2021 is the beginning year of the country's 14th Five-Year Plan and also marks a new starting point for the golden decade of the 'Healthy China 2030' strategy. Amid the ongoing two-year rampage of the COVID-19 pandemic, the pharmaceutical and healthcare industry has become a new high ground for global competition. Globally, the number of IPOs in the healthcare industry in 2021 was second only to the technology sector. Domestically, in 2021, a total of 38 pharmaceutical companies successfully listed on the A-share Sci-Tech Innovation Board, far exceeding the 28 companies in 2020 and the 16 companies in 2019. On the Hong Kong Stock Exchange, a total of 20 non-profit biotech companies successfully went public in Hong Kong in 2021, with over 20 healthcare industry companies having submitted IPO applications, more than 90% of which are from mainland China.

Focusing on the key points and difficulties in analyzing the biopharmaceutical investment and financing market, January 20, 2022.Mr. Mao Hua, Partner and Managing Director of Frost & Sullivan Greater China Region, was invited by TBio to share with everyone a summary of the domestic and international biopharmaceutical investment and financing markets in 2021 and future prospects at the TBio's live medical course.

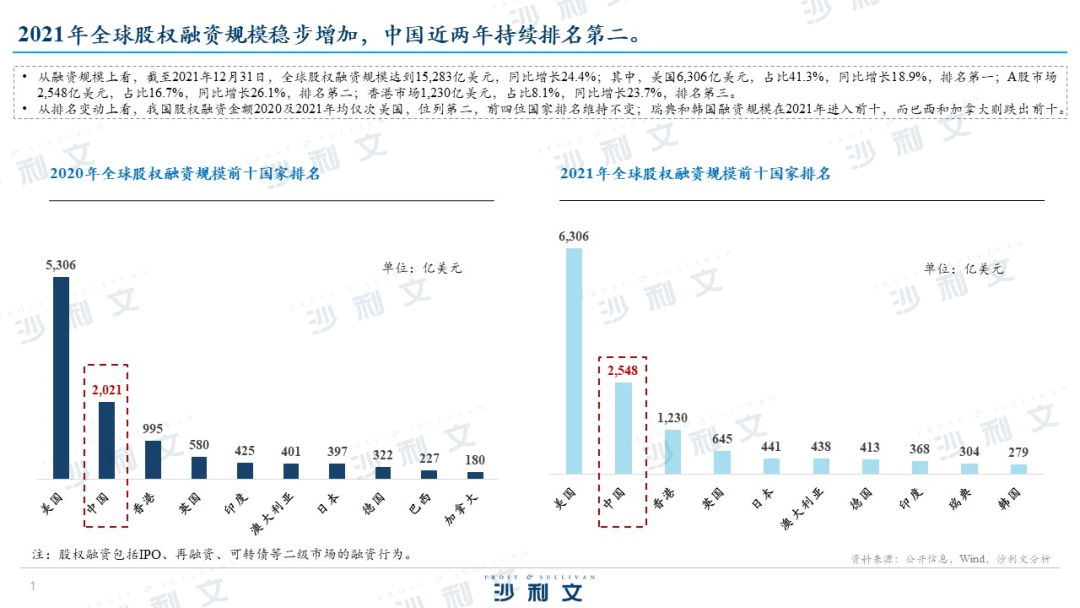

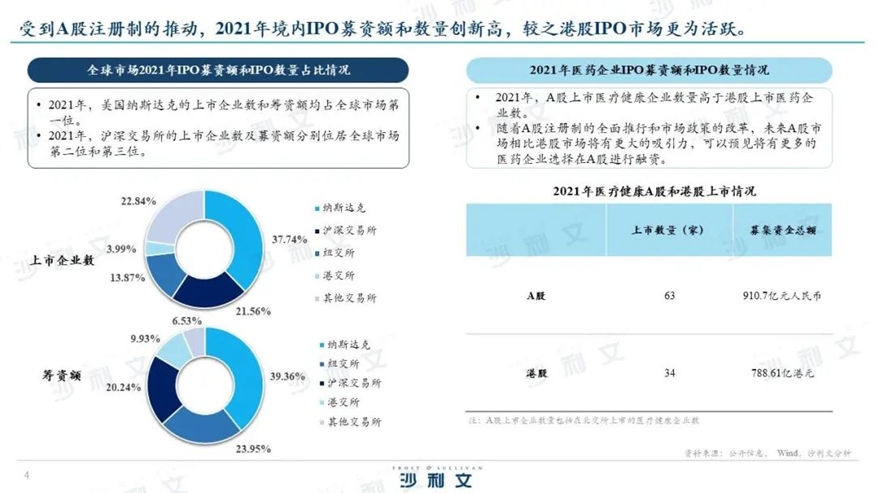

During the live broadcast, Mao Hua first conducted a detailed analysis of the investment and financing status of the global and Chinese biopharmaceutical industries in 2021. He pointed out that the global equity financing scale increased steadily in 2021, with China consistently ranking second over the past two years. In the healthcare sector, between 2020 and 2021, the number of listed companies increased in all major global sectors, with A shares being particularly favored. With the full implementation of the A-share registration system and market policy reforms, the A-share market will have greater attractiveness compared to the Hong Kong stock market in the future, and it is foreseeable that more pharmaceutical companies will choose to raise funds on the A-share market. In the Chinese A-share market, the IPO financing scale and number of IPO companies in the healthcare industry rank third and fifth among all industries, respectively.

