On August 9, 2022, the Hengtai Natural Safety Group's National Dairy Distributor Conference with the theme of 'Perseverance for Innovation' was successfully held. Frost & Sullivanfrost &Mr. Zhang Jian, Partner and Managing Director of Frost & Sullivan's Greater China Region, was invited to attend the conference and delivered a speech on 'Risks and Opportunities in the Catering Industry in the Post-Pandemic Era'.

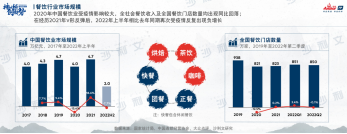

Zhang Jian first introduced the overall development overview of the catering industry to the guests present. He stated that in recent years, the Chinese catering market has shown significant volatility.From 2017 to 2019, the scale of China's catering market increased from 4 trillion yuan to 4.7 trillion yuan, with an increment of 700 billion yuan. After the outbreak of the pandemic in 2020, the overall market size plummeted to the level of 2017. Although there was a V-shaped rebound in 2021, this year, after the Spring Festival, the pandemic has seen nationwide multi-point outbreaks, causing a significant negative impact on the catering market.

At the same time, there are corresponding changes in the number of catering outlets nationwide. The data shows thatIn 2020, the number of catering stores decreased by 12.5% year-on-year, with a total reduction of over 1.1 million outlets. Although the overall market warmed up in 2021 and the first quarter of 2022, data from the second quarter showed that the number of catering stores mirrored the trend of 2020 and experienced a certain degree of decline.

From the perspective of sub-segmenting various catering formats, the impact of the pandemic on catering operations has become evident. The most noticeable change is the development of online channels in the catering industry. Sales of Chinese-style full meals and hot pot catering have seen the greatest growth, both exceedingA 14% increase was seen, with group meals and Chinese-style full-course dining showing the most active momentum in e-commerce channels, achieving growth rates of 4.4% and 3.9%, respectively. However, e-commerce channels account for the smallest proportion among all catering formats and have significant potential for future growth.

From a cost perspective, raw material costs, labor expenses, and rent are the three major burdens of the catering industry. The average proportion of these costs in the industry is as follows: raw materials41.9%, labor 21.4%, rent and property management 11.9%, totaling over 75%. "In a period of relative turmoil in the catering industry, cost reduction and efficiency improvement are propositions that every practitioner must consider," said Zhang Jianshe.

Zhang Jian pointed out that the reduction in passenger flow and the complexity of the catering supply chain are challenges that the entire industry needs to face. Affected by the recurring pandemic, customer traffic at offline dining establishments has significantly decreased. Although the overall consumer market has recovered in the first quarter of this year, the stricter control over dine-in services in Beijing, Shanghai, and their surrounding cities starting from the second quarter has led toIn the first half of 2022, catering consumption as a whole experienced a relatively significant decline.

The challenges of the supply chain stem from numerous links and complex functions, as well as a low coverage rate of cold chain logistics. Compared to mature markets, China's cold chain logistics industry started relatively late and is still in its growth phase. Currently, the infrastructure for cold chain logistics is still relatively weak, and there are certain gaps compared to developed countries such as Europe and America in terms of cold chain logistics facilities and equipment, refrigerated logistics technology and management levels, and overall planning of cold chain logistics.

In the future, the development opportunities for the catering industry are mainly reflected in the following aspects:

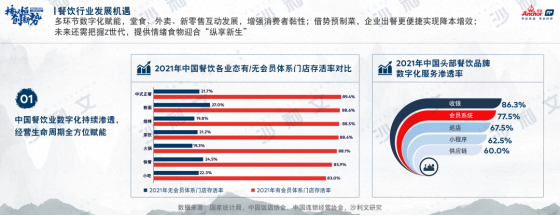

1) Empowering digitalization with multi-ring structures, integrating dine-in, takeout, and new retail for interactive development, thereby enhancing consumer loyalty. According to a survey by Frost & Sullivan,In 2021, the survival rate of various catering stores with a membership system was above 80%, with the average survival rate for full-service, noodle, barbecue, tea, and hot pot restaurants reaching over 88%. Leading catering brands are at the forefront in digital services, achieving penetration rates of 86.3% and 77.5% in cashier and membership system digitization, respectively. Service links such as store visits, mini-programs, and supply chain have achieved a digital penetration rate exceeding 60%.

