Hong Kong stock subscriptionKOL (Key Opinion Leader)carnival

1month12On the 1st, hosted by TradeGo2023 - 2024Hong Kong stock subscriptionKOLThe carnival has come to a successful conclusion. This year's carnival featured “new sharesFINIThe platform held a new issue launch event themed "New Opportunities for Investors" ” and invited industry heavyweight figuresKOLGuests shared their investment experiences, insights over the years, as well as current investment opportunities.

Frost & SullivanFrost & SullivanYang Xiaocheng, Partner and Managing Director of Frost & Sullivan's Greater China Region, was invited to attend and delivered a presentation on2023Hong Kong stocks for the yearIPO listing"Research Review and Analysis of Popular Tracks" was presented for sharing.

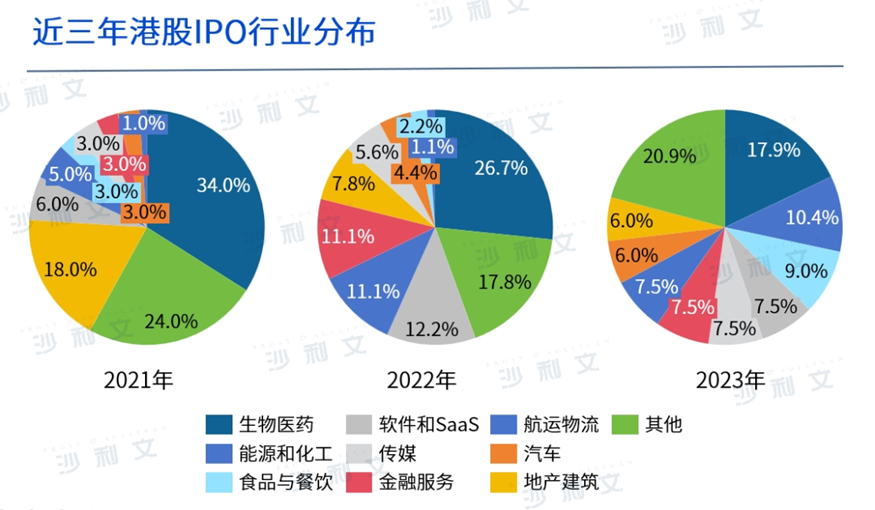

Yang Xiaocheng pointed out, from Hong Kong stocksIPO listingIn terms of industry distribution, Hong Kong stocks over the past three yearsIPO listingThere have been changes in the industry structure.

Among them, biomedicine in the overall Hong Kong stock marketIPO listingIt continues to rank first in industry distribution, however its proportion has been declining year by year, from2021year34.%reduce to2023year17.9%In contrast, energy and chemicals, food and catering, and software andSaaSThe industry proportion has been significantly enhanced, rising from2021year1.0%,3.0%and6.0%Grew to2023year10.4%,9.0%and7.5%. in2021Among the industries with a high proportion ranking, the real estate construction industry's proportion has seen a significant decline in the past three years, from2021year18.0%Falling to2023year6.0%.

