Socially-run Medical Institutions: The Development Summit Forum on Blood Purification

Socially-run Medical Institutions: The Development Summit Forum on Blood Purification

2023year2month8day-9On the day, sponsored by “Health China Observation” magazine and undertaken by the Western Promotion Association of the Zhongguancun Nephropathy and Hemodialysis Innovation Alliance,2023Healthy China-The "Socially Operated Medical Institutions' Hemodialysis Development Summit Forum" was held at the Yanlong Bay Hotel in Sanya City, Hainan Province. The forum focused on hemodialysis technology innovation, the current situation and prospects of socially operated medical institutions providing hemodialysis services, and socially operated nephrology hospitals./The paper conducts an in-depth discussion on four aspects: operational management of dialysis centers, investment and financing in the blood purification industry run by non-governmental organizations.

As a special invitee at the conference, Frost & SullivanFrost & SullivanGuo Jing, Senior Consulting Director of the Healthcare Business Unit at Frost & Sullivan (referred to as 'Frost & Sullivan'), was invited to attend the event and delivered a speech on the current situation and development trends of China's blood purification industry.

Senior Healthcare Industry Consultant, Frost & Sullivan Greater China Guo Jing

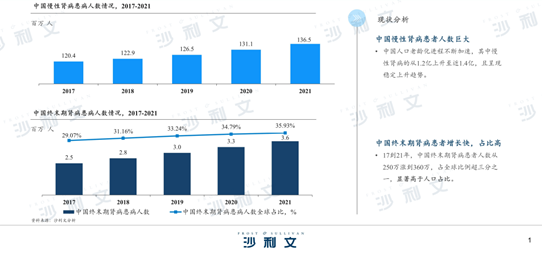

Guo Jing first briefly analyzed the current diagnosis and treatment status of patients with end-stage renal disease in China. Data shows that the number of patients with chronic kidney disease and end-stage renal disease in China is huge, and it is showing an increasing trend. 2017reach2021In [year], the number of end-stage renal disease patients in China decreased from250Ten thousand rises360Ten thousand, accounting for more than one-third of the global proportion, is significantly higher than the proportion of the population. According to Guo Jing, the treatment rate for end-stage kidney disease in China remains low. Considering the course of the disease and accessibility, hemodialysis is currently the main treatment method.

In recent years, although the treatment rate for end-stage renal disease patients in China has been continuously increasing, it is still far lower than that in Europe and America. On one hand, there are fewer hemodialysis centers in China, which is a relatively backward situation compared to developed regions such as Europe and America, accounting for about1/5On the other hand, China's accessibility of healthcare professionals per thousand population is also far lower than that of developed regions such as Greece, Norway, the United States, and Japan.

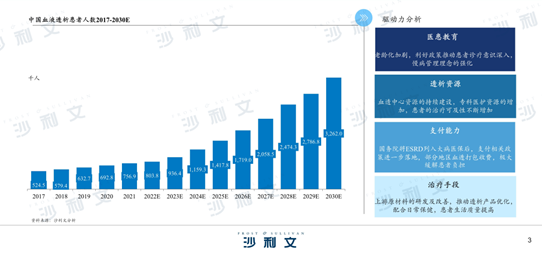

Guo Jing pointed out that there are significant regional differences in hemodialysis conditions in China, with both economic capabilities and the number of dialysis centers jointly affecting the treatment situation for local patients. Research by the Medical Insurance Branch of the Chinese Social Insurance Society indicates that due to the high frequency and persistence of dialysis treatment, the treatment rate for end-stage renal disease among patients in underdeveloped regions is generally lower than that in developed regions. In the future, improvements in multiple factors such as education, dialysis resources, affordability, and treatment methods will strongly drive the continuous growth in the number of dialysis patients in China.

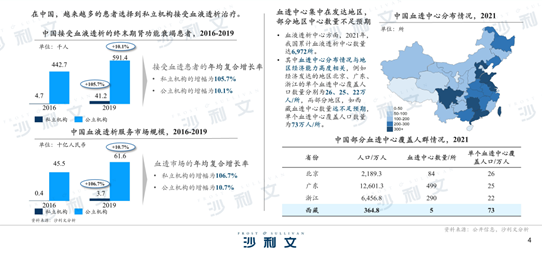

According to a study by Frost & Sullivan, current hemodialysis services in China are still dominated by public institutions. However, an increasing number of patients are choosing private institutions for hemodialysis treatment. Both the number of patients receiving hemodialysis at private institutions and the market size of these institutions have shown significant growth.

