As a strategic partner of the forum, Frost & Sullivan (referred to as 'Frost & Sullivan') jointly released the 'White Paper on the Global Pharmaceutical and Healthcare Industry Layout and Development Trends' with the Organizing Committee of the Boao Forum for Asia Global Health Forum at the industry report launch event on April 21. Dr. Wang Xin, a global partner at Frost & Sullivan and President of Greater China, provided an in-depth interpretation of the report.

Dr. Wang Xin, Global Partner and President of Frost & Sullivan Greater China, and Professor Wang Yu, Expert Advisor to the Boao Forum for Global Health and a representative of the co-publishing party, jointly participated in the report release ceremony.

Dr. Wang Xin stated that through observation and analysis of the global pharmaceutical and healthcare industry, Frost & Sullivan believes that the industry is currently facing three major challenges.

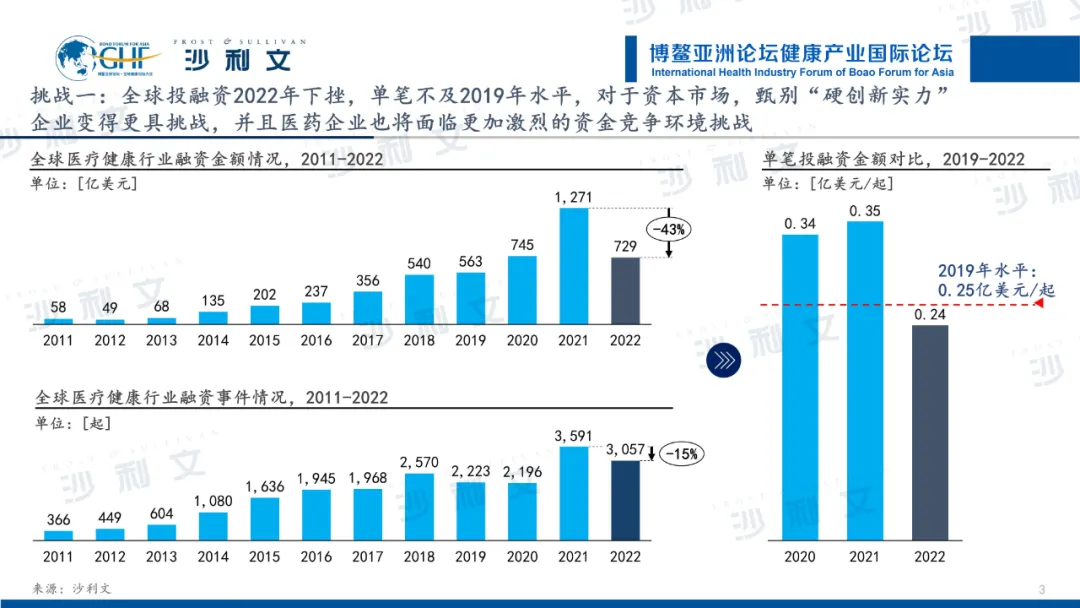

The first challenge comes from the external funding environment.Since 2022, due to factors such as geopolitical conflicts, energy shortages, the COVID-19 pandemic, and high inflation, the global healthcare industry capital market has seen a significant decline. In 2022, there were a total of 3,057 financing events in the global healthcare industry, a 43% decrease compared to 2021, indicating an overall trend towards calmness and prudence.

In terms of total financing, the amount in 2022 was $729 billion, a 15% decrease from 2021, approaching the level of 2020. Nevertheless, the capital structure in 2022 was significantly different. Compared to the obvious clustering of funds in 2020, capital was more rational. In 2022, investors' strategies tended to favor more certain high-quality targets, and the number of financing enterprises participating and the amount they could raise were both decreasing.

Dr. Wang Xin stated that investment and financing are the lifeline of pharmaceutical innovation and are crucial for promoting the success of R&D and commercialization in healthcare enterprises. For capital markets, identifying 'hard innovation capability' enterprises has become more challenging, and pharmaceutical companies will also face more intense competition for funds.

