2025 Economic Outlook Conference

On February 14, 2025, the Zhuhai Shanwei Chamber of Commerce grandly hosted the "2025 Economic Outlook Conference and Tungsten Industry Chain Industry Analysis Conference" at the Renheng InterContinental Hotel in Zhuhai. The conference gathered elites from government, enterprises, academia, representatives of friendly business associations in the Guangdong-Hong Kong-Macao Greater Bay Area, and industry professionals to explore new drivers for economic development, discuss new economic trends, and empower new industrial development.

Lou Lei, Executive Director of Frost & Sullivan's Greater China region, was invited to attend the event and analyzed the development trend of the entire tungsten industry chain from an industry perspective.

Lou Lei stated that tungsten is a rare metal widely used in communication electronics, machinery manufacturing, aerospace, optoelectronics, military industry, and other fields due to its high hardness and melting point. Due to the global scarcity of tungsten resources, their irreplaceability in industrial applications, and their increasing importance in national economy, national defense construction, and high-tech industries, its strategic position is very prominent.

Lou Lei, Executive Director of Frost & Sullivan's Greater China region

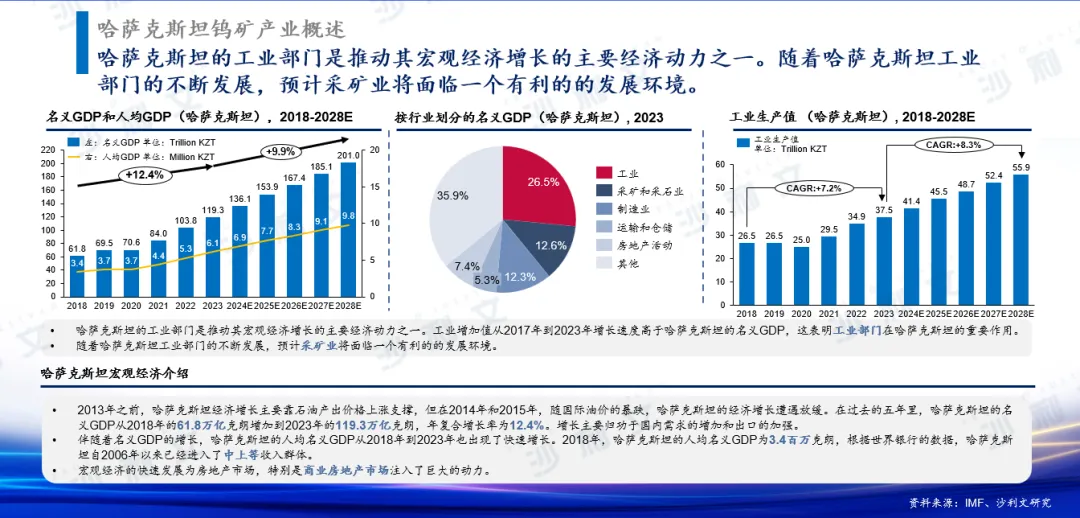

Lou Lei pointed out that the distribution of tungsten ore resources around the world is uneven, with major tungsten deposits mainly located in the Circum-Pacific mining belt, followed by the Mediterranean and European regions along the Atlantic coast, with a small portion scattered in the hinterlands of Asia, Europe, America, and Africa. Kazakhstan is located in Central Asia and is the world's largest inland country, with an economy mainly based on oil, natural gas, mining, coal, and agriculture and animal husbandry. Its processing industry and light industry are relatively backward, and most daily consumer goods rely on imports. It has very rich natural resources and a relatively complete range of mineral types. Kazakhstan's industrial sector is one of the main economic drivers for its macroeconomic growth. With the continuous development of Kazakhstan's industrial sector, it is expected that the mining industry will face a favorable development environment. In addition, the joint construction of the "Belt and Road" has injected new vitality into China-Kazakhstan cooperation, promoted changes in Kazakhstan's economic policies, continuously raised bilateral relations to new heights, and deepened and solidified cooperation in various fields such as politics and economy, benefiting the people of both countries.

