Future Trends of China's Healthcare Industry

"Healthy China 2030"Since the implementation of the strategy, China's healthcare industry has developed rapidly driven by both market and policy factors. Data shows,"2021In China, the total investment and financing in the healthcare industry reached2,192100 billion yuan, hitting a new high and a year-on-year increase32.84%Driven by capital and the parallel implementation of an innovative model integrating industry, academia, and research, Chinese local pharmaceutical companies have grown rapidly. The transformation of scientific research achievements has been advanced efficiently, moving from following to paralleling to surpassing others, gradually stepping onto the world stage, and is expected to completely break through bottleneck issues.

Standing at the new starting point of the first year of the 14th Five-Year Plan, and further deepening and advancing the Healthy China 2030"Under the strategy In the new decade-long journey, how can we promote the synchronous resonance of healthcare industry, technology, talent, and capital? We should be clinical-oriented in driving product development, creating personalized medical products and services with high pharmacoeconomic value, narrowing the gap with developed countries' healthcare standards, and further strengthening the stability and sustainability of China's healthcare supply chain. Chinese healthcare enterprises still have a long way to go.

9month1day-2day,2022 CHC· CITIC Securities Healthcare Conference & 11th China Healthcare Industry Investment and M&ACEOThe summit was grandly held in Hefei, Anhui Province, at Frost & Sullivan (Frost & Sullivan,Dr. Wang Xin, Global Partner and President of Greater China at Frost & Sullivan (hereinafter referred to as 'Frost & Sullivan'), was invited to attend the summit and delivered a speech on the future trends of China's healthcare industry.

Global Partner and President, Greater China at Frost & Sullivan Dr. Wang Xin

Global Partner and President, Greater China at Frost & Sullivan Dr. Wang Xin

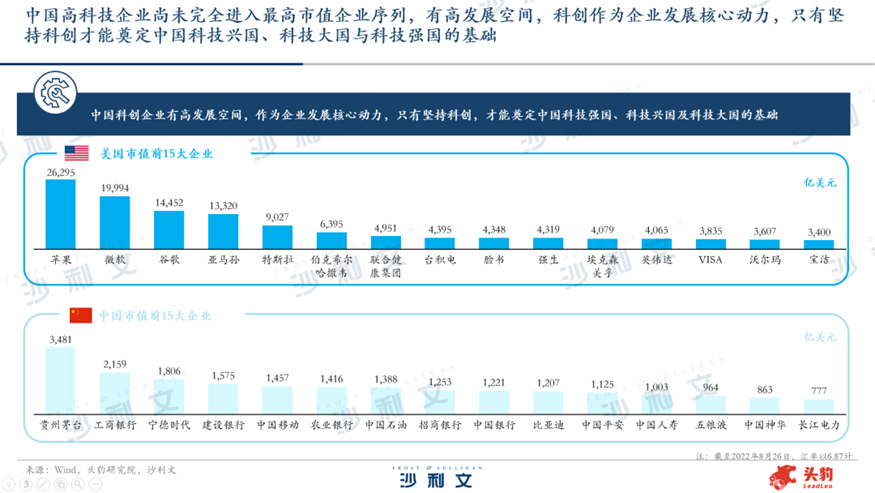

Dr. Wang Xin first analyzed the opportunities for the healthy development of healthcare in China. He pointed out that Chinese technology companies still have great room for development and growth opportunities. Compared to the US stock market, Chinese high-tech companies have not yet fully entered the ranks of the highest market value companies, and their proportion can be further increased. Technological innovation is the core driving force for enterprise development. Only by persisting in technological innovation can we build a technically competitive system and lay the foundation for China to become a science and technology powerhouse, a major scientific and technological nation, and a strong scientific and technological country.

Data shows, Chinese healthcare enterprisesTop 20The average total market value gap with US companies9times more, and the total market value is more concentrated in leading enterprises. United StatesTop 20Enterprise market value average1,759.73billions, half of which are above the mean, while in ChinaTop 20The average enterprise market value is only193.20billions of dollars, and only7Leading companies are above the average. In addition, China's top20The market value of the top enterprises is the sum3,864dozens of millions, lower than UnitedHealth1Family-owned4,319Billions of dollars. Multiple data indicate that Chinese pharmaceutical companies are still focusing on the domestic market, with huge potential for future growth, and leading enterprises urgently need to shine.

