Yunkang Group Co., Ltd. (hereinafter referred to as Yunkang Group) successfully went public on May 18, 2022, with an issue volume of 138,188,000 shares at a subscription price of HK$7.89 per share, raising approximately HK$761 million in net funds.

During the Hong Kong listing process, Frost & Sullivan mainly undertook the following tasks: helping the company accurately and objectively understand its positioning in the target market, using objective market data to discover, support, and highlight the company's competitive advantages, assisting the company, investment banks, and other intermediaries in completing relevant parts of the prospectus (such as the overview, competitive advantages and strategy, industry overview, business, and other important sections), facilitating communication with the Hong Kong Stock Exchange and investors, helping investors quickly understand the market ecosystem and competitive landscape, and assisting the company in completing feedback on various industry-related issues from the Hong Kong Stock Exchange.

China Medical Operation Service Market

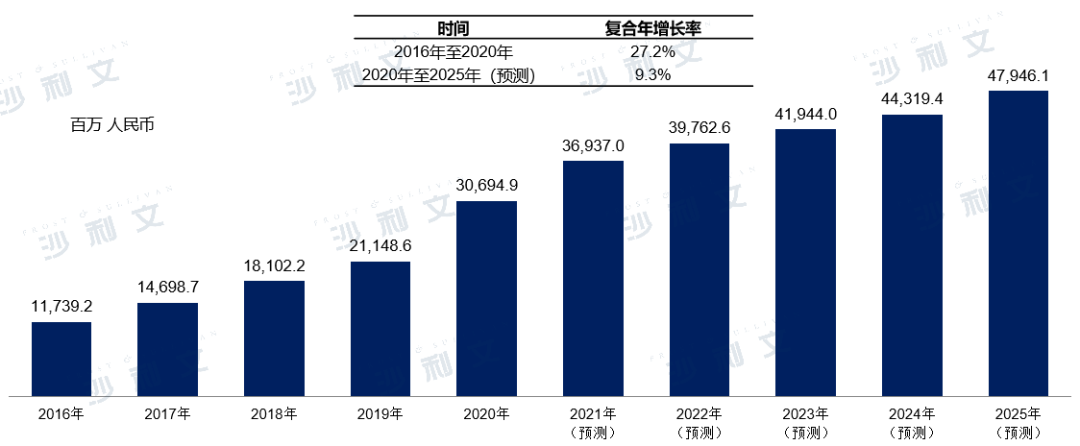

Medical operation services are mainly related to diagnostic testing services provided to medical institutions, which can be divided into diagnostic outsourcing services and diagnostic testing services provided for medical consortia. With the introduction of favorable policies in China and the enhancement of public healthcare awareness, the market for medical operation services in China has developed rapidly, increasing from 11.74 billion yuan in 2016 to 30.69 billion yuan in 2020, with a compound annual growth rate of 27.2%. It is expected that the market for medical operation services in China will continue to grow significantly, reaching 479.5 billion yuan by 2025.

Market scale and forecast of medical operation services in China2016-2025E

Source: Frost & Sullivan report

Independent clinical laboratories are independent legal entities qualified to provide clinical testing or pathological laboratory services under the permission of health administrative departments. Frost & Sullivan research shows that independent clinical laboratories are in an early stage in China and have great growth potential. In terms of the number of independent clinical laboratories, as of the end of 2020, China had more than 1,800 independent clinical laboratories, while the United States had about 6,800 independent clinical laboratories. In terms of testing capabilities, leading independent clinical laboratories in China can provide approximately 3,500 testing items, while those in Europe and the United States can offer about 5,000 testing items.

In addition, independent clinical laboratories are highly concentrated in China, especially in first- and second-tier cities. Many medical institutions find it difficult to locate a qualified independent clinical laboratory nearby, so they must conduct diagnostic tests themselves even if time and cost are high. Especially for diagnostic tests with high technical and operational requirements, such as pathology tests, genetic disease tests, and infectious disease tests, lower-level medical institutions do not have the technical and operational capabilities to perform these tests.