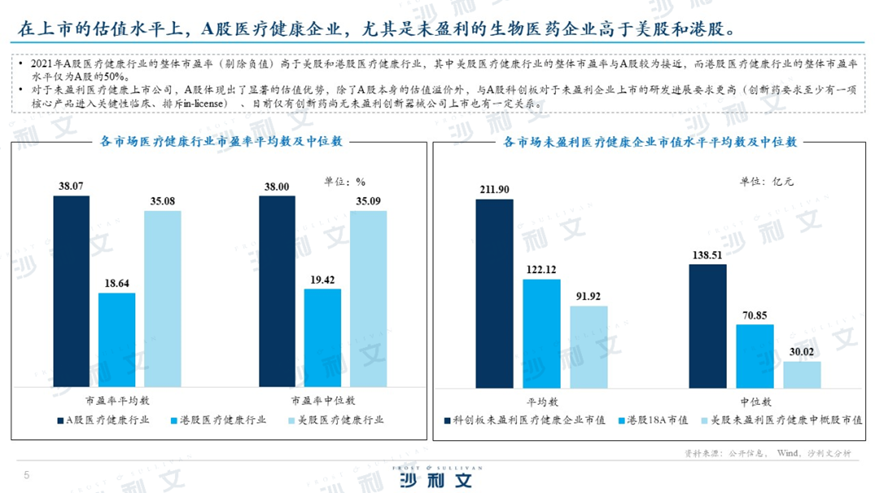

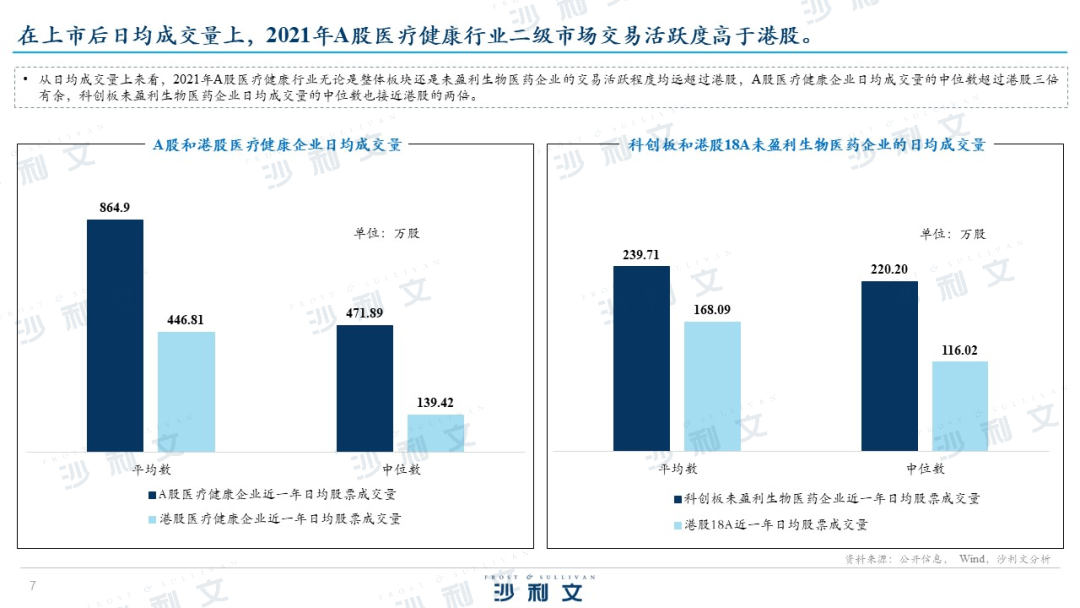

Mao Hua said that in terms of the review process during the listing process, medical and health enterprises vary in procedures and timelines across different sectors. The average number of days for review on the A-share Sci-Tech Innovation Board and Growth Enterprise Market is 300 days and 374 days respectively, far higher than the 128 days on the Hong Kong stock market and the 31 days on the US stock market. Moreover, after the review phase is completed, A-share companies also need to pass a meeting of the Issuance Examination Committee/Listing Committee, making the process more complex. In terms of the valuation level after listing, A-share medical and health enterprises, especially those without profitability, are higher than those on the US and Hong Kong stock markets. Looking at the stock price on the listing day in the second half of the year, Hong Kong-listed unprofitable biotech companies have a high initial-day underpricing rate, accounting for 82% of all initial-day underpricing companies. A-share companies, affected by policies, have seen a reduction in initial-day underpricing; in terms of average daily trading volume after listing, in 2021, the trading activity of the A-share medical and health industry, both as a whole sector and among unprofitable biotech companies, far exceeded that of the Hong Kong stock market.

Mao Hua said that in terms of the review process during the listing process, medical and health enterprises vary in procedures and timelines across different sectors. The average number of days for review on the A-share Sci-Tech Innovation Board and Growth Enterprise Market is 300 days and 374 days respectively, far higher than the 128 days on the Hong Kong stock market and the 31 days on the US stock market. Moreover, after the review phase is completed, A-share companies also need to pass a meeting of the Issuance