"The healthcare industry is still in a critical period dominated by domestic enterprises. Although there are short-term impacts,PESTAnalysis shows that multiple factors are favorable to the development of China's healthcare industry, and the medical sector has broad development opportunities in the medium to long term. Dr. Wang Xin further explained, From the perspective of the policy environment, 2021The year 2021, which marked the beginning of the "14th Five-Year Plan," has passed. Over the past decade or so, China's healthcare industry has achieved rapid growth. Multiple policies have brought about changes in the rules of the game for the medical industry. In the future, against the backdrop of shared prosperity, the "14th Five-Year Plan" will comprehensively promote the development of the healthcare industry to a new level by outlining medical strategies.

From the perspective of the economic environment, Under the trend of normalized epidemic control, per capita healthcare expenditure has reached2,115Yuan, year-on-year growth15.90%The level of attention to people's health has risen once again.

From the perspective of the social environment, What China's healthcare sector needs to address is14The healthcare issue for hundreds of millions of people needs to be resolved2 - 3The healthcare issue for hundreds of millions of elderly people is a responsibility that the industry should undertake.

From the perspective of the technical environment, Artificial intelligence, biosynthesis technology,CGTBy bringing new innovation to the healthcare industry, looking at the international scene, China's R&D investment ratio has been continuously increasing. The continuous growth in pharmaceutical R&D investment indicates an enhanced R&D capability of pharmaceutical companies, which feeds back into the market through innovation and drives healthcare into a new development stage.

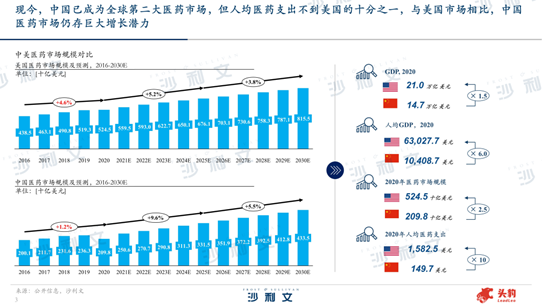

Compared with the US market, the Chinese pharmaceutical market still has tremendous growth potential. In terms of market size,2020In [year], the pharmaceutical market size in the United States was2.5times, with per capita medical expenditure being10.6times.

2020In [year], the US pharmaceutical market size was5,245billion US dollars. It is expected to2025In [year], the scale of the US pharmaceutical industry will reach6,761billion dollars2020Year to2025The annual compound growth rate for5.2%.2020In [year], the scale of China's pharmaceutical market was2,098billion dollars With the continuous development of domestic pharmaceutical companies and the implementation of multiple favorable policies in China, it is expected that by2025In [year], the scale of China's pharmaceutical industry will reach3,315billion dollars2020Year to2025The annual compound growth rate for9.6%.

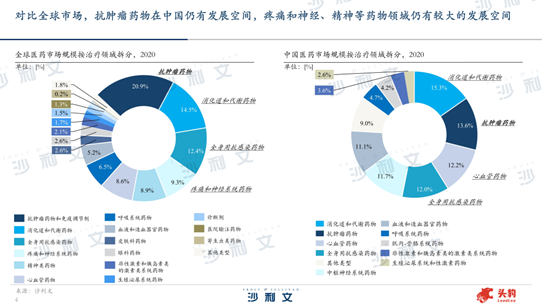

According to a study by Frost & Sullivan, in the Chinese pharmaceutical market, digestive system and metabolic drugs account for the highest proportion of market share. has been achieved15.3%; the anti-tumor drug market accounted for13.6%The cardiovascular drug market and the systemic anti-infective drug market accounted for12.2%and12.0%Antitumor drugs and immunomodulators account for the largest market share globally, reaching20.9%, It can be seen that the proportion of anti-tumor drugs in China still has significant room for growth. In addition, sub-sectors such as pain and neurological drugs, as well as psychotropic drugs, also have great development potential in China.