Source: Analysis by Frost & Sullivan

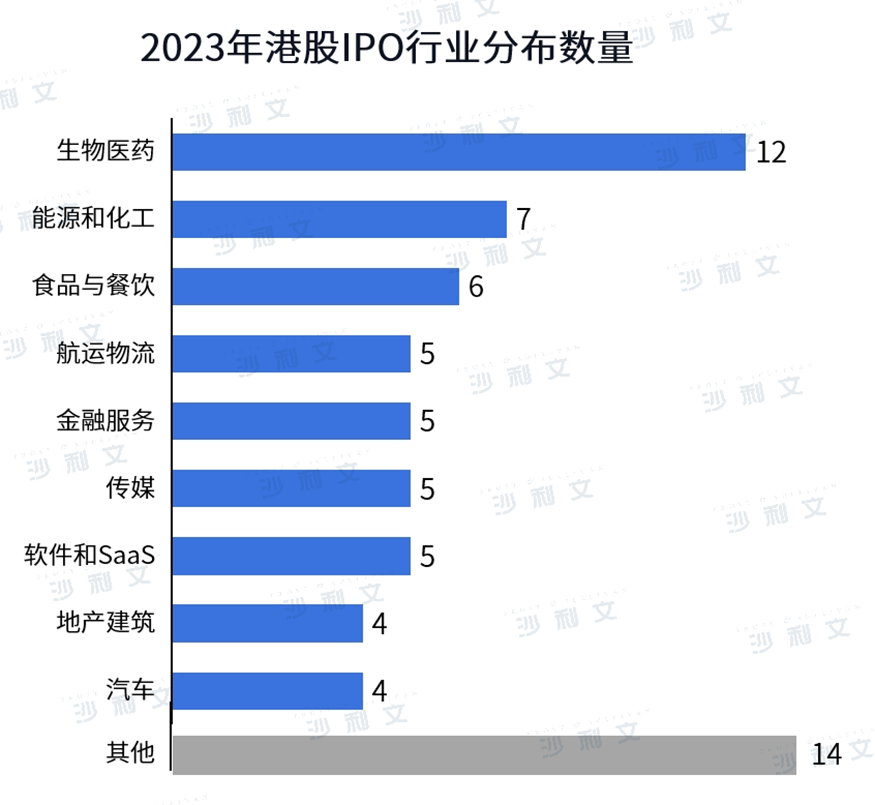

Data shows that compared with the past two years,2023Hong Kong stocks for the yearIPO listingThe quantity decreased slightly, as of2023At the end of the year, the number of newly listed companies reached73Home. Among them, looking at the industry track distribution of companies listed on the Hong Kong Stock Exchange, the top three industries in terms of proportion are biomedicine, energy and chemicals, and food & catering. Among these industries, those that have successfully gone public in Hong KongIPO listingListed companies include Wuhan Biomarker, Neusoft Xikang, Pharmacist Assistant, Jinyuan Hydrogen Energy, and Fourth Paradigm, among others.

Source: Analysis by Frost & Sullivan

Subsequently, Yang Xiaocheng covered Hong Kong stocks in biomedicine, medical aesthetics, food & catering, automotive and technology sectors respectivelyIPO listingA brief analysis of popular tracks has been conducted.

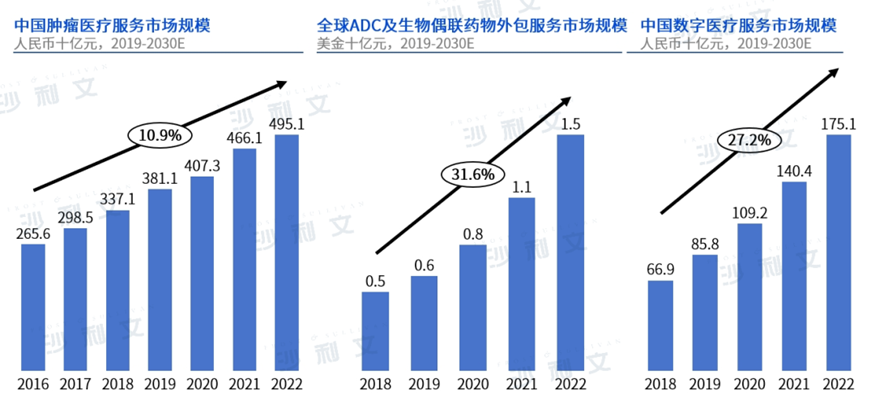

2023Biopharmaceutical companies listed in Hong Kong each year are in the fields of oncology medical services,ADCAnd broader biologics outsourcing services and digital healthcare services, etc. With the continuous release of demand for cancer treatment, it will drive further growth in China's oncology medical service market. Calculated by revenue, the scale of China's oncology medical service market is from2016year2,656RMB billion growth to2022year4,951Yuan. In addition, based on the globalADCRapid growth in pharmaceutical sales2022GlobalADCAnd the market value of broader bioconjugation drug outsourcing services reaches15Billions of dollars. The digital healthcare service market in China has developed rapidly in recent years,2022In China, the scale of the digital healthcare service market reached RMB1,751100 million yuan.

Source: Analysis by Frost & Sullivan

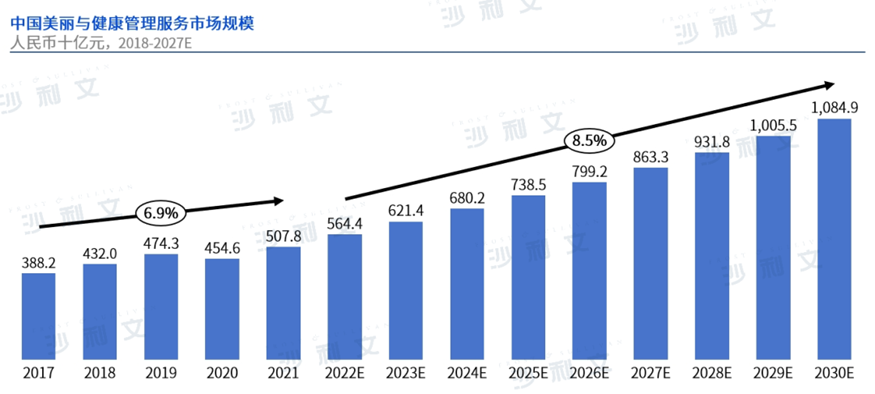

2023The medical beauty companies listed in Hong Kong each year mainly consist of sub-sectors such as traditional beauty services and non-surgical medical beauty services. The total revenue of the traditional Chinese beauty service market is composed of2017Renminbi in [year]3,451RMB10 billion grew to2021Renminbi in [year]4,032Yuan, with an annual compound growth rate of4.0%The total revenue of China's non-surgical medical beauty service market has risen from2017Renminbi in [year]401RMB billion growth to2021Renminbi in [year]977Yuan, with an annual compound growth rate of24.9%The total scale of China's beauty and health management service market is2017Renminbi in [year]3,882RMB billion growth to2021Renminbi in [year]5,078Yuan. Estimated2030RMB will reach1,084.9100 million yuan.