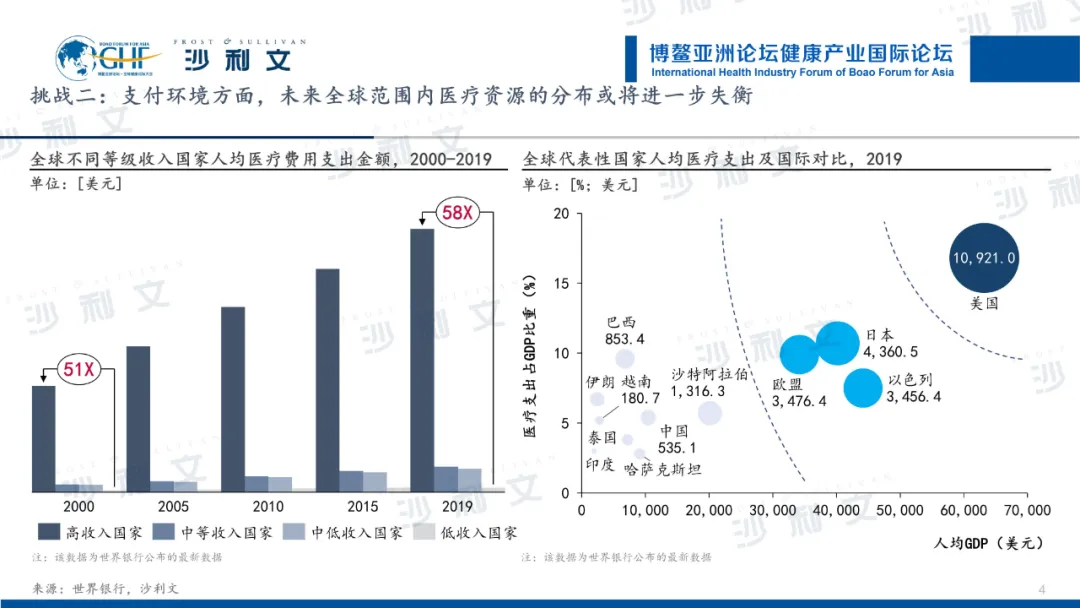

The second challenge is in the payment environment.From the perspective of income levels, the gap in per capita medical expenditure among countries with different income levels has further widened. The disparity between high-income and low-income countries has increased from 51 times in 2000 to 58 times in 2019. Looking at specific economies, a clear bipolar distribution has gradually formed globally. The per capita medical expenditure in wealthy countries is much greater than that in low-income countries. For example, in 2019, the per capita medical expenditure in the United States was about 20.4 times that of China and 60.4 times that of Vietnam.The distribution of global healthcare resources is positively correlated with regional economies. In developed regions, high healthcare expenditures enable patients to receive more advanced treatments in terms of medical health. In low-income areas, it is more about maintaining basic essential medicines and medical services. It is expected that the distribution of healthcare resources worldwide may become even more imbalanced in the future.

