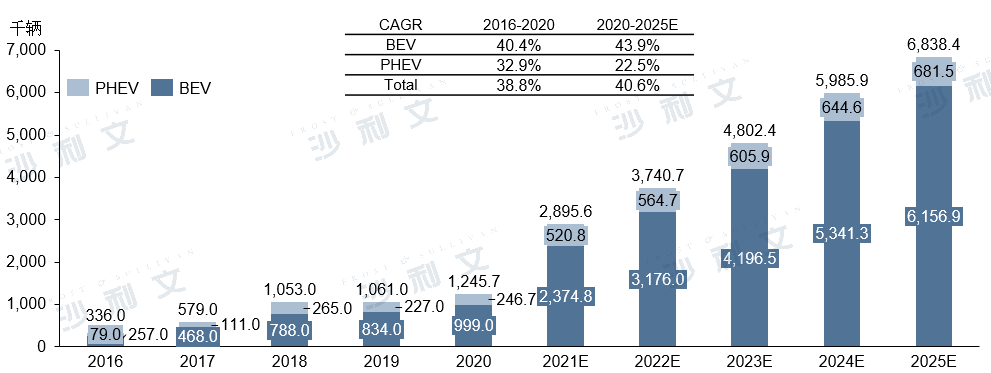

In 2020, global electric vehicle sales reached 2.9 million units. According to a Frost & Sullivan report, global electric vehicle sales are expected to reach 14.3 million units by 2025, with a compound annual growth rate of 37.1%. In the electric vehicle market, the pure electric segment is expected to grow at a faster pace, with global sales increasing from 2 million units in 2020 to about 11.4 million units in 2025, with a compound annual growth rate of 41.7%. At the same time, the penetration rate of pure electric vehicles in the global passenger vehicle market is expected to increase from 3.4% in 2020 to 15.4% in 2025. In the first nine months of 2021, the global pure electric vehicle market continued the aforementioned momentum, selling 2.6 million units, a year-on-year increase of 148.4%.

Global electric vehicle sales by type

2016 to 2025 (forecast)

Source: Frost & Sullivan report

China is an absolute leader in the global pure electric vehicle market

In terms of sales volume, China is the world's largest passenger vehicle market. According to a Frost & Sullivan report, China's passenger vehicle sales are expected to increase from 20.2 million units in 2020 to 2.35 million units in 2025, accounting for 31.9% of global market sales. The vast majority of the share of the Chinese electric vehicle market is occupied by pure electric vehicles. In 2020, compared with the global market's 67.6%, China had the highest proportion, reaching 80.2%. As the penetration rate of pure electric vehicle sales grows from 5.0% in 2020 to 26.2% in 2025, the Chinese market is expected to bring the largest global market opportunity to pure electric vehicle manufacturers in the long term.

According to a Frost & Sullivan report, China is the largest pure electric vehicle market in 2020, accounting for 50.2% of global pure electric vehicle sales. It is also one of the fastest-growing pure electric vehicle markets in the world, with sales increasing from 300,000 units in 2016 to 1 million units in 2020, a compound annual growth rate of 40.4%. From 2020 to 2025, it is expected that China's pure electric vehicle market will continue to grow rapidly at a compound annual growth rate of 43.9%, reaching an annual sales volume of 6.2 million units by 2025.

The significant growth potential of China's pure electric vehicle market is evident from the 1.7 million pure electric vehicles sold in the first nine months of 2021, a year-on-year increase of 229.6%, with a sales penetration rate of 11.5%.

Sales volume of electric vehicles in China by type

2016 to 2025 (forecast)

Source: Frost & Sullivan report

European and US markets

The European market is an important geographical region for electric vehicle sales, with a total sales volume of 1.3 million vehicles in 2020 and an expected growth to 4.7 million vehicles by 2025, with a compound annual growth rate of 30.1%. Among them, the European pure electric vehicle market saw sales of 700,000 vehicles in 2020 and is expected to reach 3.4 million vehicles by 2025, with a compound annual growth rate of 37.6%. According to Frost & Sullivan's report, the penetration rate of pure electric vehicles in Europe is expected to increase from 5.1% in 2020 to 19.5% in 2025.

According to a Frost & Sullivan report, the US electric vehicle market is expected to grow rapidly from 300,000 units in 2020 to 2.6 million units in 2025, with a compound annual growth rate of 51.0%.

According to a Frost & Sullivan report, consumers are increasingly concerned about the environmental impact of vehicle emissions and have turned towards cars that emit less or no emissions. Using electric vehicles can reduce emissions more effectively than traditional fuel vehicles.