In addition, affected by COVID-19, the global pharmaceutical market competition landscape has changed.2020Year-on-year,2021Among the world's top five best-selling drugs globally, Pfizer's COVID-19mRNAThe vaccine has entered the list and topped it.ModernaCOVID-19mRNAVaccines also rank among the top. In China, one of the earliest domestic biopharmaceutical companies to develop innovative drugs, Junshi Biology, Qianyan Biotech, and Keda Pharmaceutical, have seen their stock prices rise after announcing the progress of their COVID-19 research and development efforts. This indicates that COVID-19 treatment drugs may become a new focus for research and development in the future.

In recent years, domestic biopharmaceutical companies have continuously increased their R&D expenditures to support innovation. Pharmaceutical company2021In terms of R&D investment ranking for the year, it has become the first company to list on NASDAQ, Hong Kong stocks, andABiotech star company BeiGene, listed on the stock market, has ranked first in R&D investment with ample capital support brought about by its listing in three major markets. The R&D expenditure reached94.14100 million yuan; ZaiDi Pharma itself2020After successfully going public on the Hong Kong Stock Exchange for a second time in 2021, leveraging the abundant financing available in the secondary capital market,2021R&D expenditure in the year2020Compared with last year, it has been achieved140.7%The year-on-year growth also confirms the importance of capital for the development of biotech companies.

Dr. Wang Xin stated that cross-border mergers and acquisitions transactions have decreased significantly in recent years due to the impact of the pandemic, butLicense-in grantedTransactions continue to set new highs in terms of volume and value, involving multiple emerging medical fields. Several biotech companies have chosen to introduce products that are in the early stages of research and development, clinical trials, or already on the market at home and abroad to acquire advanced R&D technologies, to make up for their own product pipeline shortcomings, create differentiated business advantages, and provide more treatment options for Chinese patients. According to statistics, only2021In [year], Chinese pharmaceutical companiesLicense-in AcquisitionThe number of transactions has reached130Yuqi, with most transaction volumes exceeding1billion US dollars, with some transactions exceeding3billions, product selection involves dual antibodies,siRNA,mRNAVaccines, cell therapy,ADCand many other emerging fields.

The advantage of introducing advanced R&D technologies from home and abroad lies in two aspects. On one hand, if the target or indication area aligns with the company's core R&D direction or compensates for the company's own product pipeline shortcomings, it can enrich the business layout and create a differentiated advantage. On the other hand, most of the products introduced are those that have entered clinical trials or are already on the market, and existing data can initially verify the efficacy and safety of the products. This will accelerate the domestic approval process for marketing and bring more treatment options to Chinese patients as soon as possible.

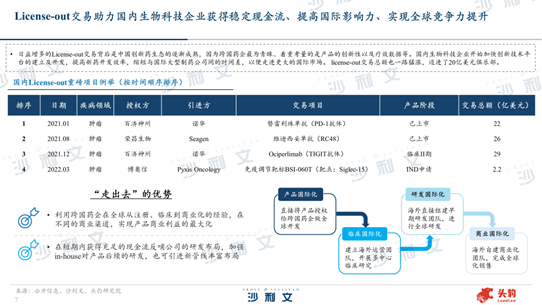

"With the enhancement of economic strength and the accelerated development of globalization, biotech companies are required not only to actively 'import' but also to seize the opportunity to boldly 'go global'." Dr. Wang Xin further said, 'As the domestic innovation drug ecosystem gradually takes shape and matures, biotech companies are continuouslyLicense-out of the MainlandTransactions bring domestic technology abroad, and by collaborating with multinational enterprises, we can better participate in global competition. Due to the emphasis on product innovation and efficacy data by multinational pharmaceutical companies, domestic biotech enterprises have begun to accelerate the establishment and development of innovative technology platforms, improving new drug development efficiency and shortening the time lag with international large pharmaceutical companies in order to enter larger international markets.

The advantage of bringing technology, equipment, and products abroad is that, on one hand, cooperation with multinational pharmaceutical companies means leveraging their global experience from registration, clinical trials to commercialization. At the same time, with a large amountLicense-out of the MainlandDriven by the project,FDAThe recognition of Chinese clinical data is beginning to emerge, which will facilitate the internationalization of domestic products. Multinational pharmaceutical companies' resources in different commercial channels can also help them maximize product commercial benefits. Especially for domestic pharmaceutical companies with overseas expansion needs, the endorsement from multinational pharmaceutical companies is more conducive to market expansion, allowing them to focus their efforts and resources on more competitive projects.