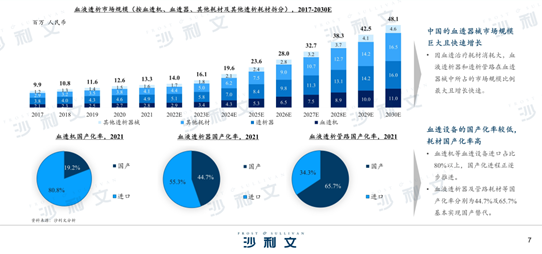

In addition, hemodialysis services have strong regional characteristics, and the patient coverage across the country is not balanced.2021In [year], the cumulative number of hemodialysis centers in China reached6,972Among them, the distribution of hemodialysis centers is highly correlated with regional economic capabilities. For example, in economically developed regions such as Beijing, Guangdong, and Zhejiang, the number of people covered by a single hemodialysis center is26,25,22ten thousand/Therefore, in some areas, such as Tibet, the number of hemodialysis centers is far from meeting expectations, with each center covering a population of73ten thousand/there

"The base number of patients with end-stage renal disease in China is large, the demand for hemodialysis is high, and there is broad market space," Guo Jing further added, 'However, due to reasons such as overloaded operations of public hospitals and uneven quality among private institutions, the hemodialysis treatment rate in China is relatively low. There is a high market demand with a large gap, and at present, there has not yet been a scale effect. The market needs to be improved and matured, and the existing hemodialysis demand needs to be released; In the future, driven by multiple policy factors, it is expected that China's hemodialysis service market will accelerate its development in the direction of resource accessibility, specialized teams, standardized management, centralized players, and chain layout. "

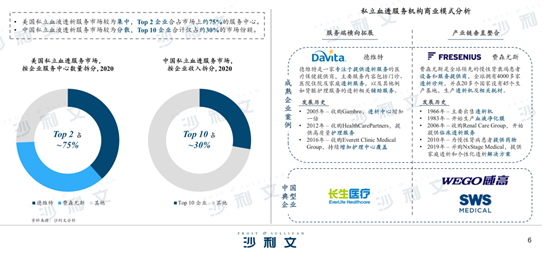

Data shows that the private hemodialysis service market in the United States is relatively concentrated.Top 2Enterprises jointly occupy about75%The service centers are located in [specific locations]; the private hemodialysis service market in China is relatively fragmented.Top 10The enterprise accounts for only about30%Market share. Guo Jing used Dwebet and Fresenius as examples to analyze the business models of two private hemodialysis service institutions, namely, horizontal expansion of services and vertical integration of the industrial chain, to the guests present. She believes that for hemodialysis service providers, exploring more diversified business models is also an important way to bring about sustained revenue growth and profitability.

"In addition, with the expansion of service market demand, upstream pharmaceutical and medical device R&D and production will also be an important direction for future market development," said Guo Jing. Due to the high consumption of consumables for hemodialysis treatment, hemodialyzers and dialysis tubing account for the largest market share among hemodialysis devices and are growing rapidly. At the same time, the proportion of imported hemodialysis equipment such as hemodialysis machines80%As mentioned above, the localization process is being gradually advanced; The localization rates of hemodialysis machines and tubing consumables are as follows:44.7%and65.7%It has basically achieved domestic substitution.

Guo Jing stated that it is expected that the future development of the hemodialysis device market will possess the following characteristics:

(1) Accelerated localization: Domestic devices have a price advantage, policy support, and technological innovation that drive up the localization rate;

(2Membrane technology R&D: Reduce protein adsorption, lower immune response, and improve biocompatibility;

(3Intelligent development: Standardized and automated functions, intelligent monitoring system, reduced failures, saved clinical time, and improved treatment outcomes;

(4) Industry concentration increases: Driven by volume-based procurement, production capacity is centralized, enhancing the competitiveness of leading enterprises.

About Frost & Sullivan's Healthcare Practice

The Healthcare Practice of Frost & Sullivan has professional analytical capabilities and extensive project experience in the life sciences field. Leveraging the global think tank resources of Frost & Sullivan and its cross-industry business development platform in Greater China, Frost & Sullivan Healthcare has unique core advantages in healthcare industry investment and financing services. Frost & Sullivan Healthcare has a wide range of corporate clients in China and in the past20In the year, a vast customer network was established, and a wealth of project experience in various medical sub-fields was accumulated.

Project types include Knowledge Center projects (in-depth content, promotional activities).Pre-IPO financingprojectDCF modelValuation, Business Plan Services),IPO listingWe provide listed projects (industry consulting, clinical audits, fundraising and investment writing), market research, market value management, and strategic consulting. We also cooperate with well-known domestic and international information platforms and investment and financing institutions to offer one-stop solutions for enterprises in specialized sub-sectors such as pharmaceuticals and medical devices. Our services have received wide attention from investors.

Recent Activities