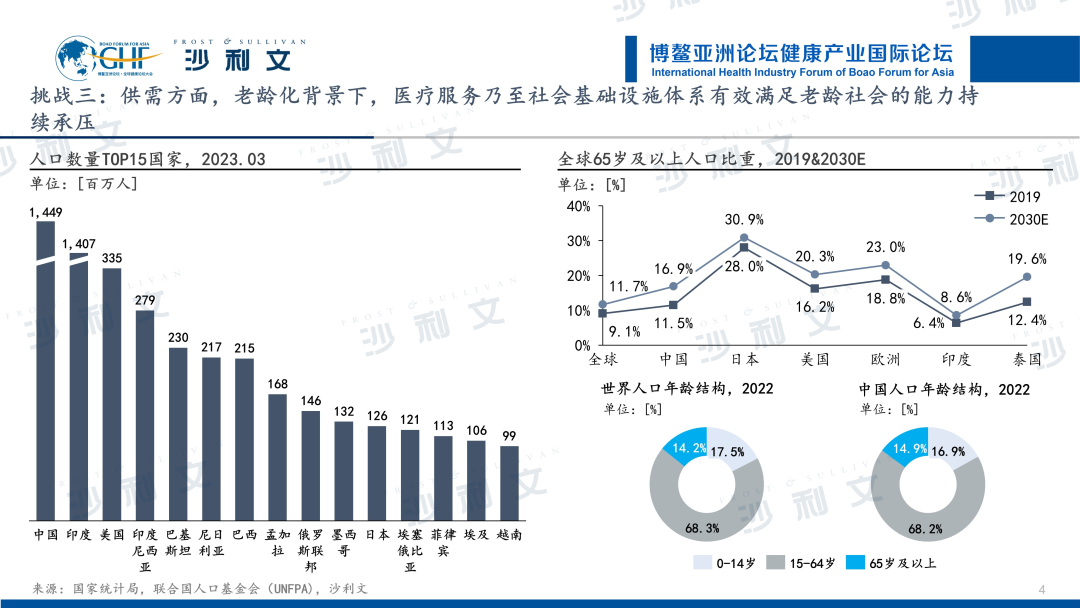

The last challenge comes from supply and demand.Driven by factors such as urbanization development, improved medical standards, and gradually extended human lifespan, the world's population is growing at a rapid rate. Population aging has become an inevitable trend in global population development, with a particularly significant acceleration in developing countries. The deepening degree of population aging means that the future demand side will have higher demands for medical and health services in terms of quantity and quality. Therefore, healthcare services and even social infrastructure systems, which were previously targeted at the young population, will find it difficult to effectively meet the severe diagnostic and treatment needs brought about by the aging society.

"Despite the global pharmaceutical and healthcare industry facing a series of risks and challenges, our research has still identified highlights in different segments of the industry," said Dr. Wang Xin.