2) Leveraging the trend of prefabricated dishes, enterprises can provide more convenient meals and achieve cost reduction and efficiency improvement. Based on the cost calculations before and after using prefabricated dishes according to data from the China Hotel Association, it can be seen that although the cost of raw materials has increased slightly after using prefabricated dishes, labor costs have decreased.10%, which ultimately increases net profit margins by 7% after the convenience of meal delivery is achieved.

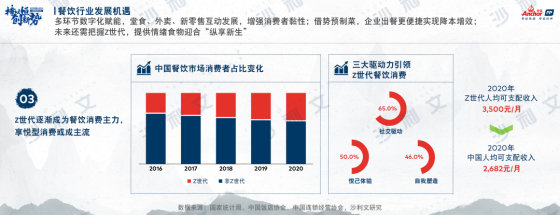

3) Grasp the Z generation and provide emotional sustenance to cater for 'vertical generativity'. The current general trend isThe Z generation is gradually becoming the main force in dining consumption, with a monthly per capita disposable income of 3,500 yuan, far higher than China's average of 2,682 yuan per month in 2020. The dining consumption of the Z generation prefers social-driven consumption, self-pleasing consumption, and self-improvement consumption. In the future, the development of the catering industry can cater to the needs and consumption characteristics of the Z generation and has great potential for growth.

Subsequently, Zhang Jianjian made brief analyses of the baking industry, new-style tea drinks, and the coffee industry respectively.

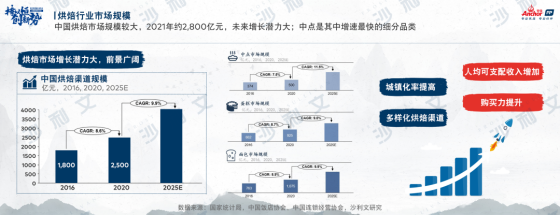

He said that with the upgrading of consumption and changes in consumption habits, China's baking market is currently in a stage of innovative development. The market scale of the baking industry reached approximately 250 billion yuan in 2020 and about 280 billion yuan in 2021. With multiple driving factors such as increased per capita disposable income and purchasing power, urbanization rate, and parallel diversified baking channels, it is expected that the compound annual growth rate of the Chinese baking market will be 9.9% from 2020 to 2025.

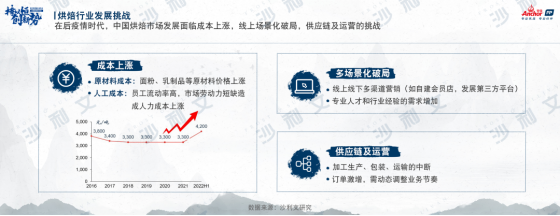

Zhang Jian believes that in the post-pandemic era, the development of China's baking market faces challenges in five aspects: rising costs, breaking through online scenarios, supply chain and operations, homogenization of baked products, and cross-border competition among different business formats.

1) Rising costs: It mainly includes two aspects: raw material costs and labor costs. On one hand, the rising prices of baking raw materials such as flour and dairy products have put pressure on the cost structure of the baking industry. In the future, baking enterprises may face the risk of continuous price increases in raw materials. How to adjust the cost structure and reduce costs while increasing efficiency is a challenge that needs to be addressed. On the other hand, due to the impact of the epidemic, there is high employee mobility and a shortage of market labor force. Therefore, how to reduce labor costs is also one of the challenges that enterprises need to cope with.

2) Online scenario-based breakthroughs: The epidemic has restricted people's travel, so some offline-only stores are urgently facing transformation and engaging in multi-channel marketing online and offline. This transformation requires experienced leaders and professionals to complete, so how to effectively break through this online scenario-based situation is a problem that needs to be solved.

3) Supply Chain and Operations: The emergence of the pandemic has increased the uncertainties faced by the baking industry. For example, travel restrictions may lead to different limitations and interruptions in raw material processing, production, packaging, transportation, etc. Residents are stockpiling goods frantically, and businesses will face a surge in orders. How to dynamically adjust business rhythms and how to accelerate production while ensuring product quality under supply-demand imbalances is a challenge that baking enterprises need to face.