As of 2020, the penetration rate of independent clinical laboratories in China was only 6%, while it was 50% and 35% respectively in Europe and America. With the increase in the number of independent clinical laboratories in China and the potential growth of medical consortia, it is expected that more medical institutions will choose to commission medical operation service providers for diagnostic testing services. To support the development of independent clinical laboratories in China, the Chinese government has introduced a series of healthcare reform policies such as the 'Administrative Measures for Clinical Laboratories of Medical Institutions' to regulate the industry and support the development and investment of independent clinical laboratories.

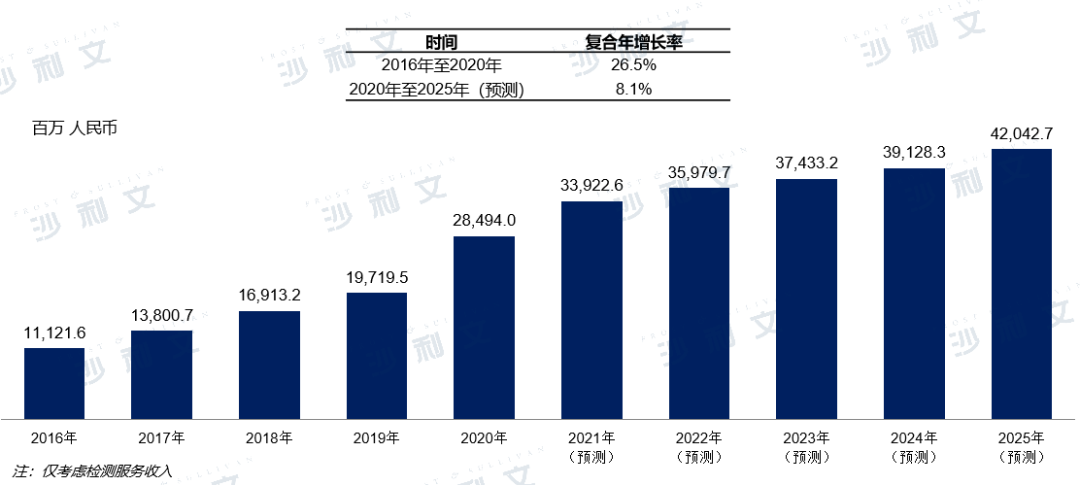

China's diagnostic outsourcing service market

Accurate and effective diagnosis is the foundation of precision medicine. Therefore, hospitals must establish diagnostic testing standards to enhance their clinical and pathological diagnostic capabilities. However, diagnostic testing is a time-consuming and costly process, and hospitals may not be cost-effective if they conduct all testing on their own. As a result, there is a huge market demand for independent clinical laboratories that can provide standardized and modular one-time diagnostic testing services. Driven by this, the scale of China's diagnostic outsourcing service market has grown rapidly, increasing from 11.12 billion yuan in 2016 to 28.49 billion yuan in 2020. It is estimated that the diagnostic outsourcing service market will further grow to 42.04 billion yuan by 2025.

China's diagnostic outsourcing service market,2016 - 2025E

Source: Frost & Sullivan report

Diagnostic outsourcing services aim to provide immediate one-time solutions for medical institutions lacking diagnostic capabilities and capacity. For medical institutions that do not possess their own diagnostic capabilities and capacity, they mainly rely on diagnostic outsourcing services for supply of diagnostic testing. In recent years, supported by favorable government policies, there has been an impetus for the development of diagnostic testing service models by medical consortiums. Medical institutions have the opportunity to cooperate with medical operation service providers to conduct diagnostic testing on-site at corresponding diagnostic centers. Therefore, the test samples collected by medical institutions do not need to be sent to independent clinical laboratories for testing but can be completed at these diagnostic centers. Compared with the diagnostic testing services of medical consortiums, the growth of China's diagnostic outsourcing service market will significantly slow down in the future.