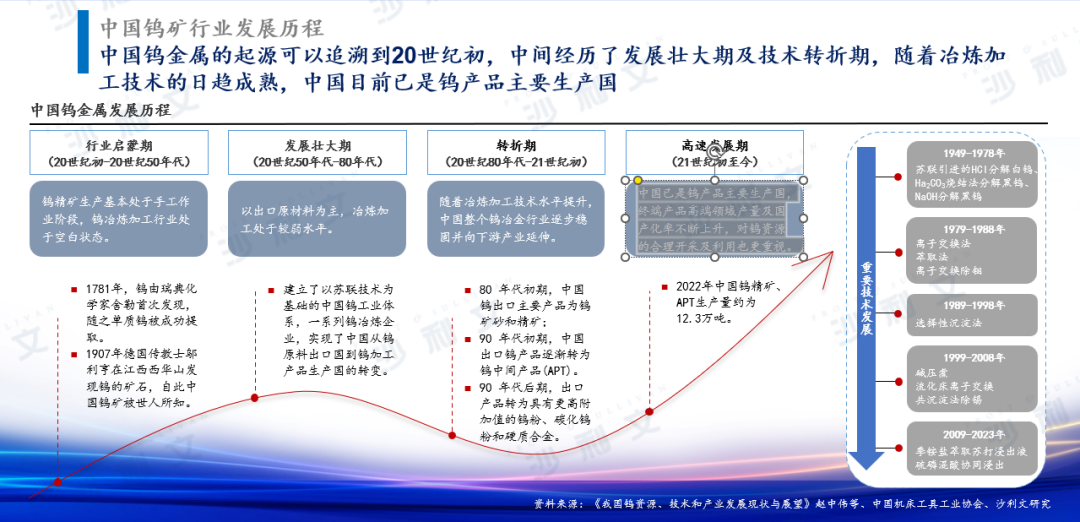

He said that the origin of tungsten metal in China can be traced back to the early 20th century, going through four development periods, including:

-

Industry Enlightenment Period (early 20th century - 1950s): Tungsten concentrate production was basically manual, and the tungsten smelting and processing industry was in a blank state.

-

Growth Period (1950s - 1980s): Mainly exporting raw materials, with relatively weak smelting and processing levels.

-

Turning Point (1980s - early 21st century): With the improvement of smelting and processing technology levels, China's entire tungsten metallurgy industry gradually stabilized and extended downstream.

-

High-Speed Development Period (early 21st century to present)China has become a major producer of tungsten products. The output and localization rate of high-end products are continuously rising, and more attention is paid to the rational exploitation and utilization of tungsten resources.

With the increasing maturity of smelting and processing technology, China is currently a major producer of tungsten products.

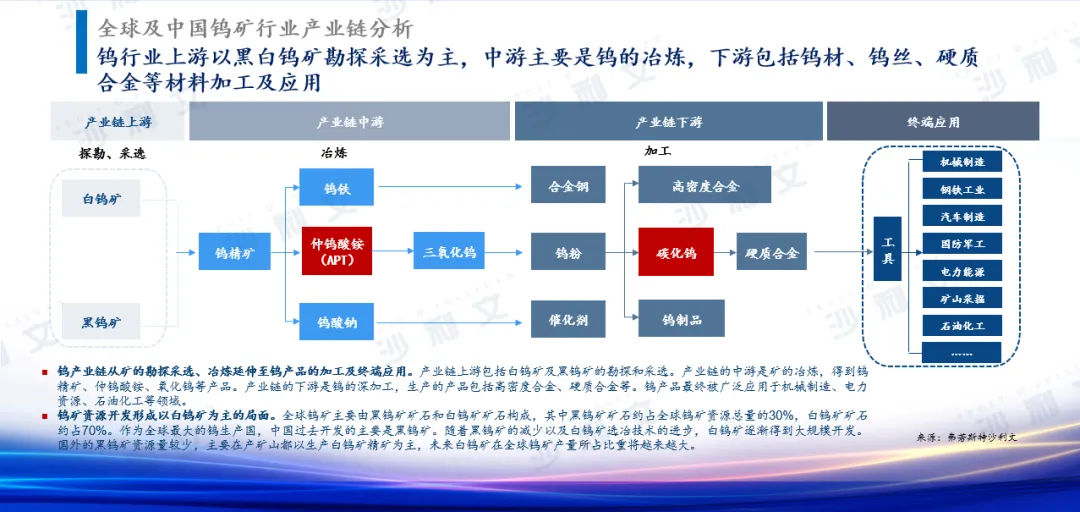

The tungsten industry chain extends from ore exploration and beneficiation, smelting to the processing and end application of tungsten products. The upstream of the industry chain includes the exploration and beneficiation of white tungsten ore and black tungsten ore. The midstream of the industry chain is ore smelting, producing products such as tungsten concentrate, ammonium tungstate, and tungsten oxide. The downstream of the industry chain is deep processing of tungsten, producing products including high-density alloys and cemented carbide. Tungsten products are ultimately widely used in machinery manufacturing, power resources, petrochemicals, and other fields.