4) Homogenization of baked products: Due to the limited variety of baked products, when a market hit product becomes popular, other brands will also start to refer to it for research and development and conduct market promotion. As an emerging track, capital is avidly chasing it, and many brands are vying to enter the market, which poses higher demands on differentiated product research and development. How to explore new flavors, textures, and tastes, and create differentiated products is one of the main challenges that baked enterprises will face in the future.

5) Cross-border competition among different business formats: Baking enterprises not only face competition within the industry but also competition from industries such as tea drinks, coffee, and catering. Currently, there has gradually formed a trend where baking products are paired with other food and beverages. In this context, traditional baking stores will be diverted by different business formats, leading to a decline in customer traffic. Therefore, how baking enterprises can still explore competitive paths amidst multiple pressures is one of the challenges for the future.

"Although the baking industry faces the challenges mentioned above, opportunities and challenges coexist. There are mainly four major opportunities that support the innovative development of the baking industry," said Zhang Jian.

1) Digital Marketing: After the pandemic, some companies specializing in offline stores began to layout their online digital transformation, launching online ordering services across platforms such as official accounts, mini-programs, social e-commerce, and comprehensive e-commerce. Although offline stores face a painful period of online transformation, with the rapid development of digitization, consumers have already developed online consumption habits. Therefore, achieving parallel development of both online and offline channels will become an opportunity for baking companies.

2) Baking + X Scene Fusion: Under the current trend of consumer scenarios, it is inevitable that baking enterprises will face competition from other business formats. Baking enterprises need to proactively expand their consumer scenarios, tap into potential consumers, and integrate and innovate in product innovation, supply channels, brand operations, and more.

3) Innovative R&D: Frost & Sullivan believes that baking companies that innovate and develop in line with market trends will see rapid development. As consumers' experience and demand for consumption continue to rise, diversification, healthiness, mini-packaging snacks, retailization, and fun are industry trends.

4) Milk Fat Upgrade: The outbreak of the pandemic has made consumers pay more attention to health, prompting businesses to upgrade their dairy fats. For example, replacing plant or mixed fats with healthier animal fats, or increasing the proportion of milk fat in dairy fats, can all improve the taste of baked products.

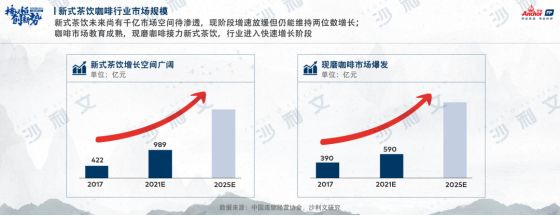

According to Zhang Jian,2016 was a breakout year for the development of new-style tea drinks. In 2017, the market scale of new-style tea drinks reached 422 billion yuan, rapidly climbing to around one hundred billion yuan by 2021, achieving an extremely high annual compound growth rate. Although the growth momentum of new-style tea drinks has slowed down at this stage, it can still maintain a double-digit growth rate. In 2020, freshly ground coffee took over from the rapid development of new-style tea drinks. That year, capital quickly completed investment layouts, and a number of well-known coffee brands emerged in the industry, such as Tims, Manner, Seesaw, Mstand, etc. The market scale also increased from 39 billion yuan in 2017 to 59 billion yuan in 2020.

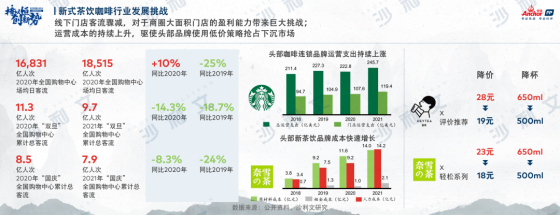

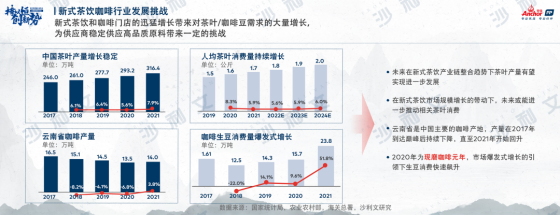

Zhang Jian pointed out that the new-style tea and coffee market also faces many challenges:1) The sudden decline in offline store traffic poses a significant challenge to the profitability of large-area stores in business districts; (2) Operating costs continue to rise, forcing leading brands to adopt low-price strategies to capture the lower-tier market; (3) The rapid growth of new-style tea and coffee stores has led to a substantial increase in demand for tea/coffee beans, posing certain challenges to suppliers' stable supply of high-quality raw materials; (4) In the early stages, new-style tea stores expanded their channels by upgrading to use light cream + cream cheese + fresh fruits. However, as the industry matures and competitors continue to pour in, product homogenization is severe, and differentiated competition has weakened.