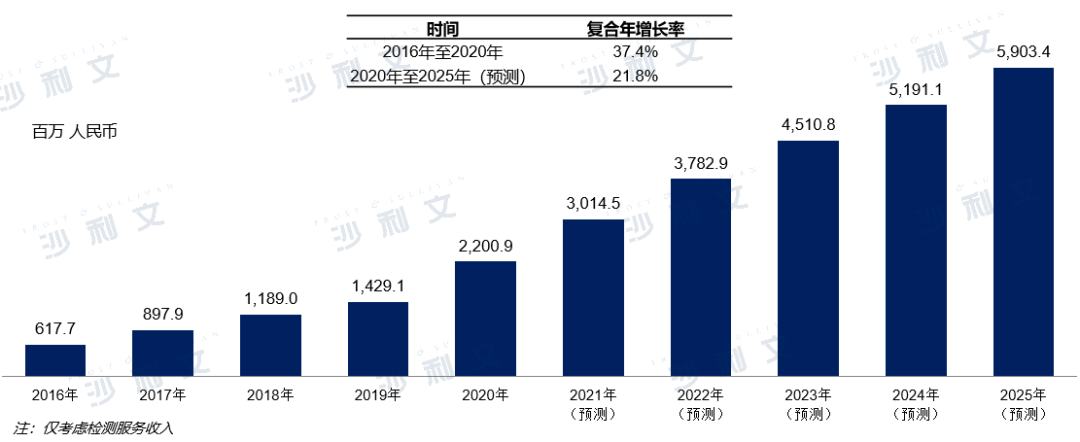

China Medical Consortium Diagnostic Testing Service Market

Medical consortia typically consist of a leading hospital (i.e., a secondary or tertiary hospital) and several member hospitals that require the support of the leading hospital. To address the limitations of diagnostic outsourcing services, many hospitals have tended to adopt new service models within medical consortia in recent years to build their own diagnostic capabilities. Under this model, healthcare institutions and medical operational service providers will cooperate to establish on-site diagnostic centers within the healthcare institution and jointly manage the daily operations of the centers. Service providers will also provide various technical supports to assist in diagnostic testing services. As a result, healthcare institutions have the opportunity to conduct on-site diagnostic testing in a timely and effective manner.

Under the medical consortium system, most patients will first go to lower-level medical institutions for diagnosis. If the lower-level institutions are unable to provide the necessary treatment, patients will be transferred to higher-level medical institutions within the consortium system. Through the collaborative efforts of multiple levels of medical institutions, and to promote the optimal allocation of medical resources, the state encourages patients with common and chronic diseases to receive treatment at primary-level medical institutions. Patients with serious or complex diseases that are beyond the capabilities of primary-level institutions should go to secondary or tertiary medical institutions for treatment, thereby improving efficiency.

Due to the current lack of such professional knowledge or experience among most member hospitals, this collaborative process has led to a market demand for standardized and professional diagnostic testing capabilities. At the same time, with the introduction of favorable policies and the public's increasing awareness of healthcare, the total market size of diagnostic testing services within China's medical consortiums is showing an increasingly growing trend. In 2020, the market size of diagnostic testing services within China's medical consortiums was 220, compared to 62 in 2016, with a compound annual growth rate of 37.4%. By 2025, the market size in China is expected to grow to 590.