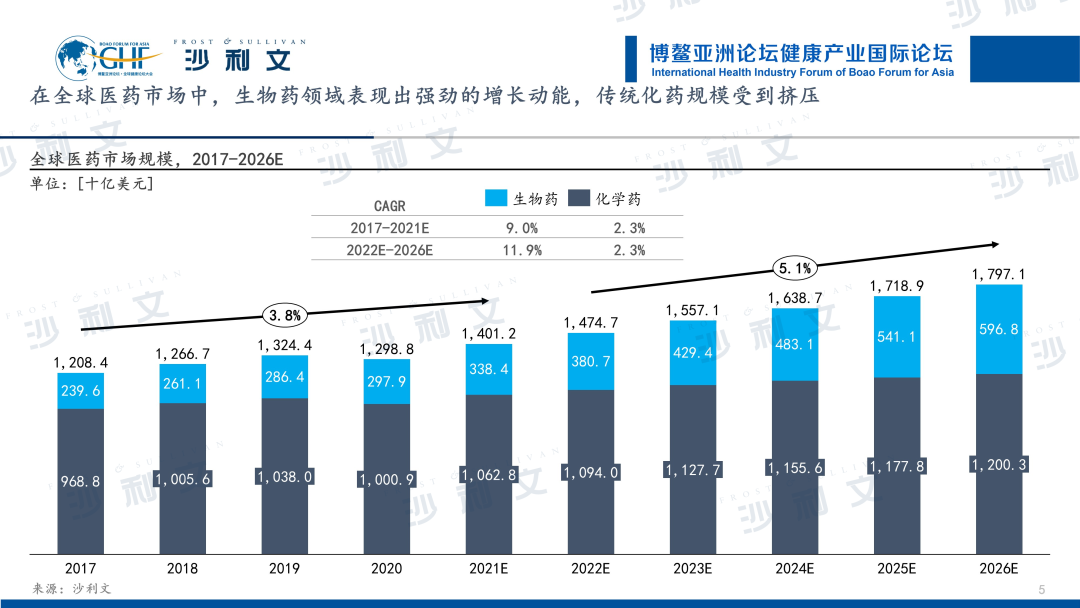

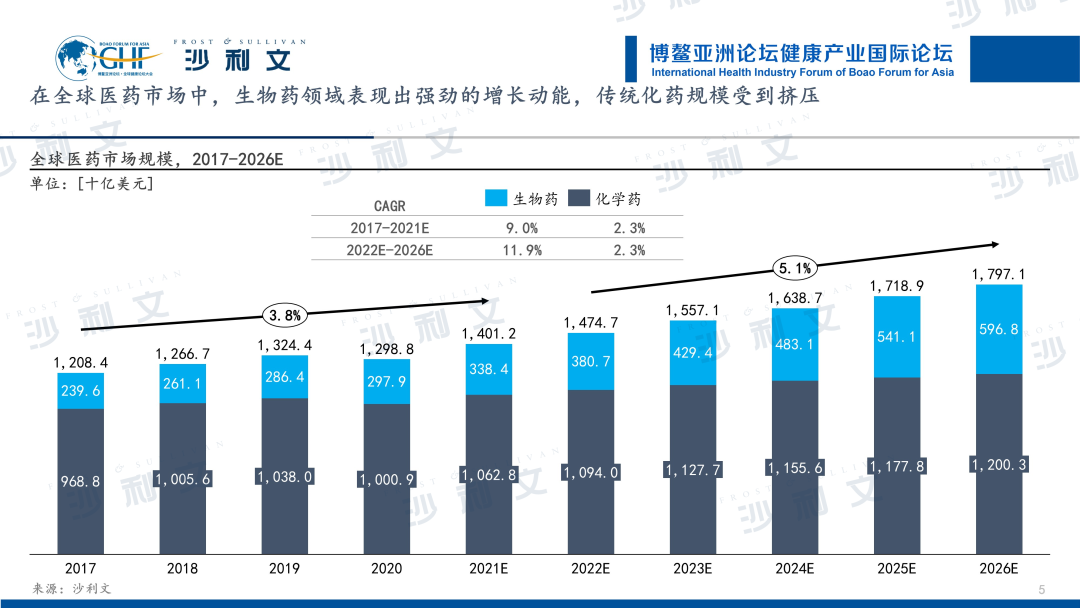

Looking at the global pharmaceutical market, the biopharmaceutical sector has shown strong growth momentum, while the scale of traditional drugs has been squeezed.Data shows that the global pharmaceutical market size grew from $1.2 trillion in 2017 to $1.4 trillion in 2021, with a CAGR of about 3.8%. It is expected to reach $1.8 trillion by 2026, with the global pharmaceutical market maintaining stable growth.Looking at the two types of drugs in the pharmaceutical market, biologics have a completely new therapeutic concept compared to chemical drugs. They provide new ideas for treating difficult and complicated diseases such as cancer and psoriasis, and currently their growth rate is much higher than that of chemical drugs.In the future, driven by factors such as enhanced efficacy of biologics, development of biotechnology, increased R&D investment, and continuous approval of biologics, the compound annual growth rate of global biologics is expected to be 11.9% from 2022 to 2026, still significantly leading over the 2.3% growth rate of chemical drugs.

Looking at the major economies, the United States occupies a world-leading position in biomedicine and its industrialization, with the biomedicine industry becoming one of the core drivers of high-tech industry development in the US.The biopharmaceutical industry is an emerging technology-intensive industry in the United States and a pillar of its economic development, exerting a significant influence. As of June 10, 2022, according to market capitalization divided into $50 billion and $10 billion segments, there are 11 companies with a market capitalization of over $50 billion, accounting for 2.6% of the number of companies in the US biopharmaceutical sector, but they account for 84.9% of the market capitalization. There are a total of 8 companies with a market capitalization between $10 and $50 billion, accounting for about 7.1% of the market capitalization. The top 39 companies with a market capitalization of over $10 billion only account for 4.5% of the number of companies in the US biopharmaceutical sector, with a total market value reaching $2.3 trillion, accounting for 92.1% of the biopharmaceutical sector's market capitalization.

In terms of regional distribution, global biomedicine is developing in clusters.In terms of invention patents in biomedicine, the United States, China, Japan, and Europe are the major patent-contributing countries globally, and the clustering effect of their biomedicine industries is becoming increasingly evident.

United StatesAs the global center for biopharmaceutical development, it has established five major biopharmaceutical industry bases including Boston, San Diego, and the North Carolina Triangle. It has achieved comprehensive development and innovation in sub-specialty drug fields such as oncology drugs, immunology drugs, cardiovascular drugs, anti-infective drugs, vaccines, and neurological drugs.EuropeThe biomedical industry cluster has gathered large pharmaceutical enterprises, leading global biotech innovation. It has significant advantages in monoclonal antibody drugs, vaccines, blood products, recombinant protein drugs, gene therapy, and other areas;JapanThere are numerous specialized enterprises, with advantageous fields including regenerative medicine research, drugs for the prevention and treatment of hypertension, diabetes, and tumors;chinaThe biomedical industrial parks are mainly distributed in four regions: the Bohai Rim, Yangtze River Delta, Greater Bay Area, and Chengdu-Chongqing Metropolitan Area. In terms of development characteristics, not only do chemical raw materials drugs and preparations, traditional Chinese medicine, etc., have development advantages, but also cutting-edge technologies such as bispecific antibodies, antibody-drug conjugates (ADCs), and cell gene therapy are also booming.