On the other hand, these companies can obtain sufficient cash flow support in the short term to strengthenIn-houseFor the subsequent research and development of products. At the same time, the substantial funds obtained enable the company to more readily introduce new technologies, expand new pipelines, develop new industries, and gradually form its own multinational corporation, better participating in economic globalization competition.

Overall, the level of domestic innovative drugs has been continuously improving with policy support. For example, a series of policies enacted in recent years have avoided generic drug monopolies on the drug approval process, reduced the threshold for establishing innovative pharmaceutical companies, encouraged new drug research and development, and focused on patient needs to avoid waste of clinical resources. Additionally, the R&D level of innovative drugs is also increasing, including a surge in overseas licensing, diversification of indications for domestic innovative drugs, and globalization trends in drugs. Against the backdrop of the COVID-19 pandemic, the development of COVID vaccines has driven rapid technological progress in the industry, but the marginal impact of the pandemic has diminished, and more focus should be placed on the company's non-COVID-related main business. Believing that under the guidance of national policies, nurtured by the global market, and catalyzed by the COVID-19 pandemic,2022In 2021, China's healthcare industry will increasingly integrate into the global innovation pulse.

Subsequently, Dr. Wang Xin analyzed the financing of China's healthcare industry in primary markets and the capital support in secondary markets.

Dr. Wang Xin believes that investment and financing are the lifeline of pharmaceutical innovation, and are crucial for promoting research and development and accelerating commercial success in the life sciences industry.

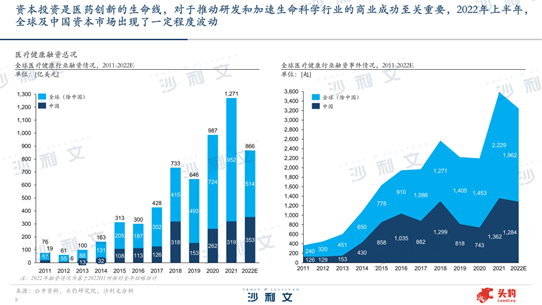

The data shows,2022In the first half of the year, there were certain fluctuations in global and Chinese capital markets. Although overall capital tends to be calm, the tolerance of capital for startups continues to improve, continuing a trend that started in2021The proactive attitude towards financing projects in the early stages of the year. An increasing number of startups with potential and growth potential have received capital support, further developing and growing in the first half of this year. At the same time, under the impact of the pandemic, the number of financing events in the local healthcare industry has decreased significantly due to a low base, while the COVID-19 pandemic has catalyzed the influx of healthcare capital.

From a global perspective, the financing amount in the global healthcare industry is continuously climbing, and global financing rounds are gradually tilting towards earlier stages.2019Global healthcare financing events slightly declined in 2021. However, exceeding1The proportion of large financing events worth hundreds of millions has increased, and funds continue to pour into the healthcare industry, indicating that investment institutions tend to favor high-quality targets with clearer business models and higher stability. The gradual shift of China's healthcare financing rounds towards the future indicates that capital is becoming more rational, favoring mature targets. This also reflects to some extent that investors' risk aversion coefficient is gradually increasing.

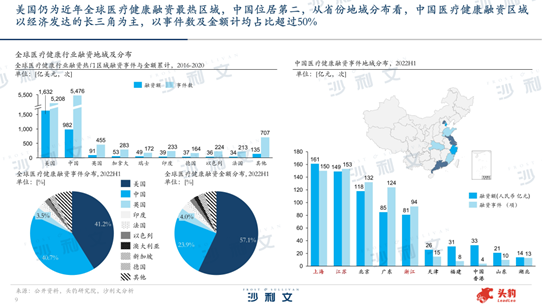

In recent years, the United States has always been the region with the hottest investment and financing in the global healthcare industry, followed by China. In terms of provincial geographical distribution,2022The five regions with the most intensive medical and health investment and financing events in a year are Jiangsu, Shanghai, Beijing, Guangdong, and Zhejiang. In terms of financing events, Jiangsu153The financing event has achieved a reversal of the lead over Shanghai. In terms of financing amount, Shanghai still ranks first nationwide, with the financing amount reaching RMB161Yuan. Apart from Beijing, the popular regions for healthcare financing are mainly in the economically developed Yangtze River Delta, where both the number of events and the amount involved account for more than50%.