China's Medical Consortium Diagnostic Testing Service Market2016 - 2025E

Source: Frost & Sullivan report

Frost & Sullivan, integrating 61 years of global consulting experience, has dedicated 24 years to serving the booming Chinese market. With a global perspective, we help clients accelerate their business growth and achieve benchmark positions in industry growth, innovation, and leadership. The healthcare industry is one of Frost & Sullivan's core areas of focus. Over the past seventeen years, the Frost & Sullivan healthcare team has provided financing financial advisory, IPO industry advisory, strategic consulting, management consulting, and other services for hundreds of outstanding domestic and international biopharmaceuticals, medical devices, healthcare services, and internet healthcare companies. Successful listings include: Ruike Biotech (2179.HK), Leopu Biotech (2157.HK), Clear Medical (1406.HK), Bexin An (2185.HK), Yonghe Medical (2279.HK), Kailaiying (6821.HK), Beihai Kangcheng (1228.HK), Gusheng Tang (2273.HK), Yingtong Technology (2251.HK), Clover Biotech (2197.HK), Minimally Invasive Robotics (2252.HK), Harmony Cayman (2256.HK), Kunbo Medical (2216.HK), Xianruida (6669.HK), Kangsheng Global (9960.HK), Yimaitong (2192.HK), Tengsheng Bo Yao (2137.HK), Canopy Biosciences (2162.HK), Chaoyu Eye Hospital (2219.HK), Guichuang Tongqiao (2190.HK), Hua Huang Medicine (0013.HK), Cope Pharma (2171.HK), Zhaoke Ophthalmology (6622.HK), Nature Pharmacy (UPC.NASDAQ), Saisen Pharmaceutical (6600.HK), Zhaoyan New Drugs (6127.HK), Novogene Health (6606.HK), Tianyan Pharmaceuticals (ADAG.NASDAQ), Beikang Medicine (2170.HK), Jianbimiao Miao (2161.HK), Minimally Invasive Heart Link (2160.HK), Rui Li Medical Beauty (2135.HK), Jiake Pharmaceutical (1167.HK), Hepcon Pharma (2142.HK), JD Health (6618.HK), Deqi Medicine (6996.HK), Rongchang Biotech (9995.HK), WuXi AppTec (2126.HK), Sonovent Pharmaceuticals (2096.HK), Yunding New Energy (1952.HK), Jiahe Biotech (6998.HK), Zai Ding Medicine (9688.HK), Ocular Biotechnology (1477.HK), Yongtai Biotech (6978.HK), Hapu Pharmaceutical (9989.HK), Pioneering Pharmaceuticals (9939.HK), Peijia Medical (9996.HK), Kangfang Biotech (9926.HK), Nuo Cheng Jianhua (9969.HK), Tianjing Biotech (IMAB.NASDAQ), Kanglong Chemical (3759.HK), China Antibody (3681.HK), Dongyao Pharmaceutical (1875.HK), Yasheng Medicine (6855.HK), Fuhong Hanlin (2696.HK), Hansoh Pharmaceutical (3692.HK), Mabtech (2181.HK), Fangda Holdings (1521.HK), Via Biotech (1873.HK), CStone Pharmaceuticals (2616.HK), Junshi Biosciences (1877.HK), WuXi AppTec (2359.HK), Innovent Biologics (1801.HK), Hualing Medicine (2552.HK), BeiGene (6160.HK), Gilead Sciences (1672.HK), WuXi AppTec (2269.HK), China Resources Pharmaceutical (3320.HK), Yakult Scientific Research Pharmaceutical (2633.HK), Hua Huang China Medicine (HCM.NASDAQ), Biotechnology (1548.HK), BBI Life Sciences (1035.HK), etc. In terms of the number of filings, the Frost & Sullivan healthcare team maintains an absolute leading position in Hong Kong's healthcare IPO market, consistently ranking first in market share from 2018 to 2021.

Since the listing of the first batch of companies on the Sci-tech Innovation Board in July 2019, Frost & Sullivan reports have also been widely cited in the prospectuses of leading Sci-tech Innovation Board-listed companies in the industry. This includes: Jicui Pharmaceutical (688046.HK), Haichuang Pharmaceutical (688302.SH), Rongchang Biotech (688331.SH), Rendu Biotech (688193.SH), Shouyao Holdings (688197.SH), Heyuan Biotech (688238.SH), Yaxin Security (688225.SH), Xidi Microelectronics (688173.SH), Mawei Biotech (688062.SH), Yahong Medicine (688176.SH), BeiGene (688235.SH), CHERA Pharma (688246.SH), Dizhe Pharma (688192.SH), Novozyme (688105.SH), Chengda Biology (688739.SH), Geke Microelectronics (688728.SH), Huaxi Biotech (688363.SH), Junshi Biosciences (688180.SH), Zhejiang Genomics (688266.SH), BeiGene Pharma (688177.SH), and Shenzhou Cells (688520.SH). They are considered the most powerful, professional, and influential industry research institutions in the sector. We hope to work with enterprises to gain insights into industry trends, seize development opportunities, jointly promote innovation and upgrading of China's healthcare industry, and build a healthy future.

Recommended Reading

Frost & Sullivan helps Zhaoyan New Drugs successfully list on the Hong Kong Stock Exchange (6127.HK)

37. Frost & Sullivan assists WuXi AppTec Biologics (0988.HK) on its successful listing in Hong Kong

41. Frost & Sullivan assists Zai Lab to successfully go public in Hong Kong (9688.HK)

49. Frost & Sullivan assisted Tianjing Biology in successfully going public in the US (IMAB.NASDAQ)