Examination Committee/Listing Committee, making the process more complex. In terms of the valuation level after listing, A-share medical and health enterprises, especially those without profitability, are higher than those on the US and Hong Kong stock markets. Looking at the stock price on the listing day in the second half of the year, Hong Kong-listed unprofitable biotech companies have a high initial-day underpricing rate, accounting for 82% of all initial-day underpricing companies. A-share companies, affected by policies, have seen a reduction in initial-day underpricing; in terms of average daily trading volume after listing, in 2021, the trading activity of the A-share medical and health industry, both as a whole sector and among unprofitable biotech companies, far exceeded that of the Hong Kong stock market.

According to a survey by Frost & Sullivan, the performance of the primary market in the biopharmaceutical sector is also remarkable both in China and globally. The COVID-19 pandemic has significantly driven investment and financing in the biopharmaceutical field. In 2021, there were a total of 1,273 investment and financing events in the global biopharmaceutical sector, involving a total amount of 369.91 billion yuan, an increase of 31.7% compared to 2020. 'Overall, the enthusiasm for investment and financing in the global biopharmaceutical sector remains at a high speed, with continuous growth in investment and financing amounts and an optimistic growth rate. It is expected that there will be further room for growth in 2022.' Mao Hua further added, 'In addition, within the biopharmaceutical industry chain, investment and financing in downstream pharmaceutical companies dominate, with small molecule and antibody drugs still accounting for the main proportion in China's primary investment and financing market for biopharmaceuticals. Investment and financing growth in innovative biotechnology fields is evident.'