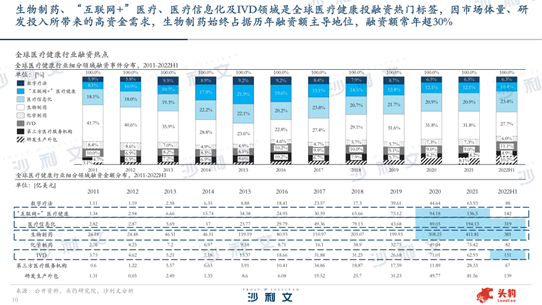

2021In the year, the global biopharmaceutical field totaled880Start trading, with411.81The financing amount of hundreds of millions of US dollars ranks first in the healthcare sub-sector. Biopharmaceuticals, “Internet+"Medical care, medical informatics, andIVDThe domain is a popular tag for global healthcare investment and financing. Among them, Due to the high capital demand brought about by market size and R&D investment, biopharmaceuticals have always dominated the financing amount over the years, with the annual financing exceeding30%.

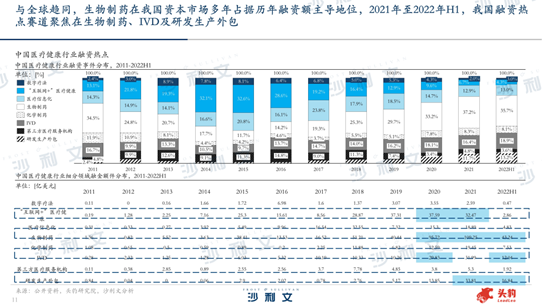

In line with global convergence, biopharmaceuticals have long held a dominant position in the healthcare segment of China's capital market. In addition,IVDR&D and manufacturing outsourcingCDMOAlso highly favored by the capital market.2021Year to2022yearH1In China, the financing hotspots are focused on biopharmaceuticals,IVDAnd R & D and production outsourcing.

As of2021year12month31On the same day, the global equity financing scale reached15,283billions of US dollars, a year-on-year increase24.4%The data shows,2021The global equity financing scale has been steadily increasing, with the Chinese mainland consistently ranking second in recent two years.

Meanwhile, being affected byAThe promotion of the share registration system,2021Domestic for the yearIPO listingThe amount and number of funds raised have reached new highs, compared with Hong Kong stocksIPO listingThe market is more active. In the healthcare sector,2017 - 2021Over the year, the number of listed companies has been on the rise in major global sectors,AShares are highly favored. In ChinaAStock market, healthcare industryIPO listingfinancing scale,IPO listingThe number of enterprises ranks third and fifth among all industries.