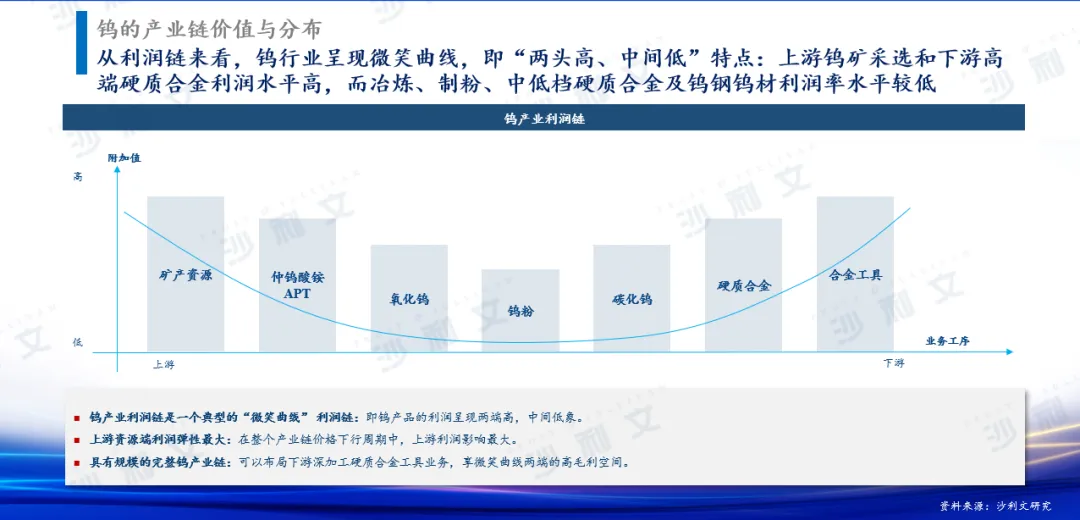

From the perspective of the profit chain, the tungsten industry shows a smile curve, characterized by "high at both ends and low in the middle": the profit levels of upstream tungsten ore exploration and beneficiation and downstream high-end cemented carbide are high, while the profit margins of smelting, powder production, medium and low-grade cemented carbide, and tungsten steel and tungsten materials are relatively low.