Source: Analysis by Frost & Sullivan

at2021 - 2023Between January and December, Chinese catering companies listed in Hong Kong included segments such as packaged food and beverages, fresh produce, fruits, ready-to-eat dishes, and chain restaurants. The consumption of leisure food in China has been steadily growing over the past few years, with an explosion of online and offline retail channels across the country. Due to the increase in per capita disposable income and the diversification of consumer preferences, the market size of leisure food in China has grown from2016Renminbi in [year]6,277RMB 10 billion grew to2021Renminbi in [year]7,961yuan, with a compound annual growth rate of4.9%The growth of China's catering industry is mainly driven by the improvement of disposable income, urbanization level, penetration of dining out and takeout services, as well as improved food safety and a favorable regulatory environment. Driven by these development drivers, the revenue scale of China's catering industry has from2016Renminbi in [year]35,799RMB billion growth to2019Renminbi in [year]46,721100 million yuan.

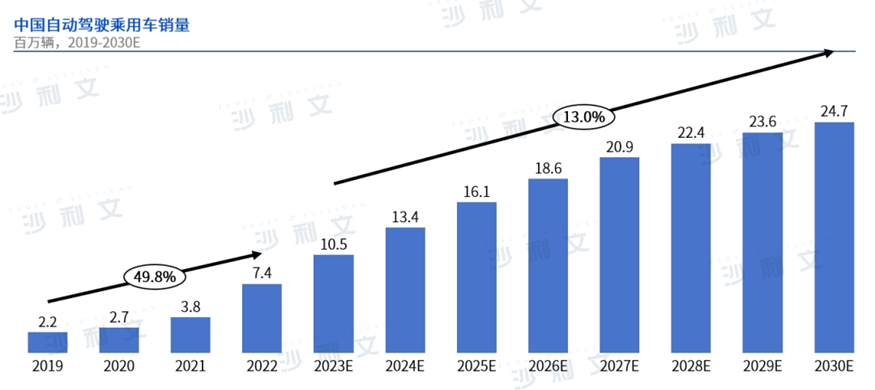

Autonomous driving is a hot investment area in the automotive sector at present. As a key development technology in the passenger vehicle industry, the market scale of autonomous driving has been increasing year by year. This is mainly driven by factors such as increased consumer acceptance, more affordable autonomous driving solutions, and advancements in autonomous domain controller research and development technology. It is expected that by2026Global sales of autonomous passenger vehicles will reach42.2One million units, penetration rate56.8%, to2030Will reach in60.6One million units, penetration rate78.3%At the same time, it is expected that by2026In China, the sales volume of autonomous passenger vehicles will reach18.6One million units, penetration rate reaches73.5%, to2030Annual achievement24.7One million units, penetration rate reaches92.7%.

Source: Analysis by Frost & Sullivan

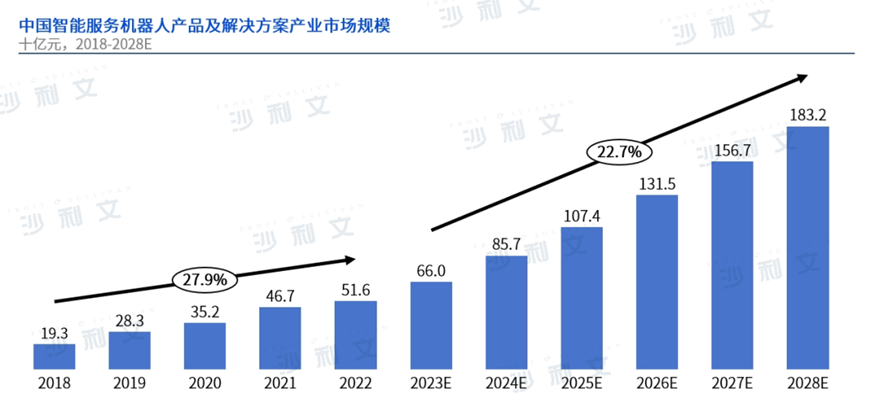

2023In the year 2023, the Hong Kong stock market welcomed the 'first humanoid robot' BYTON. Currently, market participants in China's intelligent service robot and intelligent service robot solutions industry have begun to gather and exhibit synergies. Anticipated cutting-edge artificial intelligence technologies will significantly impact the development of China's intelligent service robot and intelligent service robot solution markets in the coming years, exploring diversified application scenarios.2022Year-end2028In [year], the market scale of intelligent service robots and intelligent service robot solutions in China will reach RMB1,832yuan, with a compound annual growth rate of23.5%.