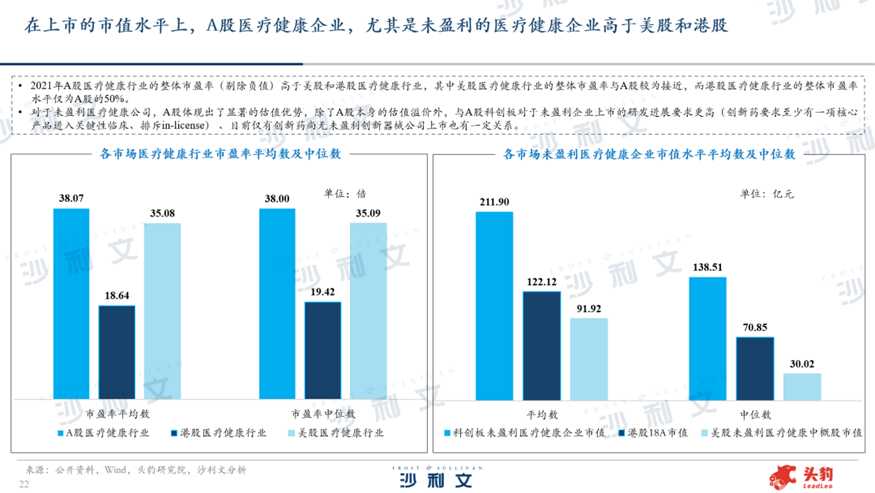

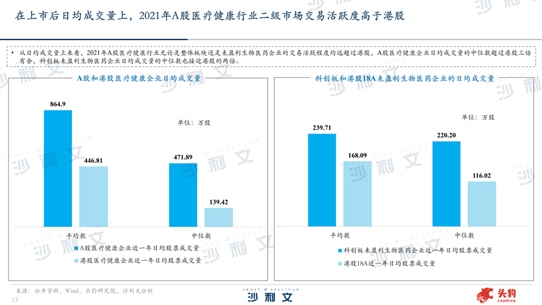

Judging from the listed market value level, 2021yearAThe overall price-earnings ratio (excluding negative values) of the healthcare industry is higher than that of the US and Hong Kong healthcare industries. For unprofitable healthcare companies,AThe stock also demonstrates a significant valuation advantage, in addition toAIn addition to the valuation premium of the equity itself, andAThe Sci-tech Innovation Board has higher requirements for the R&D progress of unprofitable enterprises seeking listing (for innovative drugs, at least one core product must enter pivotal clinical trials and be excludedin-licensee) The current situation, where there are only innovative drugs available for listing without any profitable innovative medical devices, is also related to this. Looking at the average daily trading volume after listing, 2021year AThe trading activity in the secondary market of the healthcare industry is active across both the overall sector and unprofitable biotech companies, far exceeding that of Hong Kong stocks.

projected In the later stage, asAThe full implementation of the share registration system and market policy reforms, in the futureAThe stock market will be more attractive than the Hong Kong market, and more pharmaceutical companies will choose toAThe shares were financed.

"AThe average review days for the Sci-tech Innovation Board and Growth Enterprise Market are300Heavenly Reach374The review cycle is longer compared to Hong Kong stocks and US stocks. After the review phase is completed,AThe registration and declaration of shares still need to pass the issuance review committee/The listing committee meeting process is more complex. Therefore, a professional listing application team will help pre-listing companies better complete their listing application materials and successfully pass the threshold." said Dr. Wang Xin. "Frost & Sullivan integrates global."61Consulting experience for over [X] years, entering China24Over the past year, we have served most of the biopharmaceutical companies listed on the Hong Kong stock market.2019year7Since the first batch of companies on the Sci-tech Innovation Board (STAR Market) went public, many enterprises on the STAR Market have also cited our data and reports.

According to a study by Frost & Sullivan, biotech companies listed on the Sci-tech Innovation Board are mostly concentrated in the pharmaceutical sector. The vast majority of these companies focus on the research and development and production of oncology drugs, autoimmune diseases drugs, and metabolic system diseases drugs. Among the biotech enterprises with a high market value, there are many that specialize in oncology drug research and development. Hong Kong stocks18ABiotechnology companies are involved in pharmaceuticals, medical devices, andAIThe company covers all three major medical fields, with a focus on biopharmaceuticals in the pharmaceutical sector. Medical device companies are concentrated in three sub-sectors: in vitro diagnostics, medical equipment, and medical consumables.