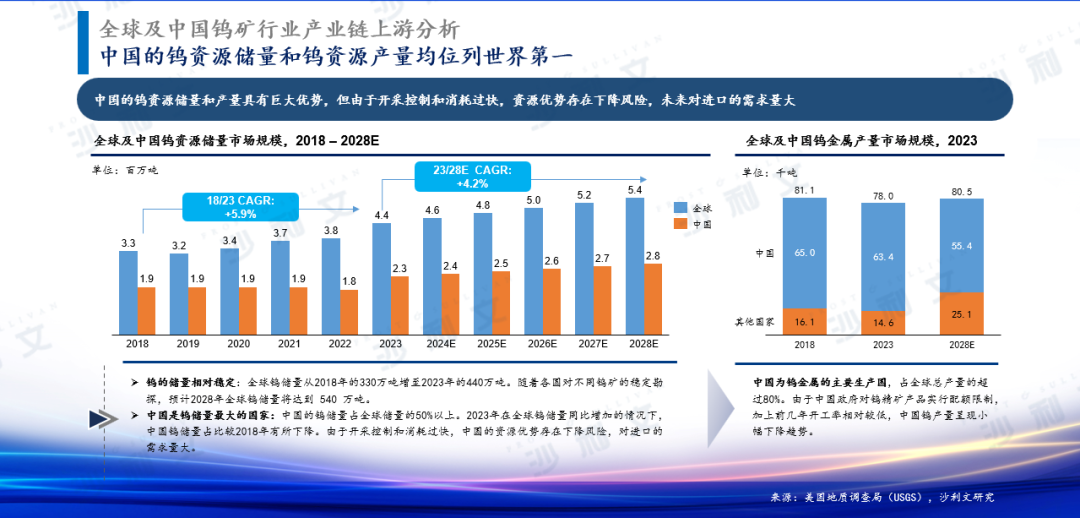

Through the analysis of the upstream of the global and Chinese tungsten ore industry chains, it is found that China is the main producer of tungsten metal, accounting for more than 80% of the global total output. China's tungsten resource reserves and production rank first in the world. However, due to the Chinese government's quota restrictions on tungsten concentrate products and the relatively low operating rate in previous years, China's tungsten production has shown a slight downward trend, with a large future demand for imports.

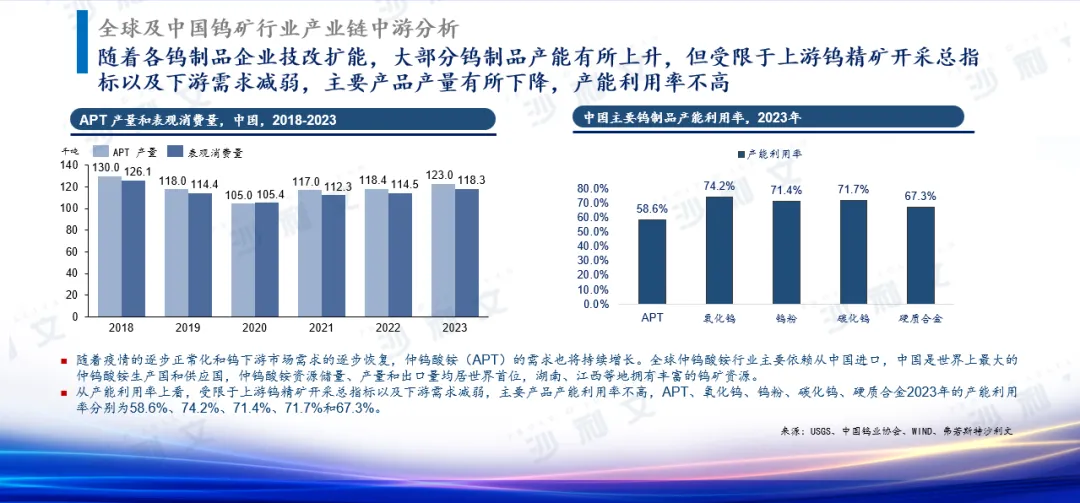

Through the analysis of the midstream of the global and Chinese tungsten ore industry chains, it is found that with the technological transformation and capacity expansion of tungsten product enterprises, most tungsten product production capacity has increased. However, limited by the total quota for upstream tungsten concentrate mining and weakened downstream demand, the output of major products has decreased, and the capacity utilization rate is not high.