Mao Hua also shared the top cases of pharmaceutical investment and financing in China in 2021 - namely, the listing cases of Aibo Biotech and BeiGene. In August 2021, Aibo Biotech completed a $700 million Series C financing, setting a new record for primary market financing by Chinese pharmaceutical companies. On December 15, 2021, BeiGene was listed on the Sci-tech Innovation Board with a fundraising amount of 222 billion yuan, setting a new record for IPO fundraising by Chinese pharmaceutical companies.

Subsequently, Mao Hua led the audience in a review of the key highlights of the biopharmaceutical market in 2021. Compared to 2020, there were not significant changes in the global top ten best-selling drugs for the first three quarters of 2021. However, affected by the COVID-19 pandemic, Pfizer's COVID mRNA vaccine made it onto the list and topped the chart, surpassing Humira, which had dominated the top spot for many years. Throughout 2021, biotech companies were active in financing, directly promoting R&D investment. Domestic biopharmaceutical companies also continued to increase their R&D investment to support innovation. BeiGene, the first star biotech company to go public on NASDAQ, Hong Kong stocks, and A shares, won the top spot for R&D innovation investment with the ample financial support brought by listing in three markets. At the same time, successful financing activities in both primary and secondary markets greatly fed back into the company's R&D layout, on one hand providing sufficient funds to introduce pipelines; on the other hand, more abundant funds also strengthened internal R&D, with self-developed products yielding results, and the total transaction volume of licensed-out products entering the 2 billion-dollar club.

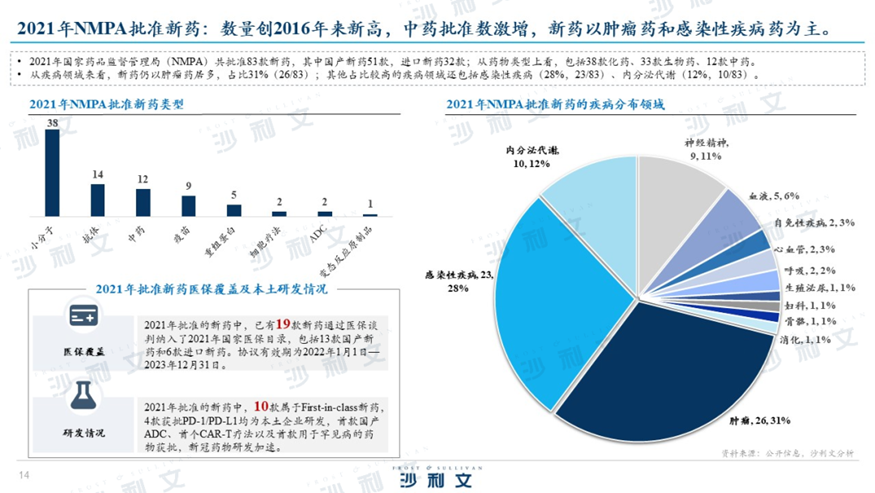

Data shows that in 2021, the National Medical Products Administration (NMPA) approved a total of 83 new drugs, reaching a new high since 2016, mainly including oncology and infectious disease drugs. Among them, there were 51 domestic new drugs and 32 imported ones; in terms of drug types, they included 38 chemical drugs, 33 biologics, and 12 traditional Chinese medicines, with a significant increase in the number of approvals for traditional Chinese medicines.

Data shows that in 2021, the National Medical Products Administration (NMPA) approved a total of 83 new drugs, reaching a new high since 2016, mainly including oncology and infectious disease drugs. Among them, there were 51 domestic new drugs and 32 imported ones; in terms of drug types, they included 38 chemical drugs, 33 biologics, and 12 traditional Chinese medicines, with a significant increase in the number of approvals for traditional Chinese medicines.