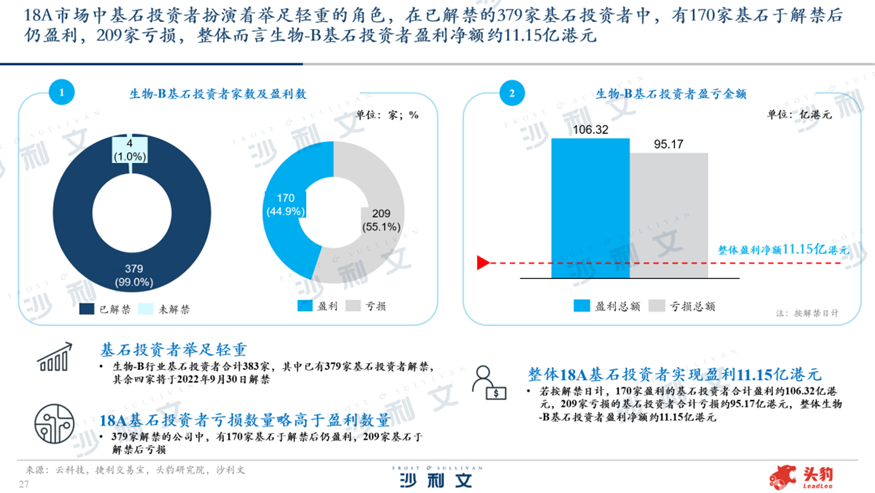

1 8ACornerstone investors play a pivotal role in the market , According to 'TradeGo'APPCornerstone Investor Data, Biology-BTotal cornerstone investors in the industry383home, which already379The investor of Homegrown is lifted from the ban, while the other four will be2022year9month30Daily lifting of restrictions. As of now,379Among the companies whose shares have been lifted from suspension, there are170Homefund, which remains profitable after the lifting of the ban,209Homefund Infrastructure suffered losses after the lifting of the ban.

If calculated based on the lifting date,170The total profit of cornerstone investors contributing to the company's profitability is approximately106.32HK$10 billion,209The combined losses of cornerstone investors with losses at home are approximately95.17HK$10 billion, overall biology-BNet profit of cornerstone investors is about11.15HK$10 billion.

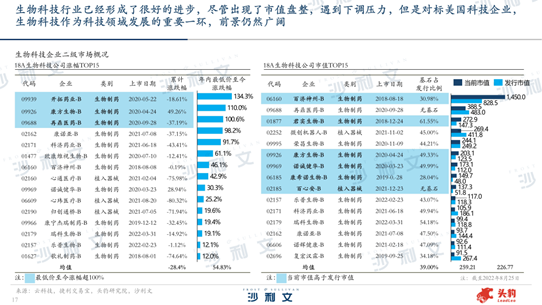

Look around entire18Amarket, According to Frost & Sullivan(shenzhen)Cloud technology data shows, from2022Looking at the data on price changes from the lowest price of the year to date, biology-BOverall increase of about34.54%, increase or decrease in priceTop 15The overall enterprise price rose by about54.83%The rebound strength is acceptable; looking at the cumulative rise and fall data since listing, biotech-BOverall decline37.33%IncreaseTop 15The overall stock market fell28.4%.

Judging from the current market value, As of8month25day18ABiotechnology ranks at the top in market value15For the companies, the average growth rate of their current market value compared to the issue market value is approximately28.1%Among them, the top three companies in terms of market value growth are CanSino Biologics Growth211.9%Baisin'an Growth164.9%, as well as the growth of Junshi Biology85.2%It is worth noting that the current market valueTop 15Among the enterprises, only six currently have a positive growth in market value compared to their initial offering, which means that future issuances18AThe overall issuance valuation of biotech companies will gradually tend towards conservatism, and there may even be cases of discounted issuance.

In terms of the proportion of core assets, 18AMarket value in the biotechnology sectorTop 15The average proportion of the enterprise's cornerstone assets is about39.0%all18AThe weighted average proportion of listed companies in biotechnology is about43.92%Therefore, biology-BIt is also a consensus that companies are looking for a cornerstone, and the proportion is not low accordingly. Of course, there are also those without a cornerstone, currently ranked by market valueTop 15Among2The proportion is relatively small if there are no cornerstones at home. Affected as a whole18AAffected by the biotechnology sector, it can be anticipated that this will continue for some time in the future18ABiotech companies are generally conservative, responding to market conditions in terms of issued market value, and there will not be significant changes in the proportion of cornerstone shares.

In summary, the biotechnology industry has made significant progress. Despite market capitalization consolidation and downward pressure, compared to US technology companies, biotechnology, as an important part of the technological field's development, still has a broad outlook.

Dr. Wang Xin concluded, 'It is not difficult to see from the overall market trend that new drug R&D capability is the only way for biopharmaceutical companies to achieve long-term and rapid development. At present, Chinese innovative pharmaceutical companies are stillMe-too syndromeUnder the 'follower model' dominated by derivative drugs, there has already been a clustering of targets in the market. Only by persisting in high investment in research and development, differentiated operations, and international strategic deployment can one be expected to occupy a high position in the industry.

Finally, Dr. Wang Xin introduced some of the high-quality tracks in China's healthcare industry to the attendees, includingmRNAFields such as domain, cell and gene therapy, smart healthcare, etc. He stated that he believes that driven by factors such as economic growth, policy support, technological progress, and capital assistance, China's health care industry will thrive in the future.