China expects to peak carbon emissions before 2030 and the government aims to achieve carbon neutrality by 2060. The Chinese government has issued a number of policies to support the growth of new energy vehicles (NEVs), including pure electric cars, with plans to achieve a penetration rate of 20% by 2025. China also introduced the new energy vehicle credits and average fuel consumption credits trading plan in 2018 to promote electric vehicle production. To further support the promotion of NEVs, national subsidies for NEVs and tax incentives have been extended from the end of 2020 until the end of 2022. The current subsidy policy for 2021 applies to new energy vehicles priced below RMB 300,000 or equipped with battery swapping technology. Compared to fuel vehicles, several Chinese municipal regulations are also conducive to the promotion of pure electric cars, including lowering the threshold for obtaining vehicle licenses and lifting restrictions on the use of pure electric cars.

Governments around the world have also formulated policies to promote electric vehicles. The EU aims to achieve net greenhouse gas emissions of zero by 2050 and has introduced a number of support policies for zero-emission vehicles, including purchase subsidies and tax exemptions. The Norwegian government plans to make all new private cars, urban buses, and light trucks zero-emission by 2025. The British government announced that it plans to end the sale of new gasoline and diesel vehicles by 2030, with the goal of making all new car sales zero-emission by 2035. In the United States, a presidential executive order was signed on August 5, 2021, setting the goal of having 50% of all new passenger cars and light trucks sold by 2030 be zero-emission (including pure electric and plug-in hybrid vehicles). In addition, 40 states offer tax incentives or rebates for purchasing electric vehicles, and California has even stipulated that all new passenger cars and trucks sold within the state must be zero-emission by 2035.

Battery technology progress

Battery technology advancements have enabled the rapid development of the electric vehicle industry. Continuous technological progress has increased energy density, improved safety levels, and extended battery life. For example, in 2019, the energy density of battery cells ranged from 217 to 252 watt-hours per kilogram. As of the latest practicable date, according to Frost & Sullivan reports, the energy density of multiple battery cell products on the market has exceeded 300 watt-hours per kilogram. Due to these advancements, the user experience of electric vehicles has been further improved.

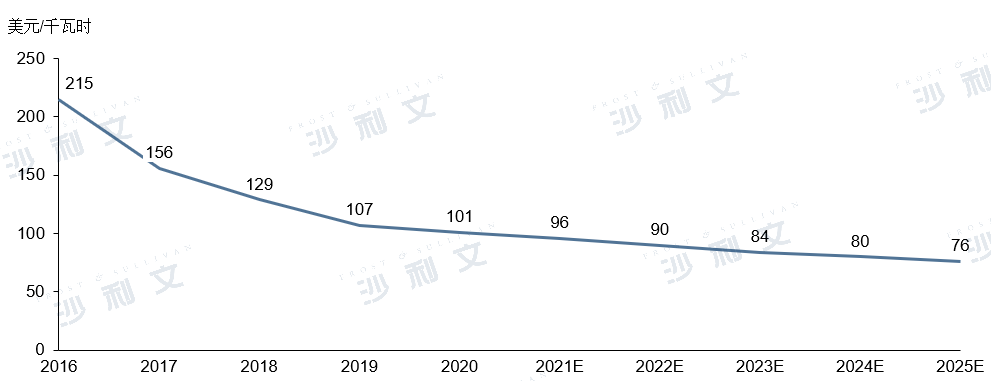

Due to the increased scale effect of battery production and technological progress, battery costs are expected to be significantly reduced. According to a Frost & Sullivan report, the price of battery cells in China is expected to fall from $101 per kilowatt-hour in 2020 to $76 per kilowatt-hour in 2025.

Weighted average price of Chinese battery cell transactions

From 2016 to 2025forecast

Source: Frost & Sullivan report

According to a Frost & Sullivan report, battery swapping technology facilitates the separation of ownership of cars and batteries, allowing consumers to purchase cars separately from renting batteries. This scheme reduces upfront costs while providing flexibility for battery upgrades with technological progress.