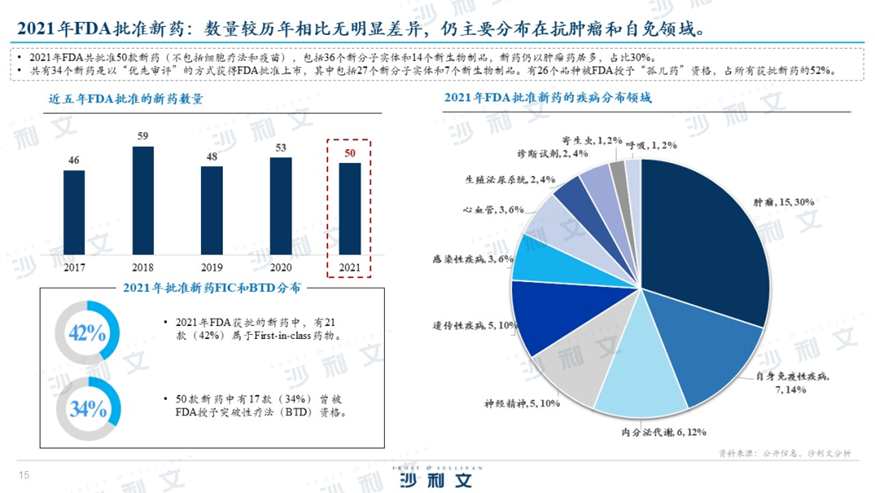

In 2021, the US Food and Drug Administration (FDA) approved a total of 50 new drugs (excluding cell therapies and vaccines), including 36 new molecular entities and 14 new biological products. New drugs are still predominantly oncology drugs, accounting for 30%. A total of 34 new drugs were approved by the FDA for marketing under the 'Priority Review' program, including 27 new molecular entities and 7 new biological products. Twenty-six varieties have been granted the 'Orphan Drug' designation by the FDA, accounting for 52% of all approved new drugs.

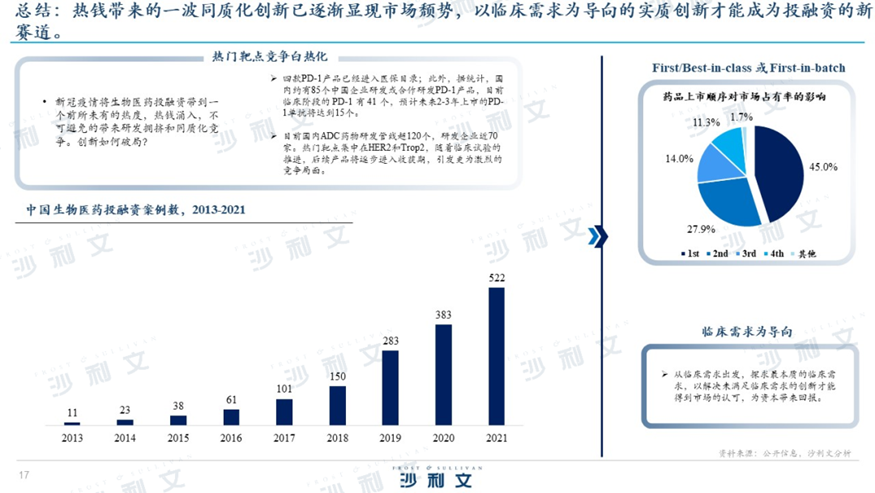

Finally, Mao Hua summarized that the COVID-19 pandemic has brought biopharmaceutical investment and financing to an unprecedented level of enthusiasm. The influx of hot money inevitably leads to crowded R&D and homogenized competition. However, a wave of homogenized innovation brought about by hot money has gradually shown signs of market decline, and only substantial innovation oriented towards clinical needs can become a new track for investment and financing.

"Of course, we can all see that national policies are guiding Chinese pharmaceutical companies towards innovation. Under the policy dividend, the level of domestic innovative drugs is continuously improving, and the R&D level of innovative drugs is growing day by day. On the other hand, the development of COVID-19 vaccines is also driving rapid technological progress in the industry. It is believed that in 2022, China's biopharmaceutical industry will become increasingly integrated into the global innovation pulse," said Mao Hua.