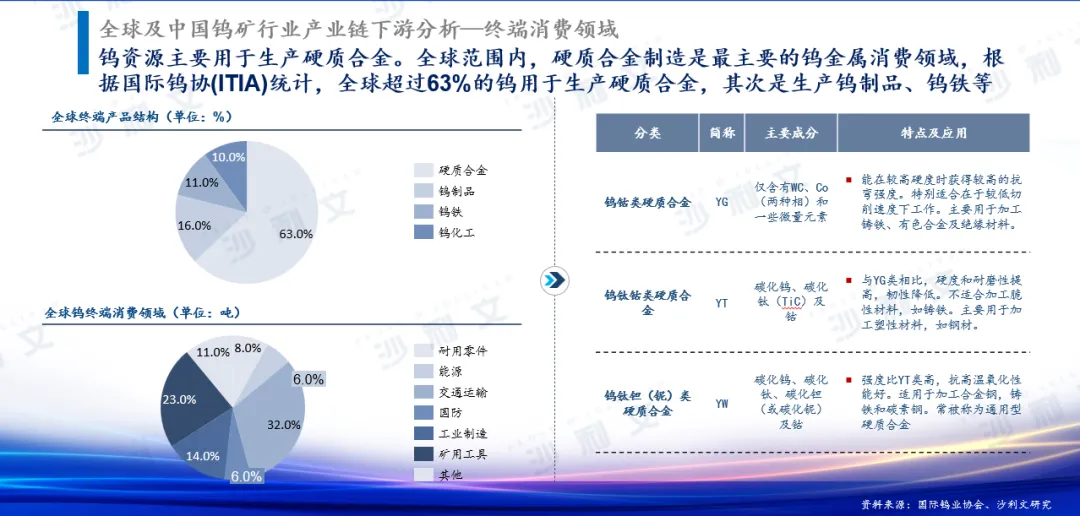

Through the analysis of the downstream of the global and Chinese tungsten ore industry chains, it is found that tungsten resources are mainly used for the production of cemented carbide. Globally, cemented carbide manufacturing is the main consumption field for tungsten metal. According to statistics from the International Tungsten Association (ITIA), more than 63% of the world's tungsten is used for cemented carbide production, followed by the production of tungsten products, ferrotungsten, etc.

Specifically analyzing the end consumption fields of the tungsten ore industry, the largest downstream application field of cemented carbide is cutting tools. Cemented carbide cutting tools have important applications in the field of metal cutting machine tools. National policies strongly support the development of high-end CNC machine tools, thereby increasing the demand for cemented carbide. China's newly installed photovoltaic capacity has continued to grow rapidly in multiple rounds, with the growth rate reaching 148.1% in 2023, and tungsten wire is also the most mature alternative solution for high-carbon steel wires at present.

Finally, Lou Lei said that looking back at human history, mineral resources are an important material foundation for the progress and economic development of human society. The advancement of new materials and cutting-edge technologies such as high-tech, aerospace, electronic information, nuclear energy, and new energy today cannot be separated from the development and utilization of mineral resources, and tungsten ore resources play an important role. Due to the global scarcity of tungsten resources, their irreplaceability in industrial applications, and their importance in national economy, national defense construction, and high-tech industries, its strategic position is very prominent. It is an indispensable strategic resource in national economy and national defense construction, thus attracting increasing attention from various countries. The tungsten ore industry will show the following four main development trends:

First,Increase investment in tungsten ore exploration, pay attention to black tungsten ore, and at the same time improve the beneficiation technology and process of white tungsten ore: The proportion of white tungsten ore is increasing, and due to over-mining, the decline in tungsten resources is very obvious. In recent years, thanks to continuous investment in exploration, the future development trend of tungsten ore will continue with high investment in tungsten ore exploration, especially focusing on high-grade and easy-to-mine black tungsten ore;

Second,Achieve green development of tungsten smelting: Research, promote, and apply new efficient and green tungsten smelting process technologies, as well as comprehensive utilization technologies for tungsten slag and heavy metal pollution prevention and control technologies, to prevent and reduce the generation of hazardous waste from the source; accelerate the digitalization, automation, intelligence of production processes of tungsten smelting enterprises, and the informatization construction of enterprise management to promote the green and high-quality development of the tungsten smelting industry;

Third,Enhance the control of tungsten resourcesSince 2002, through standardizing the approval management of tungsten resource exploration and mining, strengthening the supervision of total mining volume, curbing the disorderly expansion of tungsten ore exploration and beneficiation capacity, improving the contradiction of market supply exceeding demand, slowing down the consumption rate of tungsten resources, and achieving remarkable policy results. Although there are still areas where the implementation effect of the total tungsten ore mining volume control indicators is not satisfactory, it has played an important role in stabilizing market supply, protecting the ecological environment, and maintaining resource advantages;

Fourth,Accelerate the transformation and upgrading of the industry:The intensity of tungsten ore mining in the upstream of the tungsten industry chain is high, the overcapacity of tungsten smelting in the midstream is large, the overcapacity of medium and low-end processing capacity in the downstream is large, the competitiveness and profitability of products are relatively low, the coordinated development of the tungsten industry chain and region is unbalanced, the industrial concentration degree and capacity utilization rate are low, and the overall competitiveness of the industry is not strong. Organizing core technology research and development for high-end tungsten products, improving product research and development capabilities, and expanding the application of tungsten in fields such as aerospace, national defense military industry, nuclear energy, integrated circuits, 5G mobile communication, rail transit, high-end equipment manufacturing, precision processing, etc. is the future development direction.