The development opportunities for the new-style tea and coffee industry mainly focus on digital empowerment and industrial chain integration. Zhang Jian further explained that digital empowerment for the business operations of new-style tea beverage brands is the result of the integration of online and offline services in the context of big data era. Digital operations have become a key aspect for leading new-style tea beverage brands."The new ace." And industrial chain integration allows new tea drink brand owners to continuously extend upstream in the supply chain, control upstream production, and standardize the quality and standards of the industrial chain; establish supply chain advantages to support the brand's scaled expansion and rapid product innovation; simplify the supply chain circulation path and reduce supply chain management costs.

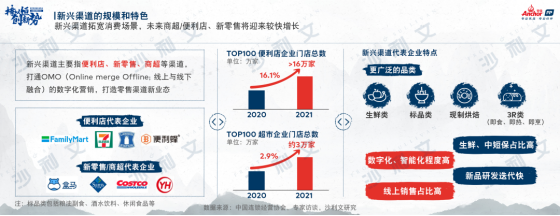

In recent years, emerging channels have emerged. Emerging channels mainly refer to convenience stores, new retail, supermarkets, etc., and are being integrated.OMO (OnlinemergeOffline: Digital marketing that integrates online and offline channels to create new retail formats. According to data from the China Chain Operation Association, despite the impact of the COVID-19 pandemic, the number of stores in the industry has still achieved relatively stable growth. In 2021, the total number of stores of the top 100 convenience store enterprises exceeded 160,000, a year-on-year increase of 16.1%; in 2021, the total number of stores of the top 100 supermarket enterprises was about 30,000, a year-on-year increase of 2.9%. Emerging channel enterprises are characterized by a wider range of categories, a high proportion of fresh and medium- to short-term products, a high degree of digitization and intelligence, rapid new product research and iteration, and a high proportion of online sales.

The development of emerging channels faces three major challenges: inventory and supply chain management, high operating costs, and fierce regional competition. In terms of inventory and supply chain management, the pandemic has had a significant impact on production and logistics. The epidemic has sounded an alarm for businesses, and how to identify and resolve potential risks in the supply chain in the post-pandemic era is something that enterprises need to pay attention to. In terms of operating costs, in addition to rising raw material and labor costs, emerging channels are also facing increases in marketing and advertising costs. Therefore, how to optimize the value chain and reduce costs is also a problem that emerging channels need to solve in the future. In terms of regional competition, emerging channels also face challenges of homogenization. It is difficult to develop new products, and creating hit products is even more challenging. Therefore, avoiding fierce regional competition and highlighting brand personalization are also challenges that enterprises need to face in the future.

In the future, emerging channel enterprises can focus on digital applications, self-developed products, and cross-border collaborations. Digitalization and intelligentization are comprehensively deployed to empower customers with full lifecycle management, build user profiles, and ensure regionalized and personalized R&D and product promotion. On the basis of establishing its own brand, it has joined hands with leading brands such as baking, tea, and coffee. In addition, the leading effect in new retail and convenience stores has already taken shape. The explosive promotion of top enterprises drives imitation by mid-tier businesses in the market. Enterprises with a leading effect can embrace new development opportunities and lead market development.

In summary, the sudden decline in store traffic, imperfect supply chain, increased costs, and product homogenization are common problems faced by the entire catering industry. In the future, businesses can focus on multiple aspects:1) Empowering through digitization, strengthening online operations to improve efficiency and customer experience; (2) Advancing both online and offline efforts, broadening consumption scenarios, and creating differentiated scenarios and brand cultural outputs; (3) Innovating product research and development to meet consumers' diverse, healthy, and retail-oriented needs.

"The data shows that in the first half of 2022, among new consumer financing transactions, large catering consumption accounted for more than 41%, indicating that consumer financing has returned to rationality, with catering and food still being the top sectors," said Zhang Jian.