Expand electric vehicle infrastructure

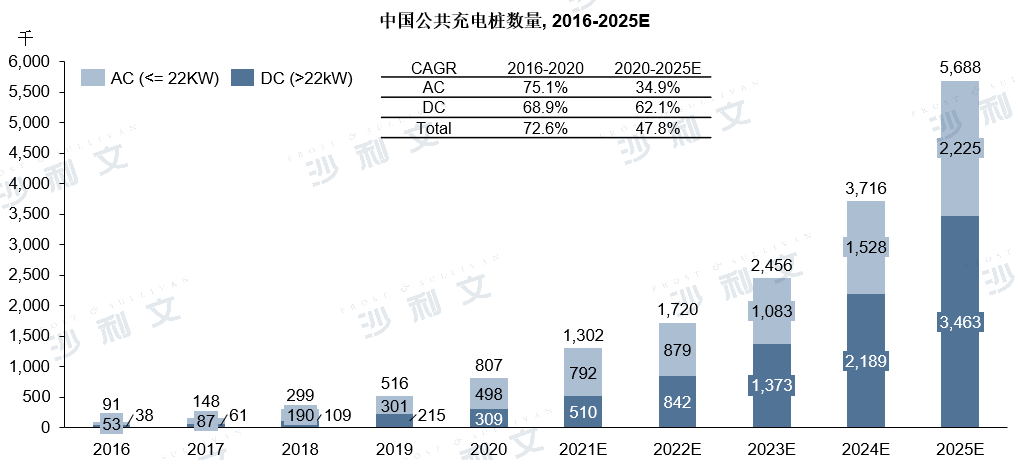

Governments around the world are continuously advancing the layout of electric vehicle infrastructure, which has become an important factor in encouraging consumers to choose electric vehicles. The Chinese government has specifically listed charging and swapping infrastructure as a key area of "new infrastructure," enjoying preferential policy support in infrastructure construction and layout. In the past five years, China's charging network has grown significantly. According to a Frost & Sullivan report, by the end of 2020, China had more than 800,000 public charging piles, of which 38% were DC fast chargers. To meet the growing demand of consumers, the total number of public charging piles in China is expected to increase significantly to 5.7 million by 2025, with a compound annual growth rate of 47.8%, of which 61% will be DC fast chargers.

Number of public charging piles in China

2016 to 2025 (forecast)

Source: Frost & Sullivan report

Meanwhile, first-class automakers are deploying their own fast charging and/or battery swapping stations to further improve the user experience.

In Europe, electric vehicle infrastructure has developed rapidly. According to a Frost & Sullivan report, by the end of 2020, there were approximately 300,000 public charging piles in Europe, of which 13% were DC fast chargers. By 2025, the total number of public charging piles in Europe is expected to reach 1.2 million, of which 38% will be DC fast chargers.

Autonomous driving and digital technology

Advanced driver assistance systems, autonomous driving, personalized entertainment, and AI-powered human-machine interaction interfaces have significantly improved the user experience. Consumers' recognition of these technologies continues to rise, promoting their broader application in the future. The advancement of such technologies requires more sensors, higher-level computing capabilities, and advanced software to more efficiently integrate and remotely upgrade according to the electric/electronic architecture of electric vehicles.

In recent years, an increasing number of automakers have introduced ADAS features, generally including adaptive cruise control, lane change/keep assist, automatic emergency braking, and autonomous parking. According to a Frost & Sullivan report, the penetration rate of ADAS in new passenger vehicles in China increased from 11.4% in 2016 to 38.4% in 2020, and is expected to further increase to 55.7% by 2025.

With the continuous progress of hardware and software technologies, it is expected that cars will become more powerful with the ongoing advancement of autonomous driving technology. Autonomous driving hardware generally includes computing system-on-chip (SoC) chips, cameras, lidar, radar, and other sensors. According to a Frost & Sullivan report, driven by consumer preferences, technological improvements, market competition, and geographical environment, the computing power of central processing unit chipsets is expected to gradually develop, while the manufacturing of microcontroller unit chipsets with lower computing power is expected to be more localized. The full-stack software capabilities for autonomous driving include perception, planning, and control algorithms, high-definition maps, and dead-loop data management. Autonomous driving technology is expected to save time spent on driving while improving road safety.

Emerging digital technologies in the automotive industry mainly include digital cockpits and digital systems. Development trends of digital cockpits: (i) Providing each passenger with rich and personalized entertainment; and (ii) AI-powered advanced human-machine interaction interfaces, such as voice control systems and driving behavior monitoring. Automakers also strengthen the development or achieve continuous upgrades of their digital systems through remote firmware and software updates. FOTA (Over-the-Air) updates can perform firmware upgrades for the entire core automotive system (such as digital cockpits, autonomous driving domain controllers, and electric powertrain). SOTA (Software-Over-The-Air) updates can improve automotive software, such as in-vehicle infotainment systems.