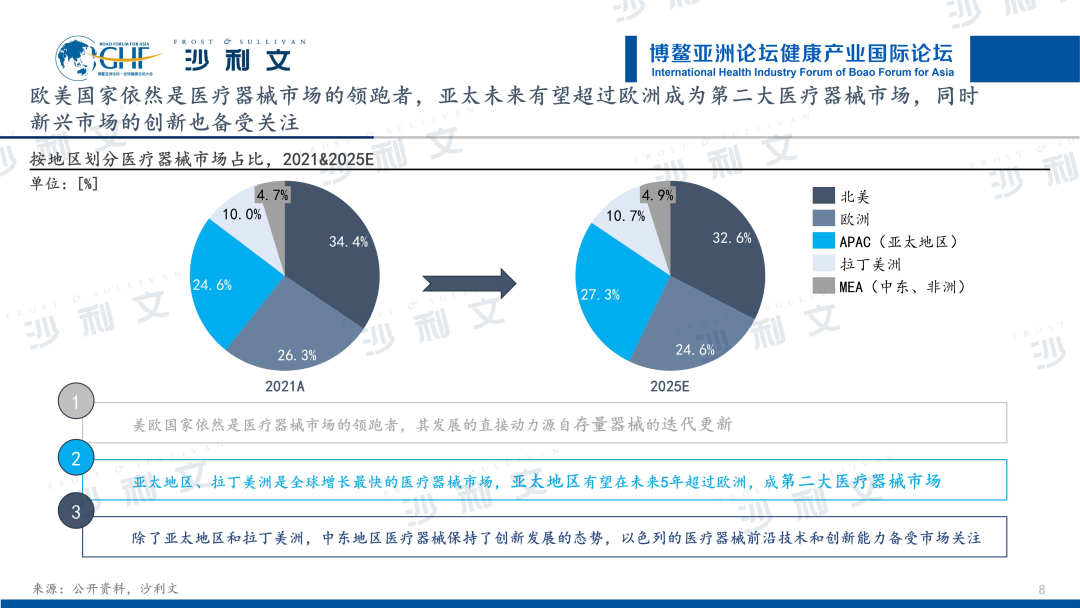

Looking at the global medical device market, European and American countries remain the leaders. Asia-Pacific is expected to surpass Europe as the second-largest medical device market in the future, with innovation in emerging markets also receiving much attention.

In terms of the global market share of medical devices, North America and Europe account for 34.4% and 26.3%, respectively, holding a dominant position in the global market competition landscape. In addition, due to the early start of the medical device industry in European and American countries, mature technological development, high market penetration rates, and an already mature market cycle, the market scale growth rate is stable. Currently, the incremental demand for medical devices mainly comes from the replacement needs of existing devices.

Driven by population changes, economic growth, and the continuously developing healthcare landscape, coupled with rising prevalence of lifestyle-related diseases and growing healthcare demand, Asia-Pacific and Latin America are becoming the fastest-growing medical device markets in the world. In the future, Asia-Pacific is expected to surpass Europe to become the second-largest medical device market.

"In the future, with increasing healthcare spending and insurance coverage rates, as regulatory environments continue to develop, review systems are continuously improved, and innovative technologies are adopted, emerging markets such as China in Asia-Pacific, India, Brazil and Colombia in Latin America will become more attractive, attracting more medical device companies to locate there." Dr. Wang Xin further added."It is worth noting that, in addition to the Asia-Pacific region and Latin America, medical devices in the Middle East have also maintained an innovative development trend. Among them, the cutting-edge technologies and innovation capabilities of medical devices represented by Israel have also attracted much market attention."