With the continuous development of autonomous driving technology and the widespread adoption of digital technology, Frost & Sullivan expects the automotive industry to generate new innovative business models. For example, autonomous driving technology can be provided to consumers as a rental service, and new technology upgrades can be achieved through convenient remote updates, continuously improving the user experience. As drivers enjoy leisure time in the car that does not require driving, additional business opportunities such as infotainment content and functions may emerge.

According to the Frost & Sullivan report, China's high-end segment (defined as automobiles priced above RMB 300,000) is expected to be the fastest-growing segment, with a compound annual growth rate of 12.1% from 2020 to 2025.

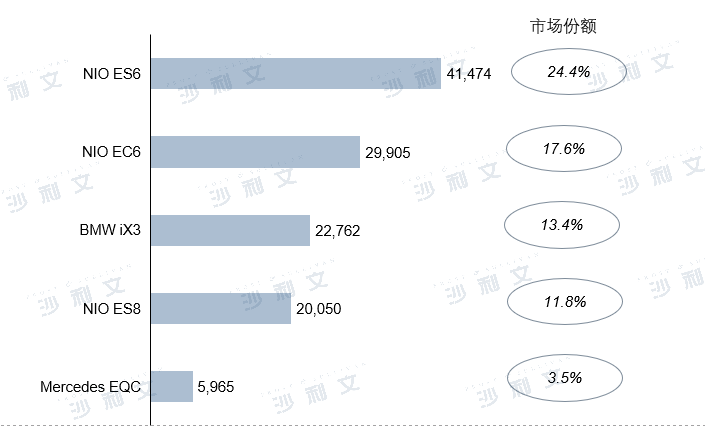

According to a Frost & Sullivan report, in 2021, NIO ES6 and EC6 were the two highest-selling high-end pure electric SUVs in China.

China's high-end pure electric SUV cumulative sales ranking2021

Source: Frost & Sullivan report

In the high-end mid-to-large SUV market, compared to similar vehicles such as fuel-powered cars, the NIO ES8 has excellent acceleration performance, horsepower, torque, ADAS and in-car AI functions, as well as a price advantage. At the same time, the ES8 is comparable in performance to the Tesla Model X and BMW iX, but it has an obvious price advantage.

Compared to other high-end mid-size electric SUVs, the WEY ES6 and EC6 offer the best NEDC range, maximum output horsepower and torque in their class, as well as cabin AI features.

In the high-end mid-to-large sedan market, compared to similar vehicles such as fuel-powered cars or plug-in hybrid vehicles, the NIO ET7 offers superior performance, richer autonomous driving and cockpit AI features, as well as more favorable pricing. Compared to the Tesla Model S, the ET7 boasts comparable performance, the best autonomous driving computing and sensing capabilities in its class, as well as the most advanced cockpit AI features, while also having a significant price advantage.

Frost & Sullivan has extensive research experience in the automotive and transportation industries, assisting well-known companies in successfully listing on capital markets. Successful listings include Cangang Railway (2169.HK), YGMZ.NASDAQ, Asia Express (8620.HK), InfinityL&T (1442.HK), TOMOHOLDINGS (6928.HK), EH.NASDAQ, Aodima (8418.HK), Xiangxing International (8157.HK), CIMC Vehicles (1839.HK), Xunlong (1930.HK), CSSC Leasing (3877.HK), Chengdu Expressway (1785.HK), Tianrui Automotive Interior (6162.HK), Periphery Holdings (2885.HK), Huazi International (2258.HK), Pulin Chengshan (1809.HK), NIO.NYSE, Wanlida (8482.HK), Qilu Expressway (1576.HK), Yingheng Technology (1760.HK), Asia Industry (1737.HK), Ruifeng Power (2025.HK), Gaomeng Technology (8065.HK), Hebei Yichen (1596.HK), Zhengli Holdings (8283.HK), Junao Holdings (8035.HK), Yadi Group (1585.HK), Yihai Car Rental (EHIC.NYSE), Xinchen Power (1148.HK), Zhengxing Wheels (ZX.NYSE), Shuanghua Holdings (1241.HK), Changche Bridge (1039.HK).

Recommended Reading

02. Frost & Sullivan assists YGMZ.NASDAQ's successful listing in the US

06. Frost & Sullivan assists iFlytek in successfully going public in the US (EH.NASDAQ)

17. Frost & Sullivan assists NIO Automotive in successfully going public in the US (NIO.NYSE)

Frost & Sullivan assists Asian companies in successfully going public in Hong Kong (1737.HK)

Frost & Sullivan helps Gaomeng Technology successfully go public in Hong Kong (8065.HK)

24. Frost & Sullivan assists Hebei Yichen in successfully going public in Hong Kong (1596.HK)