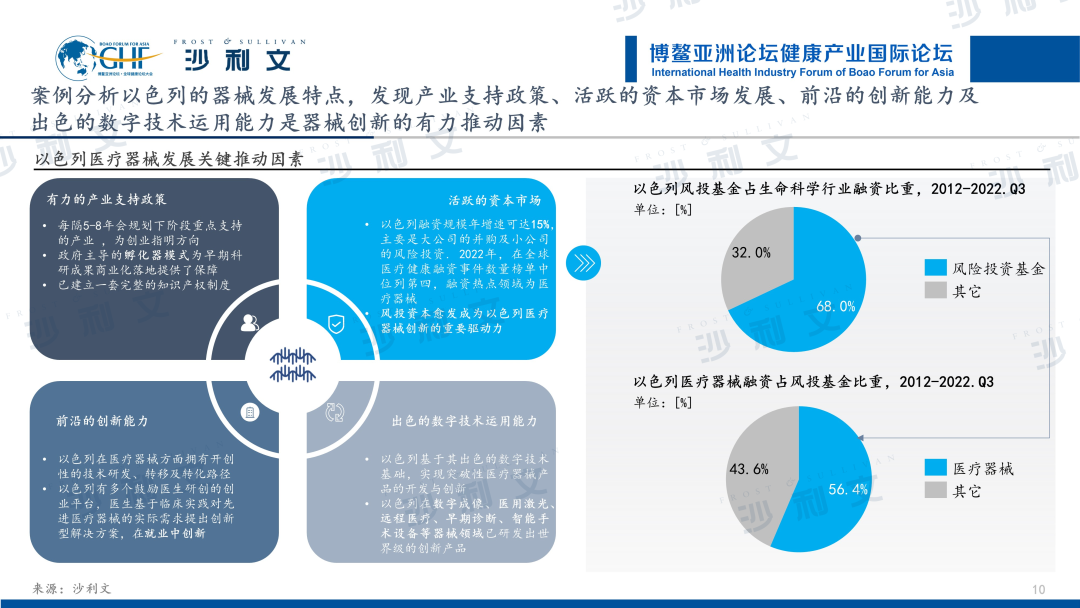

Israel is a small country with scarce resources and a weak industrial chain, but it is renowned worldwide for its strong innovation capabilities and developed high-tech industries. As a globally recognized leader in the field of life sciences, Israel currently has nearly 2,000 life science industry companies. Through a comprehensive review of these enterprises, Frost & Sullivan has found that Israel's life science industry can be divided into four major areas: medical devices, biotechnology, digital health, and pharmaceuticals. The industry focuses on the medical device sector and has significant advantages in medical device innovation. In addition, strong industrial support policies, active capital market development, cutting-edge innovation capabilities, and excellent digital technology application skills are powerful driving factors for Israel's device innovation.

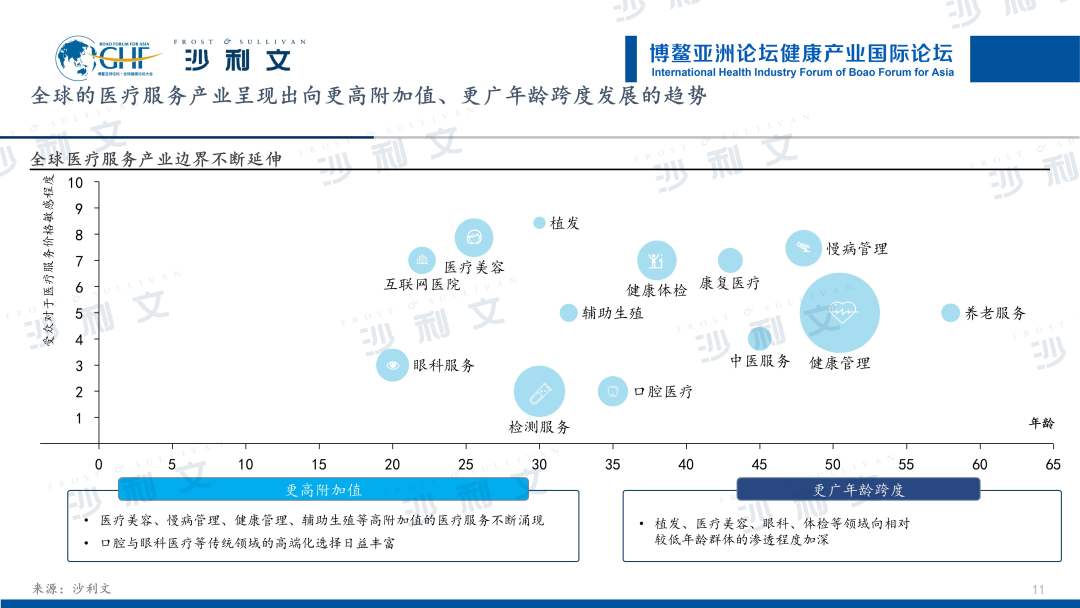

Looking at the global healthcare service sector, the industry is showing a trend towards higher added value and a wider age range of patients.High-value medical services such as medical aesthetics, chronic disease management, health management, and assisted reproduction are emerging continuously. High-end choices in traditional fields like oral and ophthalmic medicine are becoming increasingly abundant. Under the influence of a series of social factors, fields such as hair transplantation, medical aesthetics, ophthalmology, and physical examinations have penetrated deeper into the relatively younger population.

At the same time, medical consumption is shifting from 'subsistence-oriented' to 'expansion-oriented', with service demands derived from 'healthcare' increasing day by day.In the survival phase, medical expenditures are mainly used to cover 'survival-oriented' healthcare costs, such as medications and hospital visits. With the upgrade of 'medical services' consumption, medical spending is no longer limited to the original model. It is gradually shifting from 'survival-oriented' to 'expansion-oriented' consumption. The potential demand in more niche areas such as elderly care, medical aesthetics, ophthalmology, and health management has been further unleashed. The expansion of demand and the empowerment of technology have continuously extended the boundaries of medical services.

In addition, elderly people have an even more urgent need for medical services in the future compared to middle-aged and young adults, especially as the situation of longevity with sub-health in an aging society will become more common.Therefore, the related medical service industries that revolve around the 'silver-haired economy' have broader development prospects, and more market opportunities for emerging niche tracks will emerge.Sub-sectors such as finance, home care, culture, real estate, medical devices, information systems, and education and training are expected to become potential markets for future development.

Finally, Dr. Wang Xin shared Japan's experience in elderly care services through case analysis. The fundamental reason why Japan has internationally leading elderly care services is due to the aging of its population. Japan entered an aging society in 1971 and, after 50 years of development, currently has nearly 30% of its population over the age of 65, ranking first globally. Therefore, Japanese society has carried out age-friendly renovations in medical facilities, medical services, and other aspects, cultivating a large-scale elderly care service industry to ensure social stability.

The advancement of elderly care in Japan is reflected in two aspects: the elderly care system and the elderly care model.In the pension system, to ensure the payment capacity of pensions, Japan adopts the 'three-pillar' model pension system framework, optimizing the composition of insurance benefits to enhance payment capacity. Japanese pensions combine 'public annuities + private annuities' to meet consumers' growing needs for multi-level, high-quality, safe and stable long-term pension security.

At the same time, Japan has ensured the demand for elderly care services through mandatory legal measures. For example, as one of its most important institutional designs, the nursing insurance provides care expenses or services for the elderly who are ill, elderly or have lost the ability to carry out daily life activities. Since Japan began implementing the Nursing Insurance Law in 2000, a large number of enterprises providing home medical devices, rehabilitation equipment, telemedicine, and nursing services have started to offer specialized elderly care services.

In terms of the elderly care model, Japan adopts a 'home-based care as the mainstay, supplemented by institutional care' model. Through refined operations, it ensures that residents are provided for in their old age.Home-based elderly care is Japan's largest segmented market, with as many as 14 types of home care services available in Japan. These include remote medical care, community health, and other services required by elderly people in need of home-based care.

Dr. Wang Xin stated that in the past three years, under a complex investment environment, the industrial landscape has been impacted. In 2020 and 2021, there was a surge in investment enthusiasm. Since 2022, capital investment has tended to favor more certain high-quality targets. It is believed that with the full development of sub-sectors such as biomedicine and healthcare services, there is still tremendous potential for high-quality development in the global healthcare field in the future.

Against this backdrop, Frost & Sullivan, in collaboration with the Organizing Committee of the Boao Forum for Asia Global Health, has jointly released the 'White Paper on the Global Pharmaceutical and Healthcare Industry Layout and Development Trends', aiming to analyze the layout and trends of the global pharmaceutical and healthcare industry and to uncover certainty amidst the uncertainties of global economic development.

"We aim to gain insights into the mechanisms of success and failure by analyzing the industrial layout in the three major sectors of global biomedicine, medical devices, and healthcare services. We will identify focal points for future development within the context of China's industrial operations, thereby exploring feasible directions for promoting orderly and healthy development of industries, achieving autonomous stability in the industrial chain and supply chain, constructing a dual circulation system for domestic and foreign economies, and driving the recovery and prosperity of the world economy," said Dr. Wang Xin.